Best PMI Calculators: Estimate Your Private Mortgage Insurance

Buying a home is expensive enough without hidden costs sneaking up on you. If your down payment is less than 20%, you've probably hit that annoying roadblock: Private Mortgage Insurance (PMI). It's an extra monthly fee that protects the lender, not you.

Figuring out exactly how much this will add to your monthly budget used to give me a headache. A reliable PMI calculator is the easiest way to estimate this expense and figure out when you can finally drop it. I've personally tested the top tools available in 2026 to see which ones are the most accurate, user-friendly, and actually helpful for your homebuying journey. Here are my top picks.

Key Takeaways

- Best User Experience: NerdWallet wins for clear, easy-to-read visual charts.

- Credit Impact: Experian uniquely highlights how your credit score alters your premium.

- The Bottom Line: PMI isn't permanent. The right calculator helps you pinpoint the exact month you'll build 20% equity and can cancel the insurance.

Why Use a PMI Calculator?

Trying to calculate mortgage insurance manually is a fast track to frustration because the math changes based on your home price, loan type, and credit score. Instead of guessing, running the numbers through a dedicated tool gives you instant clarity. Here is why you need one:

- Accurate Budgeting: You'll see your true monthly payment, combining principal, interest, taxes, and PMI.

- Easy Scenario Testing: Compare how bumping your down payment from 5% to 10% drops your monthly premium.

- Cancellation Planning: These tools map out exactly when your home equity hits that magic 20% mark so you know exactly when to request a PMI cancellation.

How We Evaluated These PMI Calculators?

To find the most reliable options, I didn't just look at search results; I ran identical sample numbers through dozens of platforms. I judged them based on input flexibility---like whether they let you adjust credit scores---and data accuracy. I also paid close attention to user interfaces, preferring tools that offered visual amortization charts without overwhelming the screen with ads.

4 Best PMI Calculators in 2026

Based on my hands-on testing, here are the 4 most accurate and user-friendly PMI calculators available right now. I broke down what each tool does best to help you choose the right fit.

