PMI vs MIP: All the Differences Explained in 2026

I still remember the headache of navigating my first home purchase. I was drowning in alphabet soup, only to realize my 10% down payment wasn't going to cut it without triggering mortgage insurance costs. If you're buying a house in 2026 with less than 20% down, you've probably stumbled across two confusing acronyms: PMI and MIP.

Both are forms of mortgage insurance, but they work very differently depending on the type of loan you choose. I'm here to translate this mortgage jargon into plain English. By the end of this guide, you'll know exactly which insurance applies to your financial situation and, most importantly, how to keep more money in your pocket.

Key Takeaways

- Loan Types: PMI applies exclusively to Conventional loans, while MIP is strictly required for government-backed FHA loans.

- Upfront Costs: MIP requires a hefty upfront fee paid at closing, whereas PMI typically only charges a monthly premium.

- Cancellation Rules: PMI automatically falls off once you reach 20% home equity. MIP usually lasts for the life of the loan, unless you put 10% or more down, in which case it generally falls off after 11 years.

What is PMI (Private Mortgage Insurance)?

Private Mortgage Insurance, or PMI, is a policy designed to protect your lender, not you, if you happen to default on your monthly payments. You will only encounter PMI if you take out a conventional loan and put down less than 20% of the home's purchase price.

Because private insurance companies provide this coverage rather than the federal government, the rates are heavily tied to your personal financial health.

Features of PMI:

- Monthly Payments: It's usually rolled directly into your regular monthly mortgage bill.

- Credit-Dependent: Excellent credit means much cheaper premiums. Poor credit makes it quite expensive.

- Cancellable: The best part about PMI is that it's temporary. Once you build up 20% equity in your property, you can request to drop it entirely.

What is MIP (Mortgage Insurance Premium)?

Mortgage Insurance Premium (MIP) is the Federal Housing Administration's (FHA) version of mortgage insurance. Just like PMI, it exists to protect the lender if you stop paying your mortgage. However, MIP is mandatory on all FHA loans, regardless of your credit score or the size of your down payment.

The FHA program is designed to help folks buy homes even with past credit bumps or low cash reserves. To make this possible, the government requires a standardized insurance structure.

Features of MIP:

- Two-Part Fee: You pay both an Upfront MIP (UFMIP) at closing and an Annual MIP divided into monthly chunks.

- Government-Backed: Since the FHA ensures the loan, the insurance rates are standard and don't heavily penalize lower credit scores.

- Stricter Cancellation: If you put less than 10% down on an FHA loan, MIP typically lasts for the life of the loan unless you refinance. If you put 10% or more down, MIP is usually removed after 11 years.

