How Much Does PMI Cost? Rates, Factors & Calculation

Saving up for a down payment is hard enough for any homebuyer today. But just when you think you've finally hit your target, you check your mortgage estimate and spot a mysterious extra monthly fee: Private Mortgage Insurance.

It feels like a penalty for not having enough cash upfront, right? I've been there, and I know how frustrating it is. If you are wondering exactly how much does PMI cost, you are in the right place. I'll break down the real numbers, how it's calculated, and most importantly, how you can eventually get rid of it.

Key Takeaways

- Average Rate: Annual PMI premiums typically range from 0.5% to 1.5% of your total loan amount.

- The Trigger: You will have to pay this fee if your down payment is less than 20% on a conventional loan.

- Who It Protects: Despite the name, this insurance protects your lender in case you default, not you.

- Cancellation: It isn't forever. You can drop it once you reach 20% equity in your property.

What is PMI?

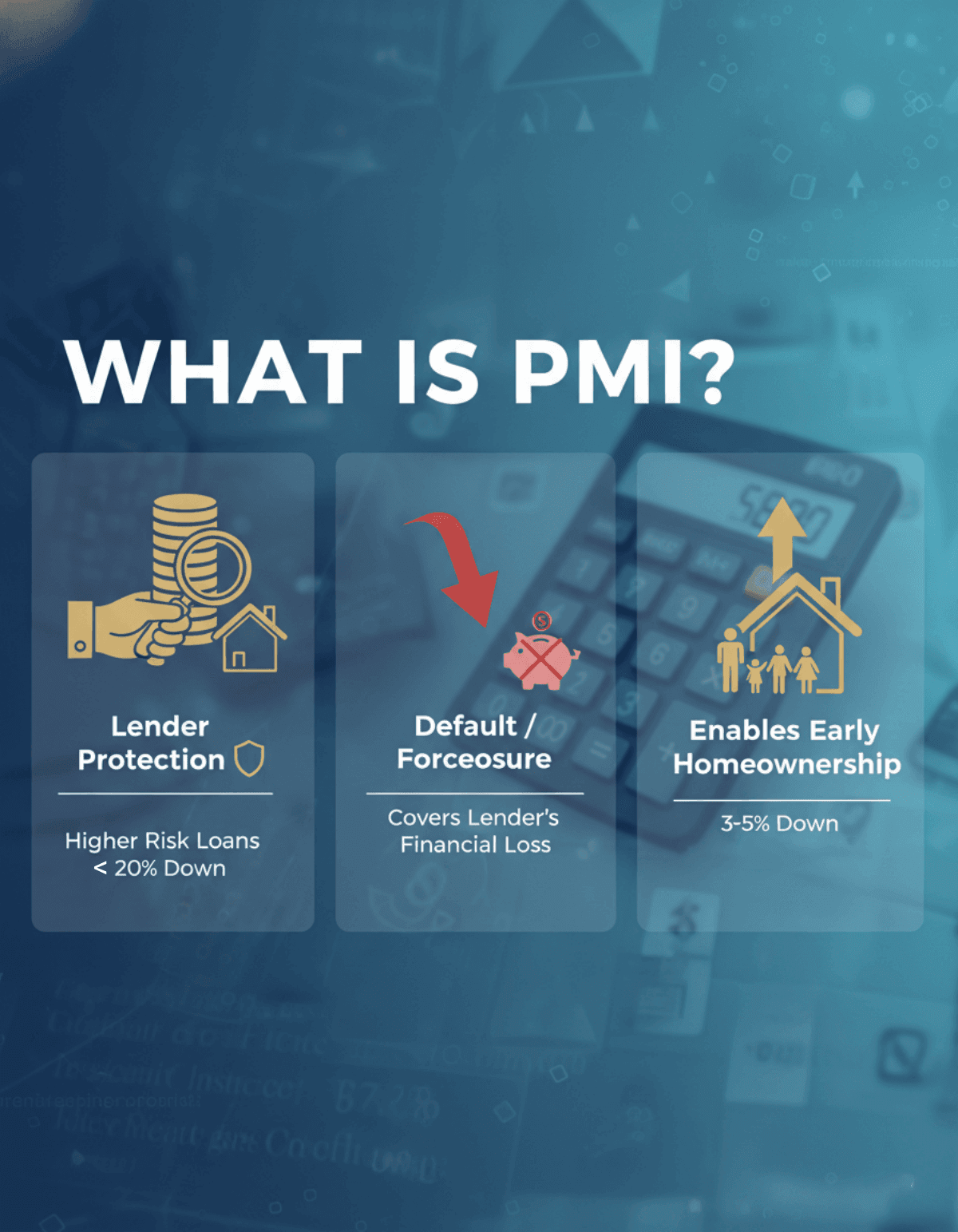

Whenever I review loan estimates with first-time buyers, I always have to clarify a major misconception. People assume Private Mortgage Insurance (PMI) is like homeowner's insurance, protecting their family if something goes wrong. Unfortunately, that's not the case. PMI exists solely to protect the lender.

Because you are putting down less than 20%, banks view your loan as a higher risk. If you stop making payments and they have to foreclose, this policy covers their financial losses. According to the Consumer Financial Protection Bureau (CFPB), this system is actually what allows lenders to offer mortgages to folks who can't save a massive lump sum. So, while it feels like a pesky added expense, it's also the specific tool that makes early homeownership possible for millions of people who only have 3% or 5% to put down.

How Much Does PMI Cost?

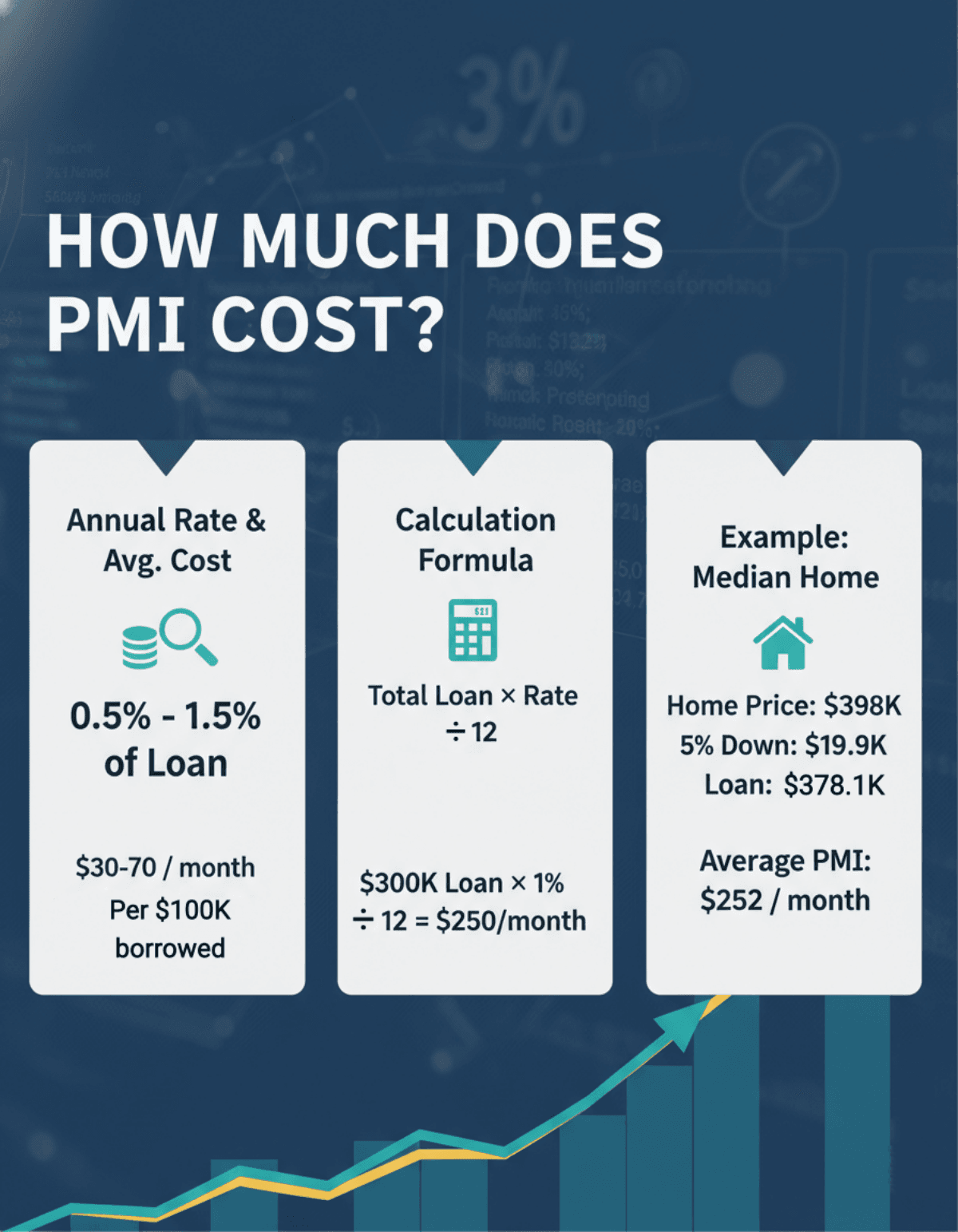

So, let's get to the math. As a general rule of thumb, you can expect your annual premium to cost between 0.5% and 1.5% of your original loan amount. Freddie Mac estimates that borrowers usually pay roughly $30 to $70 per month for every $100,000 borrowed.

