Best Mortgage for Low Income 2026: Which One for You?

I was scrolling through the /r/AskLosAngeles subreddit the other night, and a post caught my eye. A first-time buyer asked, "Low income, how can I ever buy a house here?" Honestly, as a licensed Loan Officer for 20 years, I hear this panic daily. With 2026 home prices still high, buying on a tight budget feels terrifying. But it's genuinely not impossible. You just need the right program.

And no, you don't have to hunt for it blindly anymore. You can actually use tools like the Bluerate AI Agent to just chat your way into finding a mortgage expert who gets your exact situation. Let me show you how.

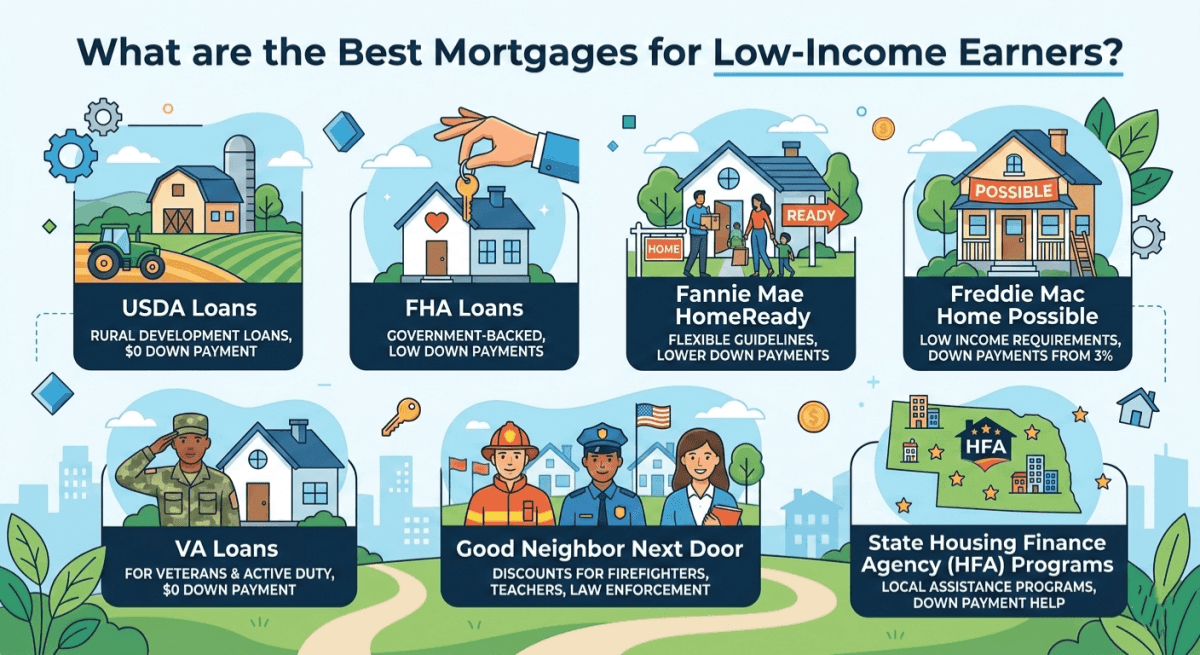

What are the Best Mortgages for Low-Income Earners?

Federal agencies and private lenders actually have specific programs built from the ground up for low-to-moderate-income (LMI) buyers. Knowing which of these government-backed or conventional loans fits your life is the biggest hurdle. Here's what I'm currently putting my clients into this year.

USDA Loans

If you're open to living outside the crowded city limits, the USDA loan is a massive lifesaver. Backed by the Department of Agriculture, it's meant to build up rural and suburban neighborhoods. Why do I love it for tight budgets? Zero down payment. I just helped a young couple close on a house last month without them draining their tiny savings account.

But the rules are strict. First off, you have to buy in an "eligible rural area" based on the USDA's map, which includes surprisingly normal suburbs, by the way. Secondly, it has a hard income cap. USDA income limits are set at 115% of the county's median income (e.g., $86,850-$212,550 for 1-4 person households in California counties as of 2026).

Key Features:

-

0% Down: You finance the whole purchase price.

-

Cheaper Mortgage Insurance: The upfront and annual fees are usually lower than FHA.

-

Credit Flexibility: They prefer a 640 FICO, but we can sometimes push it through with alternate credit history.

