![[2026 Guide] 6 Best AI Mortgage Underwriter Software to Pick](/_next/image?url=https%3A%2F%2Fdynamic-light-ab6e2536d6.media.strapiapp.com%2Fai_mortgage_underwriter_software_banner_b2406625c0.png&w=3840&q=75)

[2026 Guide] 6 Best AI Mortgage Underwriter Software to Pick

Having spent years analyzing mortgage applications, I know the headache of endless guideline updates and complex calculations. Today's high-pressure market demands tools that simplify our desks rather than complicate them. That is why I have evaluated the current landscape of AI underwriting software.

For those needing an efficient, highly cost-effective assistant to verify guidelines, calculate income, match Down Payment Assistance (DPA) programs, and streamline loan origination, Zeitro has quickly become my go-to recommendation.

Takeaways

Before we jump into the individual reviews, here is a quick summary of what I consider when evaluating AI mortgage underwriting software. Through trial and error, I have learned that the best tool depends on where your business faces its biggest bottlenecks.

-

Workflow Match: Choose between front-end document collection, automated guideline search, or official automated underwriting systems (AUS).

-

Compliance and Citations: In our industry, an AI tool must prove its answers. Always look for systems that back their guidelines with verifiable sources to avoid audits.

-

Cost vs. ROI: Balance heavy enterprise platforms against lightweight, high-yield solutions that save hours without draining your budget.

-

Specialization: Ensure the platform handles your specific mix of conforming, Jumbo, and alternative Non-QM loan types.

6 Top AI Software for Mortgage Underwriter in 2026

In my search for the best platforms, I categorized these tools by their practical roles in the lending pipeline. Here are the six best software solutions that have proven most effective for modern mortgage professionals.

#1 Zeitro

Best for: Best value-for-money AI mortgage assistant for quick guideline lookups, Non-QM pricing, and income calculations.

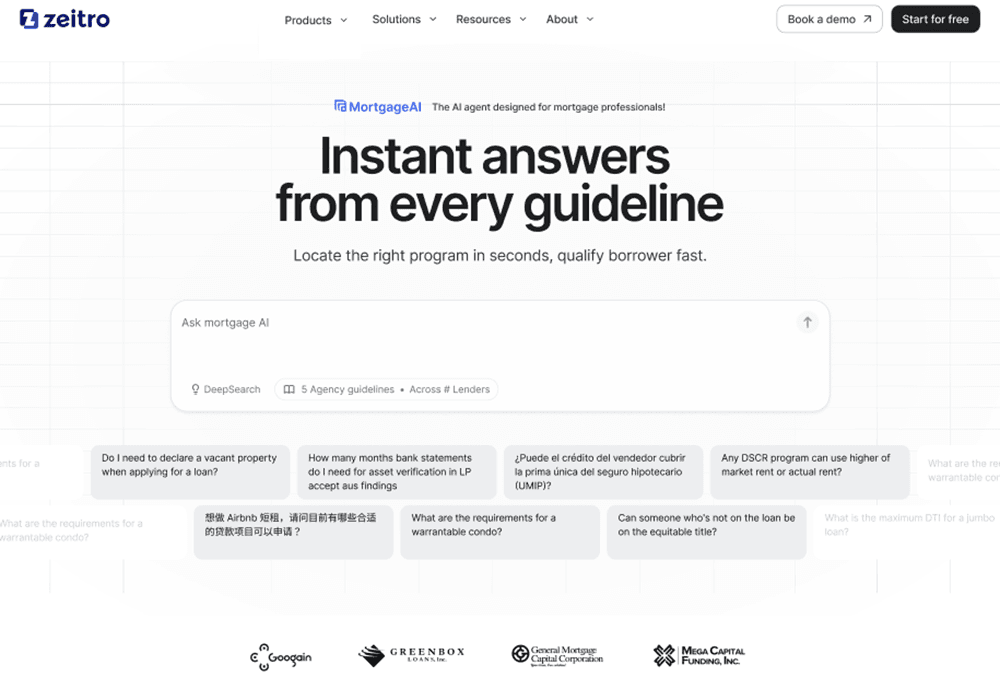

I have used Zeitro extensively to tackle the complexity of alternative lending. Designed for US mortgage professionals, it acts as a dedicated AI agent. Its Zeitro Strata AI is particularly impressive, allowing underwriters and loan officers to search through more than 1,000 guidelines from over 100 lenders in seconds.