To figure out your exact monthly burden, you don't need complex software. Just use this straightforward formula:

Total Loan Amount × Annual PMI Rate ÷ 12 = Your Monthly PMI Fee

For instance, if your lender assigns you a 1% rate on a $300,000 mortgage, your annual cost is $3,000. Divide that by 12, and you'll be paying $250 every single month on top of your standard principal, interest, taxes, and insurance. The exact percentage you get hit with isn't random. Lenders calculate it based on your unique financial profile.

Also Read: 2026 Guide: How to Calculate PMI on Your Mortgage

Average PMI Cost

Recent data shows the median home price is hovering around [$398,000](https://www.scrippsnews.com/us-news/housing/us-homes-sales-rose-in-february-as-homebuyers-seized-on-easing-mortgage-rates). If you make a 5% down payment ($19,900), your loan amount is $378,100.

Assuming an average mid-tier rate of 0.8%, your annual premium would be $3,025. On average, a typical American buyer purchasing a median-priced home will spend roughly $252 per month on mortgage insurance.

Over a few years, that easily adds up to thousands of dollars.

Factors that Affect PMI Cost

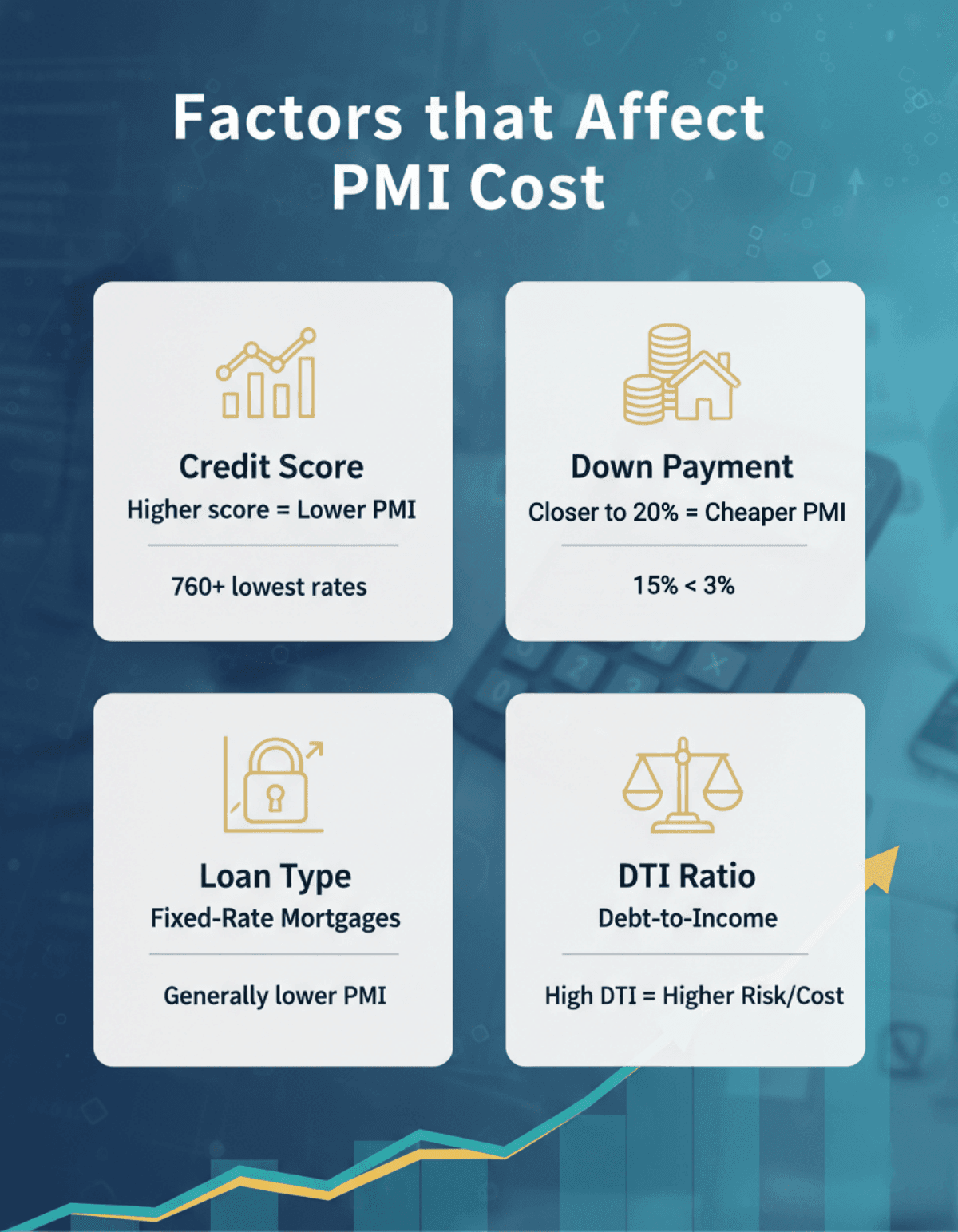

You aren't just handed a flat fee. Insurance companies run a strict risk analysis on you. Here are the main factors that dictate your final price:

- Credit Score: This is the biggest factor within your control. Excellent credit (760+) secures the lowest premiums, while scores in the low 600s will cause your costs to skyrocket.

