Best No-Income Verification Mortgage Loans: Which is Best for You?

I know the frustration firsthand. You have excellent credit, a thriving business, or substantial savings, yet traditional banks slam the door in your face because your tax returns show "losses" due to legitimate deductions. It feels unfair, but there is a solution.

Let's clear up a misconception immediately: "No-Income Verification" doesn't mean no proof of ability to repay. In the professional mortgage world, we call these Non-QM (Non-Qualified Mortgage) or Alt-Doc Loans. Instead of W-2s and tax returns, lenders use real-world data, like cash flow or assets, to approve you. If you are feeling overwhelmed by the complexity of these options, I suggest getting a free consultation with a professional loan officer to navigate your specific scenario before applying.

Top No-Income Verification Mortgage Types

Why do so many loan types exist? Simply put, the modern economy has outpaced traditional banking models. One size no longer fits all. Whether you are a real estate mogul, a freelance graphic designer, or a retiree, there is a specific no-income verification loan designed for your unique financial footprint. While these loans often carry slightly higher rates than conventional mortgages, they are critical tools that unlock homeownership for creditworthy buyers who don't fit the standard "9-to-5" mold.

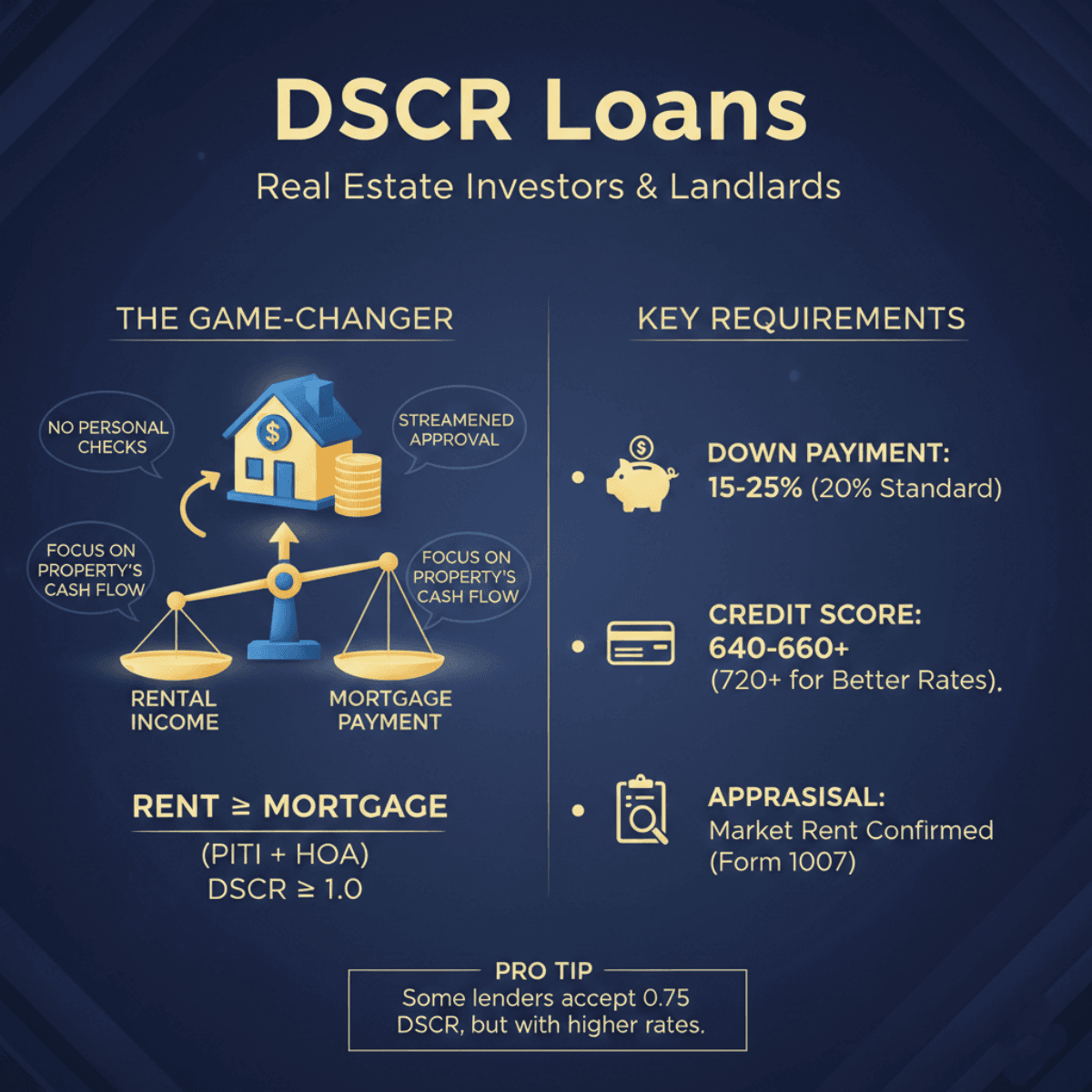

DSCR Loans

Best for: Real Estate Investors (REIs) and Landlords looking to scale their portfolios without personal income constraints.

In my experience working with investors, the DSCR (Debt Service Coverage Ratio) loan is a game-changer. It is arguably the most streamlined loan in the Non-QM marketplace because it completely separates your personal finances from the transaction. The lender doesn't care about your personal debt-to-income ratio or your tax returns. Their sole focus is the property itself: Can this house generate enough rent to pay for itself? If the answer is yes, you are likely approved. It treats the property as a standalone business entity.

Requirements

-

The Ratio Math: You typically need a DSCR ratio of 1.0 or higher. This means the monthly rental income must be equal to or greater than the monthly mortgage payment (including principal, interest, taxes, insurance, and HOA).

-

Pro Tip: Some aggressive lenders accept a ratio as low as 0.75, but expect higher interest rates for those.

-

Down Payment: Typically 15% to 25% down, depending on credit score, DSCR ratio, and property type. 20% is standard for most investors.

-

Credit Score: A score of 640–660+ is standard, though better rates unlock at 720+.

-

Appraisal: The appraiser must confirm the market rent schedule (Form 1007) to validate the income potential.

