Mortgage Prequalification Explained: What Is It and How to Get It?

You know that feeling. You're scrolling through Zillow late at night, staring at a dream kitchen, but there's a pit in your stomach asking, "Can I actually afford this?" Before you get attached to a home that's out of your league, you need a reality check.

That is exactly what mortgage prequalification is for. It's the very first step to figuring out your budget without drowning in paperwork. If you want to skip the headache and get a clear number instantly, while keeping your personal data private, platforms like Bluerate are a game-changer for getting prequalified online.

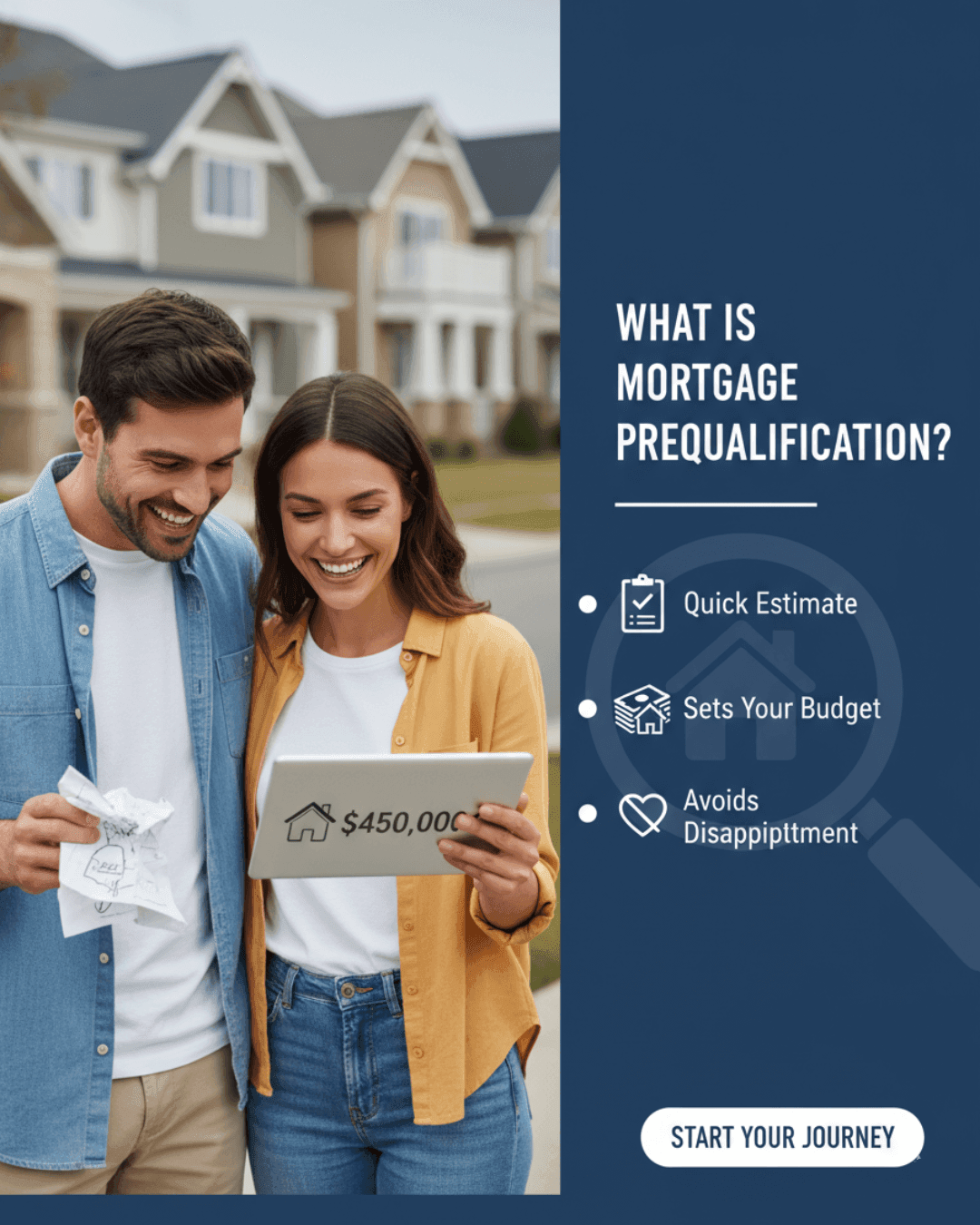

What is Mortgage Prequalification?

Think of mortgage prequalification as a "back-of-the-napkin" math session for your home-buying journey. It isn't a guaranteed loan offer, and it's definitely not the final step. Instead, it is a lender's way of saying, "Based on what you've told us, here is roughly how much we could lend you."

I always tell first-time buyers to do this before they even step foot in an open house. Why? Because it defines your sandbox. It tells you if you should be looking at the $350k range or if you can stretch to $450k. It saves you from the heartbreak of falling for a house, only to realize later that the monthly payments would eat up your entire paycheck. It's quick, usually free, and gives you a baseline to start your search.

What is a Prequalification Mortgage Letter?

