Best First-Time Home Buyer Loans 2026: Pick the Right Choice

Are you feeling entirely overwhelmed by the sheer number of mortgage options out there? I get it. When I bought my first house, trying to decode lending jargon almost made me quit before I started. Choosing the wrong loan structure can literally cost you thousands of dollars in hidden fees and unnecessary interest over the years. But don't stress---I'm here to simplify the best first-time home buyer loans for 2026.

Better yet, you can skip the endless browser tabs by using the Bluerate AI Agent. It's totally free, offers instant rate comparisons, and directly connects you with trusted local loan officers so you can move forward with complete confidence.

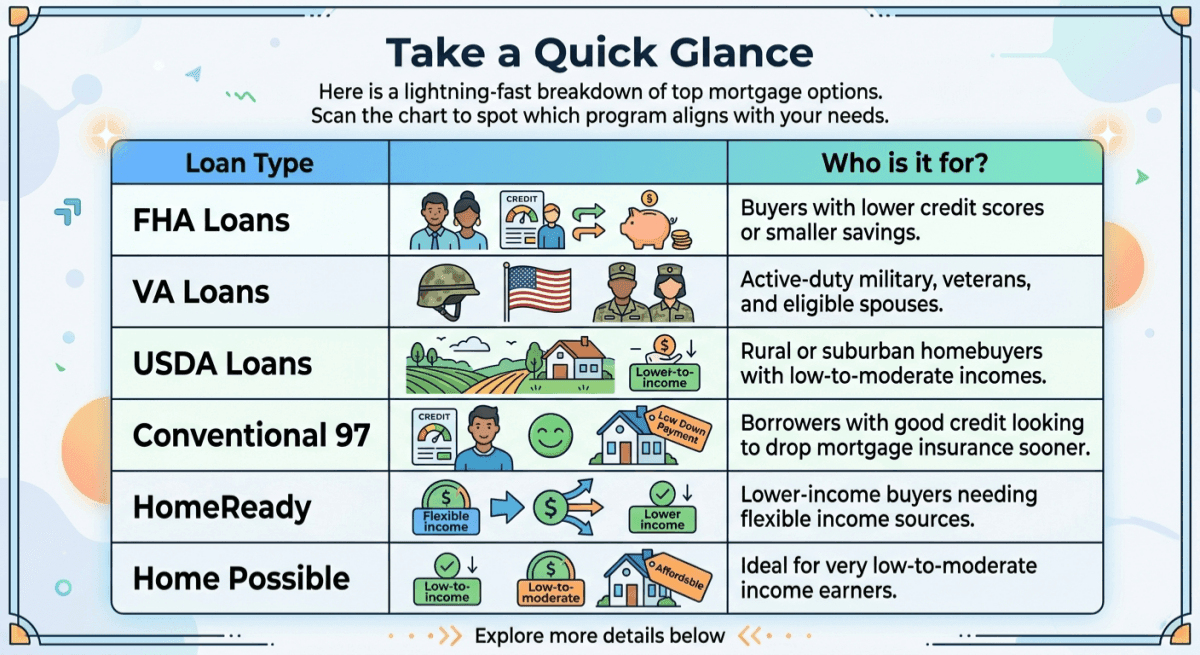

Take a Quick Glance

If you're short on time, here is a lightning-fast breakdown of the top mortgage options this year. I've put together this handy comparison table so you can instantly spot which program aligns with your current financial reality.

Also Read:

- Best First-Time Home Buyer Programs: Which One to Apply?

- Best First-Time Home Buyer Lenders: Find Your Perfect Match

Every situation is unique. Scan the chart above to find your closest match, then dive into the detailed breakdowns below to see exactly what it takes to qualify.

Every situation is unique. Scan the chart above to find your closest match, then dive into the detailed breakdowns below to see exactly what it takes to qualify.

Top First-Time Homebuyer Loans in 2026

The 2026 real estate market is still adapting to rates hovering around 6.4%. Because of this, picking a financing path that stretches your dollar is more crucial than ever. Let's break down the heavy hitters.

FHA Loans

Best for: Buyers with less-than-perfect credit and smaller down payments.

I always tell my clients not to let a few past financial hiccups keep them from homeownership. FHA loans are backed by the Federal Housing Administration, meaning the government essentially insures the lender against loss. This safety net translates to incredibly forgiving qualification standards for first-time buyers. The biggest perk? You don't need a massive cash reserve or an elite credit history to get your foot in the door. It's an incredibly accessible stepping stone into the housing market.

Requirements:

- Minimum Credit Score: 580 or higher for 3.5% down payment (maximum LTV financing). Scores between 500-579 qualify with a 10% minimum down payment.