Rather than manually digging through endless PDFs for non-conforming or DSCR programs, you can ask specific questions and get clear, documented answers. It also features a digital 1003 point-of-sale (POS) system, instant DTI calculations, and a built-in pricing engine to streamline the pre-qualification phase.

Pros:

-

Cuts down manual guideline research from thirty minutes to just a few seconds.

-

Provides source citations for every answer to prevent AI hallucinations and simplify audits.

-

Offers a versatile feature set including bank statement income calculations and DPA program matching.

-

Extremely budget-friendly with a freemium tier and plans starting at $8 per month.

-

Saves underwriters and account executives an average of 18+ hours per month.

Cons:

-

The "Explain" function consumes a query credit, which can limit free tier users.

-

Being a newer tool, some highly niche secondary market investor guides are still being added.

#2 Floify

Best for: Streamlining front-end borrower portals and automating document collection workflows.

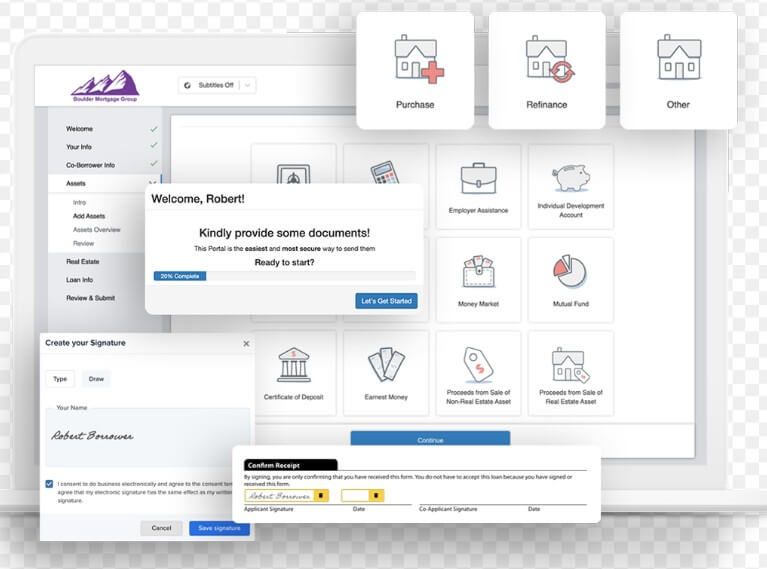

If your biggest bottleneck is chasing down borrowers for bank statements or W-2s, Floify is a tool I highly recommend. It excels at the point-of-sale (POS) stage.

With its recent updates, Floify has embedded more AI features, allowing applicants to upload financial documents while the system can extract data from uploaded documents and assist in populating the 1003 form, depending on LOS integrations and configuration, and flags missing files. It does not replace your primary loan origination system (LOS), but it acts as a highly organized digital bridge between the borrower and the underwriter.

Pros:

-

Outstanding borrower user experience that simplifies document upload and signing.

-

Automated document classification and data verification reduce manual data entry by over 50%.

-

Integrates smoothly with industry-standard platforms like Encompass and Byte Software.

-

Reduces overall desk time spent on administrative back-and-forth communication.

Cons:

-

Fewer deep-dive underwriting analysis features compared to dedicated guideline or decision engines.

-

Pricing can scale up quickly for larger teams compared to simple helper tools.

#3 FundMore.ai

Best for: Cloud-native automated pre-funding risk assessment and automated underwriting.