Once you run the numbers, you get a document called a Prequalification Letter. This is basically your "ticket" to show real estate agents that you aren't just window shopping.

While it doesn't carry the heavy weight of a formal Preapproval (we'll get to that later), it's still a useful piece of paper. It outlines the loan amount, the potential interest rate, and the type of mortgage you might get. Just keep in mind that these letters aren't guaranteed and may need updating if your finances change, such as buying a new car or switching jobs. Unlike preapproval letters, prequalification letters usually have no fixed expiration date since they rely on unverified information.

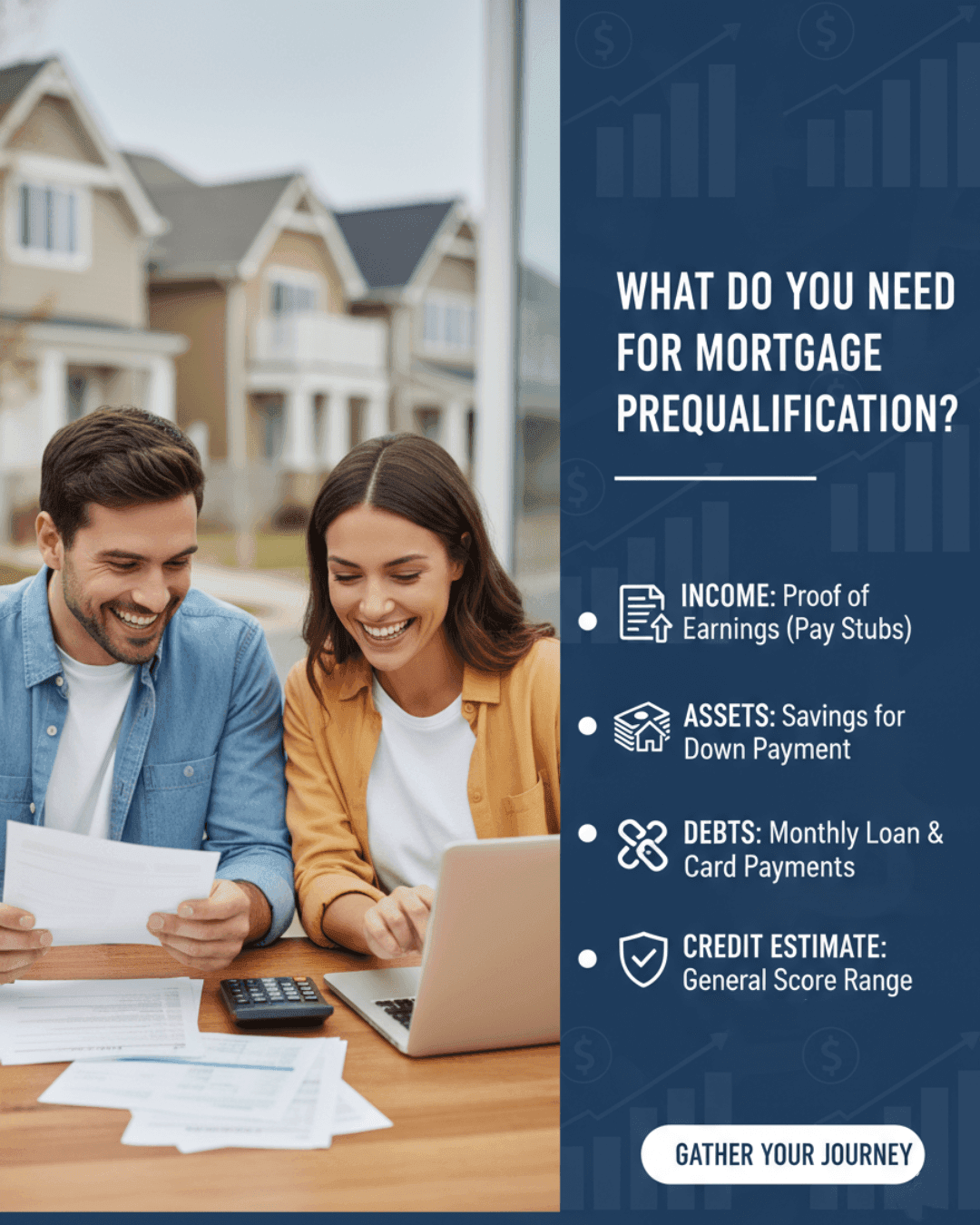

What Do You Need for Mortgage Prequalification?

Here is what you'll need to have ready in your head or on a sticky note:

-

Income: How much you make before taxes (Gross income).

-

Assets: Roughly how much cash you have for a down payment.

-

Debts: Your monthly obligations like student loans, car notes, or credit card minimums.

-

Credit Estimate: You don't need the exact point score, but knowing if you are in the "Good" (700s) or "Fair" (600s) range is key.

Since this is based on what you say, accuracy is on you. If you guess too high on your income, the prequalification number will be useless, and you'll hit a wall later when the lender actually checks your pay stubs.

How to Get a Prequalification for a Mortgage?