- Down Payment Amount: The closer you are to that magic 20% mark, the cheaper it gets. A 15% down payment triggers a much lower rate than a 3% one.

- Loan Type: Fixed-rate mortgages generally carry cheaper insurance premiums than adjustable-rate mortgages (ARMs) because the monthly payments are predictable.

- DTI Ratio: If a large chunk of your monthly income already goes toward paying off other debts (Debt-to-Income), insurers see you as a higher risk, raising your premium accordingly.

How to Pay PMI?

Most people just assume they have to pay this fee monthly, but lenders actually offer a few different structures. Here is how you can handle the bill:

- Monthly Premium: This is the most common route. The fee is simply baked into your monthly mortgage payment. It's convenient, and it automatically drops off once you hit enough equity.

- Upfront Premium (LPMI): You pay the entire policy cost as a lump sum at closing. The pro is that your monthly payment stays lower. The huge con? If you move or refinance two years later, this upfront cash is usually non-refundable.

- Hybrid: You pay a portion upfront at closing and finance the rest into your monthly bill. This is a solid middle ground if you want to lower your monthly burden but don't want to risk losing a massive lump sum.

How to Avoid or Remove PMI?

Nobody wants to pay this fee forever. In my experience, taking an active approach to dropping your mortgage insurance is the easiest way to save money.

How to get rid of PMI?

- Save 20%: It's tough, but reaching a 20% down payment bypasses the requirement completely.

- Use a Piggyback Loan: This involves an 80/10/10 structure. You take out a first mortgage for 80%, a second loan (like a HELOC) for 10%, and put 10% down in cash.

- Get a VA Loan: If you are a veteran or active military member, VA loans require zero down payment and absolutely no ongoing mortgage insurance.

How to remove it later?

- Request Cancellation: Once your equity reaches 20% (80% LTV), you can formally ask your servicer to remove it. You can speed this up by making extra principal payments or ordering a new appraisal if your home's value has spiked.

- Automatic Cancellation: By law, your lender must automatically drop the policy when your loan balance is scheduled to reach 78% of the original purchase price based on the amortization schedule.

FAQs About PMI Cost

Q1. How much is PMI on a $300,000 mortgage?

A $300,000 mortgage typically incurs a PMI of $1,500 to $4,500 annually. This translates to about $125 to $375 per month. Your exact bill will depend heavily on your current credit score and how much cash you put down at closing.

Q2. How much is PMI on $400,000?

For a $400,000 loan, you can expect your annual cost to range from $2,000 to $6,000. Broken down, that means you will be paying roughly $166 to $500 monthly. A higher credit profile keeps you closer to the lower end of that spectrum.

Q3. Is PMI 10% or 20%?

No, the premium rate itself is never 10% or 20%---it is usually just 0.5% to 1.5%. Those larger numbers refer to your down payment. If your upfront down payment is less than 20%, it triggers the insurance requirement.

Q4. When does PMI go away?

You can proactively ask your lender to cancel it once your home equity reaches 20% (an 80% Loan-to-Value ratio). If you don't ask, lenders are legally required to automatically terminate the policy once your mortgage balance drops to 78% of the original purchase price.

Final Word

Seeing an extra couple of hundred dollars tacked onto your monthly housing bill is never fun. However, rather than viewing this insurance as a pure financial loss, I encourage you to see it as a temporary stepping stone. It allows you to stop renting, secure a property, and start building long-term wealth years earlier than if you had to save up a massive 20% down payment.

Keep a close eye on your local market values and aggressively pay down your principal when possible. Ready to run your own numbers? Speak with a mortgage professional today to review your options and map out a clear plan to drop that fee as soon as possible.

People Also Read

- 3 Methods: How to Calculate Debt-to-Income Ratio for Mortgage?

- How to Calculate Early Payoff of Mortgage? Formula and Penalty

- How to Pay off Mortgage Faster? Pros, Cons, and 7 Ways for You

- Home Refinance Meaning: What Does Refinance Mean?

- PMI vs MIP: All the Differences Explained in 2026

- Best PMI Calculators: Estimate Your Private Mortgage Insurance