What are Mortgage Guidelines? How to Verify Accurately?

As a mortgage broker, my desk is constantly buried under a mountain of underwriting updates. Keeping up with different lender guidelines feels like chasing a moving target, especially when a client's pre-approval hangs in the balance.

Over the years, I've realized that manually digging through 500-page PDFs is a fast track to burnout. That is why I started using Zeitro Strata AI. It has completely changed my daily routine. Instead of spending my mornings hunting down complex rules, I can simply verify guidelines across multiple lenders through a quick, conversational chat, allowing me to deliver faster, more reliable answers to my clients.

Learning What Mortgage Guidelines Are

At their core, mortgage guidelines are the underwriting blueprints lenders use to determine whether to approve a loan. Think of them as the guardrails of the primary and secondary mortgage markets. Established by government-sponsored enterprises like Fannie Mae and Freddie Mac, or by private institutional investors, these rules dictate the exact level of risk a lender is willing to assume.

They do not just exist to make our jobs complicated. They ensure systemic stability. By defining strict parameters for creditworthiness, income stability, and collateral standards, these guidelines keep the mortgage market liquid. Without them, lenders would struggle to sell their loans on the secondary market to free up capital for new borrowers. For mortgage professionals, mastering these rules is the difference between a smooth closing and a last-minute loan denial.