If you had asked me this five years ago how to get a mortgage prequalification, I would have told you to brace yourself for a headache. The old way involved calling individual banks or filling out those "Compare Rates" forms online. The problem? The second you hit enter, your phone would explode with spam calls from aggressive salespeople. It felt less like financial planning and more like being hunted.

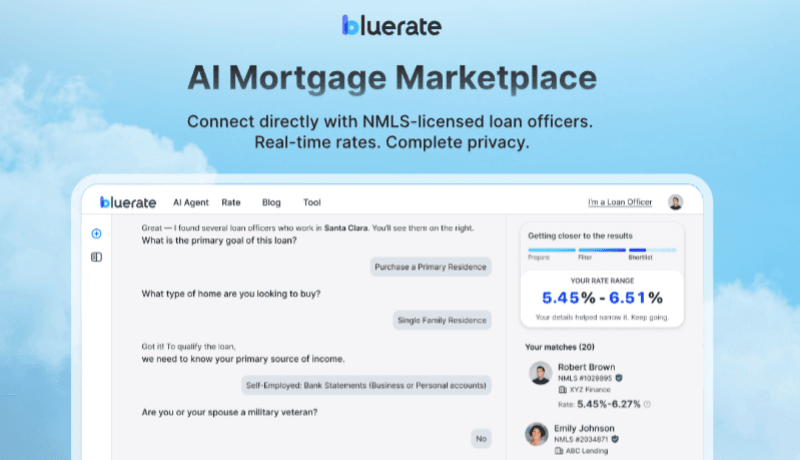

Thankfully, the industry has finally caught up with technology. This is where I've seen Bluerate really stand out.

Bluerate isn't just another lead-generation site that sells your phone number to the highest bidder. It's a proper Marketplace powered by a smart AI Agent. Instead of blindly searching, you actually chat with their AI. You tell it where you want to buy, your income situation, and what you're looking for.

The AI uses a "Prepare-Filter-Shortlist" method to cut through the noise. It analyzes your financial profile and instantly matches you with NMLS-Verified Loan Officers who specialize in your specific needs, whether that's a standard Conventional loan, FHA, or something more niche like Non-QM.

More Features to Explore:

-

No Spam: This is the big one. They prioritize privacy, so you aren't bombarded by random callers. You choose who to connect with.

-

Real Options, Real Fast: The AI scans over 100 lenders to find real-time rates that actually apply to you, not just teaser rates.

-

Tailored Matches: It doesn't just give you a list. It ranks Loan Officers based on how well they fit your profile.

-

Speed: Because the AI handles the heavy lifting of sorting data, you can get pre-qualified significantly faster, about 2.5x quicker than the old manual way.

It's essentially a shortcut to finding a pro who can help you, without the risk of exposing your data to the whole internet.

Also Read:

- Bluerate AI Agent - Meet Your New AI Mortgage Expert in 2026

- 4 Real Use Cases: How Bluerate AI Agent Transforms Mortgages

Mortgage Prequalification VS Preapproval

People use these terms interchangeably, but they are definitely not the same thing. Think of Prequalification as a rough draft, and Preapproval as the final essay.

Here is the breakdown of the differences between mortgage prequalification and preapproval:

-

The Check: Prequalification typically uses self-reported data without a credit pull (no hard inquiry). Preapproval requires a hard pull and verified documents.

-

The Weight: You can't usually buy a house with just a Prequalification letter. In today's market, sellers want to see a Preapproval because it means a lender has fully vetted you and committed to the loan (conditionally).

-

The Timeline: Do the Prequal first to set your budget. Do the Preapproval when you are ready to hire a realtor and start making offers.

FAQs About Mortgage Loan Prequalification

Q1. Are prequalification and preapproval the same?

Nope. Prequalification is an estimate based on your word. Preapproval is a verified commitment from a lender after they've checked your documents and credit history.

Q2. Does mortgage prequalification affect credit score?

Usually, no. Most prequalification processes do not check your credit at all, avoiding any inquiry. Confirm with the lender if they use a soft pull.

Q3. Is it worth getting prequalified for a mortgage?

100%. It's free and low-risk. It helps you catch deal-breakers early, like a Debt-to-Income ratio that's too high, before you waste time looking at homes you can't buy.

Also Read: 3 Methods: How to Calculate Debt-to-Income Ratio for Mortgage?

Q4. How much income do you need to qualify for a $500,000 mortgage?

It's not a fixed number because interest rates change the math daily. Roughly speaking, with today's rates and a 20% down payment, you might need an income between $120k and $140k. But don't guess, and use the Bluerate AI Agent to run the specific numbers for your situation, as property taxes and insurance also play a huge role.

Conclusion

Buying a home is massive, and it's easy to feel overwhelmed by the financial jargon. But getting prequalified is the one step that brings clarity to the chaos. It turns "I hope I can buy" into "I know what I can buy."

Don't let the fear of spam calls or complicated forms stop you. If you want a stress-free way to see your numbers, give Bluerate a shot. Their AI Agent can help you find the right NMLS-verified loan officer and get accurate rates in minutes, all while keeping your personal info secure. It's the smartest first move you can make.

People Also Read: