LTV Ratio Explained: Meaning, Example, Limits, FAQs

I still remember looking at my first pre-approval letter and feeling completely overwhelmed by the alphabet soup of mortgage terms. Among all those acronyms, one stood out as a total dealmaker or dealbreaker: LTV, or Loan-to-Value ratio.

Let me tell you, this single number dictates whether your loan gets approved and how much interest you'll end up paying over the next 30 years. Although understanding LTV is incredibly helpful, consulting with a professional is always your safest bet. You can easily find a local loan officer for free advice at Bluerate.ai to get accurate numbers tailored to your specific situation.

Key Takeaways

- LTV defined simply: It's the percentage of your home's appraised value that you are borrowing through a mortgage.

- Lower is always better: A lower LTV reduces lender risk, meaning you get better interest rates and can avoid costly mortgage insurance.

- The standard limit: For most conventional loans, the maximum allowable LTV cap sits at 97% for first-time homebuyers, requiring just a 3% down payment.

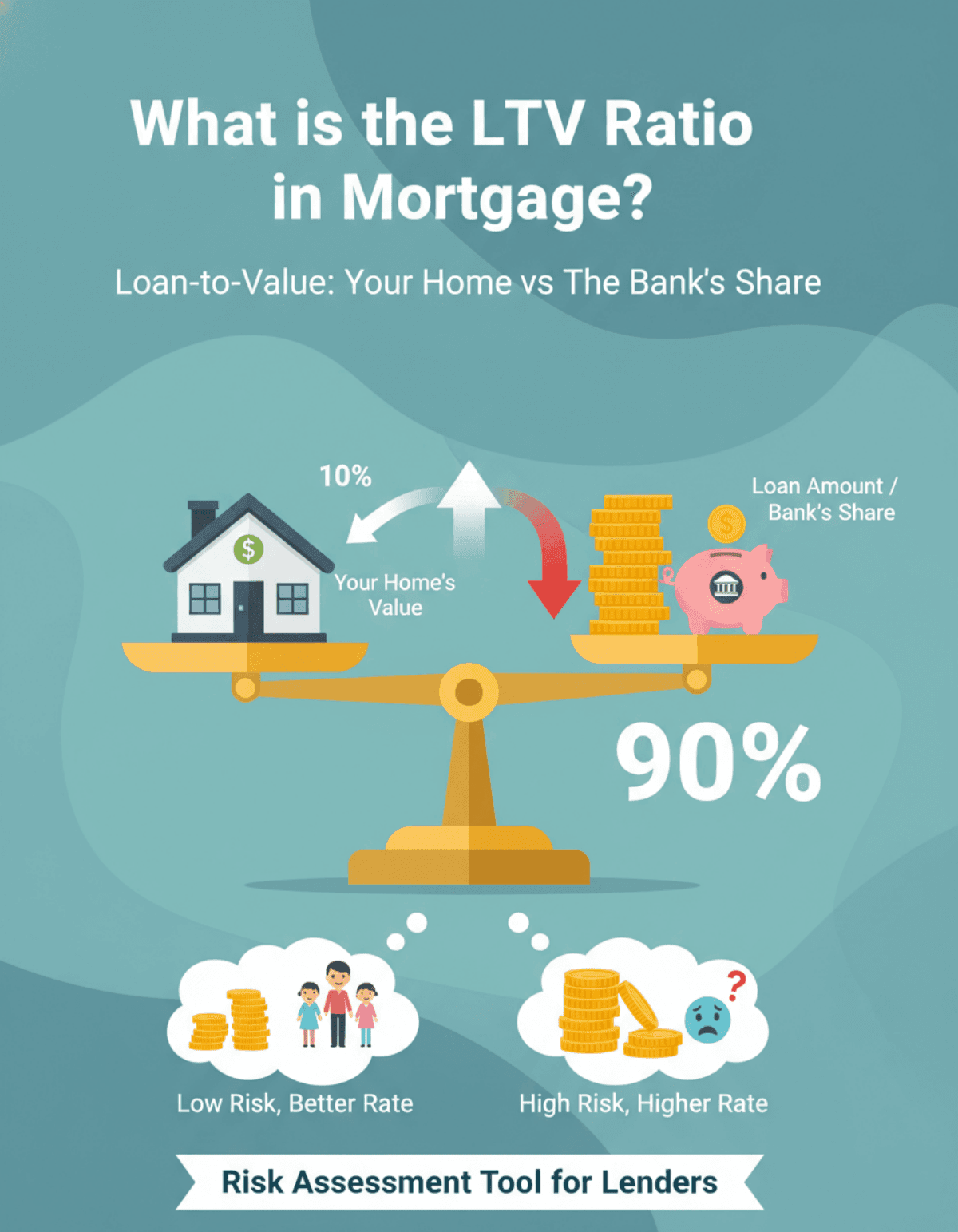

What is the LTV Ratio in Mortgage?