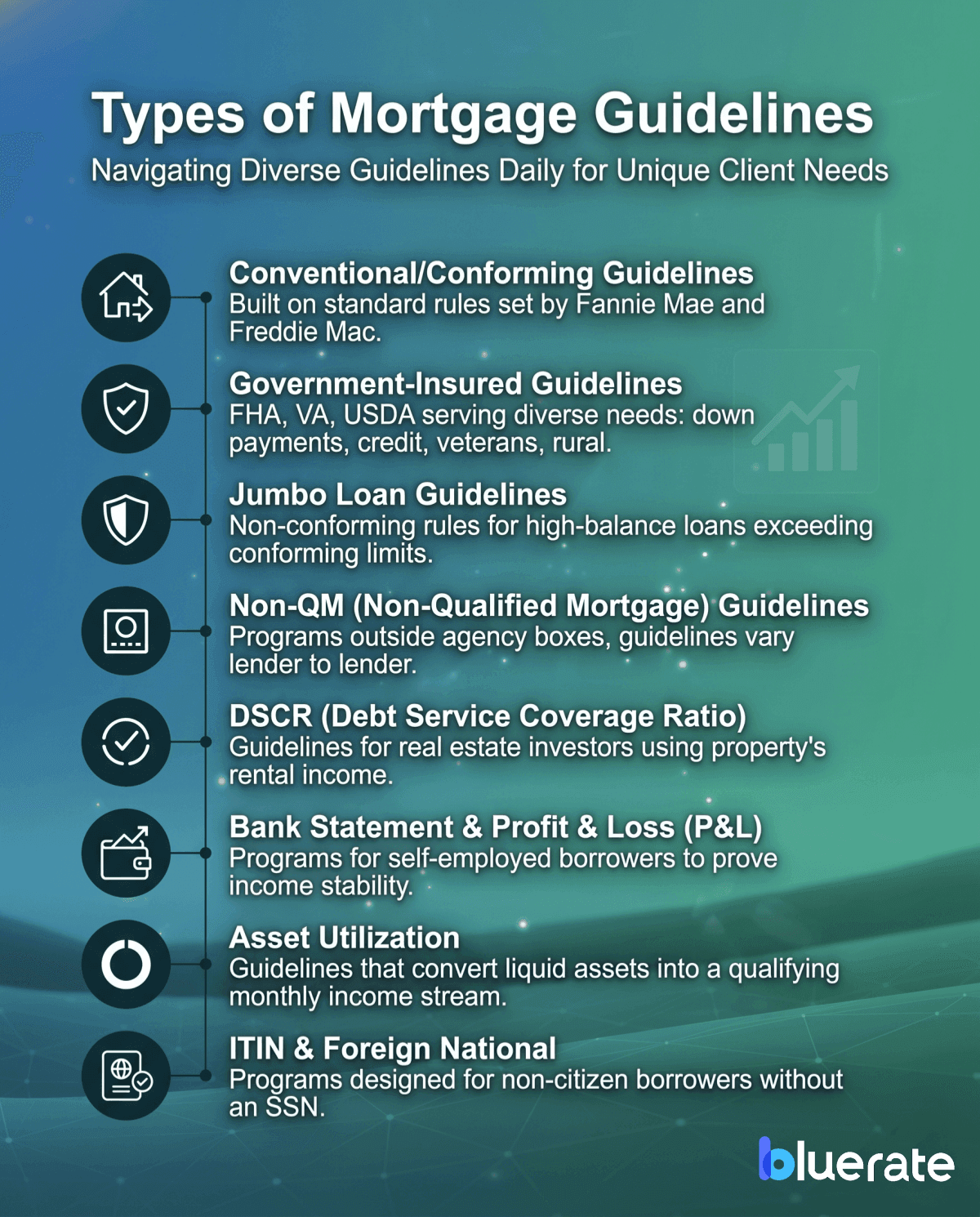

Types of Mortgage Guidelines

Depending on my client's unique financial situation, I have to pivot between completely different sets of rules. While conforming loans are highly standardized, the non-conforming and Non-QM space is incredibly diverse and constantly changing. Here are the primary types of guidelines I navigate daily:

-

Conventional/Conforming Guidelines: Built on standard rules set by Fannie Mae and Freddie Mac.

-

Government-Insured Guidelines: FHA, VA, and USDA programs serve different borrower groups, including those with lower down payments or credit flexibility (FHA), eligible veterans (VA), and income-qualified rural borrowers (USDA).

-

Jumbo Loan Guidelines: Non-conforming rules for high-balance loans that exceed conforming limits.

-

*Non-QM (Non-Qualified Mortgage) Guidelines:* Programs that do not fit standard agency boxes, which is where guidelines vary wildly from lender to lender.

-

DSCR (Debt Service Coverage Ratio): Guidelines for real estate investors using the property's rental income rather than personal income.

-

Bank Statement & Profit & Loss (P&L): Programs specifically tailored for self-employed borrowers to prove income stability.

-

Asset Utilization: Guidelines that convert liquid assets into a qualifying monthly income stream.

-

ITIN & Foreign National: Programs designed for non-citizen borrowers without a Social Security Number.