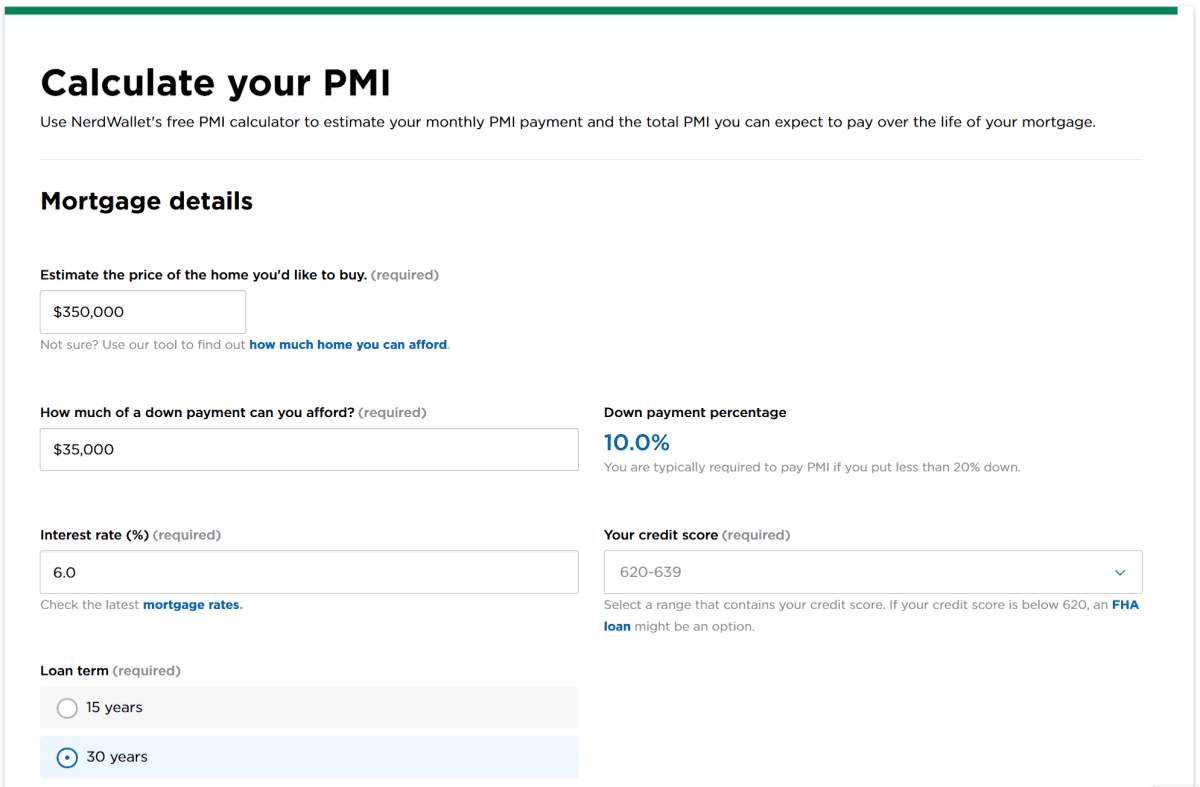

Nerdwallet PMI Calculator

Website: https://www.nerdwallet.com/mortgages/calculators/pmi

NerdWallet is famous for turning complex financial math into something visually digestible, and their mortgage tool is no exception. It's my go-to recommendation for first-time buyers who need visual feedback. Beyond the standard home price and down payment, it lets you select credit score ranges. The output gives a crisp breakdown of your monthly PITI plus the exact insurance cost. The design is minimal and strictly text-based. It skips fancy graphs in favor of straightforward, hard numbers.

- Pros: Beautiful, beginner-friendly interface; accurately includes credit score impacts.

- Cons: The page has a few partner advertisements that might distract you from the actual data.

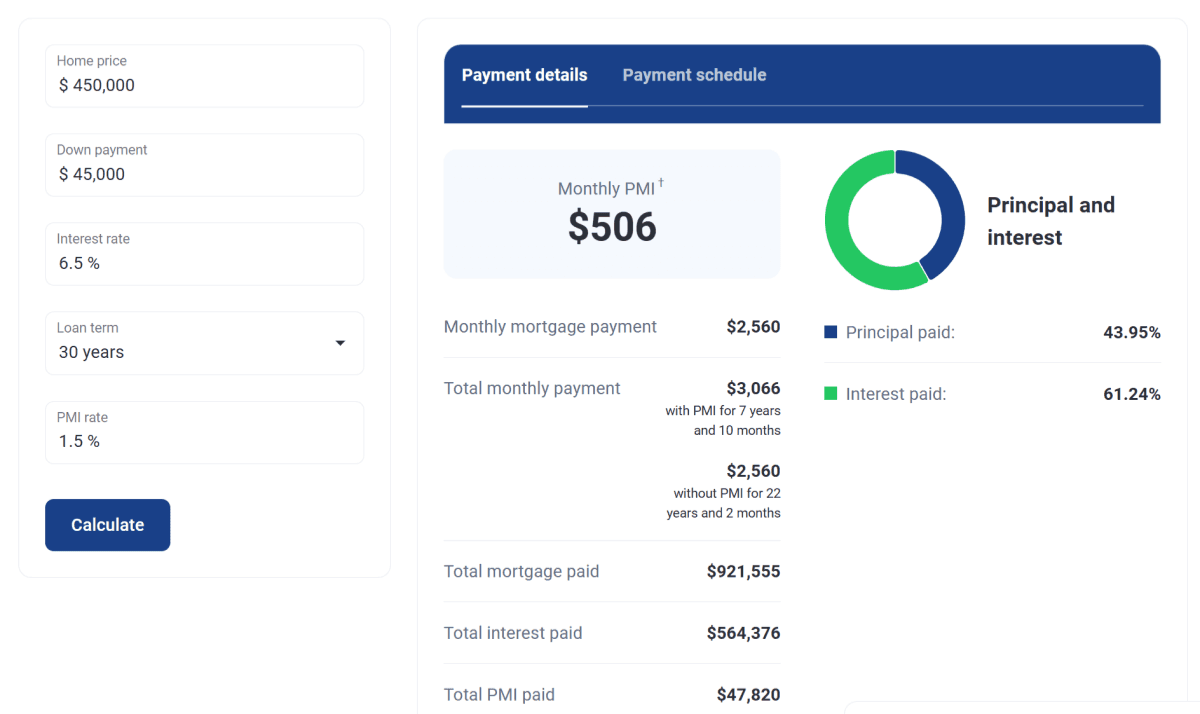

Experian PMI Calculator

Website: https://www.experian.com/blogs/ask-experian/mortgage-insurance-calculator/

As one of the three major US credit bureaus, Experian brings a unique angle to the table. Their calculator heavily emphasizes how your credit history directly dictates your insurance rate.

You enter home price, down payment, interest rate, loan term, and an estimated PMI rate (typically 0.2% to 2.0%). It then shows your monthly PMI and total payments. It reveals your monthly payment and estimates the PMI percentage rate.

The interactive donut chart is fantastic. You can see exactly what slice of your monthly payment goes toward principal versus insurance.

- Pros: Offers the most realistic rate adjustments based on specific credit score tiers.

- Cons: Lacks a visual amortization schedule, making it harder to map out when the premium will finally fall off.

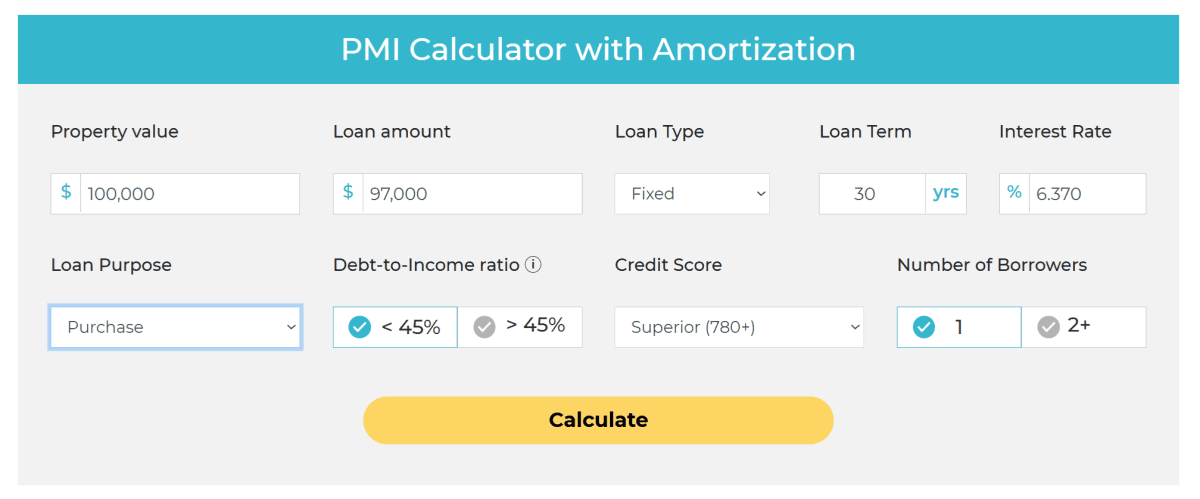

HSH PMI Calculator

Website: https://www.hsh.com/calc-pmi.html

HSH is a veteran mortgage data provider. While the site looks a bit old-school, the tool is a powerhouse for number crunchers who want detailed, granular control over their loan parameters.

You can adjust loan types (like ARMs vs. Fixed), purpose (purchase vs. refi), and precise credit brackets. It generates a comprehensive amortization table and your automatic cancellation date.

The layout feels a bit dated, but the detailed amortization schedule it generates is simply unmatched for long-term planning.

- Pros: Extremely customizable; tells you the exact month and year your insurance drops off.

- Cons: The traditional interface and sheer volume of numbers might feel intimidating for absolute beginners.

CreditKarma PMI Calculator

Website: https://www.creditkarma.com/calculators/mortgage/pmi

Credit Karma excels at tying your overall financial health to your borrowing power. I found their calculator incredibly responsive, especially when testing it on a smartphone screen.

It requires your target price, down payment, interest rate, and estimated FICO score. It calculates the premium while helping you keep an eye on your overall debt-to-income (DTI) ratio.

The mobile-friendly design is flawless. It's clearly built for users who are checking numbers on the go while actively touring open houses.

- Pros: Great mobile experience; smoothly connects your credit profile to the calculation.

- Cons: Might prompt you to create an account if you want to save your customized scenarios.

FAQs About PMI Calculators

Q1. What is PMI and when is it required?

Private Mortgage Insurance is a fee that protects the lender if you default on your loan. You are generally required to pay it if you buy a home with a conventional mortgage and put down less than 20% of the purchase price.

Q2. How accurate are online PMI calculators?

They provide a very solid estimate, but they aren't perfect. Your final premium depends on your lender's specific policies and your official credit report. Always use these tools for budgeting, but rely on your official Loan Estimate for the exact cost.

Q3. Does my credit score affect my PMI rate?

Absolutely. Lenders view a lower credit score as a higher risk, meaning your insurance premium will cost more. Maintaining a score above 760 usually secures the lowest possible monthly rate, while a score in the 600s will drive the price up.

Q4. Can I avoid paying PMI without a 20% down payment?

Yes, you have a few options to get rid of PMI. VA loans don't require it, and some lenders offer Lender-Paid Mortgage Insurance (LPMI). However, with LPMI, you usually accept a slightly higher interest rate for the entire life of the loan to cover the cost upfront.

Q5. How long do I have to pay PMI?

You don't have to pay it forever. Once your home equity reaches 20% of the original purchase price, you can formally request your lender to cancel it. If you do nothing, lenders are legally required to terminate it automatically at 22% equity.

Final Word

Paying an extra fee every month isn't exactly fun, but PMI does serve a vital purpose: it allows you to buy your dream home years before you could comfortably save up a massive 20% down payment. The five tools I tested will absolutely help you take control of your budget and plan for the future.

Just keep in mind that online calculators only provide estimates. Before making any final financial decisions, I highly recommend taking these preliminary numbers to a licensed mortgage broker or lender to get an official Loan Estimate. By knowing your numbers beforehand, you'll be negotiating from a place of confidence.