In simple terms, your Loan-to-Value (LTV) ratio compares the amount of money you want to borrow against the actual value of the property you are buying. Think of it as a financial scale measuring how much of the house you actually own right now versus how much the bank temporarily owns.

But why does this metric even exist? From my experience working through real estate transactions, I can tell you it's purely a risk assessment tool for lenders. Banks are essentially placing a bet on you. An LTV of 95% means the lender is putting up almost all the cash, absorbing massive risk if you default. Conversely, an LTV of 70% shows you have significant "skin in the game," making you a safe bet. Ultimately, this ratio acts as the ultimate risk yardstick in the mortgage industry.

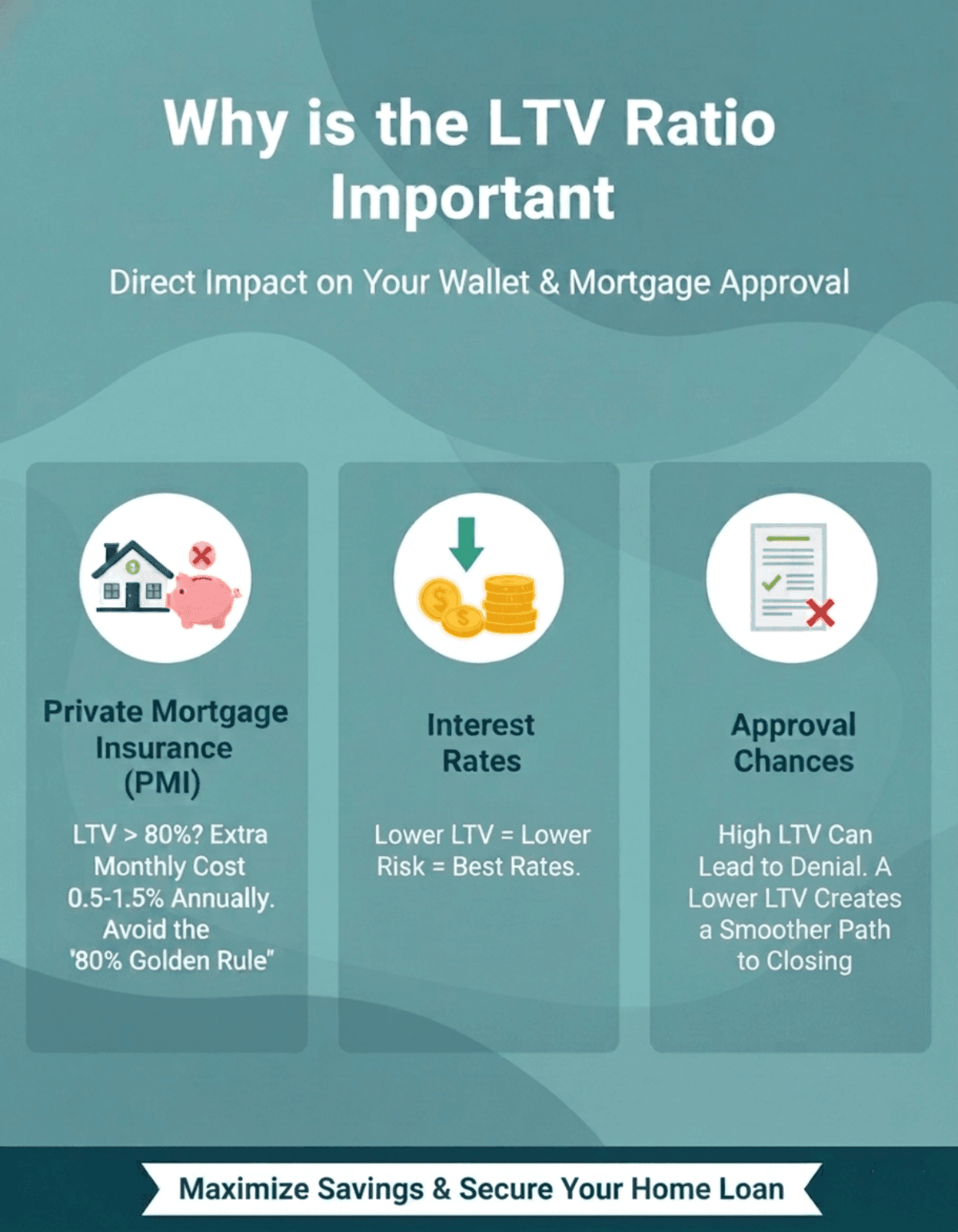

Why is the LTV Ratio Important?