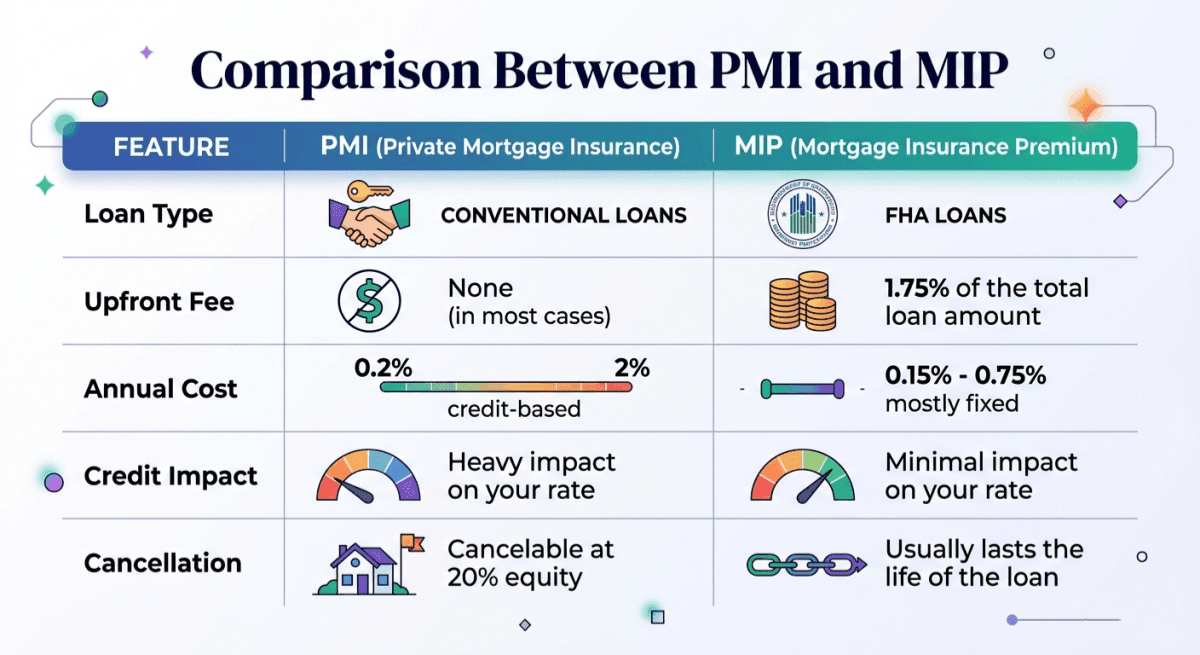

Comparison Between PMI and MIP

While PMI and MIP share the same goal of reducing lender risk, they differ dramatically in how they are structured, priced, and eventually removed. Let's break down the exact differences so you know what to expect when reviewing your loan estimates.

Loan Type

The easiest way to tell which insurance you'll pay is by looking at your mortgage. PMI is strictly tied to Conventional Loans. These are mortgages backed by private lenders and eventually sold to government-sponsored enterprises like Fannie Mae or Freddie Mac.

Because private entities assume the risk, they demand private insurance. MIP, on the other hand, is a legal requirement exclusively for FHA Loans. The Federal Housing Administration (under HUD) ensures these loans, meaning the government is on the hook if you stop paying. This fundamental difference dictates exactly which insurance policy you'll sign for.

Credit Score & Down Payment Impact

Here's where your unique financial profile really matters. PMI providers care deeply about your credit score and use a tiered pricing system. If your score is 760 or above, your PMI rate might be incredibly cheap. But if it's in the low 600s, PMI gets painfully expensive because private insurers view you as a higher risk.

MIP is a lot more forgiving. Because the federal government backs FHA loans, the MIP rates remain relatively standardized. Whether your credit score is a stellar 800 or a struggling 580, your MIP premium stays roughly the same, making FHA loans a lifeline for buyers with lower credit.

Upfront Cost

This is a major difference that often catches first-time buyers off guard. PMI generally has no upfront cost. You simply start paying the premium as part of your normal monthly mortgage bill. MIP, however, requires an Upfront Mortgage Insurance Premium (UFMIP).

In 2026, the upfront MIP rate is typically 1.75% of your base loan amount. You can pay this lump sum out of pocket at the closing table, but most buyers choose to roll it directly into their total mortgage balance. Just keep in mind that financing the fee means you'll also pay interest on that 1.75% for the next 30 years.

Cost

Your monthly budget will be directly impacted by these rates. For 2026, PMI rates often fall within the range of about 0.5%-1.5% of your total loan amount per year, depending on your credit score, down payment, and lender. If you borrow $300,000, that's anywhere from $1,500 to $4,500 annually, depending largely on your credit health and down payment size.

FHA annual MIP rates were recently reduced to make housing more affordable. Today, they hover between 0.15% and 0.75%. For many standard 30‑year FHA loans with a 3.5% down payment, you can expect an annual MIP rate in the range of about 0.50% to 0.55%, depending on your loan amount and LTV ratio. That's about $1,650 a year (or $137 a month) on a $300,000 loan.

Duration & Ability to Cancel

This is arguably the biggest long-term factor! Under the Homeowners Protection Act, lenders must automatically cancel your PMI once your loan balance reaches 78% of the home's original appraised value for certain conventional first‑mortgage loans that meet the statute's criteria.

You can even request early cancellation once you hit 20% equity. MIP is much stickier. If you put less than 10% down on an FHA loan (which most FHA buyers do), you will be locked into paying MIP for the entire life of the loan. It never falls off. If you manage to put down 10% or more upfront, the MIP will eventually drop off after 11 years of payments from the start of your loan, for FHA loans originated on or after June 3, 2013. Prior‑to‑2013 FHA loans have different cancellation rules.

