2026 Guide: How to Calculate PMI on Your Mortgage

Are you struggling to figure out how to calculate PMI for your upcoming 2026 home purchase? When I was saving for my first house, realizing my down payment fell short of 20% was stressful because I knew private mortgage insurance would increase my monthly costs.

It sounds complicated, but there's a straightforward formula to determine this expense. While doing the math yourself is a great starting point, the most accurate way is to consult a nearby loan officer to get your exact PMI rate. Let me break down exactly how you can estimate these numbers today.

Key Takeaways

- Average 2026 Rates: PMI typically costs between 0.5% and 1.5% of your total loan amount annually.

- The Core Formula: Monthly PMI = (Total Loan Amount × Annual PMI Rate) ÷ 12.

- Cancellation Threshold: Request cancellation at 20% equity (80% LTV). Automatic termination at 22% equity (78% LTV).

What is PMI?

Private Mortgage Insurance (PMI) is a monthly fee added to your conventional loan if your down payment is less than 20% of the home's purchase price. I often remind homebuyers that while you pay the premium, PMI actually protects your lender in case you default on the payments. It's essentially the cost of getting into a house sooner without needing a massive cash reserve.

It's important to note that PMI specifically applies to conventional loans. If you're using an FHA or USDA loan, this coverage is called a Mortgage Insurance Premium (MIP) or a Guarantee Fee, which follows completely different calculation rules and requirements.