-

Strict Income Caps: Designed strictly for lower-earning families.

FHA Loans

The FHA loan is my go-to recommendation for folks dealing with a combo of low income and a bruised credit score. Because the Federal Housing Administration insures the lender in case things go south, mortgage companies are way more willing to approve you.

If your credit took a hit recently, you can still get in with a score as low as 580 and only need a 3.5% down payment. The downside? Mortgage Insurance Premiums (MIP). For loans with <10% down, MIP is required for the full loan term (post-2013 FHA rules). With ≥10% down, it cancels after 11 years. Also, the appraiser will be picky about the home's condition—no peeling paint or leaky roofs allowed.

Key Features:

-

Super Low Credit Hurdle: 580 FICO gets you the max financing.

-

Tiny Down Payment: 3.5%, and yes, it can be 100% gifted from family.

-

Forgiving DTI: I've gotten approvals with debt-to-income ratios over 50%.

-

No Income Limits: Make as much or as little as you want, as long as the math works.

Fannie Mae HomeReady

Unlike the FHA, Fannie Mae's HomeReady isn't a government loan. It's conventional. It was specifically built for creditworthy buyers who just don't make a ton of money.

I push my clients toward this one because of a massive long-term perk: you can cancel your private mortgage insurance (PMI) once you hit 20% equity. That saves you thousands over the years. To get approved, your income can't exceed 80% of your Area Median Income (AMI). (e.g., Los Angeles ~$90,000 for 1-4 persons in 2026). So if your county's median is $100,000, you need to make $80,000 or less. You'll also need a slightly better credit profile than FHA, ideally around a 620 FICO.

Key Features:

-

Only 3% Down: Keeps your upfront closing cash very manageable.

-

PMI Drops Off: You aren't stuck paying insurance forever.

-

Creative Income Allowed: Got a roommate or a basement unit? We can often use that rental income to help you qualify.

-

Strict Income Ceiling: You strictly must earn under the 80% AMI limit.

Freddie Mac Home Possible

Freddie Mac's Home Possible is basically the twin brother to HomeReady. It targets the exact same crowd: low-to-moderate-income earners who have okay credit but can't possibly save up a 20% down payment.

Just like the Fannie Mae version, you can't make more than 80% of your local Area Median Income (AMI) to use it. Why pick this over an FHA loan? Again, it's all about the mortgage insurance. The PMI rates are reduced, and they eventually go away. One really cool trick I've used with Home Possible is "sweat equity." If you do repairs on the property yourself, the value of your labor can sometimes count toward your down payment.

Key Features:

-

3% Minimum Down: You can use your savings, a gift, or even a grant.

-

Reduced Insurance Costs: Monthly PMI is cheaper than standard conventional rates.

-

Co-Borrower Friendly: A parent who won't live in the house can co-sign to help you qualify.

-

Credit Score: Usually needs a 620 to 660, depending on who you borrow from.

VA Loans

If you served in the military or are an eligible surviving spouse, skip the rest of this list. The VA loan, backed by the Department of Veterans Affairs, is hands down the best mortgage in America.

It doesn't explicitly say "for low income," but its setup is a godsend for military families on tight budgets. I love writing these because they require zero down payment and absolutely zero private mortgage insurance. The savings are huge. The main catch is simply eligibility. You need a valid Certificate of Eligibility (COE). You'll also have to pay a one-time VA funding fee, which we usually just roll into the loan amount, though if you have a service-connected disability, that fee is completely waived.

Key Features:

-

Zero Down: Keep your cash in the bank.

-

No PMI Ever: This drops your monthly payment significantly.

-

Easy Qualifications: Extremely forgiving on past credit blips and high debt ratios.

-

Rock-Bottom Rates: They typically carry the lowest interest rates you'll find anywhere.

Good Neighbor Next Door

To be totally accurate, the Good Neighbor Next Door (GNND) isn't a loan itself. It's a wild discount program from HUD.

If your day job is a pre-K through 12th-grade teacher, cop, firefighter, or EMT, you can buy specific HUD-owned houses for 50% off the list price. Yes, half off. A $300k house becomes $150k instantly. For public servants who are notoriously underpaid, this is the golden ticket. But there are major strings attached. The houses are in specific "Revitalization Areas," inventory is super rare, and homes are only listed for 7 days. Plus, you absolutely must live there as your primary home for three full years.

