Best First-Time Home Buyer Programs: Which One to Apply?

I'll never forget sitting in a cramped apartment, staring at my first mortgage application and feeling like I was taking a test in a language I didn't speak. If the acronyms and math have your head spinning, you aren't alone. Buying a home in 2026 is a massive hurdle, but you don't have to clear it with pure savings alone.

While this guide breaks down the best paths forward, numbers change daily based on your zip code. For the most accurate, zero-fluff advice, I'd suggest heading over to Bluerate to chat with a local loan officer who actually knows your specific neighborhood.

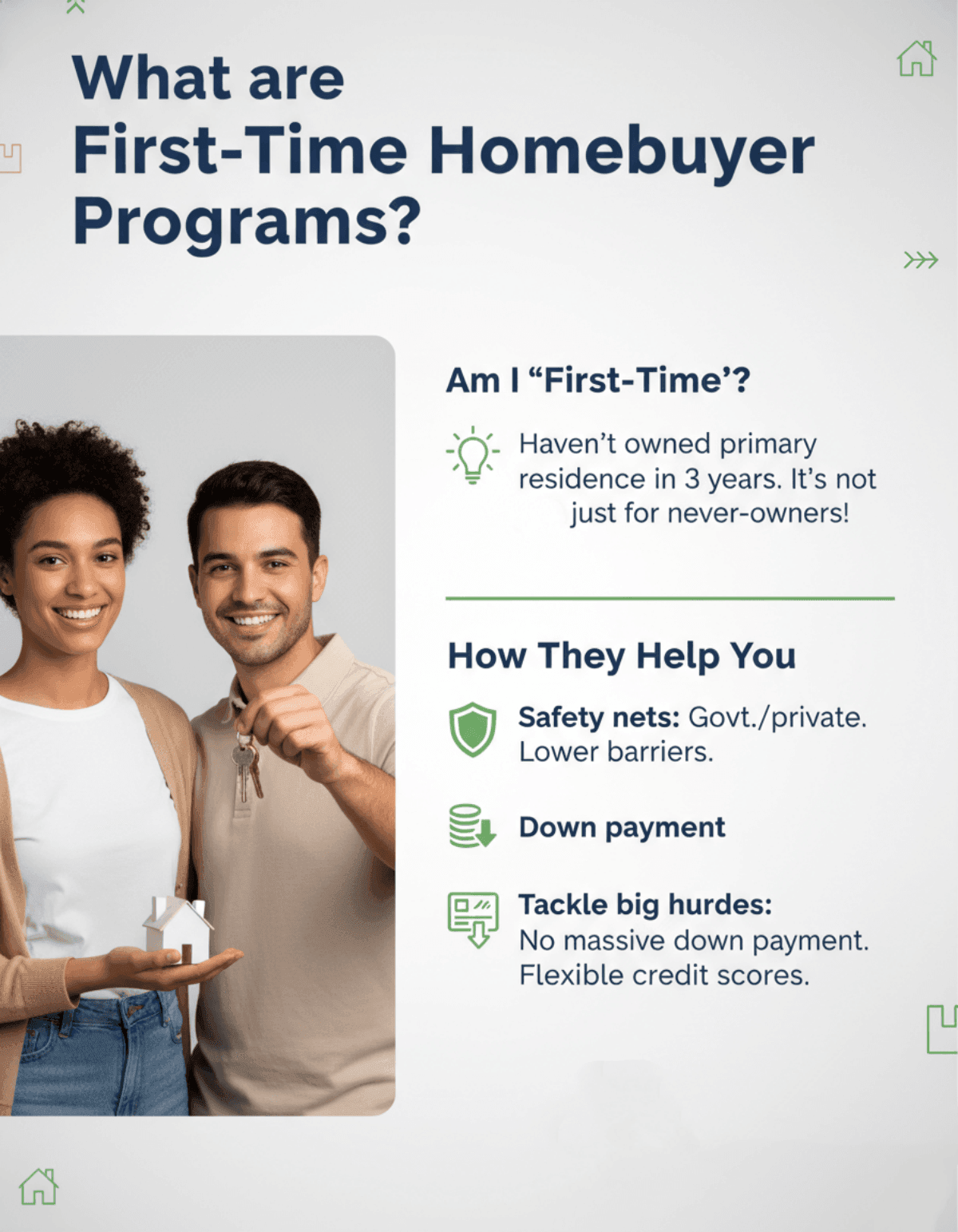

What are First-Time Homebuyer Programs?

Most people assume "first-time" means you've never owned a single brick in your life. But here's a professional secret: you usually qualify if you haven't owned your primary residence in the last three years. These programs are essentially "safety nets" created by the government or private lenders to lower the barrier to entry. They tackle the two biggest ghosts that haunt renters: the massive down payment and the "perfect" credit score requirement.

Whether it's a 0% down loan or a grant that covers your closing costs, these programs are designed to bridge the gap between "I can afford the monthly rent" and "I can afford to own the building."

Also Read:

- First-Time Home Buyer Requirements: Everything You Need to Know

- Best First-Time Home Buyer Loans: Pick the Right Choice

- Best First-Time Home Buyer Lenders: Find Your Perfect Match

- 30 Questions to Ask a Loan Officer as a First-Time Home Buyer

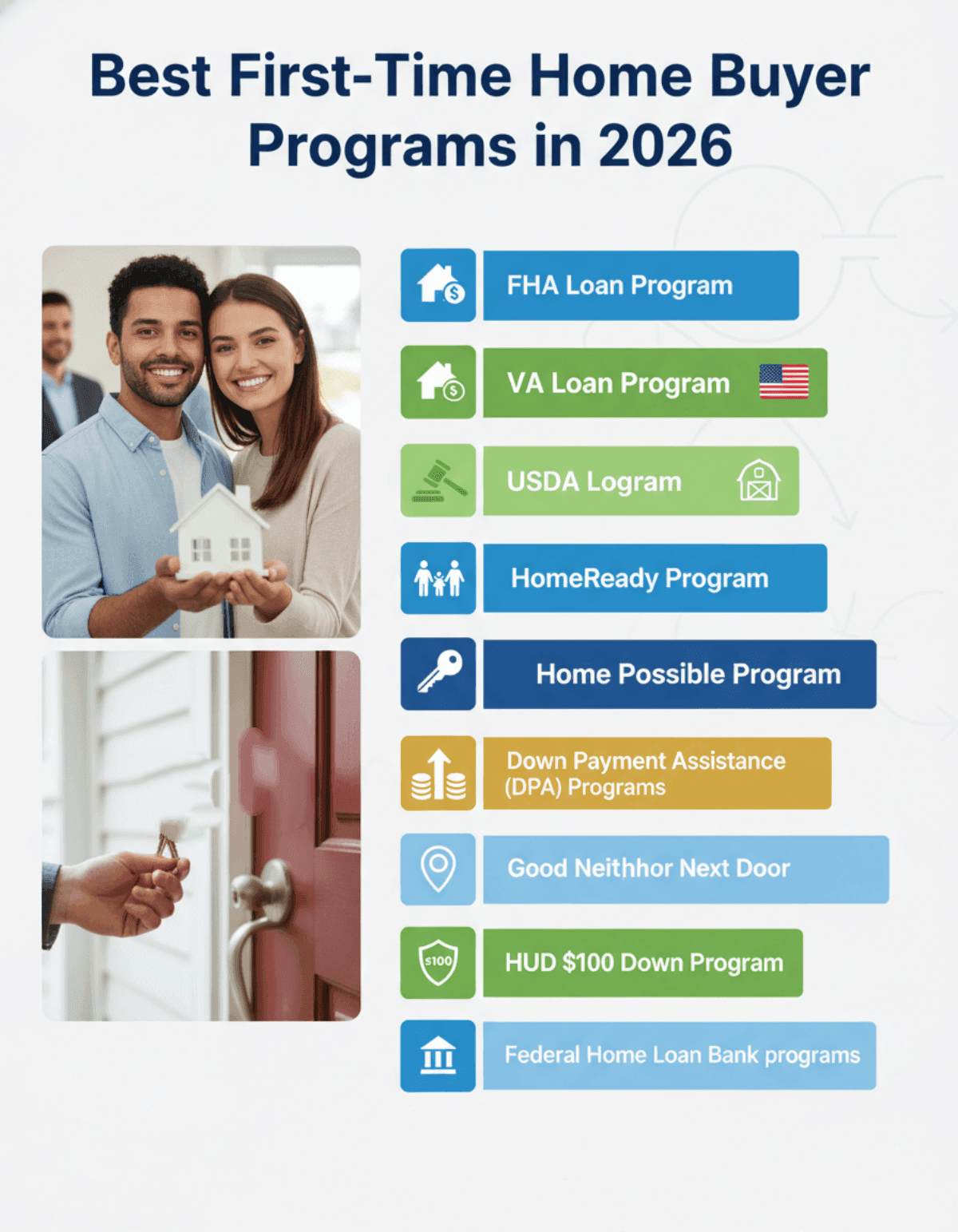

Best First-Time Home Buyer Programs in 2026

The 2026 market is tricky, but these ten programs remain the most reliable ways to get your foot in the door without draining your entire life savings.

#1. FHA Loan Program

Best for: Buyers whose credit scores have a few "bruises" or who have limited cash for a down payment.

I like to think of the FHA loan as the "great equalizer." Insured by the Federal Housing Administration, it allows lenders to take a chance on you even if your credit isn't pristine. The 3.5% down payment is a major draw, but keep in mind the "catch": you'll pay Mortgage Insurance Premiums (MIP) for the life of the loan. It's a trade-off. You get in the door sooner, but your monthly bill is a bit higher.

Requirements:

- Credit Score: 580 gets you the 3.5% down deal. 500-579 requires 10% down.

- Down Payment: 3.5% of the purchase price.

- DTI Ratio: Usually capped at 43%, but some lenders approve up to 56.99% or 57% with strong compensating factors.

- Appraisal: The home must meet strict safety and habitability standards.

#2. VA Loan Program

Best for: Veterans, active-duty service members, and eligible surviving spouses.