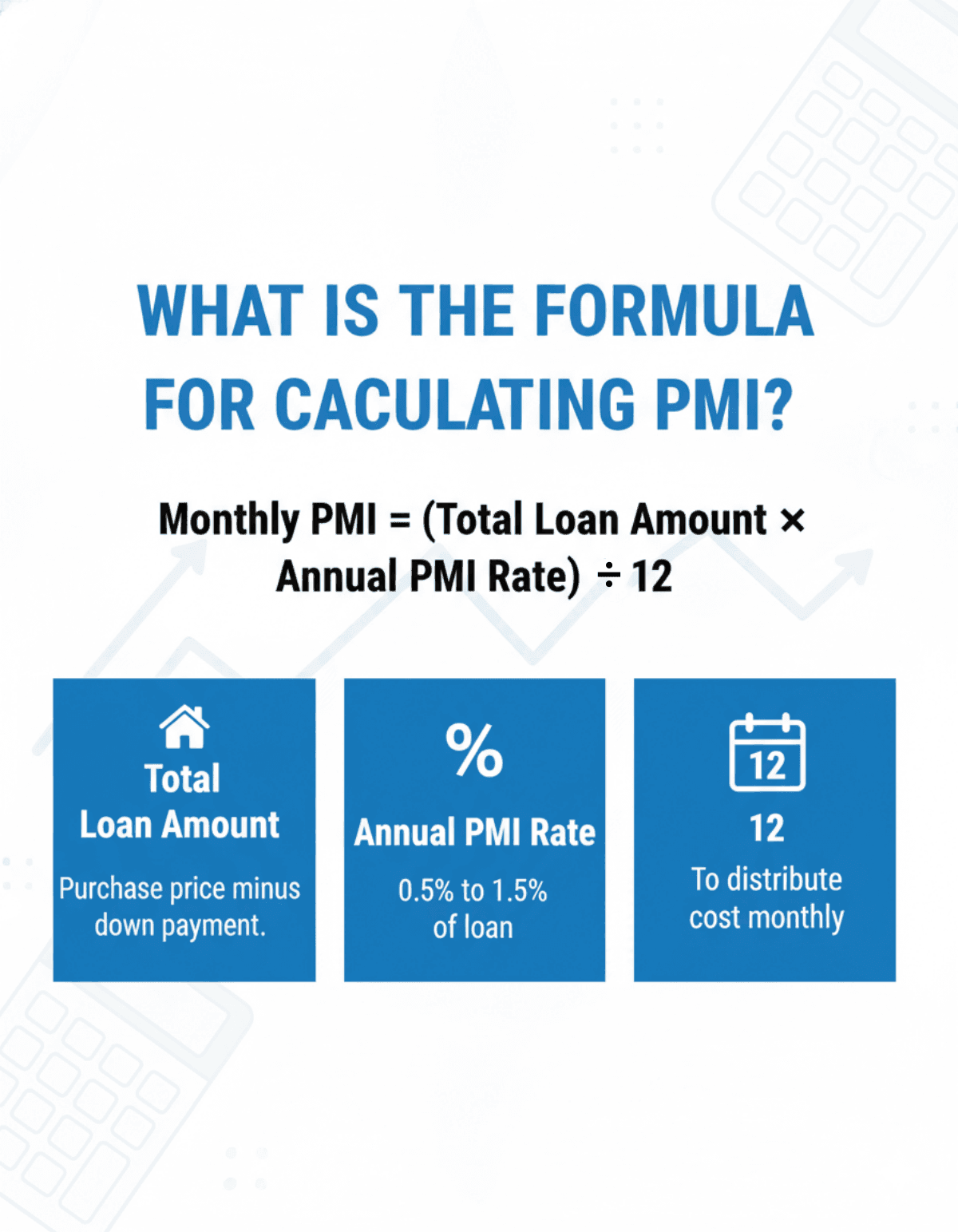

What is the Formula for Calculating PMI?

Finding out your estimated monthly cost isn't magic. You just need a simple math equation:

Monthly PMI = (Total Loan Amount × Annual PMI Rate) ÷ 12

Here is what each part of that equation means:

- Total Loan Amount: This is the final purchase price of your home minus your initial down payment.

- Annual PMI Rate: The percentage charged by your lender based on your financial profile (usually between 0.5% and 1.5%).

- 12: We divide the annual total by 12 to distribute the cost evenly across your standard monthly mortgage payments.

Example of PMI Calculation

Let's look at a realistic scenario for the 2026 US housing market. Suppose you are buying a $400,000 home. You put down 5%, which is $20,000. That leaves you with a total loan amount of $380,000.

Let's assume your credit is decent, and your lender quotes an annual PMI rate of 0.75%.

We plug these numbers into our formula:

- $380,000 × 0.0075 = $2,850 (This is your total annual PMI cost)

- $2,850 ÷ 12 = $237.50

In this example, you will be paying an extra $237.50 every month on top of your principal, interest, taxes, and standard homeowners insurance.

