Mortgage Preapproval Explained: Know Everything About it

House hunting right now is brutal. When I bought my first place, I learned the hard way that browsing Zillow without a real budget is just window shopping. If you actually want to buy a house, you need a mortgage preapproval first. It proves you have the cash backing to make a serious offer. The good news? You don't have to sit in a bank lobby anymore to get one. Platforms like Bluerate let you handle the whole thing online, quickly and without the usual headaches.

What is Mortgage Preapproval?

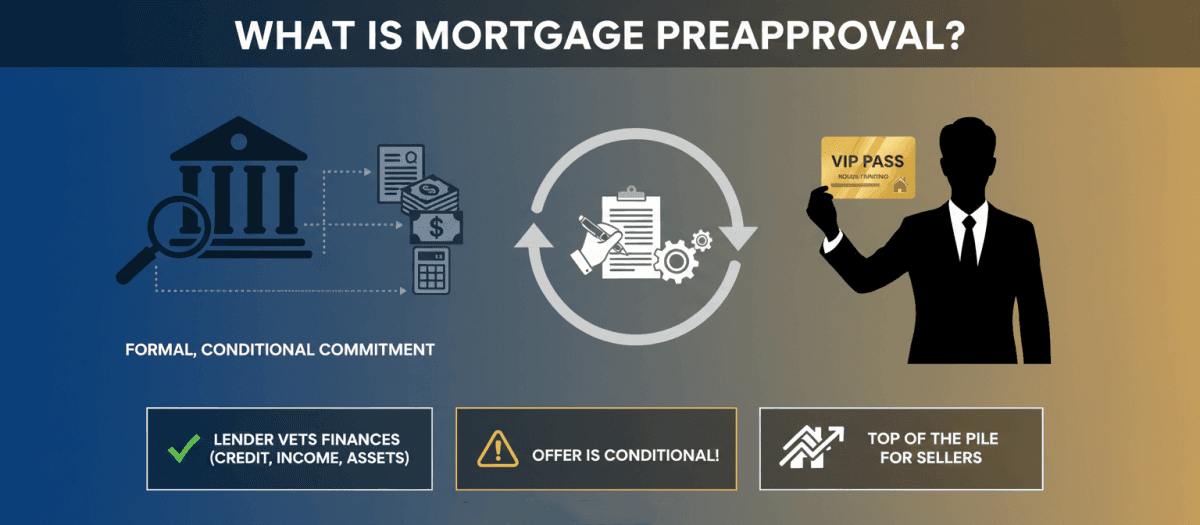

So, what exactly are we talking about here? A mortgage preapproval isn't just a lender guessing what you might afford. It's a formal, conditional commitment. To give you this, a bank or lender actually digs into your financial life. They pull your credit report, verify your income, check your assets, and crunch your debt-to-income (DTI) ratio.

After looking under the hood, they agree to lend you a specific amount under certain conditions. I usually tell friends to treat it like a VIP pass for house hunting.

But here is the catch: "preapproved" does not mean "cleared to close." The offer is strictly conditional. If you suddenly decide to finance a new truck, quit your job, or rack up massive credit card debt right before closing, the lender will pull the plug on your loan. Still, crossing this hurdle is mandatory. It shows sellers that a financial institution has actually vetted you, instantly putting your offer at the top of the pile compared to buyers who skipped this step.

What is a Mortgage Preapproval Letter?