Honestly, this is the single best mortgage product in the U.S., period. If you've served, the VA loan lets you buy with $0 down and, this is the big one, zero private mortgage insurance (PMI). That saves you hundreds of dollars every month compared to any other loan. There is a "funding fee" (2.15% for first-time use with 0% down, up to 3.3% for subsequent use), but it can be rolled into the loan, so you aren't paying it out of pocket on day one.

Requirements:

- Eligibility: Must have a Certificate of Eligibility (COE) based on your service record.

- Down Payment: 0% required.

- Credit: The VA doesn't set a minimum, but most lenders want to see at least a 620.

- Primary Residence: You have to actually live in the house. No investment properties allowed here.

#3. USDA Loan Program

Best for: Low-to-moderate income earners looking for a home in suburban or rural areas.

People often hear "USDA" and think they have to buy a farm. In reality, plenty of quiet, developed suburbs fall into USDA-eligible zones. It's another 0% down option, making it a "hidden gem" for families who want more space. The limitation is strict: both the house and your income must fit within USDA's specific geographic and financial maps. If you earn too much, you're disqualified.

Requirements:

- Location: Property must be in a USDA-defined rural area.

- Income: Household income generally cannot exceed 100% of the area's median income (AMI), varying by location.

- Credit Score: Usually 640 for streamlined processing.

- Debt Ratio: Lenders prefer your monthly debt to be 41% or less of your gross income.

