Read First: How to Calculate LTV Ratio for Mortgage?

When I bought my first home, the sheer number of financial acronyms felt completely overwhelming. One term my lender kept repeating was the Loan-to-Value ratio. If you're wondering how to calculate LTV ratio for a mortgage, you are in the right place.

Simply put, this metric determines whether your loan gets approved and how good your interest rate will be. In this guide, I will walk you through exactly how to crunch these numbers yourself. You'll quickly see that understanding your LTV gives you a massive advantage when negotiating with lenders and planning your homebuying budget.

Key Takeaways

- Your LTV ratio compares your total loan amount to the property's overall market value.

- You can easily figure it out by dividing the borrowed amount by the home's appraised value.

- Keeping your LTV at 80% or below is the magic number to avoid paying for Private Mortgage Insurance (PMI).

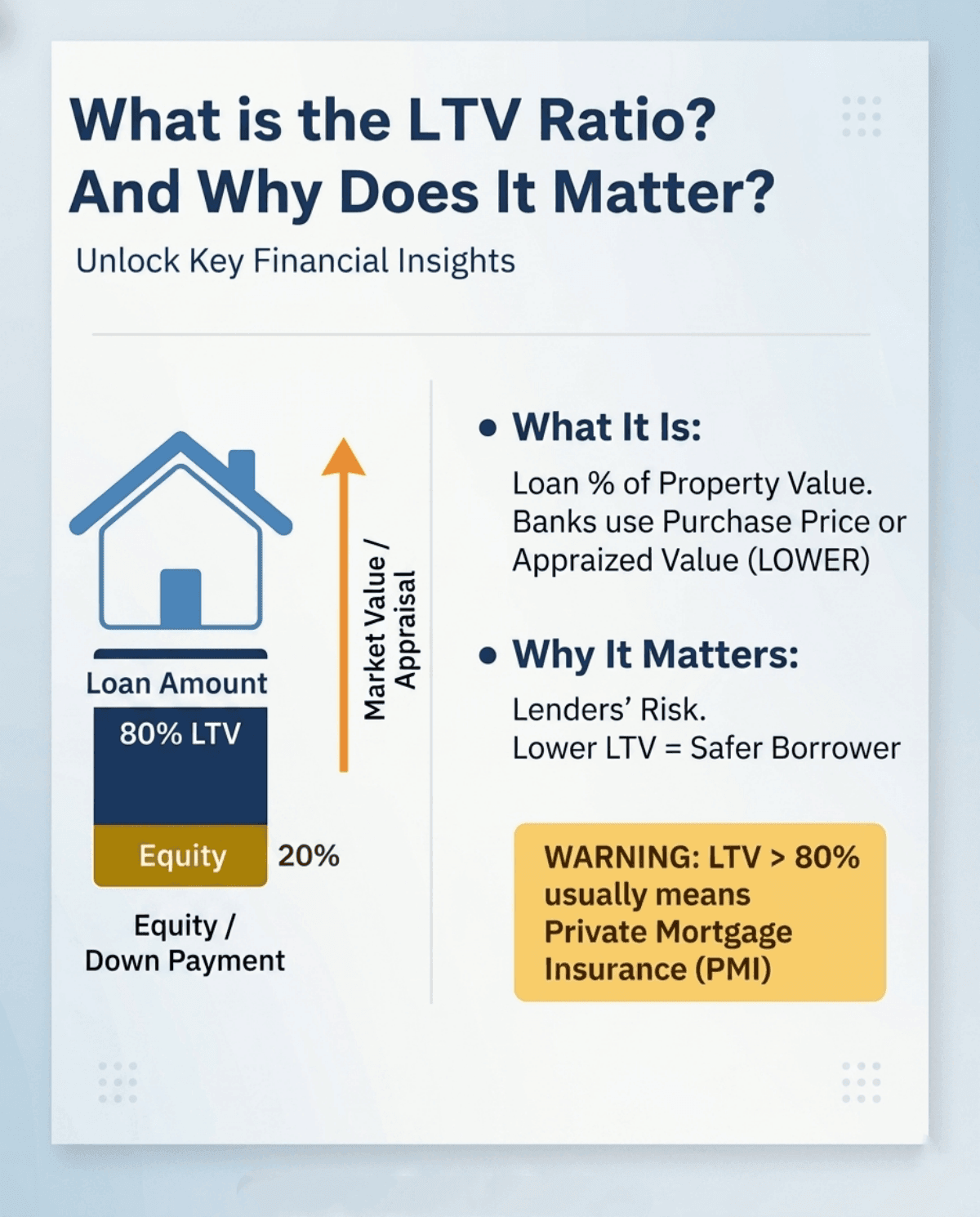

What is the LTV Ratio? And Why Does It Matter?