- Minimum Down Payment: Just 3.5% if your score is 580 or higher. If it's below that, expect to put down 10%.

- DTI Limit: Generally capped around 43%, though some lenders might stretch to 50% if you have strong compensating factors like a hefty savings account.

- Mortgage Insurance: You will pay both an upfront Mortgage Insurance Premium (MIP) and an annual fee, regardless of your down payment size.

VA Loans

Best for: Active-duty military members, veterans, and eligible surviving spouses wanting zero down.

Serving our country comes with profound benefits, and the VA loan is arguably one of the greatest financial tools available to military families. Guaranteed by the Department of Veterans Affairs, this program is designed specifically to reward your service by removing the biggest barriers to buying a house. I've watched countless veterans use this exact route to purchase beautiful properties without draining their life savings. The standout advantage here is undeniably the ability to finance 100% of the home's purchase price while completely bypassing monthly mortgage insurance.

Requirements:

- Minimum Credit Score: No VA minimum. Most lenders require 620+, though some accept 580 with strong factors.

- Minimum Down Payment: Absolutely 0%. You can buy a home without putting a single penny down.

- DTI Limit: Lenders generally prefer a debt-to-income ratio of 41% or lower, but they also heavily weigh your residual income (the cash left over after paying bills).

- Mortgage Insurance: No monthly PMI is required! However, you will typically need to pay a one-time VA funding fee, which can be rolled directly into the loan amount.

USDA Loans

Best for: Low-to-moderate-income buyers looking to settle down in rural or eligible suburban areas.

Don't let the word "rural" fool you. You don't have to buy a working farm to qualify for a USDA loan. Backed by the U.S. Department of Agriculture, this initiative is meant to encourage development outside of major metropolitan hubs. I frequently surprise clients by showing them that many quiet suburban neighborhoods just outside city limits actually qualify for this program. It's an incredible avenue for first-time homebuyers who want space and affordability, offering a rare zero-down-payment structure for those who fit the location and income brackets.

Requirements:

- Minimum Credit Score: No USDA minimum. Most lenders require 620+, with 640+ for automated GUS approval.

- Minimum Down Payment: 0%. Similar to the VA program, you can finance the entire purchase price.

- DTI Limit: Typically strict. The standard limits are 29% for housing costs and 41% for total debt, though automated approvals might allow slightly higher ratios.

- Mortgage Insurance: There is no traditional PMI, but you will pay an upfront guarantee fee and a small annual fee built into your monthly payments, which is usually cheaper than FHA alternatives.

Conventional 97

Best for: Borrowers with solid credit profiles who want to avoid permanent mortgage insurance.

When people think of "traditional" mortgages, they usually imagine needing 20% down. The Conventional 97 program shatters that myth. Backed by government-sponsored enterprises like Fannie Mae and Freddie Mac, this loan allows you to finance 97% of the property value. In my experience, this is the gold standard if your credit is in good shape because it offers a crucial exit strategy that FHA loans lack: the ability to cancel your mortgage insurance once you build enough equity. It's a smart, long-term wealth-building choice.

Requirements:

- Minimum Credit Score: You'll need at least a 620, though locking in the most competitive interest rates usually requires a 740 or above.

- Minimum Down Payment: Just 3% of the purchase price. Plus, that entire amount can come from gifted funds from a family member.

- DTI Limit: Usually capped at 43%, but strong credit or significant cash reserves might push the allowable limit up to 50%.

- Mortgage Insurance: Private Mortgage Insurance (PMI) is mandatory since you are putting down less than 20%. However, unlike an FHA loan, you can request to drop it once your loan balance falls to 80% of the home's original value.

HomeReady

Best for: Lower-income buyers who need flexibility with their qualifying income sources.

Created by Fannie Mae, the HomeReady program was specifically engineered to help modern, diverse households achieve homeownership. If you live in a multi-generational home or have working adults living with you who aren't on the mortgage, this loan can be a game-changer. I love recommending this option because it features highly reduced mortgage insurance costs compared to standard conventional loans. It acknowledges that today's financial realities are complex and offers a pathway for those earning below the median income in their target neighborhood.

Requirements:

- Minimum Credit Score: A 620 is the baseline, but hitting 680 or higher will unlock significantly better pricing and lower fees.

- Minimum Down Payment: Only 3%.

- DTI Limit: The standard maximum is 45%, but you might be able to push it to 50% with a strong automated underwriting approval.

- Mortgage Insurance: PMI is required, but it comes at a steeply discounted rate compared to normal conventional loans. Also, it's cancellable once you reach 20% equity.

