A Detailed Guide: How to Get Preapproved for a Mortgage?

When I bought my first home, I quickly learned that browsing real estate apps is the fun part, but securing financing is the real first step. Why? Because in today's highly competitive market, a mortgage preapproval is your golden ticket. It proves to sellers that you are a serious buyer and gives you a crystal-clear picture of your actual budget.

Instead of guessing what you can afford, you have hard facts. In this detailed guide, I'll walk you through exactly how to get preapproved. The best part? You can start right now by finding a trusted, local loan officer to guide you.

Step-by-Step Guide: How to Get Preapproved for a Mortgage?

Getting that preapproval letter might seem intimidating, but it's actually a highly standardized process. If you follow these five straightforward steps, you'll breeze through the paperwork and be ready to make a winning offer on your dream home in no time.

STEP 1. Find a Mortgage Lender

Let me be honest: the hardest part for me was just figuring out who to talk to. The market is flooded with options, and if you start randomly requesting rate quotes online, your phone will blow up with telemarketer calls. That's why I highly recommend starting with Bluerate. It's an all-in-one platform that securely connects you directly with NMLS-licensed loan officers in your specific area.

What makes Bluerate a true game-changer is the Bluerate AI Agent. Think of it as your 24/7 personal mortgage assistant. You just hop into a simple AI Chat, answer a few basic questions about your location and financial goals, and it instantly matches you with the right expert.

Here are a few ways this platform makes your life easier:

-

Smart AI Agent Matching: Analyzes your financial profile to precisely match you with the right loan officer without feeling judged.

-

Privacy First (No Spam): Shop anonymously and keep your data safe. You choose who to contact.

-

Real-Time Verified Rates: Compare accurate rates from over 30+ lenders in seconds.

-

Top Local Experts: Easily find pros specializing in Conventional, FHA, VA, or Non-QM loans.

-

Tailored for Unique Needs: Perfect for first-time buyers or self-employed individuals needing 1099/LLC loan experts.

-

Fast Track: Get pre-qualified 2.5x faster to help you close 20% sooner.