The Loan-to-Value ratio represents the percentage of your property financed by a loan compared to its actual market worth. Lenders obsess over this metric because it directly measures their financial risk. A lower percentage means you have more equity built up, making you a much safer bet.

However, the biggest trap I see buyers fall into is assuming "value" just means the asking price. In reality, banks always use the purchase price or the Appraised Value, whichever is lower. If you borrow more than 80% of that baseline, you will almost certainly have to pay Private Mortgage Insurance (PMI), protecting the lender if you happen to default.

Ways to Calculate Loan-to-Value Ratio

Figuring out this crucial metric is surprisingly straightforward. Based on my own real estate journey, you basically have two options: crunching the numbers yourself using a simple math equation, or leveraging reliable online calculators to do the heavy lifting for you.

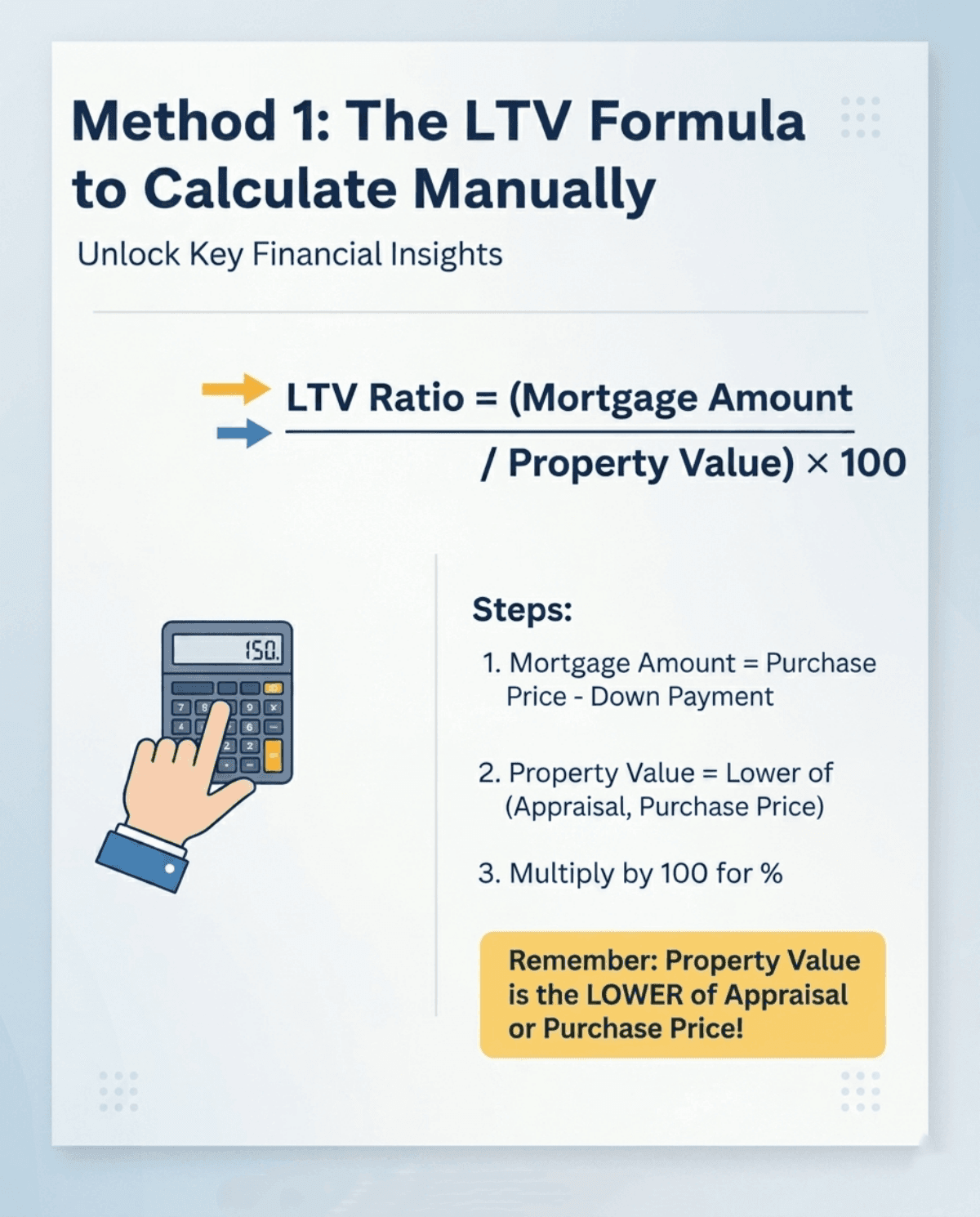

Method 1: The LTV Formula to Calculate Manually

I actually prefer doing the math by hand first because it helps me understand exactly where my money is going. The formula itself is basic division:

LTV Ratio = (Mortgage Amount ÷ Property Value) × 100

To get your exact Mortgage Amount (the numerator), take the total agreed-upon purchase price and subtract your cash down payment. Then, divide that figure by the Property Value (the denominator). Remember my earlier warning: this bottom number must be the appraisal amount if the appraiser values the home lower than what you agreed to pay. Finally, multiply the result by 100 to convert it into a neat percentage.

Let's say you are sitting at your kitchen table reviewing your budget. Grabbing a standard calculator and punching in these two numbers gives you immediate clarity on whether you'll be hit with extra insurance fees. It's a quick math trick that puts you firmly in the driver's seat.

Method 2: Use an Online LTV Calculator

If manual math isn't your strong suit, using a digital tool is a fantastic alternative. During my own refinancing process, I heavily relied on authoritative tools like the Fannie Mae Loan-to-Value Calculator and the Bankrate Mortgage Calculator. The biggest advantage of using these platforms is their incredible speed and accuracy. Many advanced calculators will even automatically estimate your monthly PMI costs if your down payment is less than twenty percent.

However, digital tools do have a few noticeable drawbacks. Most standard web calculators cannot account for sudden "under-appraisal" scenarios where your home's official valuation comes in unexpectedly low. Furthermore, they generally struggle to compute a Combined LTV (CLTV) if you are taking out a secondary mortgage, nor do they factor in specific, unique overlays that local credit unions might require. They are great starting points, but they simply don't replace human context.

Examples of LTV Calculation

Let's look at two real-world scenarios to make this crystal clear. In the first standard situation, imagine you buy a house for $500,000, and it appraises for that exact same amount. You put down $100,000 (20%) in cash, leaving a $400,000 loan. You simply divide $400,000 by $500,000, which equals an 80% LTV. You avoid extra insurance fees completely.

Now, consider a tricky appraisal shortfall scenario. Something a friend of mine recently faced. You agree to pay $500,000, but the appraiser says the home is only worth $480,000. You still contribute your $100,000 cash. Your loan is $400,000, but now the denominator must be the $480,000 appraisal. Dividing $400,000 by $480,000 pushes your ratio up to 83.3%. Because it crosses the 80% threshold, you are now on the hook for mortgage insurance.