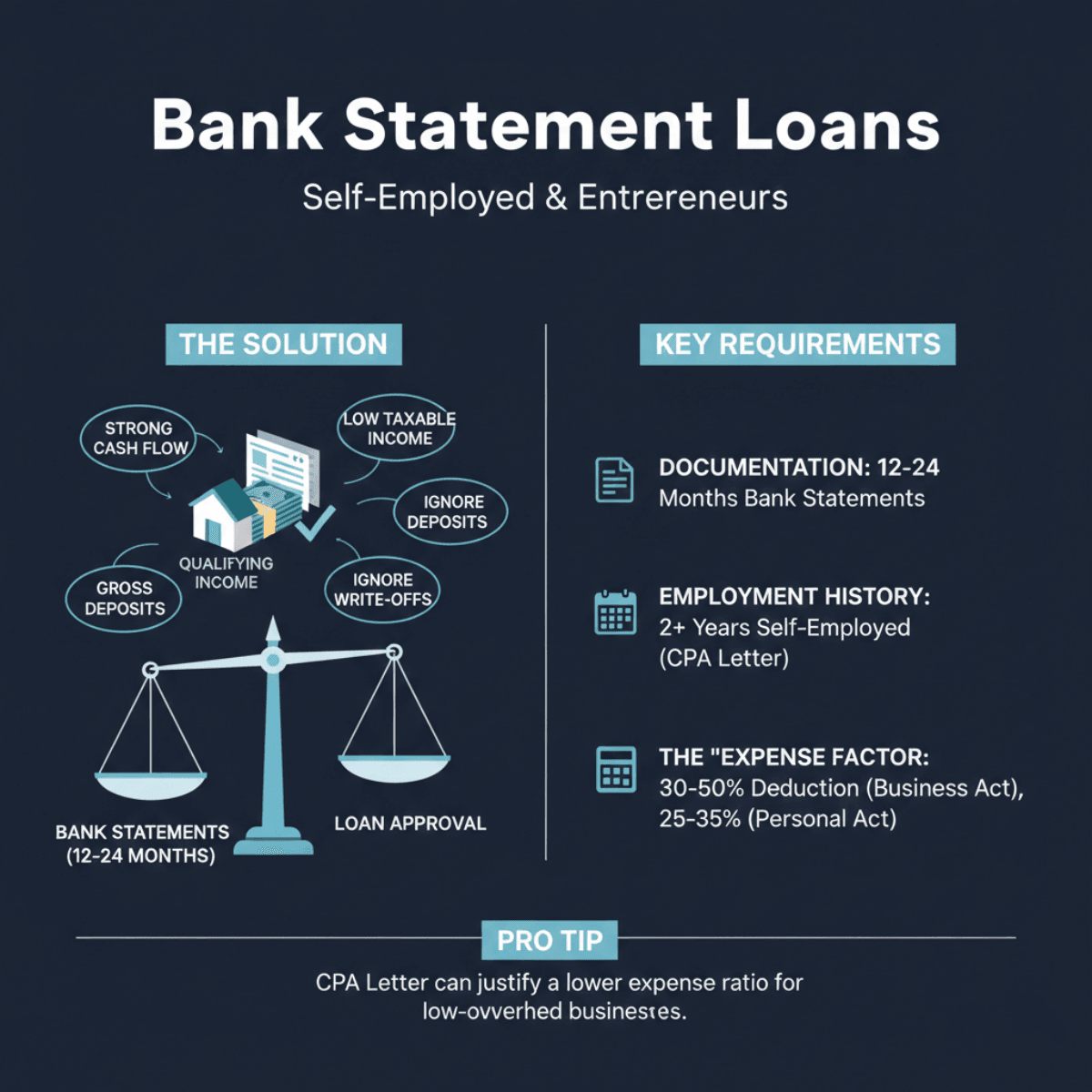

Bank Statement Loans

Best for: Self-employed business owners, Entrepreneurs, and Gig Workers with strong cash flow but low taxable income.

This is the most popular solution for the self-employed. If you have a good accountant, your tax returns likely show a low net income to minimize your tax bill. While this makes the IRS happy, it ruins your chances for a conventional loan. Bank Statement Loans solve this by looking at your gross deposits rather than your net income. Lenders review 12 to 24 months of your personal or business bank statements to calculate your "qualifying income" based on the cash actually hitting your account, ignoring those heavy paper write-offs.

Requirements

-

Documentation: You must provide 12 or 24 months of consecutive bank statements.

-

Employment History: You typically need to prove you've been self-employed for at least 2 years (sometimes a CPA letter is required to verify business ownership).

-

The "Expense Factor": Lenders typically apply a 30-50% deduction to gross deposits from business bank statements (often 40%) to estimate net income, or 25-35% for personal statements. A CPA letter can justify a lower ratio for low-overhead businesses.

If your business has low overhead, like a consultant working from home, your CPA can write a letter stating your expense ratio is lower (e.g., 20%), allowing you to qualify for a much larger loan.

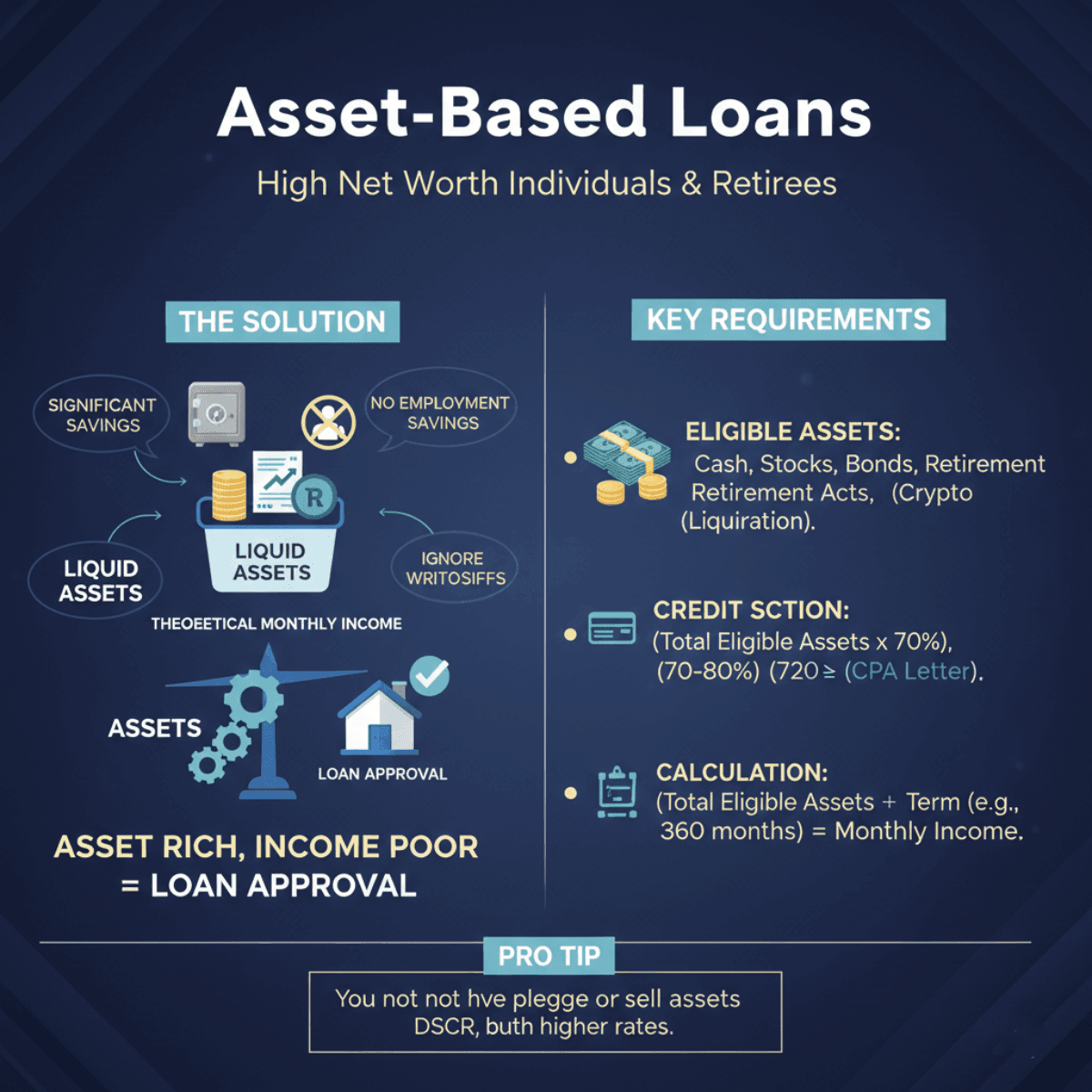

Asset-Based Loans

Best for: High Net Worth Individuals (HNWIs), Retirees, or those with significant savings but no current employment income.

What if you have $2 million in the bank but no job? Ironically, a traditional bank might still reject you. Asset-Based Loans (also known as Asset Depletion loans) utilize a logic that just makes sense: they use your liquid assets to calculate a theoretical monthly income. You do not have to pledge these assets as collateral or sell them. The lender simply uses a formula to determine your ability to pay. This is ideal for wealthy individuals who are "asset rich but income poor" on paper.

Requirements

-

Eligible Assets: Cash, stocks, bonds, and retirement accounts (though retirement accounts are often discounted to 70-80% of value to account for potential withdrawal penalties). Crypto is becoming accepted but often requires liquidation.

-

Calculation: Lenders typically use (Total Eligible Assets × 70%) ÷ a set term (e.g., 360 months for a 30-year loan or 84/60 months), yielding your 'monthly income' without depleting principal.