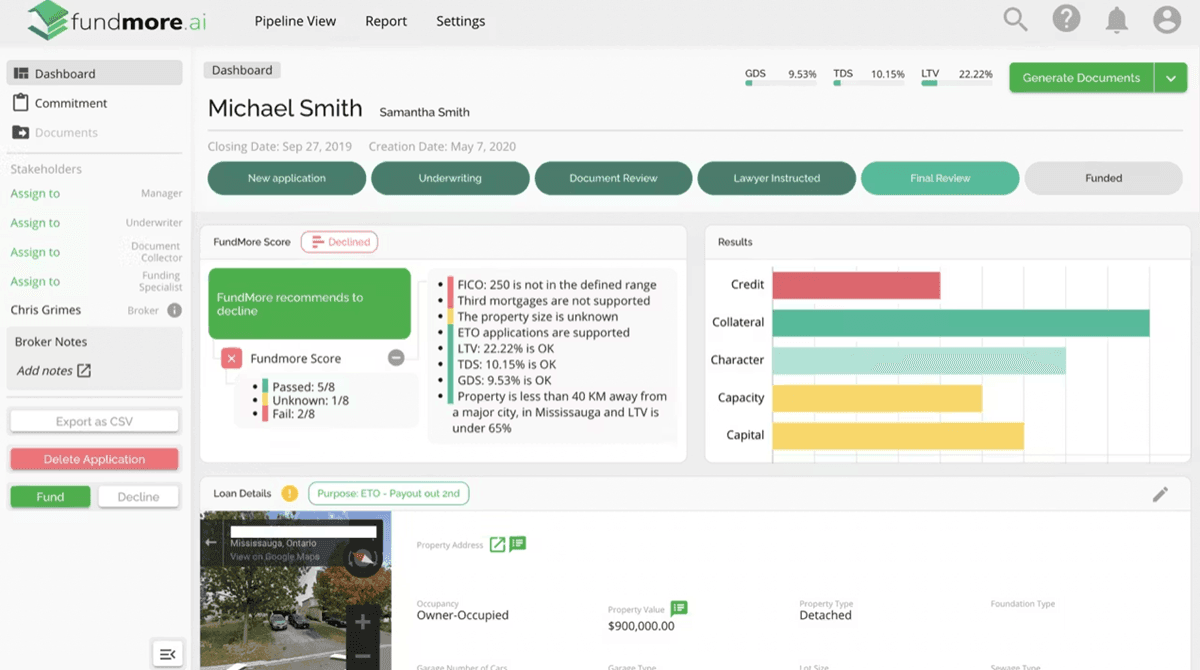

FundMore.ai is a cloud-based solution that aims to shorten the path to clear-to-close through computer-aided underwriting. I appreciate how it uses pattern recognition and machine learning to analyze credit risk, property collateral, and fraud factors before the loan hits the final approval stage.

This pre-funding verification reduces overall cycle times, making it a strong option for mortgage operations looking to standardize their risk management without relying entirely on manual checklists.

Pros:

-

Highly effective predictive models that catch underwriting errors before secondary market submissions.

-

Can significantly reduce pre-funding review time, depending on implementation and workflow efficiency.

-

Offers an intuitive dashboard with clear compliance audit trails.

-

Highly customizable rule sets to match your organization's specific risk tolerance.

Cons:

-

Mainly optimized for North American institutional lenders, with historically stronger traction in Canada.

-

The enterprise-level pricing model is too steep for independent loan officers or small brokerages.

#4 Fannie Mae Desktop Underwriter (DU)

Best for: Standard automated risk assessment and eligibility decisions for conforming conventional loans.