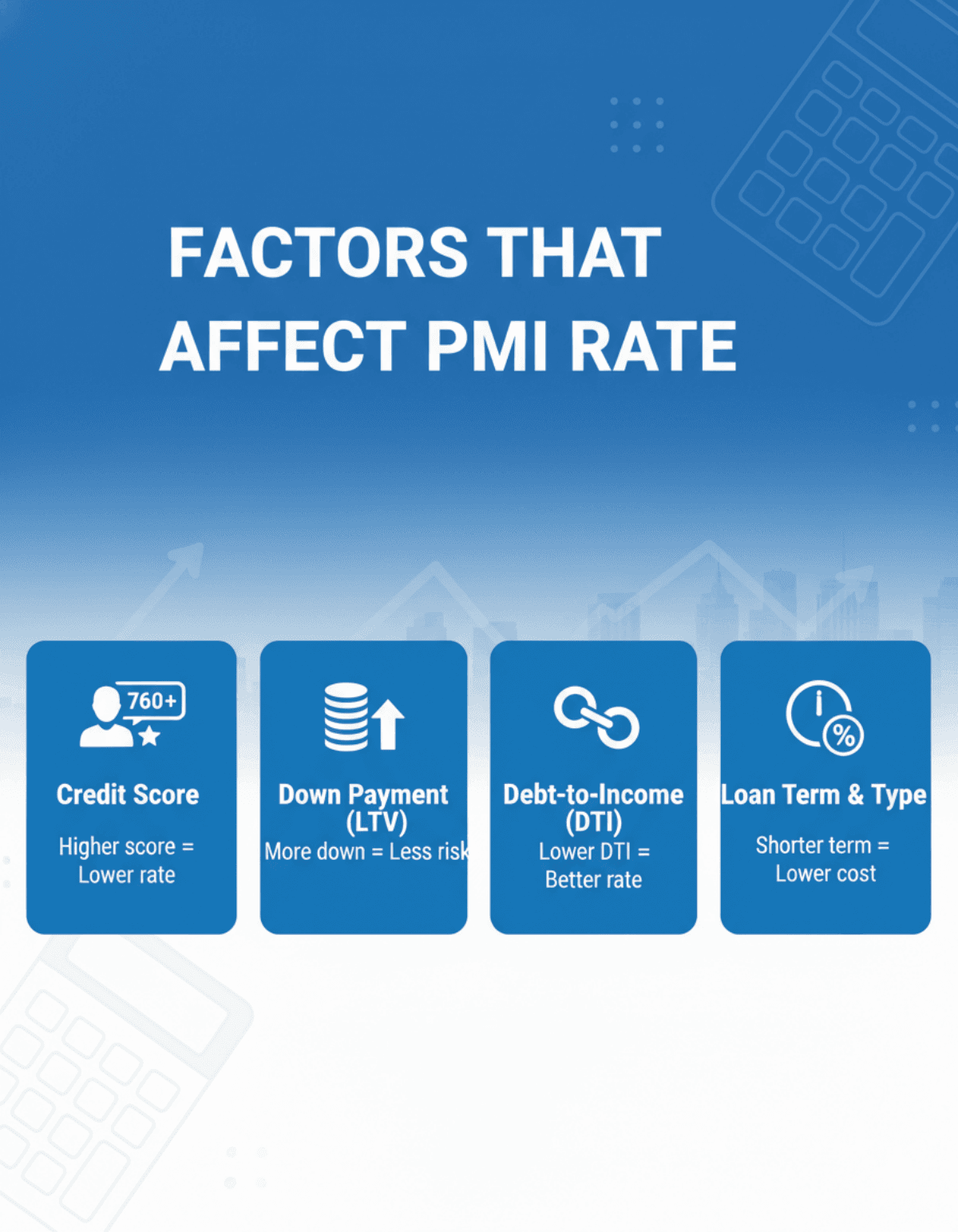

Factors that Affect PMI Rate

Your PMI rate is never a fixed, one-size-fits-all number. Lenders determine this percentage through a detailed risk assessment of your financial health. Here are the main factors that influence how much you'll pay:

- Credit Score: This is the biggest driver. According to the Urban Institute, borrowers with excellent credit (760+) might pay around 0.46%, while those with scores in the low 600s could see rates up to 1.5%.

- Down Payment (LTV Ratio): Your Loan-to-Value ratio matters. Putting down 15% carries less risk for the lender than putting down 3%, resulting in a cheaper premium.

- Debt-to-Income (DTI) Ratio: A higher burden of existing debts makes you a riskier borrower, potentially bumping up your rate.

- Loan Term & Type: Adjustable-rate mortgages (ARMs) or 30-year terms usually have slightly higher mortgage insurance costs compared to fixed 15-year loans.

Where to Get the PMI Rate?

While doing your own math using industry averages is helpful for preliminary budgeting, it won't give you the exact penny you'll owe. To secure an accurate figure, you need to consult professional channels:

- Industry Averages: Great for rough estimates, like the 0.5% - 1.5% benchmark.

- Lender Quote (Loan Estimate): Once you apply, lenders must provide an official Loan Estimate (LE) document showing your precise rate.

- Bluerate: I highly recommend matching with a professional to review your unique situation. You can connect with a local loan officer for free on Bluerate to get customized PMI rates based on your specific financial profile.