-

Asset Minimum: You generally need assets totaling at least 100% to 110% of the loan amount, plus reserves.

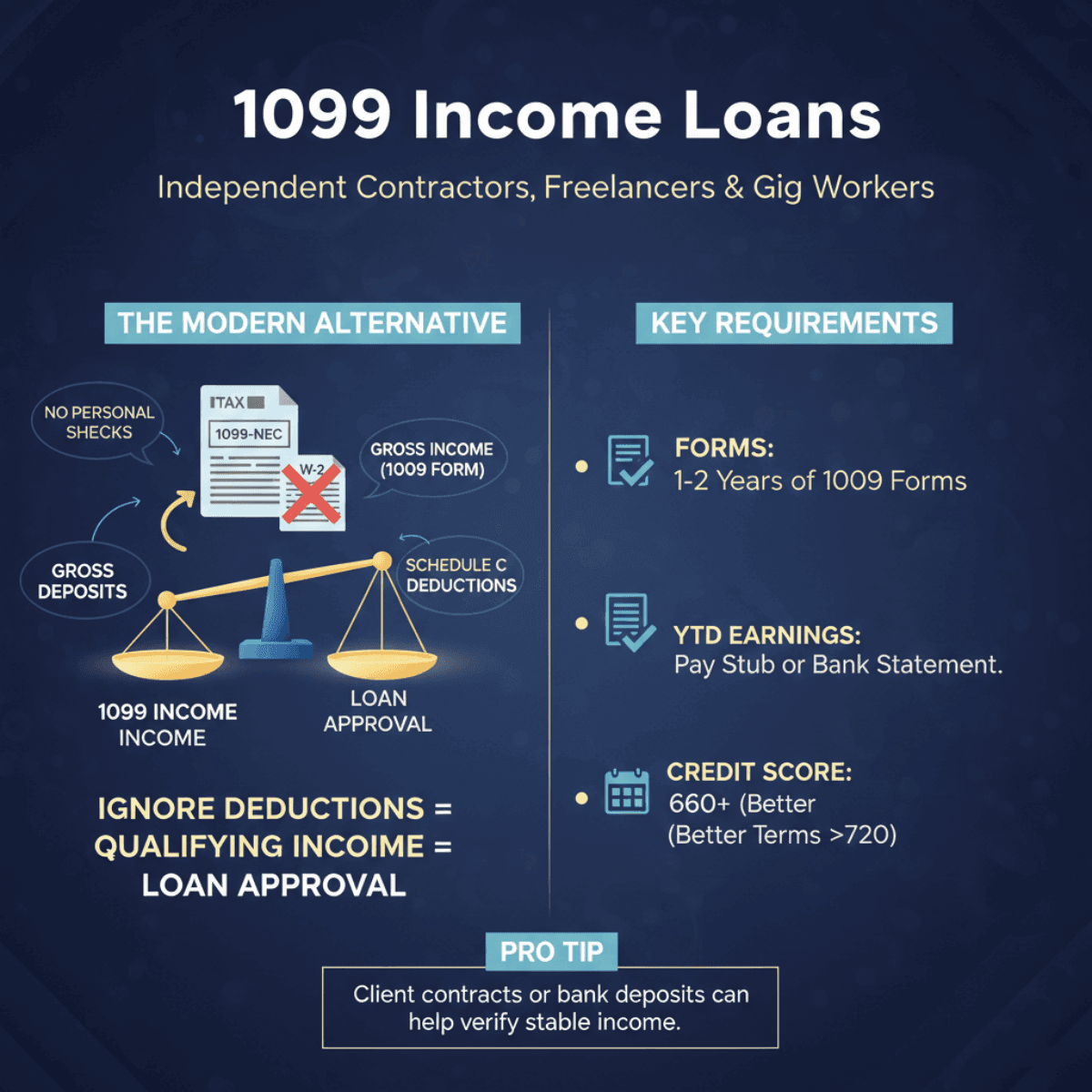

1099 Income Loans

Best for: Independent Contractors, Real Estate Agents, Freelancers, and Gig Economy workers (Uber/Lyft).