You might wonder why I stress paying so much attention to this single metric. Your LTV ratio directly impacts your wallet in three major ways:

- Private Mortgage Insurance (PMI): This is where the famous "80% golden rule" comes into play. If your LTV is above 80%, conventional lenders typically force you to pay PMI, which averages 0.5% to 1.5% of your loan amount annually. That's hundreds of extra dollars leaving your pocket each month.

- Interest Rates: Banks reward safe bets. A lower ratio almost always unlocks the best possible interest rates, saving you tens of thousands over the life of the loan.

- Approval Chances: If your number creeps too high, past the maximum guidelines for your specific loan program, lenders will flat-out deny your application. Keeping your LTV in check ensures a smoother path to the closing table.

How to Calculate LTV Ratio?

Figuring out your LTV is actually quite simple once you know the formula. Grab a calculator and use this equation:

LTV = (Loan Amount ÷ Appraised Property Value) × 100

Here is a highly professional detail you must keep in mind. One that trips up many first-time buyers: When determining the "Property Value" for the denominator, lenders will always use the lesser of the two between your negotiated purchase price and the home's officially appraised value.

For example, if you agree to buy a house for $400,000, but the appraiser says it's only worth $380,000, the bank uses $380,000 for their math. This rule protects the lender from over-financing a property. Simply divide exactly what you need to borrow by that lower value, multiply by 100, and you've got your percentage.

Examples of LTV Ratio

Let's look at two real-world scenarios to see how this plays out. Imagine two friends, Alex and Taylor, both buying identical homes priced and appraised at $400,000.

Case A (Alex):

Alex managed to save up a solid 20% down payment, putting down $80,000 and borrowing $320,000.

- Math: ($320,000 ÷ $400,000) × 100 = 80% LTV.

- Result: Alex hits the 80% golden rule, entirely avoiding PMI while securing a highly competitive interest rate.

Case B (Taylor):

Taylor prefers to keep cash on hand, opting for a 5% down payment of $20,000 and taking out a $380,000 mortgage.

- Math: ($380,000 ÷ $400,000) × 100 = 95% LTV.

- Result: Because the ratio is so high, Taylor is required to pay monthly PMI, significantly increasing the overall monthly housing expense.