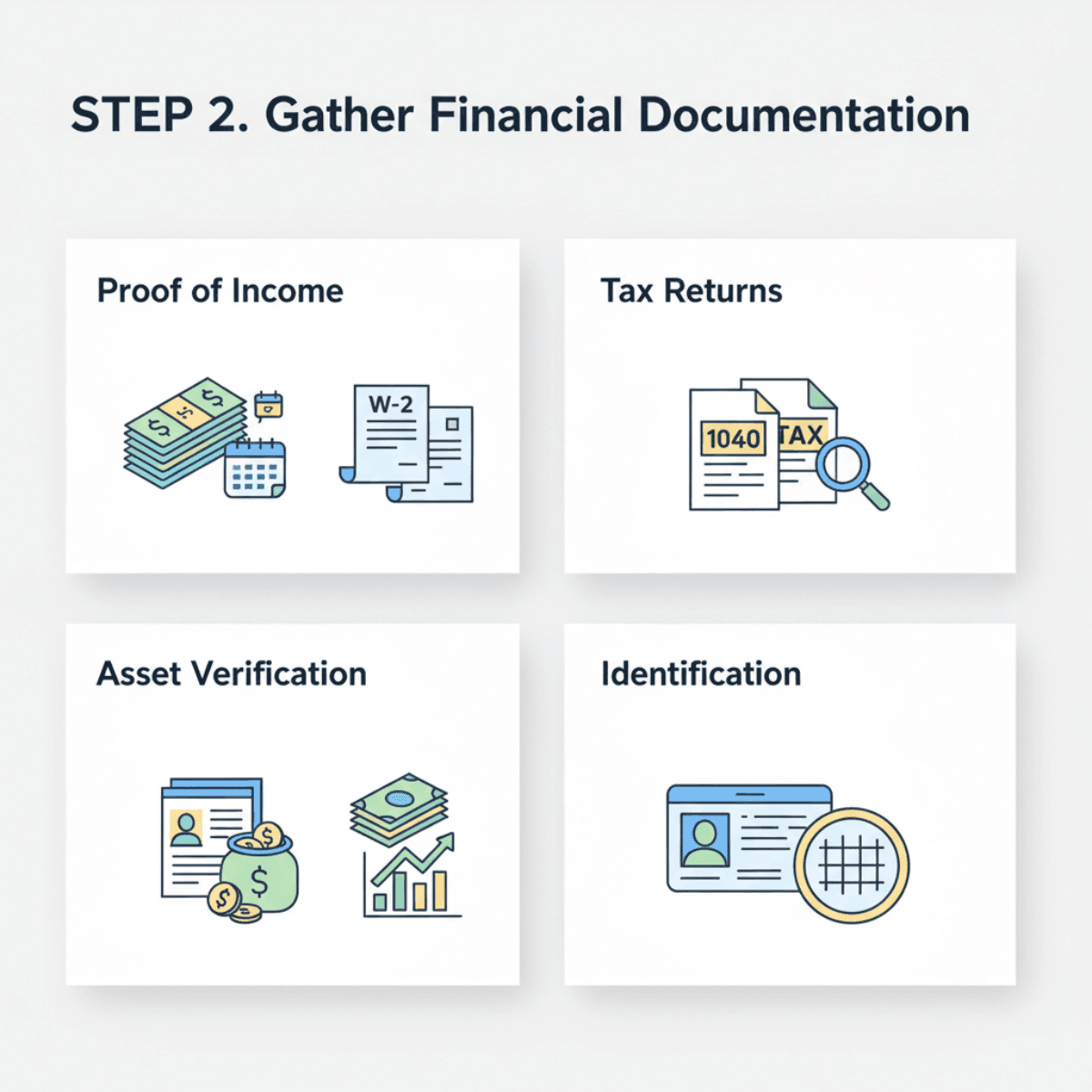

STEP 2. Gather Financial Documentation

Once you've found your loan officer, they're going to need proof of your financial health. I always tell people to treat this like packing for a road trip. The better prepared you are, the smoother the ride. Having your paperwork organized will significantly speed up your preapproval timeline.

Here is the standard checklist of documents you'll need:

-

Proof of Income: Your most recent pay stubs (usually covering the last 30 days) and W-2 forms from the past two years.

-

Tax Returns: Your personal federal tax returns for the last two years.

-

Asset Verification: Bank statements, retirement accounts, and investment records for the last 60 days to prove you have funds for a down payment.

-

Identification: A valid government ID and your Social Security number.

If you are self-employed, prepare your 1099s and profit-and-loss statements. Traditional banks can be tough on freelancers, but Bluerate can easily connect you with Non-QM experts specifically trained to handle these unique income scenarios.

