FHA Mortgage Guidelines: What and How to Verify Them?

Having spent years in the mortgage industry, I know how easily a deal can stall over a single, unverified guideline. Checking FHA rules manually can consume a significant part of your day. That's why I've come to rely on Zeitro Strata AI.

It's an AI-powered assistant that lets us verify FHA mortgage guidelines for various lenders using a simple, natural chat interface. Instead of wading through endless PDFs, I can instantly confirm compliance details and keep my pipeline moving smoothly. Here is a practical look at how FHA guidelines work and how to simplify your verification process.

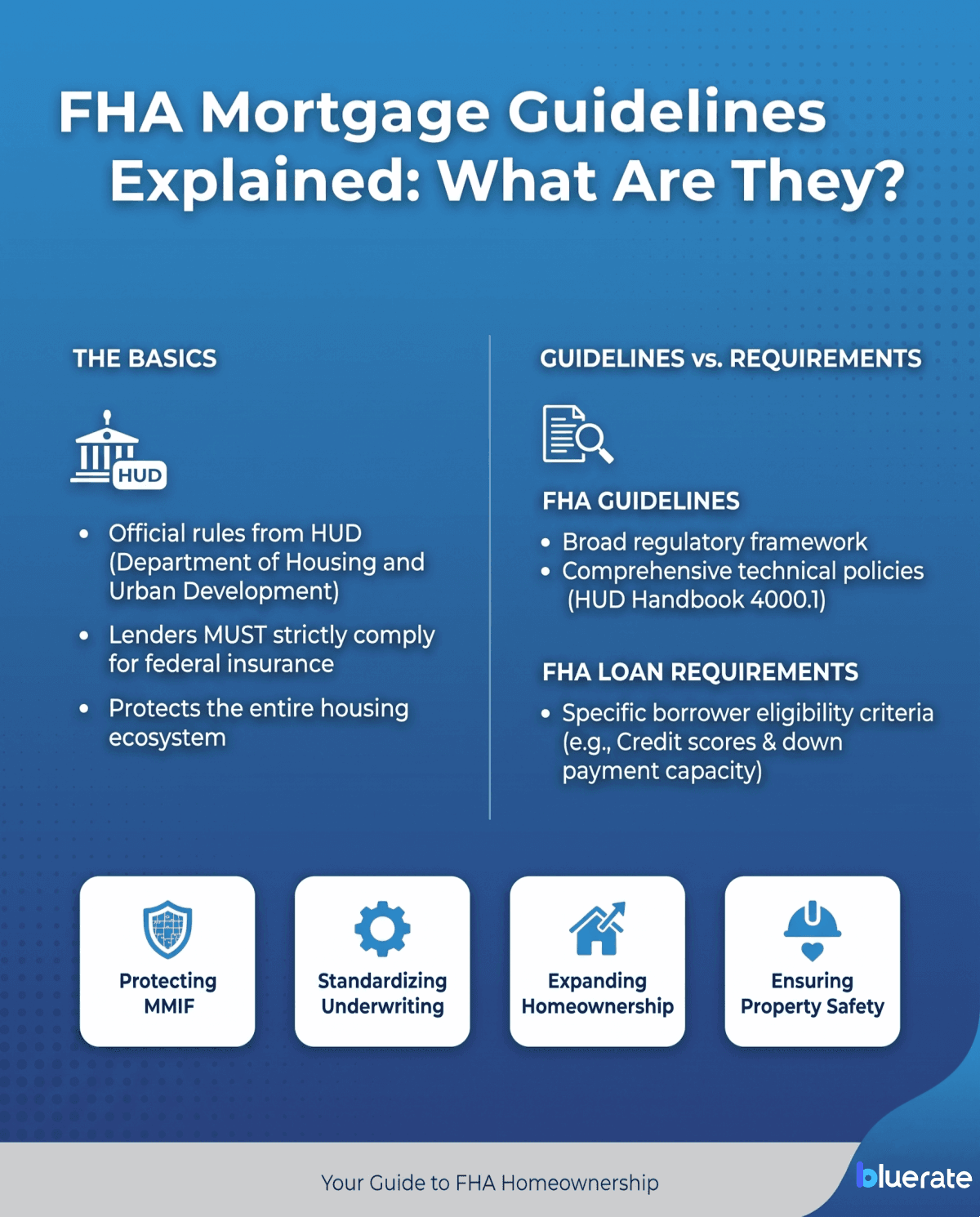

FHA Mortgage Guidelines Explained: What Are They?

To put it simply, FHA mortgage guidelines are the official rules and underwriting policies issued by the Department of Housing and Urban Development (HUD). If you are a lender, underwriter, or broker, you must strictly comply with these guidelines to ensure the loan qualifies for federal insurance.