Key Features:

-

50% Discount: You walk in with instant, massive equity.

-

Tiny Down Payment: Minimum FHA down on discounted price (e.g., ~$100 on $50k home, but varies by appraisal).

-

Strictly for Public Servants: Teachers, police, and emergency responders only.

-

3-Year Lock-in: You sign a silent second mortgage that completely vanishes after 36 months of living there.

State Housing Finance Agency (HFA) Programs (e.g., CalHFA)

People always forget they don't have to rely on federal programs. Every single state has its own Housing Finance Agency (HFA) trying to help locals buy homes.

Take California's CalHFA, for example. I've had buyers in LA who layered a regular FHA loan with a CalHFA subordinate loan to completely cover their down payment and closing costs. These state programs usually staple a 30-year fixed mortgage together with Down Payment Assistance (DPA) to get you to the closing table. The rules change wildly depending on what state you live in. Usually, you have to be a true first-time buyer, meaning no homeownership in the last three years, and you have to meet their local income limits.

Key Features:

-

Locally Focused: Matched to your specific county's median income and home prices.

-

Down Payment Assistance (DPA): They hand out deferred loans or grants to cover your cash to close.

-

First-Time Buyer Driven: Meant to get renters into their first property.

-

Education Needed: Expect to spend a Saturday taking a HUD-approved homebuyer class.

What are the Best Strategies for Low-Income Borrowers?

Picking the right loan is only step one. Over the years, I've seen that what really gets a low-income buyer the keys is how they stack different strategies. If your paychecks are stretched thin, don't rely entirely on the mortgage. Try these tactics:

-

Down Payment Assistance (DPA): Stop assuming you need to use your own cash. There are thousands of local grants (free money) and forgivable loans meant to cover that 3% to 3.5% down payment.

-

Lender Assistance Programs: Check with big banks. Some have their own grant programs, like offering $5,000 to $10,000 toward closing costs if you buy in specific lower-income census tracts.

-

NACA Program: The Neighborhood Assistance Corporation of America does a crazy zero-down, zero-closing-cost, zero-PMI loan without looking at your traditional credit score. But fair warning: their approval process is exhausting and takes months.

-

Co-borrowing/Co-signing: If your income just won't cut it for the debt-to-income math, bringing on a family member with strong income as a non-occupant co-borrower can instantly fix the problem.

Step-by-Step: How Can I Get a Mortgage Loan with Low Income?

You have to be proactive. Here is the exact checklist I hand my clients so they don't get rejected:

-

Fix Your Credit First: Pull your free annual reports. Dispute the junk and pay down credit cards. A tiny 20-point jump can save your deal.

-

Run Your DTI: Divide your monthly minimum debt payments by your gross monthly income. Pay off those small Affirm or Klarna loans to push your ratio below 43%.

-

Hoard Your Paperwork: We lenders are nosy. Have your last two years of W-2s, tax returns, and 30 days of pay stubs saved in a PDF folder.

-

Get a Real Pre-Approval: Stop browsing Zillow until a licensed lender hands you a piece of paper saying exactly what you can afford.

How to Easily Find and Qualify with Low-Income Mortgage Lenders?

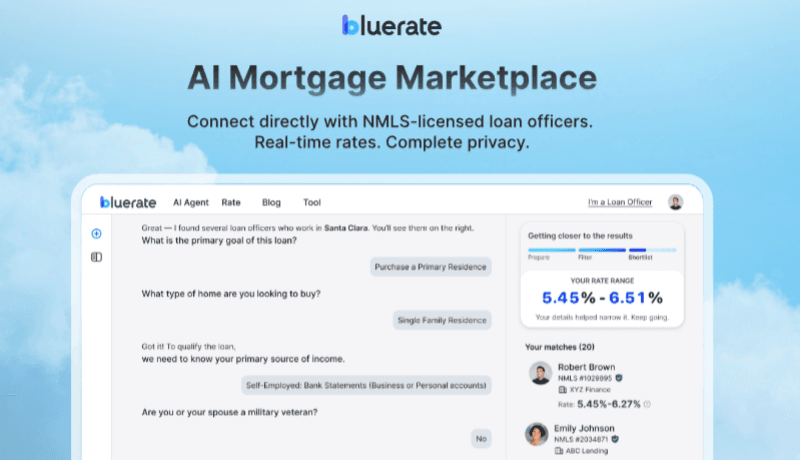

Here's where things usually fall apart. You know you need help, but big banks often brush off lower-income applications. On the flip side, if you fill out a random form online, your phone will ring 50 times a day with spammy salespeople. Finding a legit, NMLS-licensed loan officer who actually knows how to navigate local grants and USDA maps shouldn't be a nightmare.