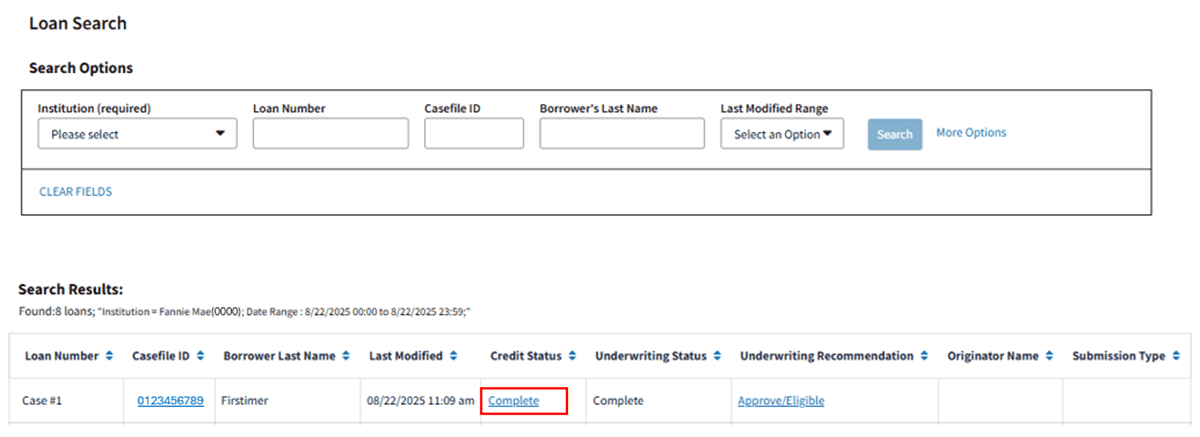

No review of underwriting software is complete without mentioning Desktop Underwriter. As the industry standard for conventional conforming mortgages, DU is a system I rely on for official loan eligibility. Once the 1003 loan application data is complete, DU runs complex algorithms to issue an Approve/Eligible or Refer/Eligible finding. It is the standard tool used when selling conforming loans to Fannie Mae and is required in most cases.

Pros:

-

The undisputed gold standard of credibility for conforming conventional loans, with integrations that support FHA and VA risk assessment through their respective agency systems.

-

Instantly updated with the latest regulatory changes and loan limits.

-

Deeply integrated into almost every loan origination system on the market.

Cons:

-

Extremely rigid. It offers zero flexibility for Non-QM, DSCR, or private portfolio loans.

-

Cannot handle conversational Q&A searches. You must fully input a loan file to receive feedback.

