![[Explained] What is PMI in Mortgage? Everything for You](/_next/image?url=https%3A%2F%2Fdynamic-light-ab6e2536d6.media.strapiapp.com%2Fwhat_is_pmi_mortgage_banner_5bed089271.png&w=3840&q=75)

[Explained] What is PMI in Mortgage? Everything for You

When my husband and I bought our first house, saving up a 20% down payment felt absolutely impossible. So, we put down 5% instead. The catch? We had to pay Private Mortgage Insurance, or PMI. If you're like most homebuyers, you've probably noticed this pesky charge tacked onto your monthly mortgage statement and wondered what it actually is.

In short, PMI is an extra fee you pay when you buy a home with less than a 20% down payment. But don't panic. In this guide, I'll walk you through exactly how it works, what it costs, and most importantly, how you can legally get rid of it.

Key Takeaways

- It protects the lender, not you: PMI is designed to save the bank's money if you stop making payments, not yours.

- Triggered by low down payments: You'll generally pay it on conventional loans if your initial equity is less than 20%.

- It's not forever: You can actively request to cancel PMI once your home equity reaches 20% (an 80% LTV), and your lender is legally required to automatically drop it when your mortgage balance falls to 78% of the original home value.

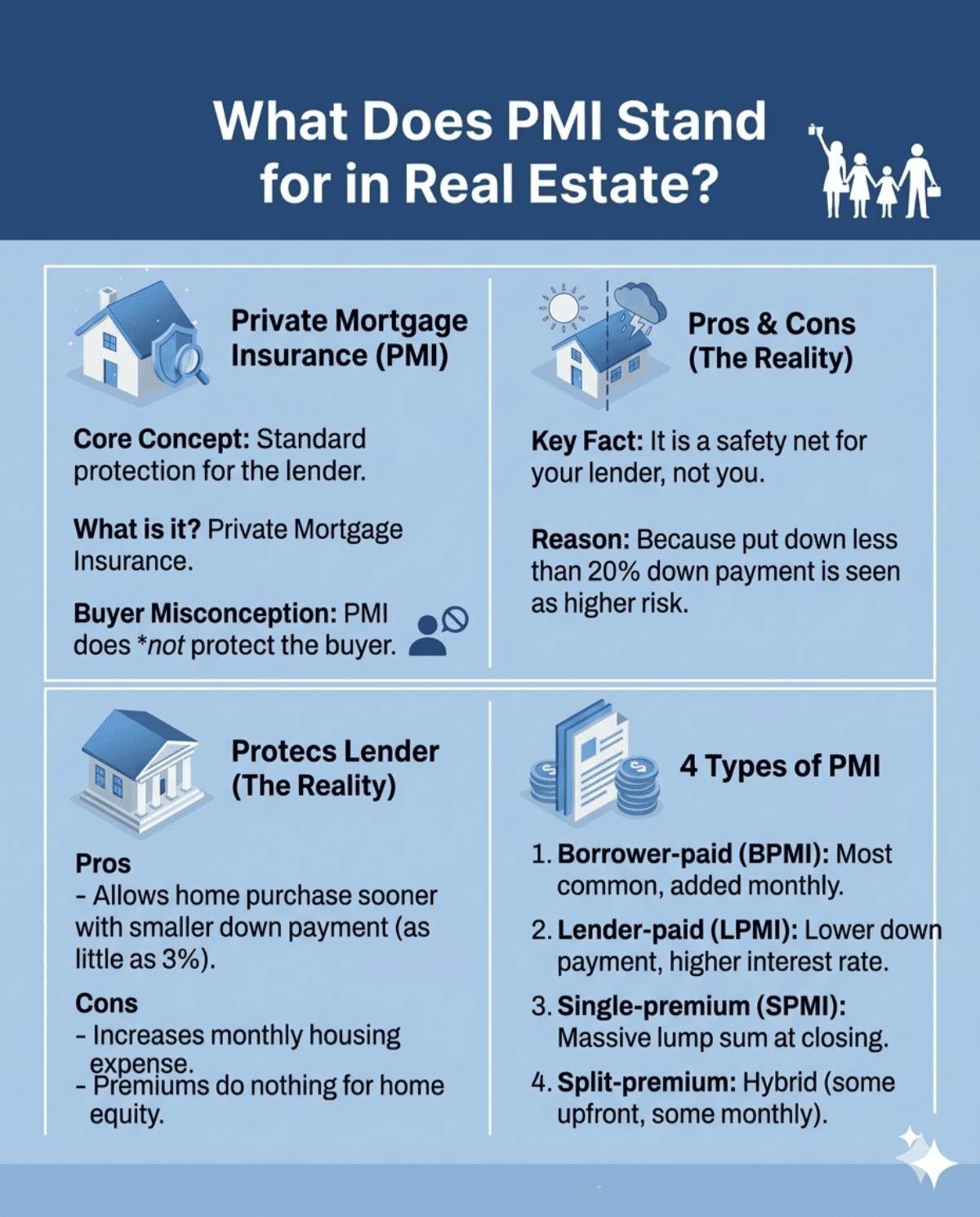

What Does PMI Stand for in Real Estate?

In real estate jargon, PMI stands for Private Mortgage Insurance. At its core, it is a safety net for your lender. Because banks view borrowers who put down less than 20% as a higher financial risk, they require you to buy this insurance policy to protect them from losing money if you ever default on your loan. I see a lot of people mistakenly believe that PMI protects the buyer in case they lose their job or face an emergency. It doesn't.