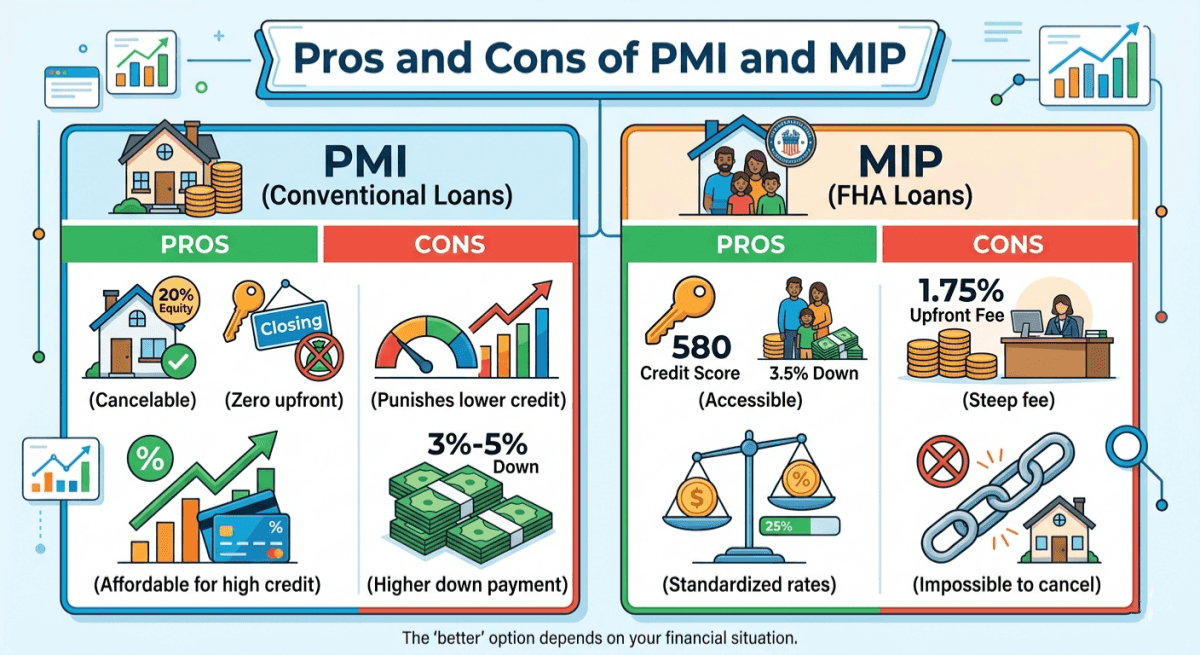

Pros and Cons of PMI and MIP

There is no absolute "better" option here. It strictly depends on what your finances look like right now. Here is a quick look at the advantages and drawbacks of each to help you weigh your options realistically.

PMI (Conventional Loans)

Pros:

- Easily cancelable once you hit 20% home equity.

- Zero upfront premium required at closing.

- Extremely affordable if you have a high credit score.

Cons:

- Punishes lower credit scores with very high monthly rates.

- Requires a slightly higher minimum down payment (usually 3% to 5%) than FHA.

MIP (FHA Loans)

Pros:

- Makes buying a home possible with a 580 credit score and just 3.5% down.

- Monthly rates are standardized and won't spike just because of a lower credit score.

Cons:

- Requires a steep 1.75% upfront fee.

- Usually impossible to cancel without refinancing the entire home.