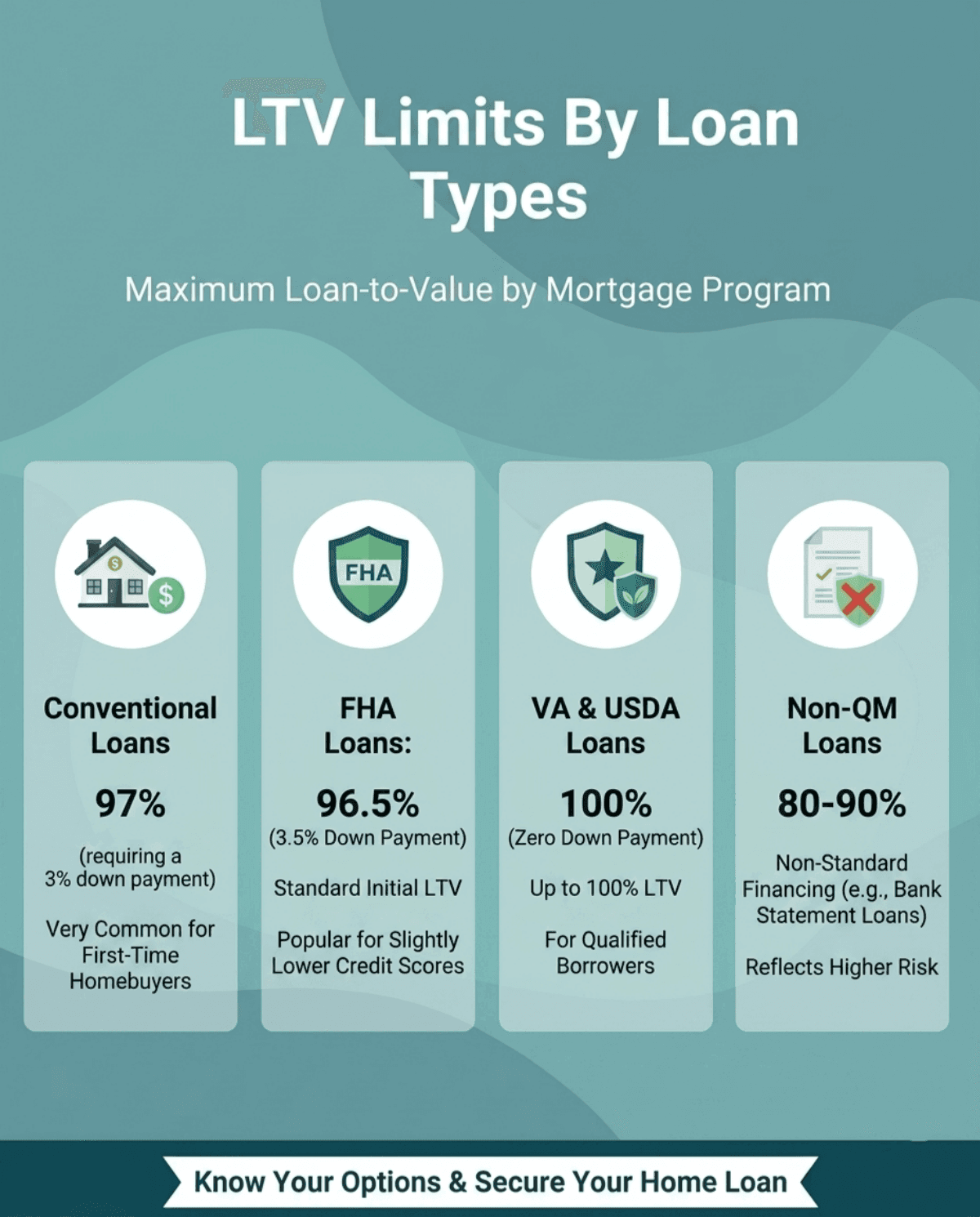

LTV Limits By Loan Types

Different loan programs have different tolerances for risk. Over the years, I've noticed that knowing these maximum LTV limits can completely change a buyer's strategy. Here's a quick breakdown of the highest LTV lenders will allow based on the mortgage type:

- Conventional Loans: The absolute maximum is typically 97% (requiring a 3% down payment), which is very common for first-time homebuyers.

- FHA Loans: FHA Loans: Standard initial LTV is 96.5% with a 3.5% down payment (before financing upfront MIP, which increases the financed LTV), making them incredibly popular for borrowers with slightly lower credit scores.

- VA and USDA Loans: These government-backed programs allow up to 100% LTV (zero down payment) for qualified borrowers, with financed fees potentially exceeding 100%.

- Non-QM Loans: For non-standard financing like bank statement or DSCR loans, lenders prefer more cushion. Maximum limits typically hover between 80% and 90%, reflecting the higher risk of alternative income verification.