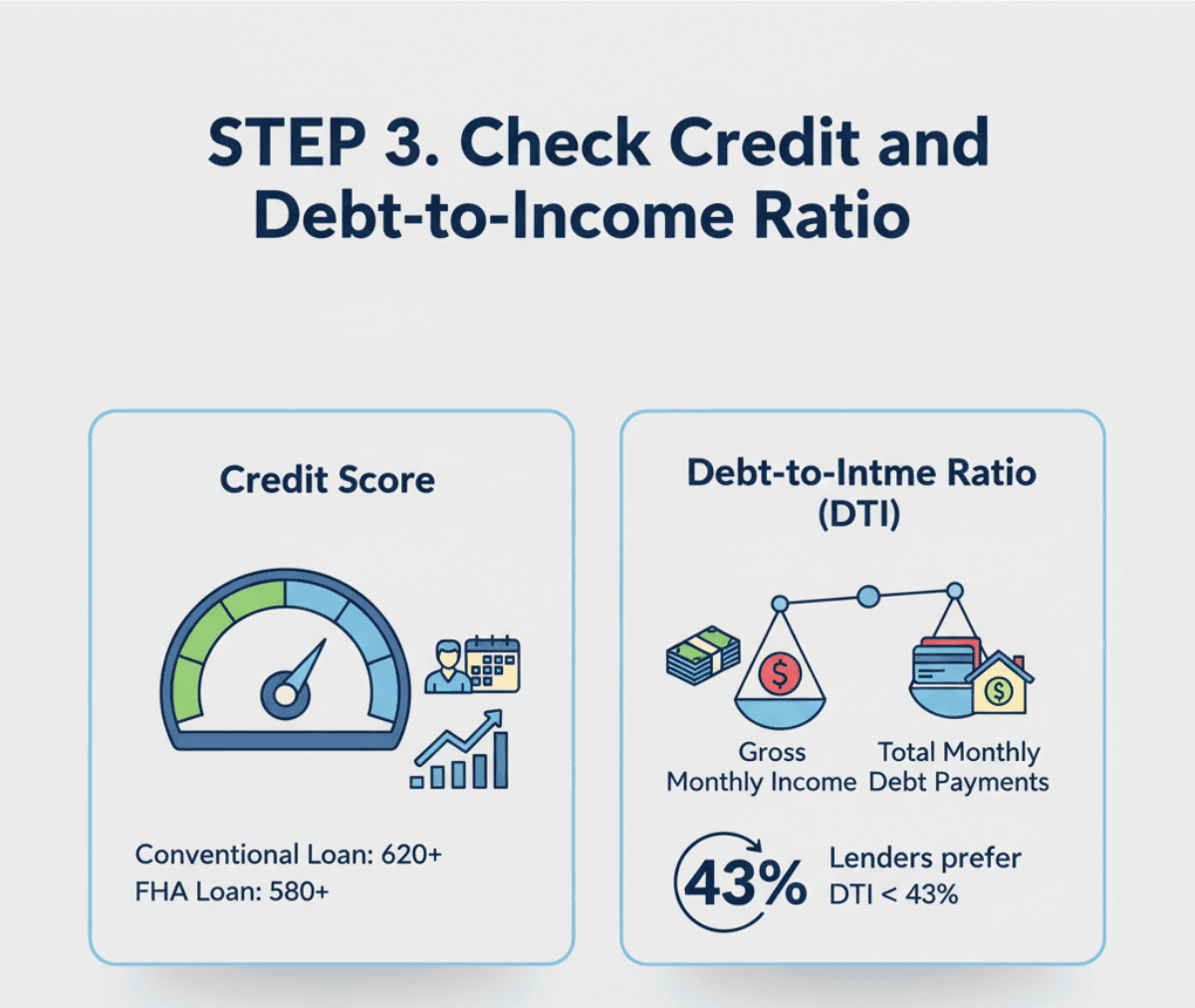

STEP 3. Check Credit and Debt-to-Income Ratio

Before a lender hands over hundreds of thousands of dollars, they look closely at two major numbers: your Credit Score and your Debt-to-Income (DTI) ratio.

From my experience, knowing where you stand beforehand saves a lot of anxiety. Generally, for a Conventional loan, you'll need a credit score of at least 620. FHA loans accept scores of 580+ for 3.5% down payment or 500-579 for 10% down.

Then there's your DTI ratio, which compares your total monthly debt payments to your gross monthly income. Most lenders typically want to see a DTI below 43%.

Not sure if your DTI meets the mark? You don't have to do the math yourself. You can leverage the Bluerate AI Agent to accurately calculate your DTI and verify your income eligibility early on.