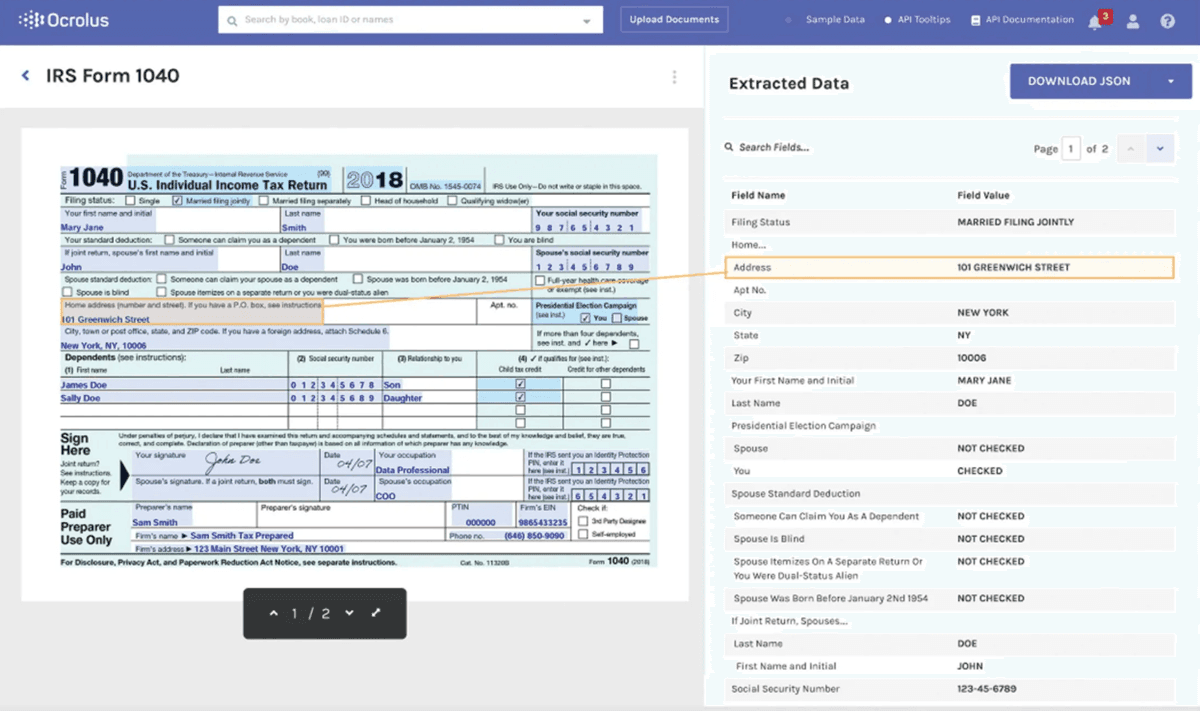

#5 Ocrolus

Best for: Precise AI document data capture and automated underwriting conditioning.

Ocrolus has been a game-changer for my team when dealing with paper-heavy files. It specializes in intelligent document processing, taking messy bank statements, pay stubs, and tax returns and turning them into accurate digital data.

Recently, they introduced an automated conditioning engine. This feature automatically identifies and tracks underwriting conditions directly within the platform, making it much easier to clear conditions quickly and maintain clean compliance audits.

Pros:

-

Extremely high accuracy in extracting data from unstructured financial documents.

-

Automated conditioning saves processors and underwriters from manually matching documents to open conditions.

-

Excellent fraud detection features that easily spot altered bank statements.

-

Integrates deeply with major LOS platforms like Encompass.

Cons:

-

Strictly focused on document processing and data extraction, rather than product pricing or guideline lookups.

-

The usage-based pricing structure can become expensive during peak volume seasons.

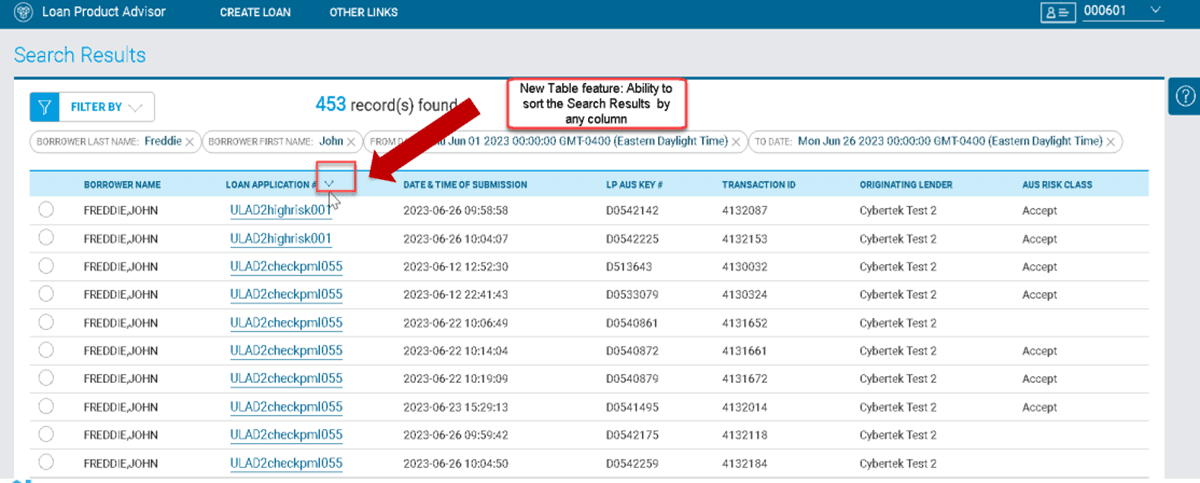

#6 Freddie Mac Loan Product Advisor (LPA)

Best for: Automated underwriting and credit risk evaluation for Freddie Mac eligible loans.