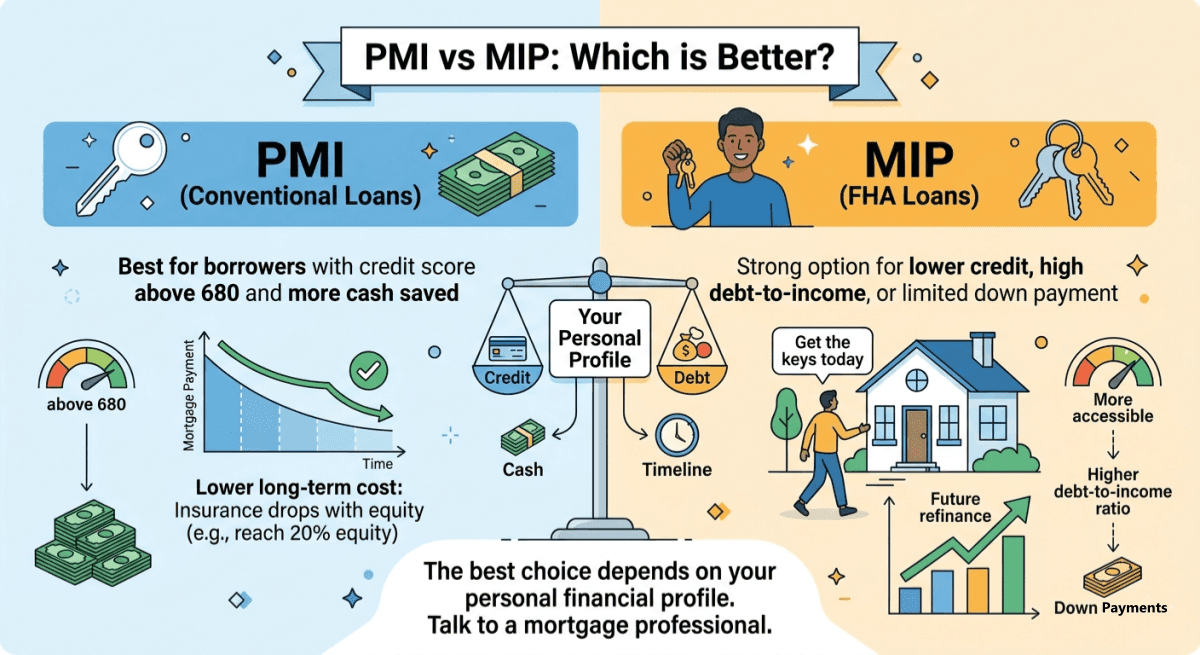

PMI vs MIP: Which is Better?

Choosing between the two comes down to your personal borrower profile. I always tell clients to lean toward PMI (a Conventional loan) if their credit score is above 680 and they have a bit of cash saved up. It's cheaper in the long run because you can eventually drop the insurance.

However, MIP (an FHA loan) can be a strong option if your credit took a recent hit, you have a high debt‑to‑income ratio, or you're struggling to scrape together a large down payment. It gives you the keys to a house today, and you can always build equity and refinance later.

FAQs About MIP vs PMI

Q1. What does MIP or PMI insurance cover?

A massive misconception is that this insurance protects the homeowner. It does not. Both PMI and MIP strictly protect your lender. If you lose your job and default on the mortgage, this insurance reimburses the bank for their financial loss.

Q2. How do I remove MIP?

If you put down less than 10%, your FHA MIP lasts for the life of the loan. The only realistic way to "remove" it is to wait until you have 20% equity, and then refinance your FHA loan into a Conventional loan without PMI.

Also Read: When Does PMI Go Away? 4 Key Ways Here to Know

Q3. Is PMI or MIP tax-deductible in 2026?

Yes! Thanks to recent legislation passed in 2025, PMI premiums are tax‑deductible starting in the 2026 tax year for eligible homeowners with an adjusted gross income under $100,000, as long as they itemize deductions.

Tax treatment for MIP may also change in 2026, but the final rules are still evolving. Be sure to consult your CPA for the latest guidance.

Q4. Can I switch from MIP to PMI?

Technically, no. You cannot just swap the insurance policy. However, you can refinance your current FHA loan into a Conventional loan. If you still have under 20% equity when you refinance, you will transition from paying FHA MIP to Conventional PMI.

Q5. How can I avoid PMI and MIP completely?

The most straightforward method is saving up a full 20% down payment for a conventional loan. Alternatively, if you are an eligible military veteran or active-duty service member, you can use a VA loan, which requires zero down payment and completely skips monthly mortgage insurance.

Conclusion

While nobody loves paying extra fees, PMI and MIP are powerful financial tools. Without them, most of us would have to wait decades to save a 20% down payment. They bridge the gap, allowing you to build wealth through homeownership years earlier than you otherwise could.

My best expert advice? Don't guess. When you're ready to buy, ask your mortgage Loan Officer to run the numbers for both a Conventional loan and an FHA loan side-by-side. Seeing the total costs compared over a five-year timeline will make your decision crystal clear.

People Also Read

- Must Read: Minimum Down Payment for House First-Time Buyer

- [Ultimate Guide] Where to Find a Loan Officer Near Me?

- What is the Lowest Mortgage Rate Today? Get Best Quote Today!

- [Must-Read Tips] How Do I Get the Lowest Mortgage Rates?

- Best First-Time Home Buyer Programs: Which One to Apply?

- Best PMI Calculators: Estimate Your Private Mortgage Insurance

- 2026 Guide: How to Calculate PMI on Your Mortgage