2026 Guide: How to Prequalify for a Mortgage Loan Online?

I remember the first time I thought about buying a home. I spent nights scrolling through listings, falling in love with kitchens and backyards, only to realize I had absolutely no idea if I could actually afford them. It's a common trap: we shop for the house before we shop for the money.

In 2026, the first step isn't calling a realtor. It's getting prequalified. It answers the scary question, "How much can I borrow?", without wrecking your credit score. Fortunately, technology has evolved. You no longer need to walk into a bank branch. You can now use free online tools to instantly consult with local loan officers and get your numbers straight from the comfort of your couch.

What is a Mortgage Prequalification?

Think of a mortgage prequalification as a "financial health checkup" or a snapshot of your buying power. It is an estimate of how much a lender might be willing to lend you based on the financial information you provide.

The outcome of this process is a Prequalification Letter. While this letter isn't a guaranteed loan offer, it's a powerful tool. You can show it to real estate agents to prove you are a serious buyer, not just a window shopper.

Crucially, prequalification is usually based on self-reported data. You tell the lender your income and debts, and they give you an estimate. Because the lender isn't doing a deep dive into your documents yet, it's fast, free, and typically doesn't damage your credit score.

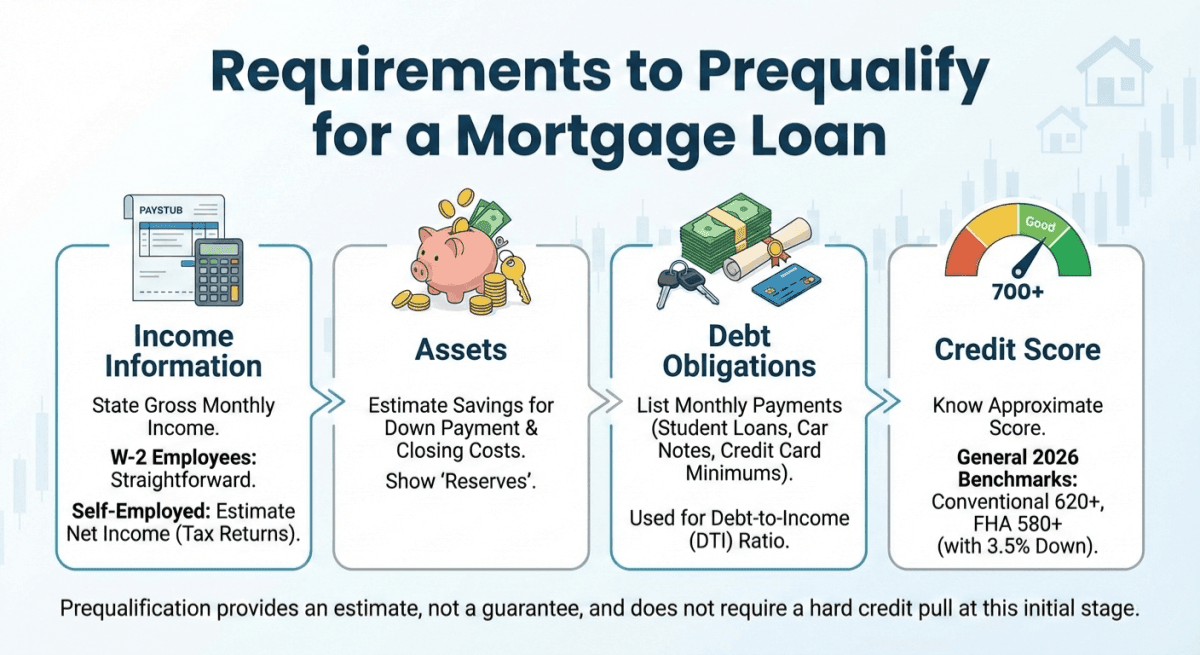

Requirements to Prequalify for a Mortgage Loan

Even though prequalification is preliminary, the accuracy of your result depends entirely on the accuracy of the information you provide. If you guess your income, your prequalification letter won't be worth the paper it's printed on.

Here is what you need to have ready to get an accurate number:

-

Income Information: You'll need to state your gross monthly income. If you are a W-2 employee, this is straightforward. If you are self-employed, you'll need to estimate your net income based on tax returns.