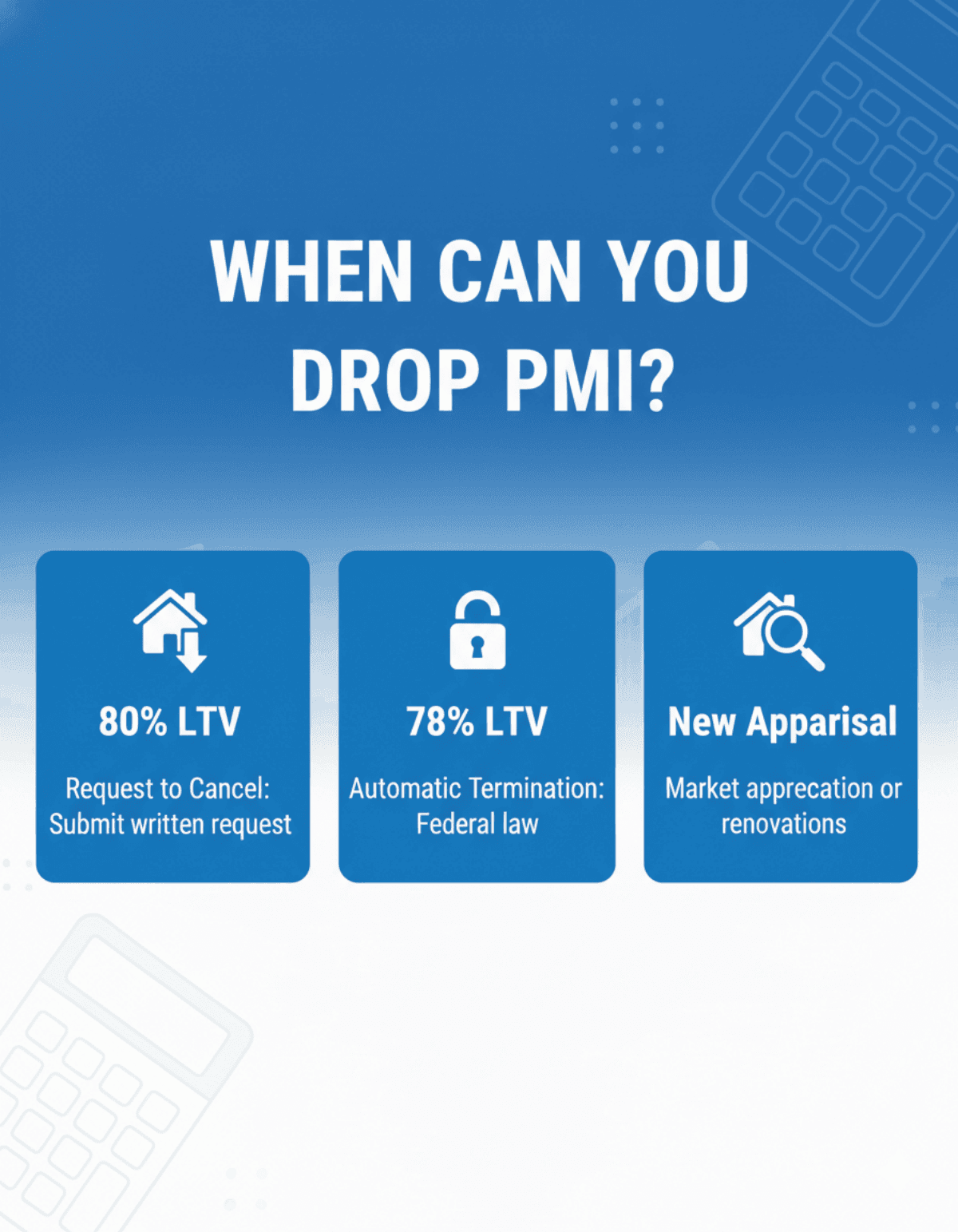

When Can You Drop PMI?

The best news is that PMI doesn't last forever. You can get rid of this expense once you build enough equity. Here are the standard ways to remove it:

- 80% LTV (Request to Cancel): When your mortgage balance drops to 80% of the home's original value, proactively submit a written request to your lender to cancel it.

- 78% LTV (Automatic Termination): By federal law, lenders must automatically terminate your PMI once your loan balance reaches 78%.

- New Appraisal: If your home's value skyrockets due to market appreciation or major renovations, you can order a new appraisal to hit that 20% equity mark ahead of schedule.

FAQs About Calculating PMI

Q1. How much is PMI on a $300,000 mortgage?

Assuming a 5% down payment, your loan amount is $285,000. With an average rate between 0.5% and 1.5%, your estimated monthly PMI will land roughly between $118 and $356. Ultimately, your exact credit score will determine where you fall in that range.

Q2. Is PMI calculated on the purchase price or loan amount?

Your private mortgage insurance is strictly calculated based on your total loan amount, not the property's overall purchase price. Because your down payment instantly creates equity, the lender only charges you the insurance premium on the actual money you are borrowing from them.

Q3. Does PMI go away once you hit 20% equity?

Yes, but it's not always automatic. When you reach 20% equity (an 80% LTV ratio), you must proactively contact your lender to request cancellation. If you wait, the lender is only legally obligated to automatically drop it when you reach 22% equity (78% LTV).

Q4. Can I pay PMI upfront instead of monthly?

Absolutely. This is called Single-Premium PMI. You can pay the entire insurance cost as a lump sum at closing. I often suggest this route for buyers who have extra cash on hand, as it lowers their overall monthly mortgage payment right from the start.

Q5. Are PMI premiums tax-deductible in 2026?

Yes, reinstated permanently for the 2026 tax year. Full deduction if AGI under $100,000 ($50,000 if married filing separately). Phases out up to $109,000 ($109,500). Consult a tax professional, as rules may vary. However, IRS rules change frequently, so always consult a licensed tax professional.

Conclusion

Figuring out your mortgage insurance doesn't require an advanced math degree. As we've covered, calculating PMI simply comes down to knowing your total loan amount and finding out your personal annual rate. While nobody enjoys paying an extra fee, I always remind my clients that PMI is a valuable tool. It allows you to stop renting and buy your dream home years earlier than if you had to save up a massive 20% down payment.

Don't let the fear of unknown numbers delay your 2026 real estate goals. The best way to make an accurate budget is to get real data. Ready to find out your exact PMI rate? Visit Bluerate.ai today to match with an experienced loan officer who can run the numbers for your 2026 home purchase.