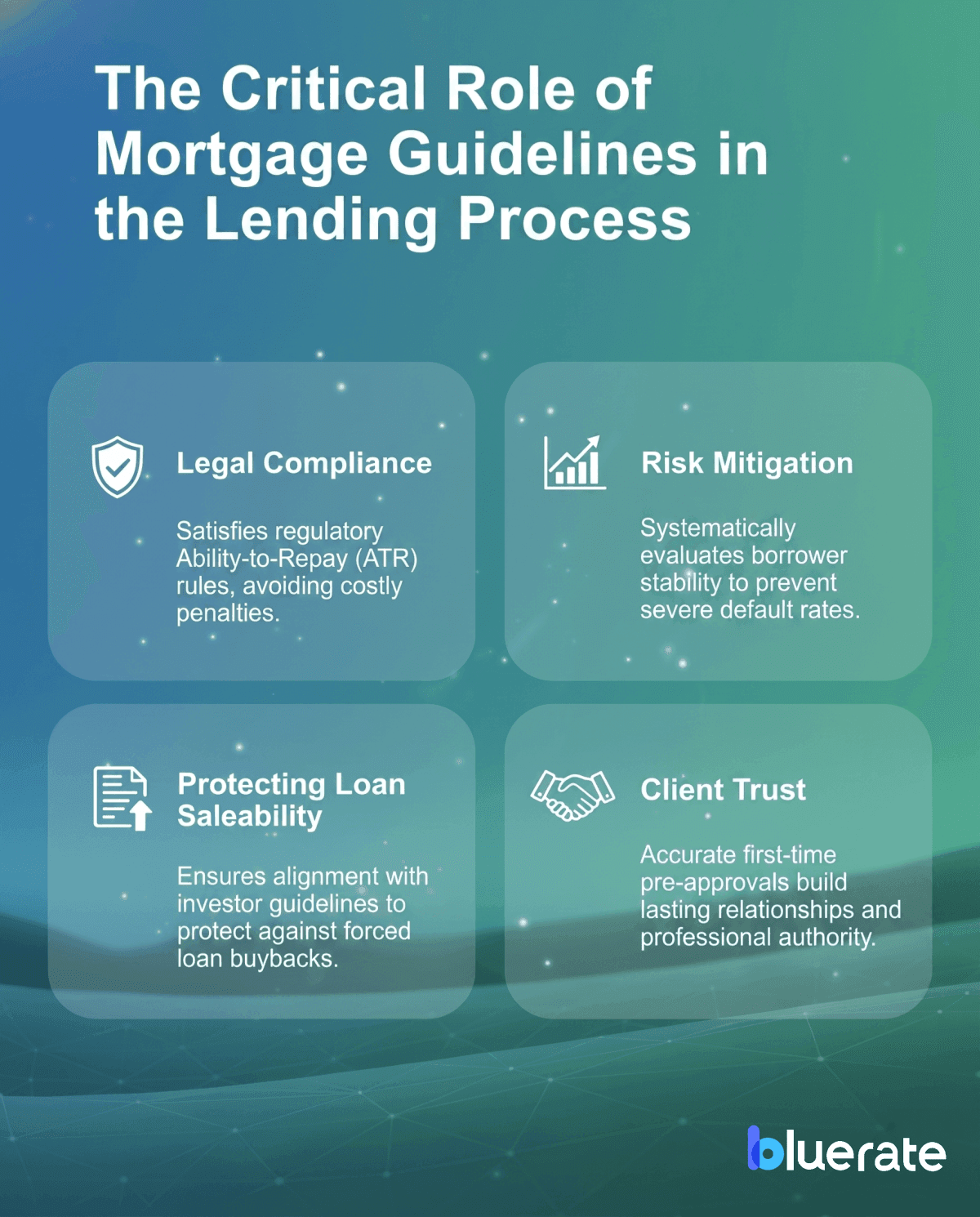

The Critical Role of Mortgage Guidelines in the Lending Process

I've learned the hard way that missing even a minor guideline change can derail an entire transaction. These standards are the lifeblood of our day-to-day operations for several critical reasons:

-

Legal Compliance: They ensure we satisfy the regulatory Ability-to-Repay (ATR) rules, keeping our business safe from costly penalties.

-

Risk Mitigation: By systematically evaluating borrower stability, lenders prevent severe default rates and maintain a healthy portfolio.

-

Protecting Loan Saleability: If a loan does not align with investor guidelines, the lender may be forced to buy back the loan, which is a massive financial blow.

-

Client Trust: Getting a pre-approval right the first time builds lasting relationships and professional authority.

Key Qualification Criteria Defined in Mortgage Guidelines

Within these guideline manuals, lenders outline the exact metrics we must calculate. However, we are currently seeing a structural shift in how these criteria are applied.

For instance, the mortgage industry is in the process of transitioning toward advanced credit scoring models like FICO 10T and VantageScore 4.0, although most loans are still currently evaluated using legacy FICO models, which utilize trended data rather than just a single-day snapshot.

Fannie Mae does not formally enforce a universal minimum credit score. However, a 620 score remains the widely accepted baseline in practice, with Desktop Underwriter (DU) providing a more comprehensive risk-based evaluation.

The core parameters we verify still include:

-

Credit History: Analyzing overall risk profiles, reserves, and credit trends.

-

DTI (Debt-to-Income): Assessing monthly debt payments against qualifying income.

-

LTV (Loan-to-Value): Evaluating the down payment size and equity requirements.

-

Asset & Reserve Requirements: Verifying that borrowers have post-closing liquidity to handle unexpected expenses.