#4. HomeReady Program (Fannie Mae)

Best for: Buyers with good credit but lower income who want to ditch mortgage insurance eventually.

HomeReady is Fannie Mae's premier first-time buyer tool. It only requires 3% down, and unlike an FHA loan, you can cancel your mortgage insurance once you hit 20% equity. This saves you a massive amount of money in the long run. My favorite feature? They let you count income from a "boarder" (someone living with you) or a basement apartment to help you qualify for the loan.

Requirements:

- Income Limit: You must earn 80% or less of your Area Median Income (AMI).

- Credit Score: Minimum 620, though 680+ gets you much better rates.

- Down Payment: 3% minimum.

- Homebuyer Education: You'll need to complete a quick online course to prove you understand the responsibilities of owning.

#5. Home Possible Program (Freddie Mac)

Best for: Low-to-moderate income borrowers, especially those with "thin" credit histories.

This is Freddie Mac's version of the 3% down loan. It's very similar to HomeReady but often a bit more flexible with where your down payment comes from. If your parents are gifting you the 3% or if you have a local grant, Home Possible is very friendly to those "non-traditional" sources of cash. It's a fantastic "conventional" alternative to the FHA loan for those who have decent credit.

Requirements:

- Income: Must not exceed 80% of the AMI for your specific census tract.

- Credit Score: No minimum set by Freddie Mac. Lenders typically require 620-660.

- Property Type: Works for single-family homes, condos, and even manufactured homes in some cases.

- Occupancy: Must be your primary home.

#6. Down Payment Assistance (DPA) Programs

Best for: Buyers who have a stable job but haven't been able to save up 10K-20k in cash.

Think of DPA as the "boost" you need to cross the finish line. These are usually grants or "silent" second mortgages provided by state housing authorities. Some are forgivable, meaning if you stay in the house for, say, five years, you never have to pay the money back. The downside? These programs sometimes come with a slightly higher interest rate on your main loan to offset the risk.

Requirements:

- First-Timer Rule: Generally haven't owned in 3 years.

- Income/Price Caps: These vary by county. Check your local housing authority's 2026 limits.

- Education: A HUD-approved counseling class is almost always mandatory.

- Cash Reserves: Some programs require you to have at least $1,000-$2,000 of your own skin in the game.

#7. State & Local First-Time Buyer Programs

Best for: People buying in specific states or cities that want to "stack" benefits.

State agencies (like CalHFA or SONYMA) are often more aggressive than national ones. They offer "packages" that might combine a low-interest loan with a $15,000 grant for closing costs. I've seen local city programs offer even more if you buy in "target" neighborhoods. It's always worth checking your specific city's "Housing and Community Development" website to see what's currently funded.

Requirements:

- Residency: You must be buying within that state or city's borders.

- Credit: Usually follows standard 620--640 credit score minimums.

- Primary Residence: You must live there. These aren't for "house flipping."

- Funding: These are "first-come, first-served," so you have to move when the money is available.

#8. Good Neighbor Next Door

Best for: Teachers, law enforcement, firefighters, and EMTs.

This program sounds too good to be true, but it's real. HUD offers certain homes at a 50% discount to public servants. If a house is listed at $300,000, you can get it for $150,000. The "catch" is that these homes are in specific "revitalization areas," and you must commit to living there for at least three full years. It's an incredible way to build instant wealth through equity.

Requirements:

- Career: Full-time employment in an eligible public service field.

- Home Choice: Must be a HUD-listed "Good Neighbor" property.

- Commitment: 36-month residency requirement is strictly enforced.

- Financing: You can use an FHA or conventional loan (VA loans often not compatible due to the silent second mortgage).

#9. HUD $100 Down Program

Best for: Buyers with very low cash savings who are willing to buy a foreclosed property.

If you have an FHA-eligible credit score but your bank account is near zero, this is your play. HUD offers select foreclosed homes for just a $100 down payment. It's designed to get families into homes quickly and stabilize neighborhoods. The inventory is limited to what HUD currently owns, so you have to be flexible on the house's condition and location.

Requirements:

- Loan Type: Must use FHA-insured financing.

- Property: Only eligible for HUD-owned homes found on the HUD Homestore site.

- Owner Occupant: You must intend to live in the home (no investors).

- Offer: Your agent must specifically mention the $100 down incentive in the bid.

#10. Federal Home Loan Bank (FHLB) Programs

Best for: Lower-income families who have started saving but need a "matching" partner.

The FHLB works through local banks to offer "matching" grants. They offer grants up to $15,000 (specific amounts vary by FHLB bank. Not always a strict dollar-for-dollar match). It's a literal "reward" for your savings habit. It's not a loan you pay back. It's a grant, provided you stay in the home for a few years.

Requirements:

- Income: Generally must earn 80% or less of the Area Median Income.

- Lender: You have to use a bank that is a member of the FHLB system.

- Time: You typically have to keep the home for 5 years to have the grant fully forgiven.

- Training: Homebuyer education is usually required.

Which First-Time Homebuyer Program to Choose?

Choosing the right program isn't about finding the "best" one on paper. It's about matching your current financial reality. Here's a quick logic check to help you narrow it down:

- If your credit score is 580-620: The FHA Loan is your most realistic path. It's the most forgiving when it comes to past credit mistakes.

- If you have $0 saved up: Check if you qualify for VA or USDA. If not, your only path is finding a DPA Grant or the HUD $100 Down program.

- If you have 700+ credit but only 3% down: Skip FHA and go with HomeReady or Home Possible. You'll get a better rate and cheaper insurance.

- If you are a teacher or first responder: Check the Good Neighbor list first. That 50% discount is life-changing if you find a house you like.

Don't try to DIY this decision. A professional loan officer can run "side-by-side" comparisons to show you exactly how much each option costs over 5 or 10 years.

FAQs About Top First-Time Homebuyer Program

Q1. What is the 3 7 3 rule in mortgage?

This rule protects you from being rushed into a bad deal. You must receive your Loan Estimate within 3 days of applying. You can't close until at least 7 days after that. Finally, you must have your Closing Disclosure in hand for 3 days before you sign the final papers to ensure no fees were "snuck in."

Q2. What is a red flag in a mortgage?

Lenders hate surprises. Red flags include large cash deposits that you can't prove came from a legal source, quitting your job during the process, or opening a new credit card to buy furniture before the house is actually yours. Keep your finances "boring" and static until you have the keys.

Q3. What is the best option for first time buyers?

For most, a Conventional 97 (3% down) is the winner because you aren't stuck with mortgage insurance forever. However, if you are a veteran, the VA loan is the undisputed champion.

Q4. What salary do you need for a $400,000 house?

With 2026 interest rates, you generally need a household income of $130,000 to $140,000 to comfortably afford a $400k home without being "house poor". Lenders look for your total housing cost to be under 30% of your gross monthly pay.

Q5. What first-time homebuyer Programs are zero down?

The heavy hitters are VA and USDA loans. Beyond those, you can achieve "zero down" by combining a 3% conventional loan with a Down Payment Assistance (DPA) grant that covers that 3%.

Conclusion

Closing on your first home is one of the most stressful yet rewarding things you'll ever do. In the 2026 market, the "old" advice of saving 20% is mostly dead. The new strategy is about leveraging these programs to get in early and let home appreciation build your wealth for you. Whether it's an FHA loan for a fixer-upper or a USDA loan for a suburban sanctuary, there is almost certainly a path that fits your budget.

If you're still feeling unsure where you stand, don't leave it to chance. I recommend using the Bluerate AI Agent. It's an incredibly smart tool that can digest your income and credit details to show you exactly which programs you qualify for in seconds. It's the fastest way to turn your "what if" into an "I'm moving in."