In the past, people might have referred to "NINJA" loans, but those risky products are largely extinct. The modern, responsible alternative for contract workers is the 1099 Income Loan. This is specifically designed for anyone who receives a Form 1099-NEC at the end of the year instead of a W-2. Similar to the bank statement loan, the lender looks at the Gross Income shown on your 1099 form. This is a massive advantage because it bypasses the heavy schedule C deductions that usually drag down your qualifying income on a standard mortgage application.

Requirements

-

Forms: You usually need to provide the most recent 1 or 2 years of 1099 forms.

-

Year-to-Date (YTD) Earnings: Lenders will often ask for a pay stub or a bank statement showing current YTD earnings to prove your income is stable and continuing.

-

Credit Score: Minimum credit scores usually start around 660, with better terms available for higher scores.

-

Client Verification: In some cases, a CPA letter, client contracts, or bank deposits confirm ongoing work. No traditional employer verification is needed.

Considerations Before Applying for a No-Income Verification Mortgage

Before you rush to apply, I need to offer a reality check. These loans are specialized tools, and they come with trade-offs that you must be comfortable with. Here is what you need to weigh:

-

Higher Interest Rates: Because lenders are taking on more risk by not viewing tax returns, expect interest rates to be 0.5% to 2.5% higher than standard conventional loans.

-

Larger Down Payments: Expect 10-25% down minimum (e.g., 10-15% possible for strong credit on Bank Statement loans, 20%+ for DSCR), with no zero-down options.

-

Prepayment Penalties: Especially on DSCR (investment) loans, watch out for clauses that charge you a fee if you sell or refinance the home within the first 1-3 years.

-

Reserves: Lenders often require you to show you have 3 to 6 months of mortgage payments left in the bank after closing.

FAQs About Best No-Income Verification Mortgage Loans

Q1. Can you get a mortgage with no income verification?

Yes. However, it is not "zero verification." It is actually "alternative verification." Lenders won't ask for your tax returns (1040s), but they will verify your ability to repay using other data points like bank statement deposits, liquid assets, or the rental income potential of the property you are buying.

Q2. Are No-Income Verification loans safe?

Yes, modern Non-QM loans are much safer than the subprime loans of 2008. Today, they are regulated by the Ability-to-Repay (ATR) rule. Lenders must make a good-faith determination that you can afford the loan based on your assets or cash flow. They are safe tools for financially stable borrowers who simply lack standard documentation.

Q3. How much down payment is needed for a no-income verification mortgage?

You should plan for a down payment between 10% and 25%. The exact amount depends heavily on your credit score and the loan type. For example, a borrower with a 740 credit score might only need 10-15% down for a Bank Statement loan, whereas a DSCR loan typically requires a hard 20% minimum.

Q4. What do I put for proof of income if I have no income?

You never put "no income." Instead, you provide the source of your funds. If you are applying for a Bank Statement loan, your proof is your monthly deposits. If you are applying for an Asset-Based loan, your proof is your brokerage or savings account statements. Honesty regarding the source of funds is critical for approval.

Final Word

Navigating the mortgage landscape without a W-2 can feel isolating, but you are not out of options. To recap:

-

Investors should look at DSCR Loans.

-

Business Owners are best served by Bank Statement Loans.

-

Contractors should utilize 1099 Loans.

-

Wealthy Individuals can leverage Asset-Based Loans.

The biggest challenge is that Non-QM lenders are fragmented. You can't just walk into a Chase or Wells Fargo for these. Finding the right lender with the specific guidelines that match your financial puzzle is difficult.

This is where technology bridges the gap. Instead of guessing, I recommend you visit Bluerate. You can chat directly with the Bluerate AI Agent. By simply describing your situation (e.g., "I'm a freelancer with $8,000 in monthly deposits"), the AI will analyze your profile, recommend the best loan type, and even match you with local loan officers to compare rates.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Mortgage guidelines change frequently. Please consult with a qualified mortgage professional for your specific situation.