When Does PMI Go Away? 4 Key Ways Here to Know

I still remember staring at my first mortgage statement and feeling a knot in my stomach over that extra $200 charge. If you bought a house with less than 20% down, you're likely paying Private Mortgage Insurance (PMI) too. It protects the lender, but it certainly drains your wallet.

The good news? You don't have to pay it forever. If you're tired of throwing money away every month, I'm going to show you exactly when PMI legally has to drop off and four proven strategies to kick it to the curb even faster.

Key Takeaway

- 20% equity (80% LTV): The exact point where you can proactively request PMI cancellation.

- 22% equity (78% LTV): The legal threshold where your lender must automatically remove it.

- Good standing matters: A flawless payment history is required to drop the premium.

- Loan types dictate rules: Conventional loans follow the rules above, while FHA loans charge an MIP that lasts for the life of the loan if the down payment is less than 10%, or drops off after 11 years if 10% or more.

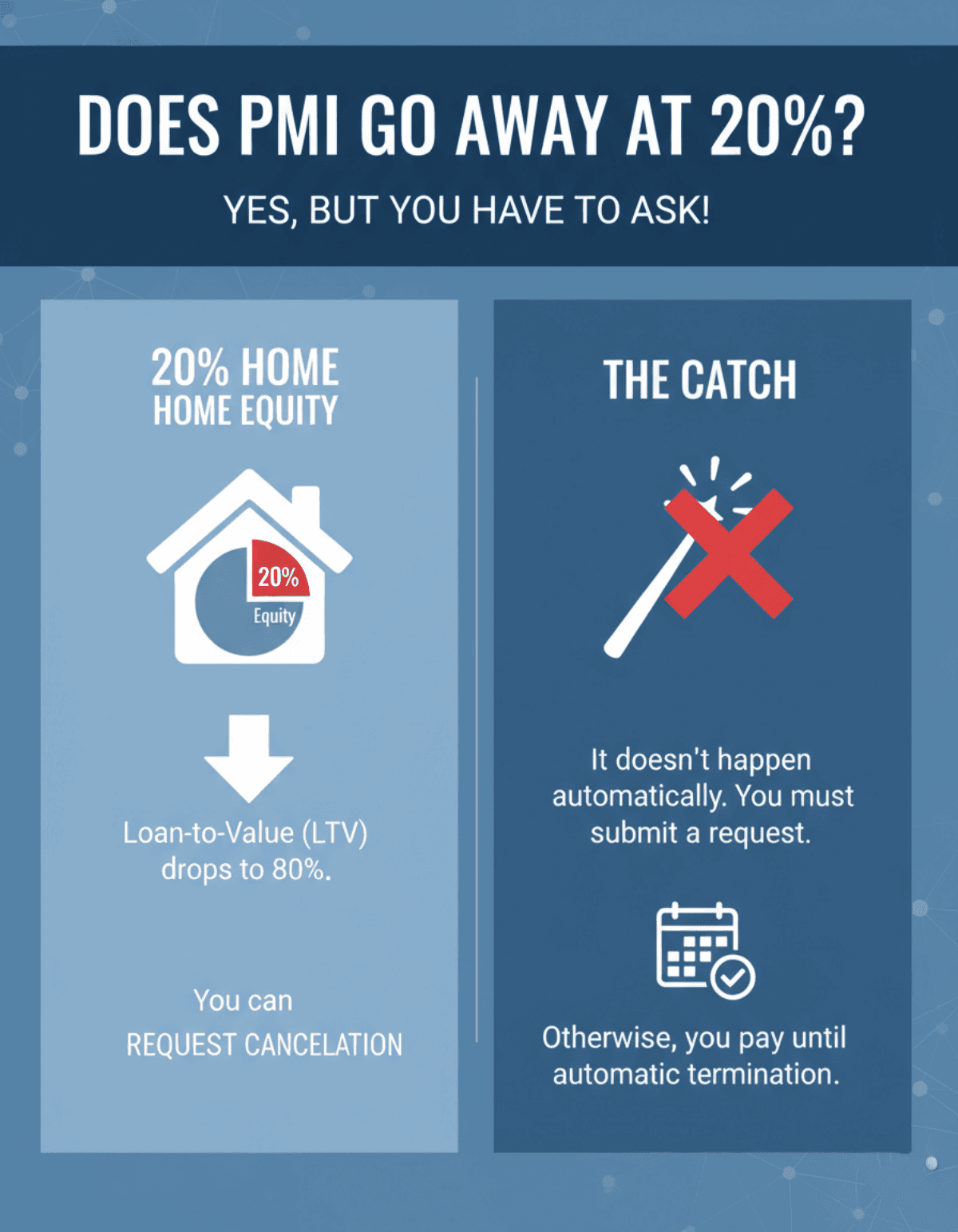

Does PMI Go Away at 20%?

Yes, but here is the catch: it doesn't happen magically on its own. When your home equity hits 20%, meaning your Loan-to-Value (LTV) ratio drops to 80%, the federal Homeowners Protection Act (HPA) grants you the right to ask for cancellation.

I see so many homeowners assume the fee will just vanish the moment they hit that threshold. It won't. Reaching 80% LTV simply puts the ball in your court to submit a request. If you sit back and do nothing, you'll keep paying until you reach the automatic termination mark.

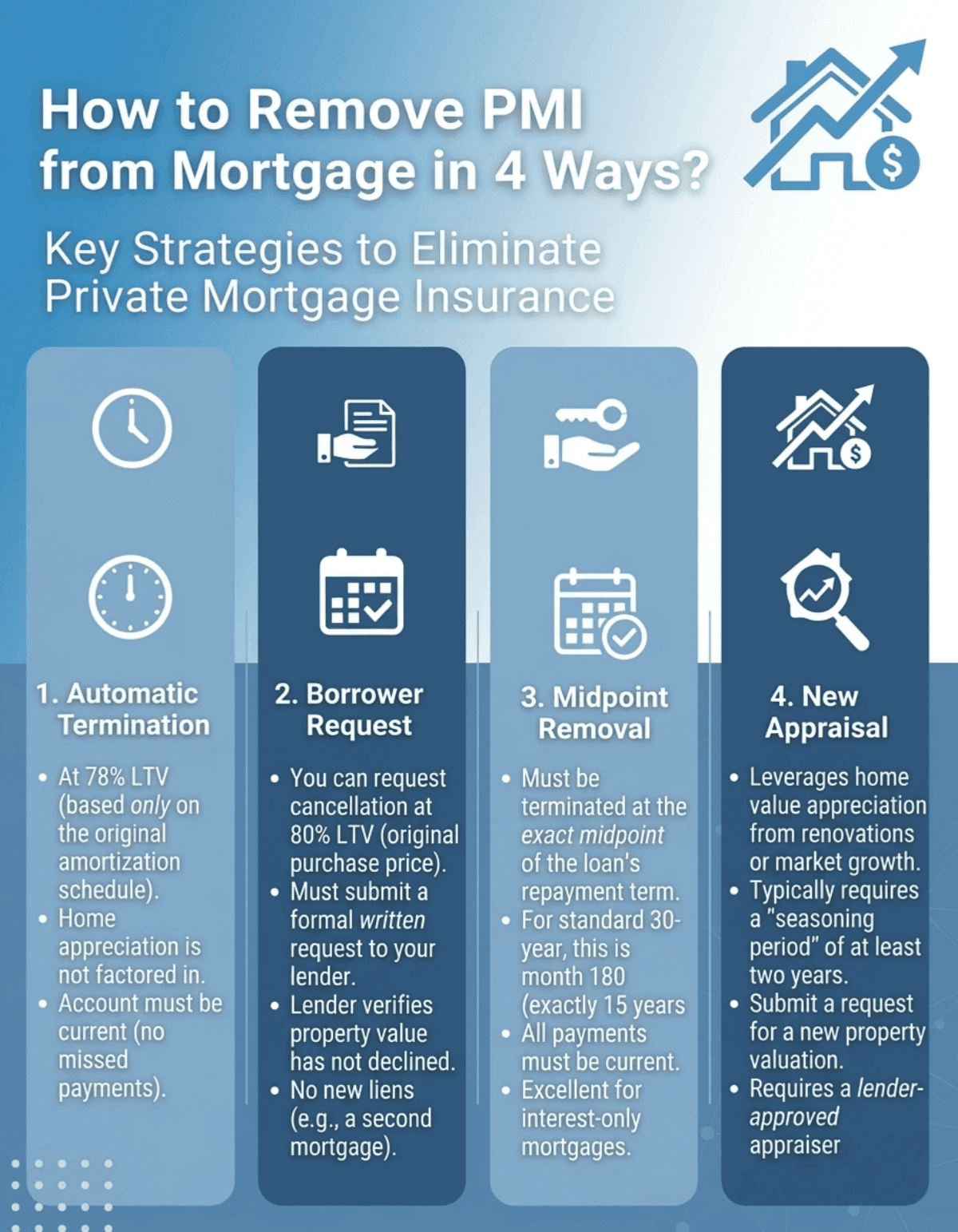

How to Remove PMI from Mortgage in 4 Ways?

Ready to stop paying that annoying premium? Depending on your financial situation and how your local real estate market is performing, here are four actionable ways to finally get rid of it.

Automatic Termination

If you prefer a hands-off approach, federal law requires lenders to automatically cancel your PMI once your mortgage balance reaches 78% LTV, which equals 22% equity.

However, there's a crucial detail most people miss: this 78% mark is based entirely on your original amortization schedule. It doesn't factor in if your home's value skyrocketed over the last few years. The lender simply looks at the original math from the day you closed. Also, for this automatic drop-off to kick in, your loan must be "current," meaning you aren't behind on any payments.

Borrower Request

Why wait for 78% when you can take action at 80%? If you've been making extra principal payments and your balance finally hits 80% of the original purchase price, you can ask your mortgage servicer to drop the PMI.

You must submit a written request. A quick phone call usually won't cut it. Your lender will then verify a few things. They need to ensure your property value hasn't declined since you bought it and that there are no new liens, like a second mortgage, attached to the house. Taking this proactive step can save you hundreds of dollars months before automatic termination triggers.

Midpoint Removal

This is a lesser-known rule that I absolutely love sharing with homeowners. Under the HPA, your PMI must be terminated at the exact midpoint of your loan's repayment term, even if your LTV hasn't reached 78% yet.

For example, if you signed a standard 30-year mortgage, the halfway point is month 180 (exactly 15 years in). Once you hit that month, the insurance requirement goes away by law, assuming your payments are current. This is particularly helpful for folks holding special structures, like interest-only mortgages, where the principal balance barely shrinks during the first decade.

New Appraisal (Home Value Appreciation)

If you live in a hot market or recently renovated your kitchen, you might be able to drop PMI without making extra payments. As your home's market value goes up, your LTV naturally goes down.

Typically, lenders require a "seasoning period" of at least two years before they let you use appreciation to cancel the insurance. If you think your house has gained enough value to put your LTV below 75% or 80%, you can request a new appraisal. Just be careful: you absolutely must use a lender-approved appraiser. Don't hire someone on your own, or the bank will reject the report.

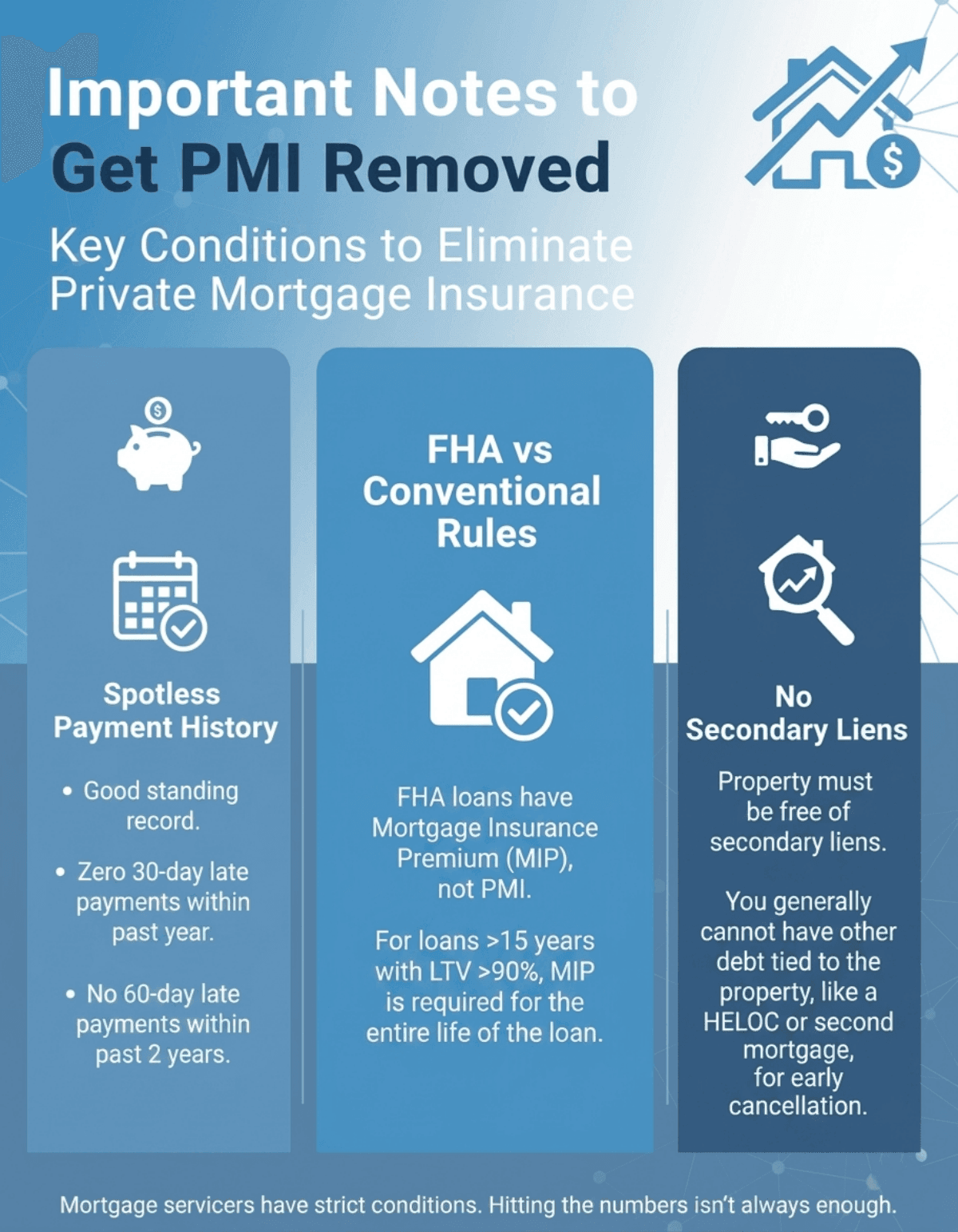

Important Notes to Get PMI Removed

Before you celebrate, you should know that mortgage servicers have strict fine print. Just hitting the right numbers won't guarantee success unless you also meet these conditions:

- Spotless Payment History: Lenders demand a "good standing" record. In plain English, this usually means zero payments that were 30 days late within the past year, and absolutely no 60-day late payments over the last 24 months.

- FHA vs. Conventional Rules: FHA loans don't have PMI. They charge a Mortgage Insurance Premium (MIP). For loans with terms over 15 years, if the initial down payment is less than 10% (LTV >90%), MIP is required for the entire life of the loan.

- No Secondary Liens: You generally cannot have other debt tied to the property, like a HELOC or second mortgage, if you want early cancellation.

Is It Better to Pay PMI or Put 20% Down?

There's a huge misconception that PMI is just a "scam." Honestly, it's an opportunity cost. Putting 20% down saves you from the monthly fee and drastically lowers your mortgage payment.

But if saving that 20% takes you five extra years, you might get priced out of a rising housing market. Putting down 3% to 5% and swallowing the PMI allows you to buy earlier, start building equity, and keep cash in the bank for emergencies or investments. It's not inherently bad. It's just a tool to help you get the keys faster.

FAQs About Getting Rid of PMI

Q1. When does PMI go away on an FHA loan?

FHA loans use MIP. For most FHA loans with terms over 15 years issued after June 3, 2013, if the initial down payment is under 10%, MIP lasts the life of the loan. If 10% or more, it drops off after 11 years.

Q2. Can remodeling my home help remove PMI?

Yes! Major upgrades like adding a bathroom or renovating a kitchen increase your property's overall market value. This naturally lowers your LTV ratio. You can then contact your lender to order a fresh appraisal and potentially remove the fee.

Q3. Do I need to refinance to get rid of PMI?

Not necessarily. For a conventional loan, you just need to reach the right LTV. However, if you have an FHA loan with permanent MIP, or if current market interest rates are significantly lower than what you're paying now, refinancing is definitely the smartest move.

Q4. Can you avoid PMI with 10% down?

Absolutely. You can use a "piggyback" loan structure, often called an 80-10-10 loan. You take out a main mortgage for 80%, a second loan for 10%, and put 10% down in cash. Just watch out, as the second loan usually carries a higher interest rate.

Q5. How much is PMI on a $300,000 loan?

Annual PMI cost typically range from 0.5% to 1.5% of your total loan amount. For a $300,000 mortgage, you are looking at roughly $1,500 to $4,500 a year. That breaks down to an extra $125 to $375 tacked onto your monthly payment.

Conclusion

The biggest takeaway here is that PMI isn't a life sentence. Whether you aggressively pay down your principal, ride the wave of market appreciation, or simply let the original amortization schedule run its course, you have options.

My best advice? Log into your mortgage portal today or call your loan servicer to find out your current LTV. Don't just sit back and wait for the automatic cancellation. By taking a proactive stance, you could easily keep thousands of hard-earned dollars in your own pocket where they belong.

People Also Read

- Self-Employed Mortgage Guide: How to Get, Requirements

- Best First-Time Home Buyer Lenders: Find Your Perfect Match

- Best First-Time Home Buyer Loans 2026: Pick the Right Choice

- Best First-Time Home Buyer Programs: Which One to Apply?

- [Solved] How Much Does it Cost to Refinance a Mortgage?

- PMI vs MIP: All the Differences Explained in 2026

- Best PMI Calculators: Estimate Your Private Mortgage Insurance

- 2026 Guide: How to Calculate PMI on Your Mortgage