-

Assets: Have a rough idea of your savings for a down payment and closing costs. Lenders want to see that you have "reserves."

-

Debt Obligations: Be honest about your monthly payments, student loans, car notes, and credit card minimums. This is used to calculate your Debt-to-Income (DTI) ratio, a metric lenders rely on heavily.

-

Credit Score: While you don't need a hard credit pull yet, you should know your approximate score. In 2026, most Conventional loans require a score of 620+, while FHA loans can go as low as 580 with a 3.5% down payment.

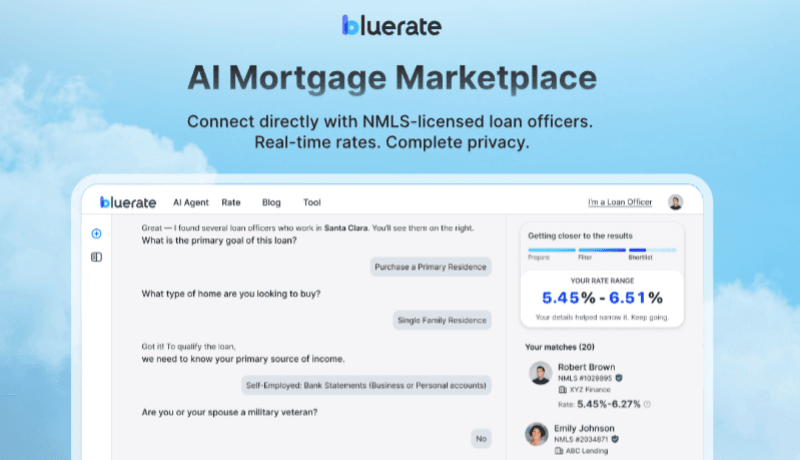

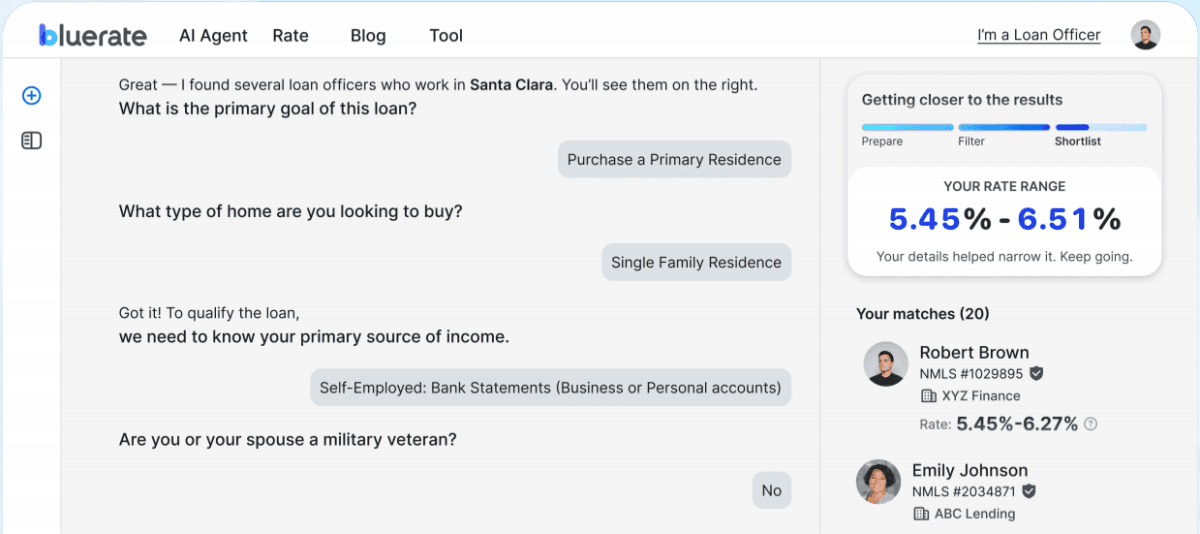

How to Get Prequalified for a Mortgage via Bluerate?

One of the biggest complaints I hear from homebuyers is the "spam nightmare." You fill out a form online to see rates, and suddenly your phone rings off the hook with aggressive salespeople.

This is why I recommend using Bluerate. It's a marketplace that connects you with local Loan Officers, but it puts you in control. Instead of selling your data to the highest bidder, Bluerate uses an AI-driven approach to match you with the right expert for your specific situation, privately.