Similar to Fannie Mae's DU, Freddie Mac's Loan Product Advisor (LPA) is a cornerstone of my daily underwriting toolkit. It evaluates loan files against Freddie Mac's specific selling guidelines to determine credit risk and eligibility. LPA is highly valued for its asset and income modeler integrations, which allow underwriters to verify borrower details electronically, reducing the need for physical paperwork.

Pros:

-

Essential for selling conventional loans to Freddie Mac.

-

Direct third-party integrations speed up the asset and income verification process.

-

Provides clear, structured feedback on what is required to secure approval.

Cons:

-

Entirely restricted to Freddie Mac's specific, conforming parameters.

-

Does not assist with alternative, non-conforming, or creative portfolio lending guidelines.

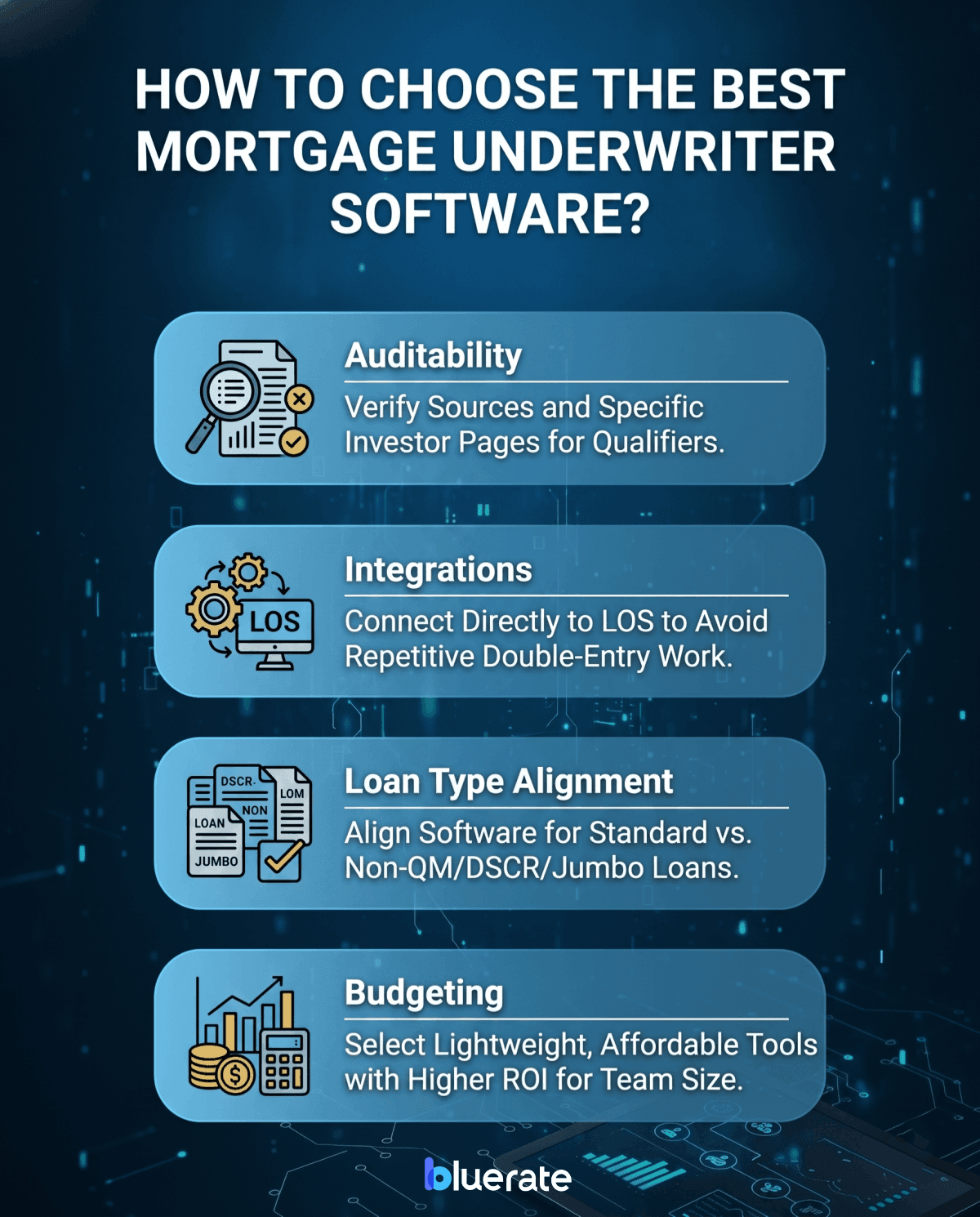

How to Choose the Best Mortgage Underwriter Software?

In my experience, no single piece of software does it all. A balanced mortgage shop often needs a combination of tools. Here is how I suggest choosing the best fit for your workflow:

-

Auditability: Always ensure your AI tool cites its sources. If an assistant tells you a borrower qualifies for a 1099 program, you must be able to verify that specific investor page instantly.

-

Integrations: Look for software that connects directly with your existing Loan Origination System (LOS) to avoid repetitive double-entry work.

-

Loan Type Alignment: If you primarily write Fannie and Freddie loans, stick to standard AUS tools. However, if you write Non-QM, DSCR, or Jumbo loans, an AI guideline assistant is indispensable.

-

Budgeting: Do not buy heavy, enterprise-level document processing platforms if you are a small team. Lightweight, affordable tools often yield a much higher ROI.

FAQs About AI Mortgage Underwriter Software

Q1. Can AI software completely replace human mortgage underwriters?

In my view, absolutely not. AI excels at processing repetitive tasks, extracting document data, and scanning thousands of pages of guidelines in seconds. However, underwriting often requires analyzing compensating factors and making complex risk decisions that a machine cannot replicate. AI serves as an incredibly useful assistant, not a replacement.

Q2. How do AI guideline assistants like Zeitro handle shifting Non-QM guidelines?