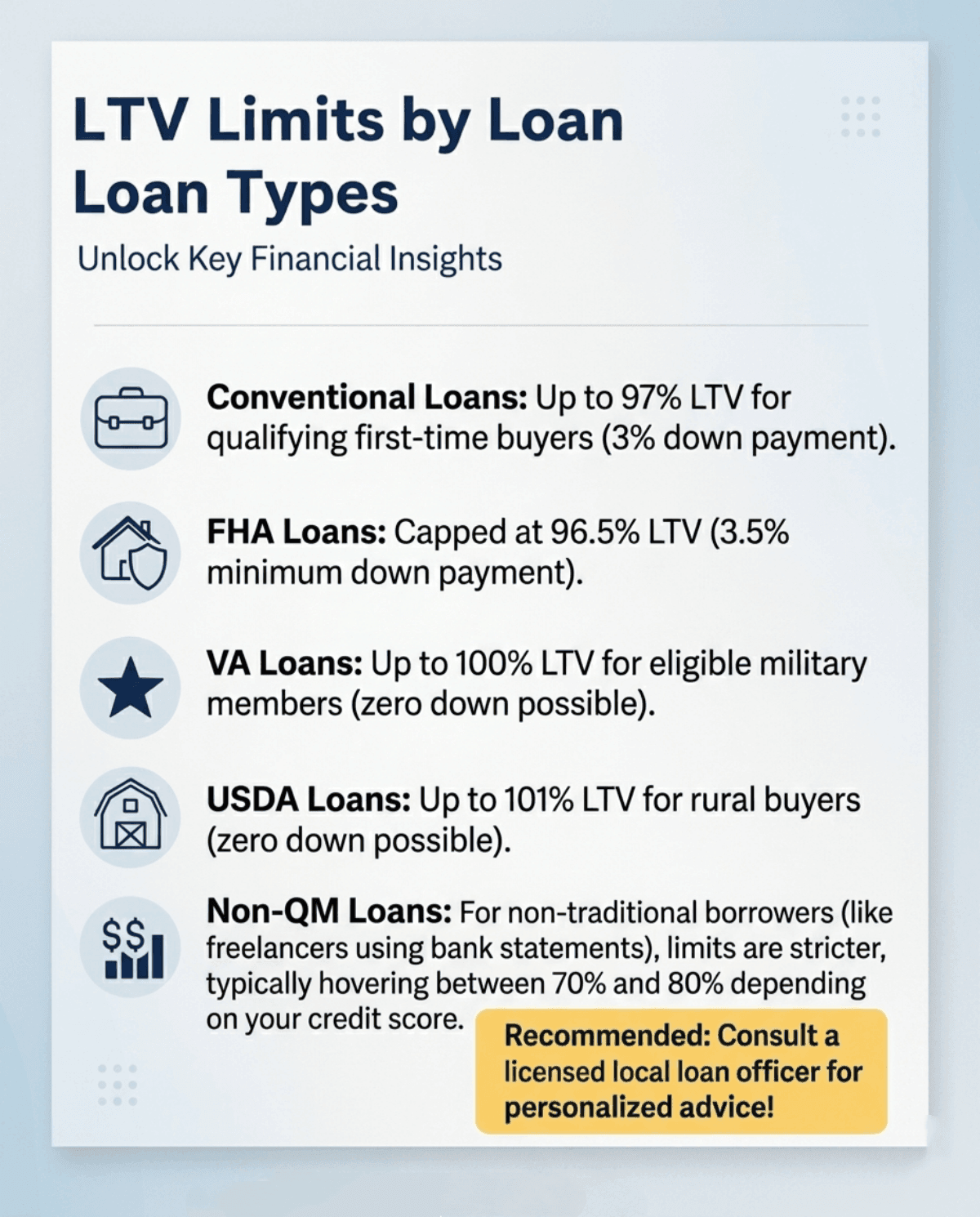

LTV Limits by Loan Types

Not every mortgage program requires you to put 20% down. Different backing agencies have vastly different maximum LTV limits:

- Conventional Loans: Up to 97% LTV for qualifying first-time buyers (3% down payment). FHA Loans: Capped at 96.5% LTV (3.5% minimum down payment).

- FHA Loans: Capped at 96.5%, meaning you need at least a 3.5% down payment.

- VA Loans: Up to 100% LTV for eligible military members (zero down possible).

- USDA Loans: Up to 101% LTV for rural buyers (zero down possible).

- Non-QM Loans: For non-traditional borrowers (like freelancers using bank statements), limits are stricter, typically hovering between 70% and 80% depending on your credit score.

Since everyone's financial profile is completely unique, I highly recommend reaching out for a free consultation with a licensed local loan officer to find the most accurate financing strategy for you.

FAQs About LTV Ratio Calculation

Q1. Does LTV use the purchase price or the appraised value?

Lenders strictly use the lesser of the two amounts. If the official appraisal comes in lower than your agreed-upon purchase price, your LTV will increase accordingly.

Q2. What is considered a good LTV ratio for a mortgage?

Generally, 80% or lower is widely considered the golden standard. Hitting this mark allows you to avoid costly private mortgage insurance and typically unlocks the most competitive interest rates.

Q3. What is CLTV and how is it different from LTV?

CLTV stands for Combined Loan-to-Value, which factors in all the mortgages on a property, such as a Home Equity Line of Credit (HELOC). A standard LTV only looks at your primary, first-lien mortgage.

Q4. How does a high LTV ratio affect my mortgage?

A higher percentage signals greater risk to the bank. Consequently, you will likely face steeper interest rates, mandatory insurance premiums, and a significantly higher chance of your application being denied.

Q5. How can I lower my LTV ratio before applying for a mortgage?

The most straightforward method is to save up a larger cash down payment. Alternatively, you can shop for a less expensive property so you don't have to borrow as much capital in the first place.

Conclusion

Grasping how to calculate your LTV is a massive stepping stone in mastering your homebuying or refinancing journey. I know the math can feel tedious, but keeping this percentage in check directly dictates your future interest rates and whether you'll be burdened with PMI.

You don't need a finance degree to get this right---just a solid grasp of your down payment and the home's true appraised worth. If you have already crunched your numbers or have lingering concerns about a potential appraisal gap, your next move is clear. Reach out to a professional mortgage advisor today to officially start your pre-approval process!