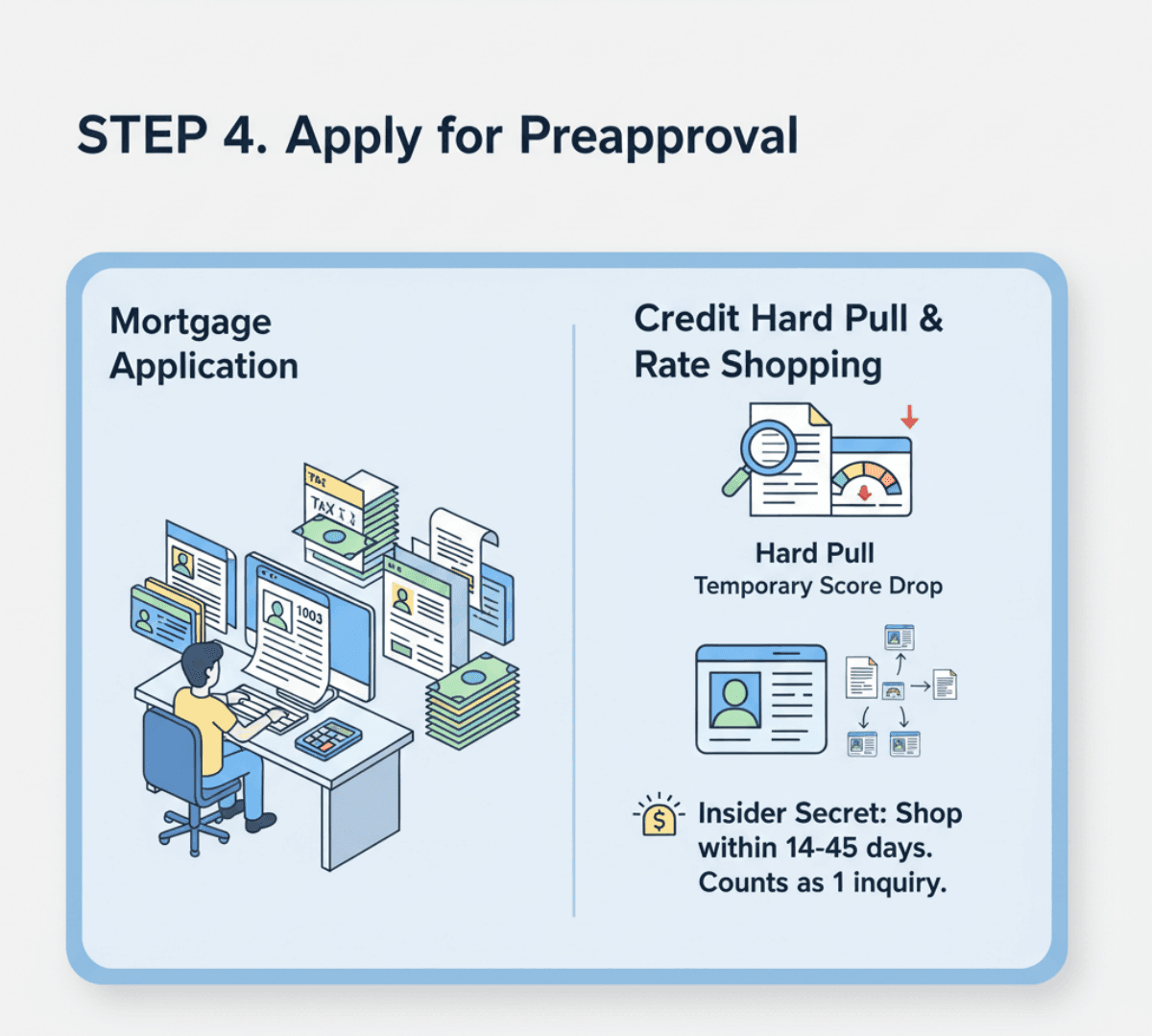

STEP 4. Apply for Preapproval

Now it's time to make it official. You'll sit down (or log on) and fill out the official mortgage application, also known as Form 1003. This is where you hand over all those documents you gathered in Step 2.

At this stage, the lender will perform a "hard pull" on your credit report to verify your history. I know hearing "hard credit pull" makes people nervous because it can temporarily drop your score. But here is an insider secret: the credit bureaus expect you to shop around for the best mortgage rate.

If you apply with multiple lenders within a specific timeframe, typically a 14 to 45-day window, it only counts as a single hard inquiry. This means you can confidently find the right loan officer without destroying your credit.

STEP 5. Get Your Preapproval Letter

This is the moment you've been working toward! After reviewing your file, your loan officer will issue a formal mortgage preapproval letter.

Think of this document as your VIP pass to the housing market. It officially states exactly how much money the lender is willing to let you borrow, the specific type of loan you qualify for, and your estimated interest rate.

Having this letter is incredibly powerful. When I bought my house, my real estate agent wouldn't even submit my offer until she had this letter in hand. It proves to sellers that your financing is rock-solid. With your golden ticket secured, you can confidently walk into open houses and make aggressive, serious offers.