- Income Limits: Your total qualifying income cannot exceed 80% of the Area Median Income (AMI) for the property's specific location.

Home Possible Loans

Best for: Very low-to-moderate-income earners looking for accessible conventional financing.

Freddie Mac's Home Possible program is the direct cousin to Fannie Mae's HomeReady. The two are incredibly similar, but Home Possible shines when it comes to specific underwriting flexibilities, like allowing "sweat equity" (where your DIY home repairs count toward your down payment). It's an empowering option. I've seen buyers who thought they were entirely priced out of the market use this program to finally get the keys to their first place. It is distinctly tailored for those who are struggling to save large chunks of cash while paying high rent.

Requirements:

- Minimum Credit Score: 660 is typically required for a standard approval, though those without a usable credit score can sometimes qualify under special manual underwriting rules.

- Minimum Down Payment: Just 3%, which can be entirely sourced from down payment assistance programs (DPA) or family gifts.

- DTI Limit: Generally capped at around 43%, though exceptions exist based on your overall financial strength.

- Mortgage Insurance: Reduced PMI applies, making your monthly overhead much cheaper. Like other conventional options, it eventually falls off once you hit the magical 80% loan-to-value ratio.

- Income Limits: Like HomeReady, your earnings cannot be higher than 80% of the local Area Median Income.

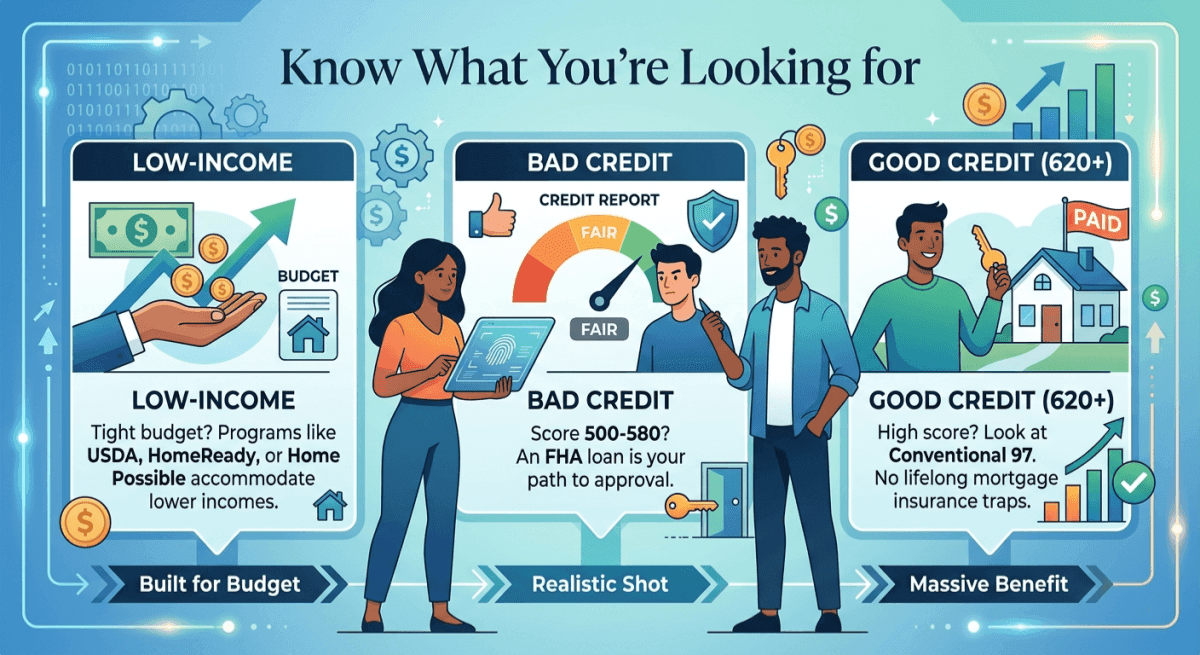

Know What You're Looking for

Choosing the right path isn't about finding the "best" overall loan. It's about finding the perfect fit for your specific financial fingerprint. Let's reverse-engineer the process based on where you stand today:

- Low-income: If your paycheck feels stretched, look heavily into USDA or the HomeReady/Home Possible programs. They are literally built to accommodate tighter budgets.

- Bad credit: Don't panic. An FHA loan is your best friend here. With scores as low as 500 to 580, you still have a very realistic shot at getting approved.

- Good credit (620+): Lean toward the Conventional 97. The massive benefit here is that you won't be trapped paying lifelong mortgage insurance.

- Self-employed: Be prepared for a bit more paperwork. You might need to explore Bank Statement Loans or ensure you have two completely clean, solid years of tax returns to hand over.