That's exactly why my team and I constantly talk about Bluerate. It's not just another lead-generation site. It's an All-in-One Marketplace that actually connects you directly with pros. The best part is the Bluerate AI Agent. Instead of filling out a confusing 10-page application, you just chat with an AI assistant. It looks at your unique financial footprint and figures out if you're an FHA, USDA, or Conventional buyer.

Here's how I tell people to use it:

-

Step 1: Hit the "Chat with AI" button on the homepage.

-

Step 2: Tell it what city or zip code you're buying in.

-

Step 3: Just answer a few conversational questions about your credit, funds, and property type (it even speaks Spanish and Chinese).

-

Step 4: The AI uses a "Prepare-Filter-Shortlist" system to instantly match you with top-rated loan officers who specialize in your situation, plus real-time rate quotes. You choose who to talk to, completely free.

FAQs About the Best Mortgage for Low Income

Q1. What is the lowest income to qualify for a mortgage?

There isn't a legal minimum income. It all boils down to your Debt-to-Income (DTI) ratio. As long as your steady paycheck covers your new housing payment plus your existing debts, usually keeping that total under 43% to 50%, you can get approved.

Q2. How to buy a house with only one income?

Focus on killing your current consumer debt to free up room in your DTI. Look heavily into local Down Payment Assistance (DPA) grants, and seriously consider starting with a smaller condo or townhouse to keep the loan amount realistic for a single earner.

Q3. What is the 28/36 rule for mortgages?

It's an old-school affordability rule. Lenders prefer that your housing payment doesn't take up more than 28% of your gross (pre-tax) income, and your total monthly debts (mortgage, cars, credit cards) stay under 36%. Though nowadays, FHA loans often allow much higher limits.

Q4. What is the minimum income for a 200k mortgage?

Assuming a standard 2026 interest rate around 6%, adding in taxes and a small down payment, you generally need to make approximately $48,000-$65,000 annually, assuming 6-6.5% rate, 3.5% down, 43% DTI, taxes/insurance, to comfortably carry a $200k mortgage. This shifts depending on your other monthly debts.

** Read Also:**

- Solved - How Much Income Needed for 300K Mortgage?

- How Much Income Needed for a 400K Mortgage?

- Read First: How Much Income Needed for 500K Mortgage?

Q5. Can I get approved for a mortgage with no income?

For a primary home, usually no. Lenders have to follow strict federal "Ability-to-Repay" rules. But "income" doesn't have to mean a salary. We can use social security, disability, child support, or even drawdowns from a large retirement account to qualify you.

Q6. What mortgage does not require proof of income?

Non-QM (Non-Qualified Mortgage) loans, like DSCR for investors or Bank Statement loans for the self-employed, skip standard W-2 checks. But honestly, these require heavy cash flow or huge down payments, so they are almost never a good fit for low-income first-time buyers.

Conclusion: What is the Best Home Loan for Low Income?

At the end of the day, the "best" loan is the one that fits your messy, real-world life. If your credit took a beating, lean on the FHA loan. Buying out in the country? The USDA loan is unbeatable. Veterans should look nowhere else but VA loans, and if your credit is decent but cash is tight, HomeReady or Home Possible are your best bets.

You really don't have to figure this out alone. Instead of stressing over which bucket you fall into, let the Bluerate AI Agent do the math. It safely and privately matches your profile with the exact loan officers who can close your deal. Head over to Bluerate today, chat with the AI for free, and finally get the right expert in your corner.

People Also Read

- First-Time Home Buyer Loans: How to Qualify Even With Low Credit or Savings

- 10 Tips: First-Time Home Buyer Tips and Advice for You

- Must Read: Minimum Down Payment for House First-Time Buyer

- Must-Read Guide: How to Buy a House for the First Time?

- How to Calculate Early Payoff of Mortgage? Formula and Penalty