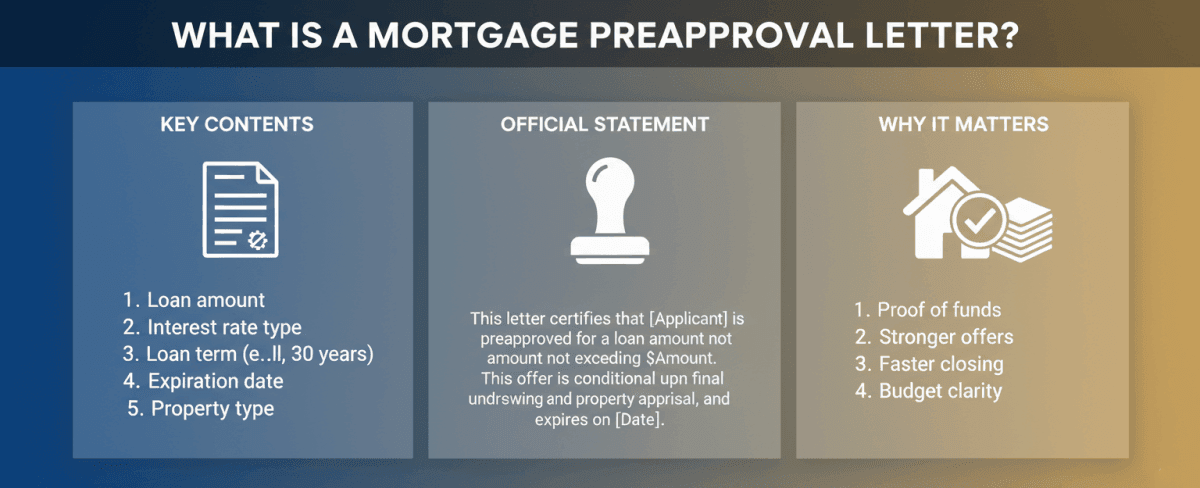

This is the actual document, either digital or physical, that the lender hands over once you pass their background check. Honestly, my real estate agent flat-out refused to let me submit an offer until I had this letter in hand.

It lays out crucial pieces of information: the maximum amount you can borrow, the specific type of loan (like FHA, VA, or Conventional), down payment requirements, and when the offer expires. An estimated interest rate may be provided as a baseline, but it is typically not locked.

In a competitive market, this piece of paper is your best weapon. Sellers want a sure thing. If they have to choose between a buyer holding a valid preapproval letter and someone just claiming they have the funds, they will pick the preapproved buyer every single time.

How Long Does Mortgage Preapproval Last?

You typically have a 30-to-90-day window before the letter expires. Why the tight deadline? Because your financial picture, and the economy, change constantly. Interest rates jump around daily, and your credit score fluctuates. Lenders need to know the data they based their decision on hasn't gone stale.

If yours expires before you land a house, don't panic. Mine expired during a long search, and getting an extension was surprisingly easy. I just had to email my latest pay stubs and updated bank statements to reset the clock. My advice? Don't pull the trigger on applying until you are actively ready to start touring properties.

Also Read: Must-Read: How Long is a Mortgage Preapproval Good for?

What Documents Do You Need for Preapproval?

Tracking down paperwork is nobody's favorite chore, but having it ready will save you days of waiting. When I did this, I just dumped everything into a single desktop folder beforehand. Here is the standard checklist you'll need to provide:

-

ID & Basics: Your driver's license, passport, and Social Security Number.

-

Income Verification: W-2s from the past two years and your most recent pay stubs, usually covering 30 days. Freelancers or business owners will need 1099s and two years of full tax returns.

-

Proof of Assets: Two months of bank statements for both checking and savings accounts. You should also include statements for retirement funds or investment accounts like a 401(k).

-

Debt Details: Lenders already see your debts on your credit report, but you might need to provide extra context for specific obligations like child support or student loans.

Having this stack ready proves you are an organized, serious buyer.

How to Get a Mortgage Preapproval?

The process sounds overwhelming, but it's really just a series of small steps to get a mortgage preapproval.

-

Check your own credit: Pull your free report before the bank does. This gives you a window to dispute any weird errors dragging your score down.

-

Gather your files: Grab those W-2s and bank statements we just talked about.

-

Figure out your real budget: A lender might approve you for $600k, but if the monthly payment makes you sweat, aim lower. Decide your comfort zone first.

-

Shop for lenders: Never settle for the first mortgage quote you get. Comparing rates is how you save thousands over the life of the loan.

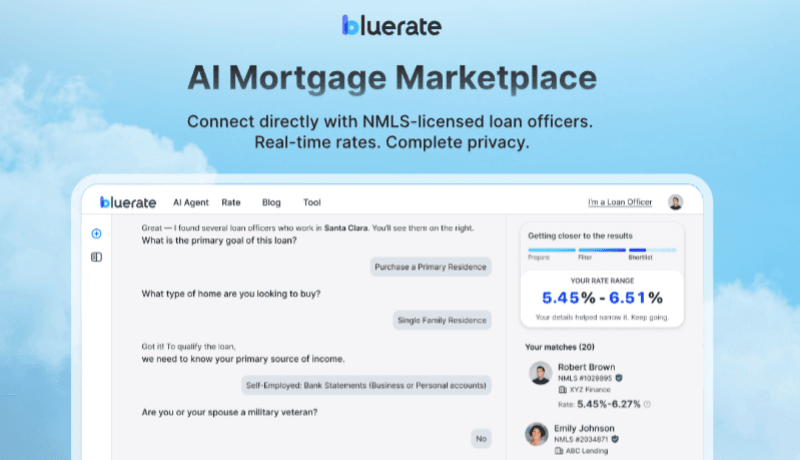

If you want to skip the endless Google searches and hold times, try using the Bluerate AI Agent. Instead of filling out clunky forms alone, you can chat directly with their AI for free. It answers your questions on the spot and seamlessly connects you with top-tier, human loan officers who can fast-track your preapproval.