How Long Does a Preapproval for a Mortgage Last?

Typically, a mortgage preapproval is valid for 60 to 90 days. Why doesn't it last forever? Because your financial situation and the broader economic market can change. Interest rates fluctuate, and lenders need to ensure your income hasn't dropped. If your house hunt takes longer than expected and your letter expires, don't panic. Renewing it usually just requires sending your loan officer your most recent bank statements and pay stubs.

Get Preapproved vs Get Prequalified

I hear people use "prequalified" and "preapproved" interchangeably all the time, but they are entirely different beasts. Prequalification is just a casual estimate based on what you tell the lender you make. Preapproval means the lender has strictly verified your documents and pulled your credit. To put it simply: one is a guess, and the other holds real weight.

Here is a quick breakdown to clear up the confusion:

| Aspect | Prequalification | Preapproval | |---|---|---| | Verification Method | Self-reported info only | Verified documents + hard credit pull | | Credit Check | Soft pull (no impact) | Hard pull (temporary score dip) | | Time to Complete | Minutes | 3-5 business days | | Seller Weight | Low - not taken seriously | High - shows serious buyer | | What You Get | Rough estimate letter | Formal preapproval letter with amount | | Validity Period | No fixed expiration | 60-90 days | | Next Step | Move to preapproval | Start making offers |

FAQs About Getting Preapproved for a Mortgage

Q1. What disqualifies you from getting a mortgage?

A high Debt-to-Income (DTI) ratio is a primary culprit. Other common disqualifiers include recent bankruptcy, an unstable employment history (like frequently jumping between different industries), or a credit score that falls below the lender's minimum threshold. Lenders want to see long-term stability.

Q2. What are red flags on a mortgage application?

Lenders get very nervous when they see large, unexplained cash deposits in your bank account, as they must source all funds legally. Other major red flags include undisclosed debts, sudden drops in income, or borrowing your down payment through a new personal loan.

Q3. What are common pre-approval mistakes?

The biggest mistake I see is making major financial changes before closing. Do not apply for new credit cards, finance a new car, or buy expensive furniture on credit. Additionally, quitting your job or switching career paths can instantly derail your hard-earned preapproval.

Q4. Can I get preapproved for mortgage online?

Yes, absolutely. Through a secure marketplace like Bluerate, you can chat with an AI Agent to privately match with a licensed loan officer, securely verify your information, and initiate the preapproval process entirely online, all while keeping your privacy intact and avoiding spam.

Q5. Does pre-approval for a mortgage affect credit?

Yes, but the impact is minimal. A preapproval requires a hard credit inquiry, which might temporarily lower your score by a few points. However, if you shop around and have multiple mortgage inquiries within a short 14-to-45-day window, credit bureaus treat them as a single inquiry.

Q6. Can I get pre-approved for a mortgage with bad credit?

Yes, though your options will be more limited. Government-backed programs, like FHA loans, accept scores as low as 500 (with 10% down) to 580+ (3.5% down). I highly recommend connecting with a professional Loan Officer to get actionable advice on improving your profile.

Q7. If you're pre-approved for a mortgage will you get the loan?

It is not guaranteed. A preapproval is always conditional. If you lose your job, take on new credit card debt, or if the home you want to buy appraises for significantly less than the purchase price, the lender can still deny the final loan right before closing.

Conclusion

Securing a mortgage preapproval is undeniably the most crucial first step in your homebuying journey. It shifts you from a daydreamer to a serious buyer, helps you understand your true purchasing power, and gives you a massive advantage when negotiating with sellers. I know the financial side of buying a house can feel overwhelming, but having the right professional in your corner makes all the difference.

Are you ready to take that first step? Leverage the Bluerate AI Agent today to start a simple, natural conversation. You don't have to fill out tedious registration forms or worry about telemarketers harassing you at dinner. Just chat, securely compare real-time rates from 30+ lenders, and instantly connect with the most trusted, NMLS-licensed loan officers in your area. Your dream home is waiting—let's get you preapproved!