Non-QM guidelines change frequently based on investor demand. Systems like Zeitro address this by pulling directly from updated investor databases and providing exact source citations. This lets you cross-reference any answer against the source document to ensure accuracy before making a decision.

Q3. Is my borrower's sensitive financial data secure in these AI systems?

Yes, security is a major focus for reputable mortgage technology. Look for software that maintains SOC 2 Type II compliance and adheres to financial privacy laws like GLBA. These systems secure data in transit and at rest, and do not use your borrowers' private details to train public models.

Q4. What is the difference between an AUS like DU and an AI assistant?

An Automated Underwriting System (AUS) like DU or LPA provides a standardized credit risk assessment and eligibility recommendation, which must still be validated by a human underwriter. An AI assistant like Zeitro is a conversational tool that helps you search guidelines, run pre-qualifications, and calculate parameters before submitting the loan to the AUS.

Q5. Can AI software accurately calculate income for complex self-employed borrowers?

Yes, to a great extent. Advanced tools use specialized OCR and financial analysis to parse tax returns, Profit & Loss statements, and bank statements. While they achieve high accuracy, I always recommend a quick human review to verify the final calculations for complex cases.

Final Word

Choosing the right technology can make a massive difference in your daily workload. Over the years, I have seen many tools promise to solve every underwriting problem, but the most effective approach is to select specialized systems for your specific needs.

-

If you are dealing with standard conforming loans, relying on industry-standard platforms like DU or LPA is mandatory.

-

If your biggest delay is chasing down borrower paperwork, tools like Floify or Ocrolus are excellent investments.

-

However, if you are looking for an all-around AI assistant to verify complex conventional and Non-QM guidelines, calculate DTI, and find niche programs without a heavy enterprise price tag, I highly recommend starting with Zeitro. It offers the best balance of speed, accuracy, and value for modern mortgage professionals.