While people often use "FHA guidelines" and "FHA loan requirements" interchangeably, I find it helpful to make a small distinction. FHA guidelines refer to the broader regulatory framework---the comprehensive, technical policies outlined in the massive HUD Handbook 4000.1.

On the other hand, FHA loan requirements represent the specific borrower eligibility criteria, like minimum credit scores and down payment amounts. To successfully close an FHA loan, we must navigate both the macro guidelines and the micro requirements without missing a beat.

What Are FHA Guidelines for?

FHA guidelines exist for several practical reasons. Over my career, I've realized these rules aren't just red tape. They protect the entire housing ecosystem. Here is what they are designed to achieve:

-

Protecting the Mutual Mortgage Insurance Fund (MMIF): By keeping standard parameters, FHA minimizes defaults that could drain the federal insurance pool.

-

Standardizing Underwriting: They provide a uniform risk framework for all participating lenders.

-

Expanding Homeownership: These rules offer more flexible qualification standards, particularly for borrowers with lower credit scores or limited down payment capacity.

-

Ensuring Property Safety: FHA appraisal guidelines verify that the property is safe, secure, and structurally sound for the buyer.

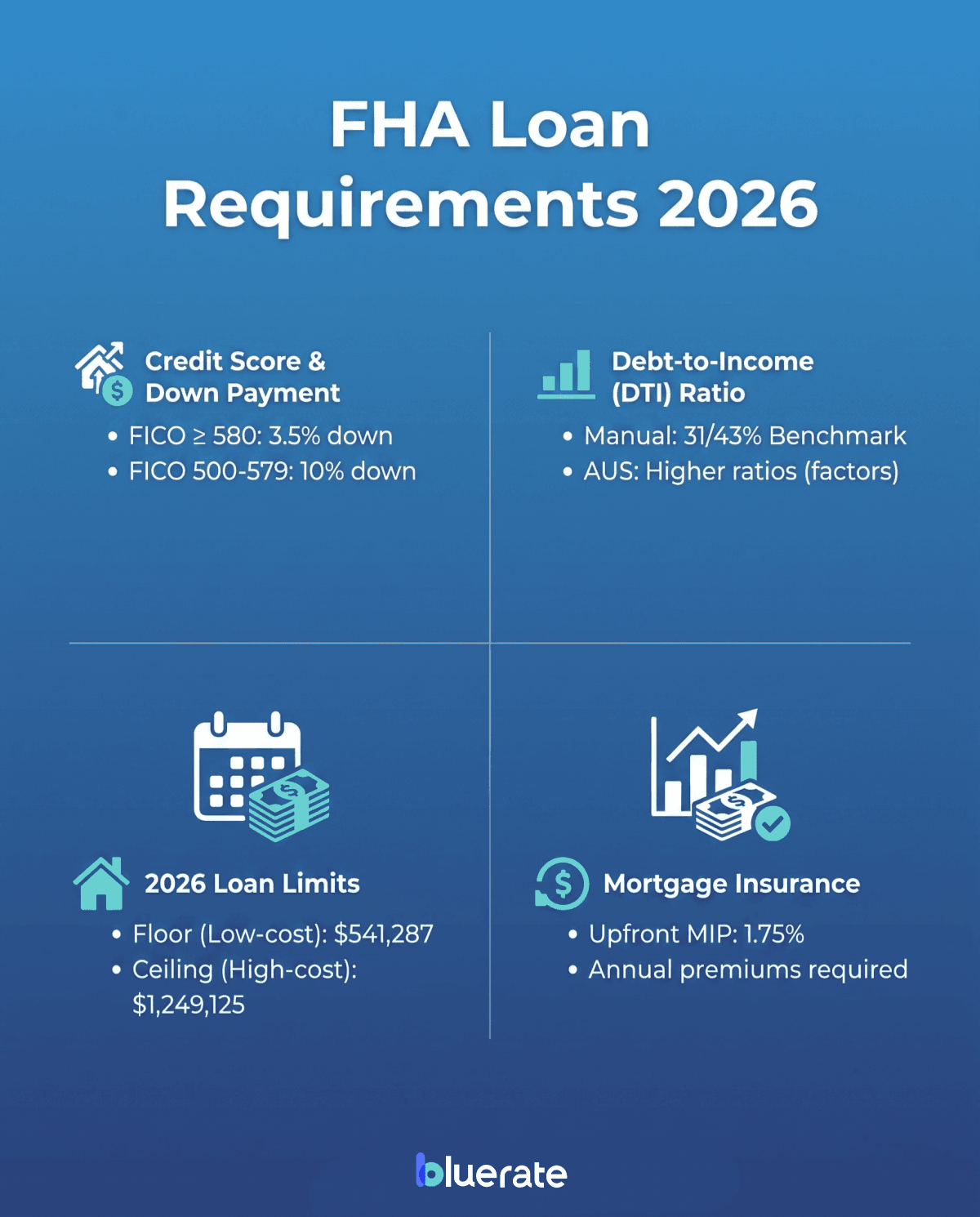

FHA Loan Requirements 2026

To keep your loans on track this year, you need to know the baseline federal criteria. Here are the core FHA loan requirements for 2026 that I keep on my desk:

-

Credit Score & Down Payment: A FICO score of 580 or higher requires just a 3.5% down payment. Borrowers with scores between 500 and 579 can still qualify but must put 10% down.

-

Debt-to-Income (DTI) Ratio: For manually underwritten loans, FHA typically uses 31/43% as a benchmark, but higher ratios are often allowed through automated underwriting systems (AUS) with compensating factors.

-

2026 Loan Limits: For a one-unit property, the 2026 FHA national loan limit floor is $541,287 in low-cost areas, reaching a ceiling of $1,249,125 in high-cost markets.

-

Mortgage Insurance: Borrowers must pay an Upfront Mortgage Insurance Premium (UFMIP) of 1.75%, alongside annual premiums.

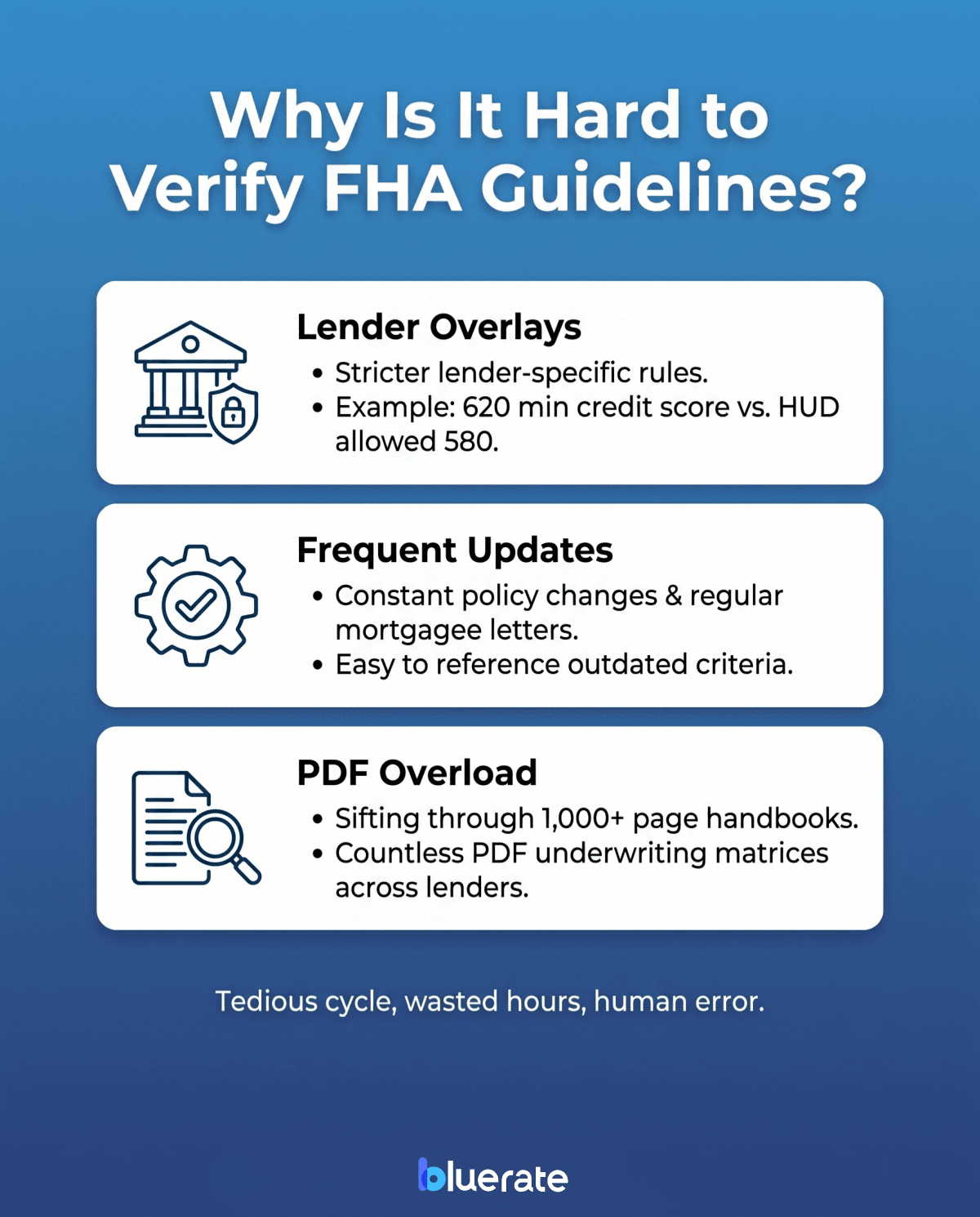

Why Is It Hard to Verify FHA Guidelines?

If FHA guidelines are publicly available, why do we struggle to verify them? In my daily work, I encounter three main roadblocks:

-

Lender Overlays: This is the biggest hurdle. Even if HUD allows a 580 credit score, individual lenders (like Freedom or AmWest) frequently add stricter overlays, such as requiring a 620 minimum score.

-

Frequent Updates: Between regular mortgagee letters and policy updates, the rules change constantly, making it easy to reference outdated criteria.

-

PDF Overload: Sifting through 1,000+ page handbooks and countless PDF underwriting matrices across 10 different lenders takes forever.

It's a tedious cycle that wastes valuable hours and introduces human error.

Zeitro Strata: Quickly and Accurately Verify FHA Guidelines

To solve this, I've integrated Zeitro Strata AI into my workflow. It's an AI-powered mortgage guideline assistant that has completely changed how I verify loan eligibility. Zeitro is designed to query both QM and Non-QM guidelines, though it excels particularly in the complex Non-QM space. It covers nearly 400 guidelines, including over 60 FHA-specific guidelines, and is continuously updated.

Here are the highlights that make it a game-changer for my business:

-

DeepSearch across Lenders: It cross-checks over 100 investors (like AD Mortgage, CMG, Forward Lending, and Freedom Mortgage) in seconds, slashing manual lookup time from 30 minutes to moments.

-

Zero Hallucinations: Zeitro provides 100% citation-backed answers. Every response links directly back to the source document, giving me absolute confidence in the accuracy.

-

Customizable Tags: I can apply tags for DSCR, ITIN, or loan-type to narrow down queries to the exact programs I need.

-