Why Bluerate stands out in 2026:

-

Bluerate AI Agent: It's like having a mortgage pro in your pocket. The AI analyzes your profile to find matches, not just random lenders.

-

Privacy First: This is huge. You connect securely without your data being sold to spammy marketing lists.

-

Local Expertise: Real estate is local. The platform connects you with NMLS-licensed officers nearby who understand your specific market (whether you need FHA, VA, or Conventional).

-

Real-Time Comparisons: You can compare personalized rates from over 100 lenders instantly to ensure you aren't overpaying.

-

Fast Track: Their system is designed to get you pre-qualified up to 2.5x faster than traditional methods.

-

No Random Assignments: You choose the loan officer you want to work with based on their ranking and profile.

How to use the Bluerate AI Agent:

-

Start the Chat: Click the "Chat with AI" button on the homepage.

-

Share Your Goals: The AI Agent will ask simple questions about your target Location, Property Type (e.g., Single-Family), and estimated Credit Score.

-

The "Prepare-Filter-Shortlist" Magic: The AI processes your answers to filter out lenders who can't help you and shortlists the ones who can.

-

Review Rankings: You'll see a ranked list of Loan Officers with a "Match Score" showing how well they fit your needs, along with their current rates.

-

Connect: Pick the one you like and start the conversation securely.

Prequalify vs Pre-Approval for Mortgage

These two terms get used interchangeably, but they are completely different beasts. Confusing them can actually cost you a house in a competitive market.

Here is the breakdown:

-

Verification: Prequalification is based on what you tell the lender (verbal/self-reported). Pre-Approval requires proof. You have to submit W-2s, bank statements, and tax returns, which an underwriter verifies.

-

Credit Impact: Prequalification is usually a Soft Pull (no impact on your score). Pre-Approval almost always requires a Hard Pull (temporary dip in score).

-

The "Weight": A Prequalification letter is good for starting your search. A Pre-Approval letter is a conditional commitment to lend. When you make an offer on a house, sellers basically require a Pre-Approval; a simple prequal often isn't strong enough to win a bidding war.

Get prequalified now to set your budget. Get pre-approved later, right before you are ready to tour homes with an agent.

People Also Read:

- Detailed Guide: How to Get Preapproved for a Mortgage Loan?

- Must-Read: How Long is a Mortgage Preapproval Good for?

- Mortgage Prequalification vs Preapproval: All Differences

FAQs About Prequalifying Mortgage

Q1. How long to get prequalified for a mortgage loan?

It's incredibly fast. If you use an online tool like Bluerate, you can get prequalified in minutes. If you go to a traditional bank branch, it might take a standard meeting, but the online route is instant 24/7.

Q2. Does getting prequalified for a mortgage hurt your credit?

Generally, no. Most modern online prequalifications use a Soft Inquiry, which does not affect your credit score. However, always double-check with the specific lender or platform before submitting to be sure they aren't running a "Hard" check.

Q3. How much can I get prequalified for a mortgage?

This depends heavily on your Debt-to-Income (DTI) ratio. Lenders typically follow the "28/36 rule", spending no more than 28% of your gross income on housing and 36% on total debt. However, FHA loans can sometimes allow DTIs up to 43% or even 50% in certain cases.

Q4. Can you get prequalified for a mortgage online?

Yes, and it is the preferred method in 2026. Platforms like Bluerate allow you to handle the entire initial process online, checking rates and matching with officers, without leaving your home.

Q5. What credit score do you need to prequalify for a mortgage?

It varies by loan type. For a Conventional loan, you typically need at least a 620. For an FHA loan, you can qualify with a 580 (with 3.5% down). If your score is lower, you might still qualify but will need a larger down payment.

Final Word

Buying a home is a marathon, not a sprint, and prequalification is your starting line. It removes the mystery from the process and gives you a clear price range so you don't waste time looking at homes that don't fit your budget.

Don't let the fear of complex math or awkward phone calls stop you. The tools available in 2026 make this step easier and more private than ever before.

Ready to see your real options? You can chat with Bluerate AI Agent right now. It's free, private, and will help you find top-rated local loan officers and compare accurate rates in just a few minutes, without the spam.