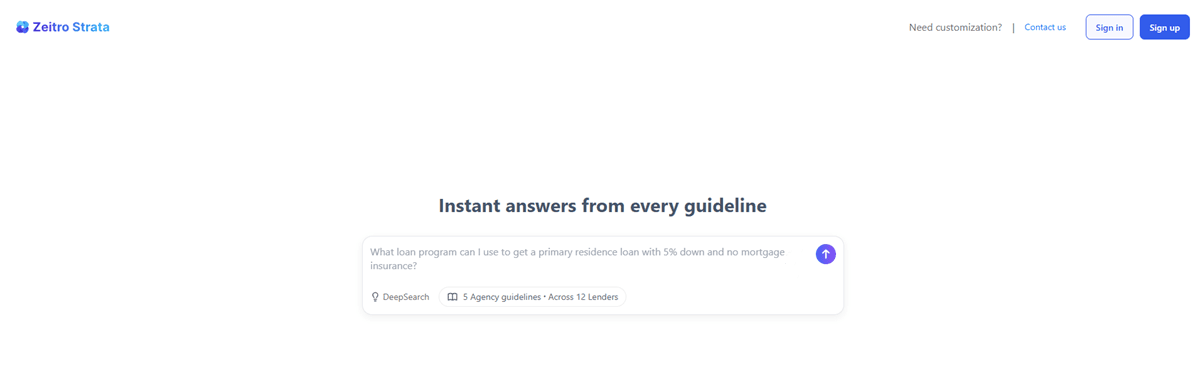

How to Streamline Mortgage Guideline Verification with Zeitro Strata AI

When I need to quickly cross-verify these criteria across multiple lenders, my go-to assistant is Zeitro Strata AI. It is an AI-powered tool specifically optimized to search QM and Non-QM guidelines---an absolute lifesaver for complex Non-QM scenarios. By allowing me to ask both highly specific and broad questions, it has shrunk my manual guideline lookup time from 30 minutes to mere seconds.

Here is what makes this tool a central part of my workflow:

-

DeepSearch Technology: It instantly searches and cross-checks policies across 100+ investors and nearly 400 guideline sources, saving hours of manual digging.

-

Comprehensive Coverage: It pulls data from major US lenders like AAA Lending, AD Mortgage, Freedom Mortgage, and HomeXpress, continually updating to reflect the latest market shifts.

-

100% Citation-Backed Answers: Unlike generic AI, it provides direct citations and source tracking, allowing me to trace answers back to the original PDFs so I can verify them with absolute confidence.

-

Smart Customizable Tags: I can filter my searches instantly by tagging specific loan types like DSCR or ITIN, immediately narrowing down the programs my clients care about.

-

Calculators & Matching Tools: It lets me upload documents to auto-calculate qualifying income and matches eligible down payment assistance programs state-by-state.

-

Interactive Explain Function: If a policy nuance is confusing, the "Explain" feature acts as a quick way to re-query and break down the selected source guidelines.

-

Sharing & Multilingual Support: I can easily share links or email results to my team, and it supports queries in multiple languages.

Zeitro Strata AI offers 10 free daily queries, making it incredibly easy to integrate into your daily pipeline.

FAQs About Mortgage Guidelines

Q1. How often do lenders update their guidelines?

Lenders update their guidelines continuously based on economic shifts, secondary market demand, and regulatory updates.

Q2. Can a borrower qualify if they miss a specific guideline requirement?

Yes. Lenders often look at "compensating factors," such as massive cash reserves or high down payments, to approve a file that has minor weaknesses elsewhere.

Q3. What is the main difference between QM and Non-QM guidelines?

QM guidelines follow federal Ability-to-Repay (ATR) requirements and are now primarily defined by pricing thresholds rather than strict debt-to-income (DTI) caps. Non-QM guidelines offer flexible underwriting, allowing bank statements or asset utilization to prove income.

Q4. Why are self-employed guidelines more complex?

Because tax write-offs often lower a borrower's net income. Lenders use specialized formulas to calculate true cash flow, which varies widely across investors.

Q5. What is the fastest way to compare rules across different lenders?

Historically, we had to keep multiple tabs open and search PDFs. Now, using conversational platforms like Zeitro Strata AI allows you to query multiple databases at once, returning reliable, cited answers in seconds.

Conclusion

In our industry, timing is everything. A delay in verifying a guideline can mean losing an escrow or missing out on a client's dream home. Relying on outdated manual search methods is no longer sustainable when guidelines change overnight.

Staying competitive in today's market requires adopting smart digital tools that enhance our expertise without replacing the human touch. If you want to streamline your workflow and minimize errors, I highly recommend trying Zeitro Strata AI. With their 10 free daily queries, you can easily test its capabilities and see how it fits into your daily routine.