Advanced Scenario Tools: From basic eligibility to complex calculations, I can even upload docs to auto-calculate income and match local Down Payment Assistance (DPA) programs.

-

Deepen the Search: When I hit an ambiguous guideline, the 'Explain' tool lets me query a specific section further (though keep in mind, this follow-up consumes one of your query credits).

It supports multi-lingual inputs and lets me share findings via email or links. With 10 free daily queries, it's an incredibly high-ROI addition to my toolkit.

FAQs About FHA Mortgage Guidelines

Q1. Can FHA guidelines change year to year?

Yes, they frequently do. HUD regularly issues new Mortgagee Letters to adjust limits, update loss mitigation policies, or modify qualifying criteria. Staying updated manually is incredibly challenging.

Q2. Are FHA guidelines the same for every lender?

No. While HUD sets the absolute floor, most lenders enforce "overlays", which are stricter credit, DTI, or asset rules. This is why tools like Zeitro Strata AI are essential to cross-check specific investor matrices.

Q3. Can I qualify for FHA with past bankruptcy?

Yes. Generally, you can qualify two years after a Chapter 7 discharge (with re-established credit) or 12 months into a Chapter 13 plan (subject to court and lender approval).

Q4. What disqualifies you from an FHA loan?

Primary disqualifiers include active delinquent federal debts (tracked via CAIVRS), failure to meet foreclosure waiting periods (usually three years), or property issues that fail basic safety and structural appraisal standards.

Q5. Is it hard to get approved for an FHA loan?

Generally, FHA loans are more accessible than conventional loans because of lower credit and down payment requirements. However, if your file requires manual underwriting instead of automated approval, the scrutiny increases significantly.

Final Thoughts

At the end of the day, verifying FHA guidelines shouldn't be the bottleneck that delays your borrower's dream of homeownership. In a competitive housing market, speed and accuracy are everything. Having a reliable, citation-backed tool to instantly cross-reference complex guidelines and lender overlays is no longer just a luxury---it's a necessity for survival.

If you're tired of digging through endless PDFs and cross-referencing conflicting investor matrices, I highly recommend giving Zeitro Strata AI a try. You can sign up and get 10 free queries every single day. Test it out on your next tricky FHA file, and experience firsthand how it shrinks a 30-minute chore into a few seconds of simple chatting.