Also Read:

- Best No-Income Verification Mortgage Loans: Which is Best for You?

- Best Mortgage for Low Income: Which One for You?

- Best Bridge Loan Lenders for Homebuyers and Investors

- Best Mortgage Loans for Self-Employed: Which to Pick?

- Best Asset Depletion Lenders: Top Rank Here

What are the First-Time Homebuyer Loan Requirements?

No matter which specific product you ultimately choose, every bank and lender on the planet will evaluate you based on three or four core pillars. They just want to know you can reliably pay them back.

- Credit History: This isn't just about your score. Lenders look at your track record of paying debts on time.

- Income & Employment Stability: Usually, a steady two-year history of income and employment stability (not necessarily the same industry).

- Debt-to-Income (DTI) Ratio: This math compares your gross monthly income against your minimum debt payments. Keep your monthly debts low to boost your buying power.

- Down Payment & Closing Costs Funds: You need to prove where your cash is coming from. Happily, most programs allow you to use "gift money" from relatives or down payment assistance (DPA) grants.

Also Read:

- Must Read: Minimum Down Payment for House First-Time Buyer

- 3 Methods: How to Calculate Debt-to-Income Ratio for Mortgage?

How to Get a Mortgage Loan as a First-Time Homebuyer?

Navigating this journey doesn't have to be a headache. If you take it step-by-step, it's actually a highly logical process.

- Evaluate your financial health. Pull your credit reports, tally up your monthly debts, and be brutally honest about your comfortable budget. Don't just look at what a bank says you can afford. Look at what your lifestyle can genuinely sustain.

- Shop around for rates and lenders. This is where most people leave money on the table. Finding the right loan officer (LO) is the absolute secret to securing a great rate. Instead of making twenty phone calls, just use the Bluerate AI Agent. It seamlessly compares rates and matches you with top-tier local experts---all for free, saving you massive amounts of time.

- Get Pre-approved. Do not skip this. A pre-approval letter proves to sellers that you are a serious buyer with verified funds. In 2026's market, no one will accept an offer without one.

- House hunt and officially apply. Once your offer is accepted, you'll convert your pre-approval into a formal application. You'll lock in your interest rate, order an appraisal, and head toward the closing table!

FAQs About Best First-Time Homebuyer Loans

Q1. What are first-time home buyer loans with zero down?

The most popular zero-down mortgages are VA Loans for eligible military personnel and USDA Loans for those purchasing in designated rural or suburban areas. If you don't fit into those categories, don't worry. You can frequently combine a traditional 3% down conventional loan with local Down Payment Assistance (DPA) grants to achieve a true "no money out of pocket" purchase.

Q2. How to get first-time home buyers $7,500 government grants?

While buzz about a broad federal $7,500 grant frequently circulates, true assistance usually happens at the local level or through specific banks. For example, certain lenders offer an America's Home Grant up to $7,500 for closing costs in select markets. I strongly suggest contacting a local LO through your State Housing Finance Agency to discover legitimate, localized grants available right now.

Q3. How much income to qualify for a $200,000 mortgage?

Assuming a current interest rate around 6.4%, and a 30-year fixed term, your basic monthly payment (with taxes and insurance) sits near $1,500. Under the standard 28% front-end debt-to-income rule, you would generally need a gross annual salary between $60,000 and $70,000. Keep in mind, this estimate assumes you aren't carrying massive auto loans or heavy student debt.

Q4. What salary do you need for a $400,000 mortgage?

Using current 2026 market averages near 6.2% with a 20% down payment, expect your monthly housing obligation to be roughly $3,000 once taxes and insurance are factored in. Applying typical lending DTI limits, a safe estimated salary range is about $115,000 to $130,000 per year. Your exact requirement will fluctuate heavily based on current interest rates and your personal monthly debts.

Also Read:

- How Much Income Needed for a 400K Mortgage? Know Your Affordability

- Read First: How Much Income Needed for 500K Mortgage?

- Solved - How Much Income Needed for 300K Mortgage?

Conclusion

Wrapping things up, figuring out the distinct differences between FHA, VA, USDA, and conventional options is merely your first step toward getting the keys. The landscape of home financing is constantly shifting, and tackling it solo is a recipe for unnecessary stress. The real secret to a smooth transaction is having a dedicated mortgage expert in your corner who understands your local market inside and out.

Don't let analysis paralysis hold you back. Take action today. I highly encourage you to utilize the Bluerate to kick off your homebuying journey. It costs absolutely nothing to evaluate your profile, instantly compare rates side-by-side, and get matched with an exclusive, highly-rated local Loan Officer. Stop guessing and start moving toward your dream home with ease!