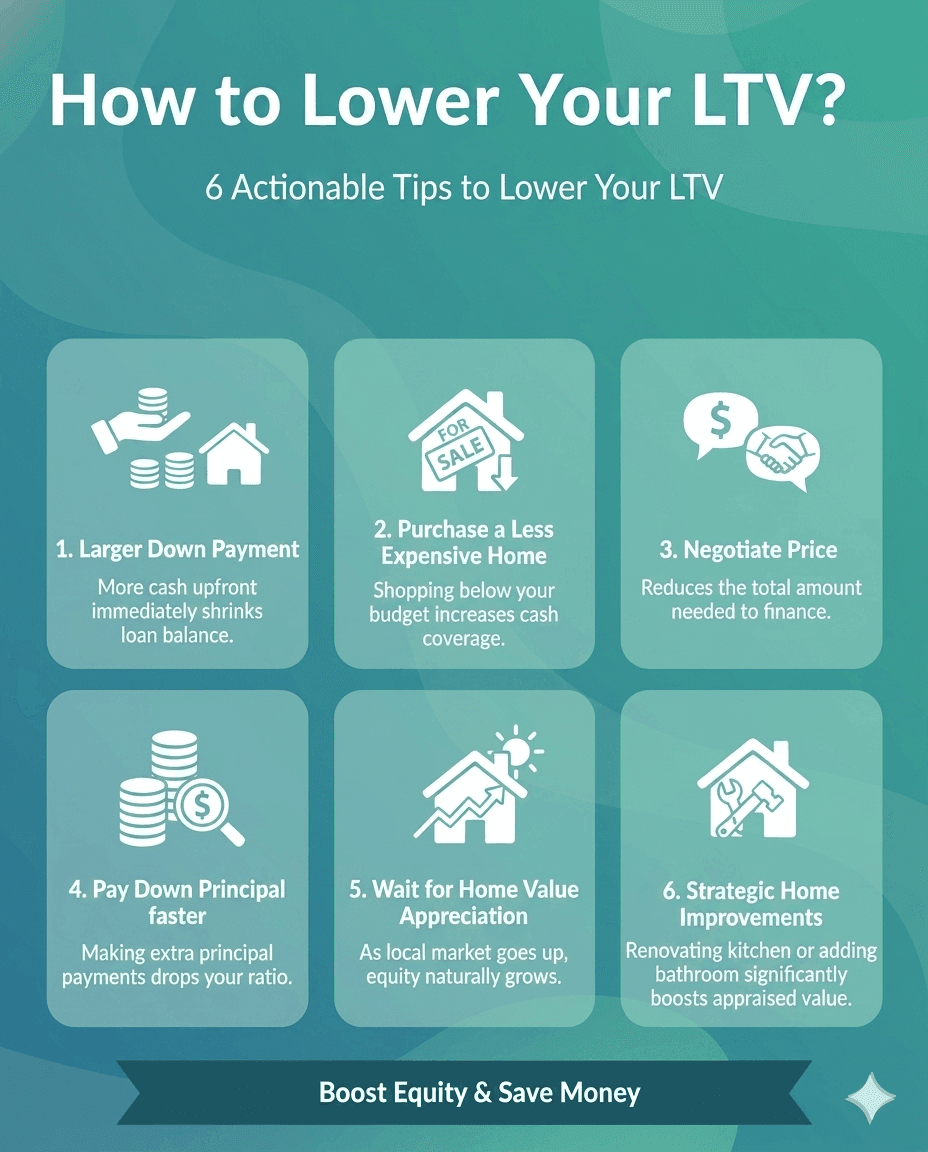

How to Lower Your LTV? Check Tips Here

Nobody wants to pay unnecessary fees or higher rates. If your percentage is currently sitting uncomfortably high, don't panic. Based on my own real estate journey, here are 6 highly actionable tips to effectively lower your LTV:

- Make a larger down payment: It sounds obvious, but bringing more cash to closing instantly shrinks your loan balance.

- Purchase a less expensive home: Shopping below your maximum budget naturally increases the percentage your available cash covers.

- Negotiate a lower purchase price: Hard bargaining reduces the total amount you need to finance.

- Pay down your principal balance faster: If you already own the home and want to refinance later, making extra principal payments will quickly drop your ratio.

- Wait for home values to appreciate: Sometimes time does the heavy lifting. As your local market goes up, your equity grows, lowering the LTV for a future refinance.

- Make strategic home improvements: Renovating your kitchen or adding a bathroom can significantly boost your home's appraised value before you refinance.

FAQs About LTV in Real Estate

Q1. What is a good LTV ratio?

Generally, an LTV ratio of 80% or lower is considered "good" because it completely eliminates the need for Private Mortgage Insurance (PMI) on conventional loans. This threshold signals low risk to lenders, allowing you to secure the most favorable interest rates.

Q2. Does LTV include closing costs?

No, your LTV ratio strictly calculates the core mortgage principal against the property's value. Standard closing costs, like appraisal fees, title insurance, and taxes, are not included in this formula unless you actively choose to roll those expenses into your final loan amount.

Q3. What is Combined LTV (CLTV)?

Combined Loan-to-Value (CLTV) is used when you have multiple loans on the exact same property. If you take out a primary mortgage plus a Home Equity Line of Credit (HELOC), the CLTV adds all your outstanding loan balances together before dividing by the home's value.

Q4. Can my LTV ratio change over time?

Yes, it constantly changes! Every time you make your monthly mortgage payment, a portion goes toward the principal balance, steadily lowering your LTV. Additionally, if the real estate market booms and your home's value rises, your ratio will decrease even faster.

Q5. What happens if my LTV is over 100%?

When your LTV exceeds 100%, you owe more than the property is actually worth. This is often called being "underwater" or "upside down" on your mortgage. It usually happens during a market crash and makes selling or refinancing incredibly difficult without bringing cash to the table.

Final Word

At the end of the day, mastering your LTV ratio isn't just about passing a math test. It's about saving yourself thousands of dollars in interest and insurance premiums. By keeping that number as low as possible, you put yourself in the driver's seat during negotiations.

However, remember that everyone's financial puzzle is unique. Online formulas are great, but your specific credit score, income, and down payment capabilities require a personalized strategy. Ready to find out your exact LTV and explore your real-world mortgage options? Don't navigate the complex world of home loans alone. Visit Bluerate.ai today to get matched with a local, experienced loan officer for a free, personalized consultation.