Despite that, PMI isn't completely evil. Let's look at the reality of the pros and cons:

- Pros: It allows you to buy a home much sooner. Without it, I would have had to rent for several more years to save a 20% down payment. Thanks to PMI, you can secure a conventional loan with as little as 3% down.

- Cons: It increases your monthly housing expense, and the premiums you pay do absolutely nothing to build your home equity.

There isn't just one type of PMI, either. Here are the four main types you might encounter:

- Borrower-paid PMI (BPMI): This is the most common kind. The premium is simply added to your monthly mortgage bill.

- Lender-paid PMI (LPMI): Your lender pays the insurance upfront, but in exchange, they charge you a higher interest rate for the life of the loan.

- Single-premium PMI (SPMI): You pay the entire mortgage insurance cost as a massive lump sum at closing.

- Split-premium PMI: A hybrid approach where you pay a portion upfront at closing and the rest gets baked into your monthly payments.

How Does PMI Work?

To understand how PMI works, you need to know a term called the Loan-to-Value (LTV) ratio. This is simply the mortgage amount divided by your home's appraised value. Whenever your LTV is higher than 80% on a conventional loan, the bank essentially flags your file and tacks on the insurance.

Once you close on the house, the magic (or the annoyance) happens behind the scenes. Your lender bundles your monthly PMI premium together with your principal, interest, taxes, and homeowners' insurance, commonly known as PITI. You write one check every month, and the lender routes the PMI portion into an escrow account to pay the insurance provider. It's entirely seamless, which is exactly why many homeowners just accept it as part of their standard mortgage payment without realizing they can eventually remove it.

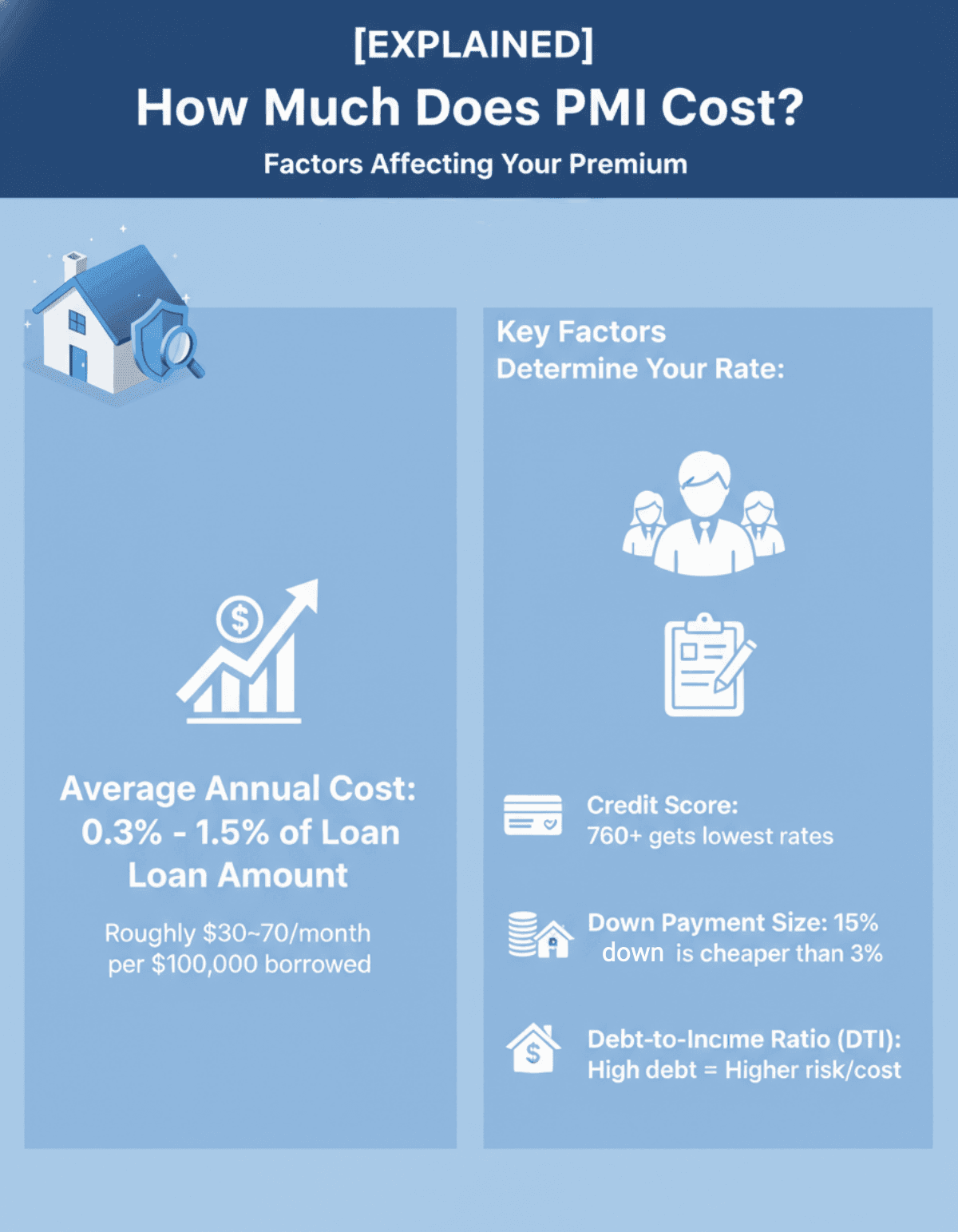

How Much Does PMI Cost?

According to Freddie Mac, the average annual cost of PMI typically ranges from about 0.3% to 1.5% of your original loan amount. In real dollars, many borrowers can expect to pay roughly $30 to $70 a month for every $100,000 you borrow, though some lenders may fall slightly outside this range.

However, your specific rate isn't chosen at random. Mortgage lenders use a few key factors to determine your exact premium:

- Credit Score: This is huge. A stellar credit score, like 760 or higher, will snag you the lowest possible rates.

- Down Payment Size: A 15% down payment will yield a much cheaper PMI rate than a 3% down payment.

- Debt-to-Income Ratio (DTI): If you already carry a lot of debt compared to your salary, lenders might charge slightly more to offset the risk.

Also Read: 3 Methods: How to Calculate Debt-to-Income Ratio for Mortgage?

How to Calculate PMI?

Figuring out your exact cost is actually pretty straightforward. You just need your total loan amount and your quoted annual PMI rate.

Here is the basic formula: Loan Amount × PMI Rate ÷ 12 Months = Monthly PMI Cost

Let me give you a real-world example. Let's say you buy a house and take out a $300,000 mortgage. Because you have a solid credit score, your lender offers you a PMI rate of 1% annually.

- First, multiply $300,000 by 1% (0.01), which equals $3,000 for the year.

- Next, divide that $3,000 by 12 months.

- Your monthly PMI payment will be $250.

Seeing $250 disappear every month definitely stings, which is exactly why you should proactively track your equity and drop the insurance as soon as you are eligible.

Also Read: 2026 Guide: How to Calculate PMI on Your Mortgage

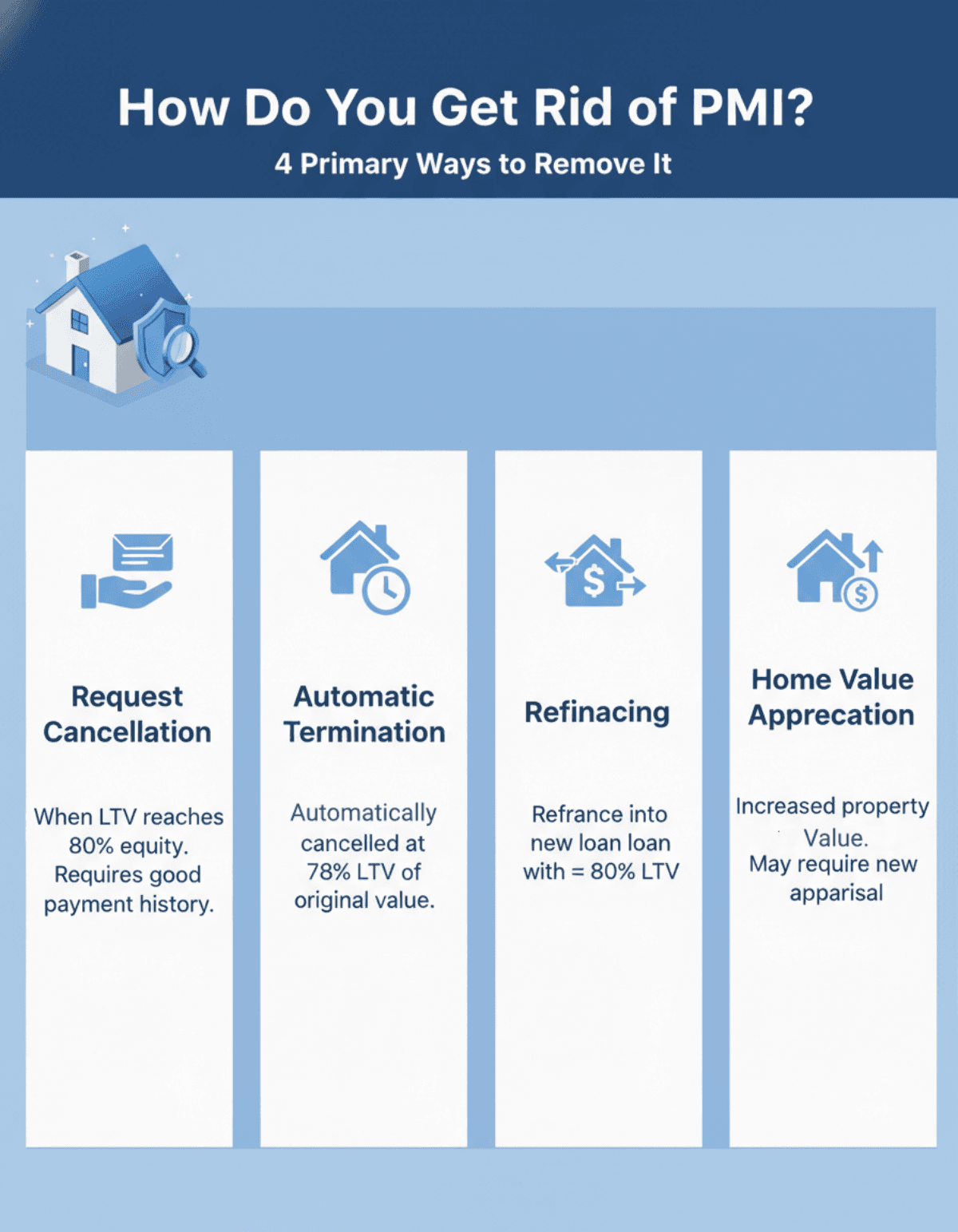

How Do You Get Rid of PMI?

This is the part I was most obsessed with after buying my home. Thanks to the federal Homeowners Protection Act, you don't have to be stuck with this fee forever. Here are the four primary ways to drop it:

- Request cancellation: Once you've paid your loan down so that your LTV reaches 80% (meaning you have 20% equity), you can write to your lender and request they remove the PMI. You must have a good payment history to do this.

- Automatic termination: If you forget to ask, the law has your back. Your lender is legally required to automatically cancel your PMI when your mortgage balance drops to 78% of the home's original appraised value.

- Refinancing: If you refinance into a conventional mortgage and your new loan amount is 80% or less of the home's current value, PMI typically vanishes.

- Home value appreciation: If your neighborhood gets hot and your property value spikes, your LTV might drop below 80% organically. You can usually pay for a new appraisal to prove this to your lender and get the PMI removed early.

PMI vs. MIP

When I was initially shopping for a mortgage, my loan officer threw both "PMI" and "MIP" at me. It's easy to get these two acronyms confused, but they belong to entirely different loan products.

- PMI (Private Mortgage Insurance): This applies exclusively to Conventional loans. As we've discussed, it goes away once you hit that magic 20% equity mark.

- MIP (Mortgage Insurance Premium): This is strictly for government-backed FHA loans.

Here is the most critical difference you need to remember: FHA MIP is significantly harder to shake. For most FHA loans with terms longer than 15 years, if you put down less than 10% at closing, the annual MIP typically stays on your bill for the entire life of the loan. If you put down 10% or more, the annual MIP usually lasts only 11 years. The only way to get rid of MIP earlier is to refinance your FHA loan into a conventional loan once you've built enough equity.

FAQs About PMI in Real Estate

Q1. How much is PMI on a $300,000 loan?

On a $300,000 mortgage, you can expect to pay anywhere from $75 to $375 per month. Your exact cost depends heavily on your credit score and down payment, but an average 1% annual rate would put you right at $250 a month.

Q2. Is it better to put 20% down or pay PMI?

If you have the cash and it won't drain your emergency fund, putting 20% down is mathematically better. However, if saving that 20% will take you five or ten years, paying a bit of PMI to buy now is often a smart move. It allows you to lock in today's housing prices and start building wealth immediately.

Q3. How long do you usually pay PMI?

If you only make the minimum standard monthly payments and your home's value stays relatively flat, it can often take a homeowner anywhere from three to seven years to reach that magic 20% equity threshold and finally drop the insurance requirement, though this timeline can vary significantly depending on your loan terms and whether you make extra payments.

Q4. Does PMI go away at 20%?

Yes, but you have to take action. When your equity reaches 20% (an 80% LTV), you have the right to request that your lender cancel and get rid of PMI. If you do nothing, the lender is not required to automatically drop it until your mortgage balance falls to 78% of the original home value.

Q5. Why should you avoid PMI?

You should avoid it if possible because it is essentially a sunk cost. The premiums you pay protect the bank, not you. The money doesn't lower your mortgage principal, it doesn't build your wealth, and it simply makes your overall housing payment more expensive every month.

Conclusion

Dealing with Private Mortgage Insurance can feel frustrating, but it's often a necessary stepping stone to homeownership. While it is an extra monthly expense, it's also the very tool that allowed me, and millions of others, to stop renting and buy a house without needing a massive pile of cash upfront.

The best thing you can do right now is grab your latest mortgage statement. Look at your current loan balance and compare it to your home's estimated value. You might be closer to that 20% equity mark than you think! Remember, you have the power to track your progress and get this fee removed.

Disclaimer: I am sharing my personal experience and research for educational purposes only. I am not a financial advisor. Please consult with a licensed mortgage broker or financial professional before making changes to your loan.

People Also Read

- Self-Employed Mortgage Guide: How to Get, Requirements

- Best First-Time Home Buyer Lenders: Find Your Perfect Match

- Best First-Time Home Buyer Loans 2026: Pick the Right Choice

- Best First-Time Home Buyer Programs: Which One to Apply?

- [Solved] How Much Does it Cost to Refinance a Mortgage?

- Best PMI Calculators: Estimate Your Private Mortgage Insurance

- Mortgage Interest Rate vs. APR: What's the Difference?