How to Improve Your Chances of Getting Preapproved?

Nobody wants to get rejected by an underwriter. If you want a smooth approval, stick to these rules:

-

Knock down your DTI: Pay off those lingering credit card balances before applying. Lenders love seeing a debt-to-income ratio below 43%.

-

Boost your down payment: Bringing more cash to the table makes you a safer bet to the bank, which can also score you a better interest rate.

-

Freeze your spending: This is non-negotiable. Do not finance a car, buy a house full of furniture on credit, or quit your job mid-process. Keep your financial footprint completely boring until the house keys are actually in your hand.

What is the Difference Between Prequalification and Preapproval?

People toss these words around like they mean the same thing, but they definitely don't. Mortgage prequalification is just a casual estimate. Preapproval is a verified offer. If you want a seller to take your bid seriously, prequalification is a hard pass.

| Aspect | Prequalification | Preapproval | |---|---|---| | What it is | Rough estimate based on self-reported info | Formal conditional commitment | | Credit Check | Soft pull or no pull | Hard pull required | | Documentation | Minimal or none | Full financial documents required | | Verification | Unverified | Verified by lender | | Seller Weight | Low - not taken seriously | High - shows serious buyer | | Duration | No fixed expiration | 30-90 days | | When to do it | Early exploration phase | Ready to make offers |

Early on, I got prequalified just to figure out what neighborhoods I could afford to look at online. But the second I hired a realtor and wanted to attend open houses, I had to upgrade to a full preapproval. Sellers demand proof, not promises.

Also Read:

- Mortgage Prequalification vs Preapproval: All Differences

- Guide: How to Prequalify for a Mortgage Loan Online?

FAQs About Mortgage Preapproval

Q1. Can I get a mortgage preapproval without a credit check?

Nope, you cannot. A legitimate preapproval demands a hard credit inquiry because the bank has to verify your financial history before committing their money. If a lender offers you an estimate without actually running your credit, they are just giving you a prequalification, which won't hold up when making an offer.

Q2. Can I get preapproved online?

Yes, 100%. You rarely need to step foot inside a physical bank branch these days. The entire application process is highly digitized and secure. Platforms like Bluerate make it incredibly easy to upload your tax documents, verify your identity, and secure your official letter right from your couch. It's fast and efficient.

Q3. How far in advance should you get preapproved for a house?

Aim for about 30 to 60 days before you plan to start aggressively touring homes and writing offers. Because the letter usually expires within 90 days, you don't want to jump the gun. However, it's smart to check your own credit report 6 to 12 months in advance to fix any errors.

Q4. Does a mortgage preapproval affect my credit score?

Yes, but barely. The hard pull usually drops your FICO score by roughly 5 points. The good news? Credit bureaus offer a "rate shopping window," usually lasting 14 to 45 days. If you apply with several different lenders within that specific timeframe, it all counts as just one single inquiry.

Q5. What salary do you need for a $400,000 mortgage?

For a $400k home with 20% down ($320k loan), at ~7% rates and 43% DTI max, required income is approximately $100k-$102k. The range is reasonable but slightly broad. It holds as a general estimate for "comfortably manage." No revision required unless specifying exact rates.

Also Read: How Much Income Needed for a 400K Mortgage? Know Your Affordability

Conclusion

Buying a house is stressful enough without guessing what you can afford. Securing that mortgage preapproval is easily the smartest first step you can take. It locks in your realistic budget, keeps you from falling for homes outside your price range, and proves to sellers that you are a serious contender ready to buy.

You don't have to navigate the paperwork alone or settle for the first lender you find. If you are ready to see your real buying power, head over to Bluerate. Their AI-driven tools and expert loan officers take the friction out of the entire process. Stop guessing your budget and get your preapproval sorted today!