Mortgage Interest Rate vs. APR: What's the Difference?

When I bought my first house, the thick stack of loan documents felt like a foreign language. The biggest headache? Seeing two completely different percentages on my Loan Estimate: the interest rate and the APR. If you are comparing lenders right now, you are probably wondering why they do not match.

In this guide, I will break down exactly how these numbers differ, cutting through the confusing mortgage jargon. By the end, you will know exactly which metric to focus on to make the smartest financial decision for your future.

Key Takeaways

-

Your interest rate determines your actual monthly principal and interest payment.

-

Your APR (Annual Percentage Rate) reflects a broader, standardized measure of the loan's cost, including the interest rate and certain lender fees, but it does not capture every expense associated with the mortgage.

-

Because it includes additional fees, the APR is typically higher than the interest rate, although in some cases (such as lender credits), it may be similar to or even lower than the base rate.

-

Always use the interest rate to calculate cash flow, but look at the APR to compare overall affordability between lenders.

What is the Mortgage Interest Rate?

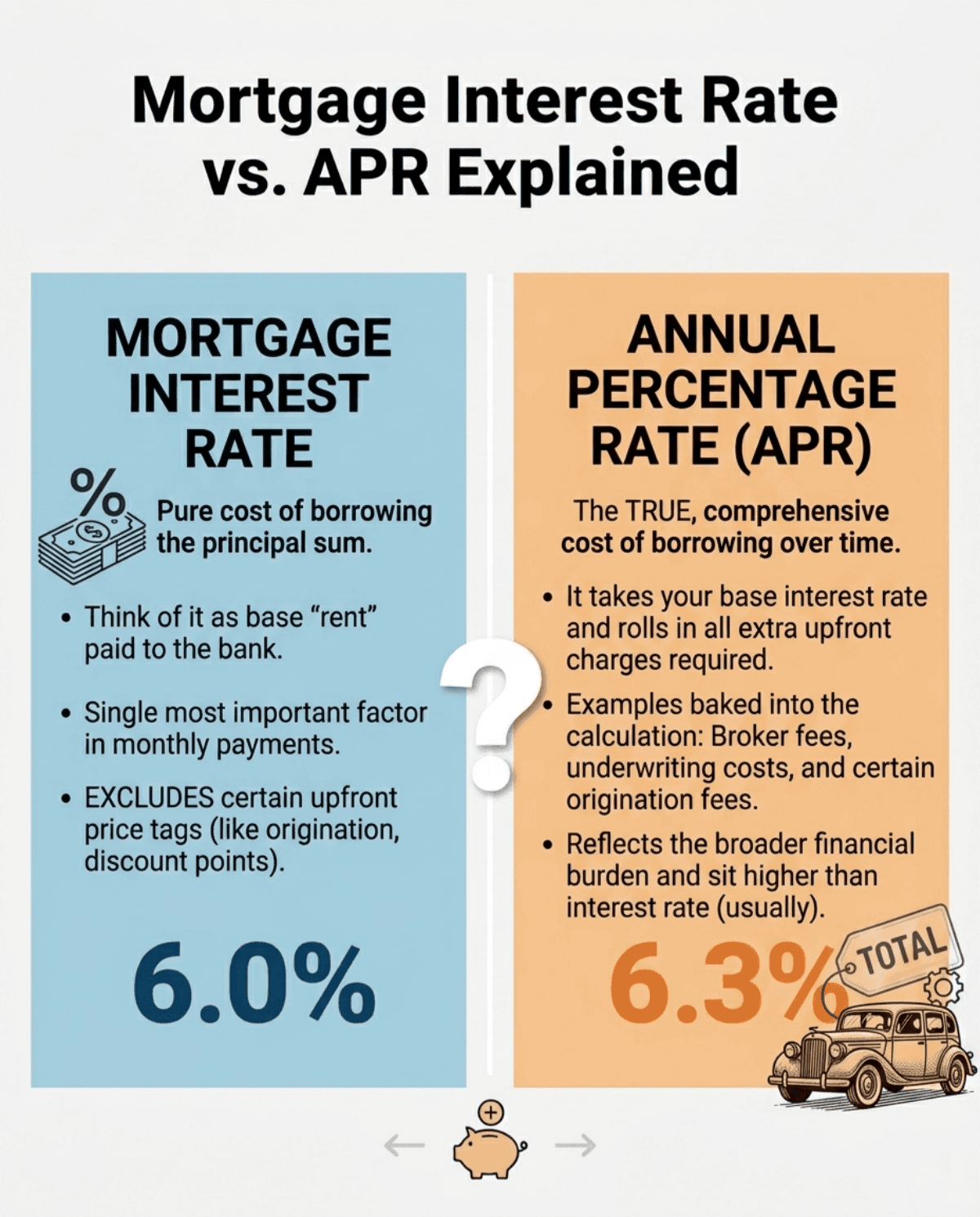

Think of your mortgage interest rate as the base "rent" you pay a bank for borrowing their money. It is a straightforward percentage applied directly to your principal loan balance.

This single number is incredibly important because it dictates exactly how much your monthly payment will be. For instance, when you hear real estate experts say the national average for a 30-year fixed loan in mid-2026 is hovering around 6.4%, this is the metric they mean.

However, what this baseline percentage excludes is the hidden price tag of securing that financing. It completely ignores out-of-pocket expenses like origination fees or discount points. So, while a low interest rate keeps your monthly bill manageable, it does not necessarily mean you scored the cheapest overall deal. It simply reflects the pure cost of the borrowed principal.

What is the Annual Percentage Rate (APR)?

If the previous metric is your baseline, the Annual Percentage Rate (APR) is your big-picture number. By law, lenders must provide this figure to show you the true, comprehensive cost of borrowing over time.

It takes your base interest rate and rolls in all the extra upfront charges required to get the mortgage. These extras typically include broker fees, discount points, underwriting costs, and certain origination fees. Because these expenses are baked into the calculation and spread out over the life of the loan, your APR will almost always sit higher than your interest rate.

I often tell new buyers that looking at the APR is like checking a car's price tag after the dealership adds destination and handling fees. It reflects the broader financial burden you are actually taking on, giving you a transparent view of your total debt.

APR vs. Interest Rate: What's The Difference?

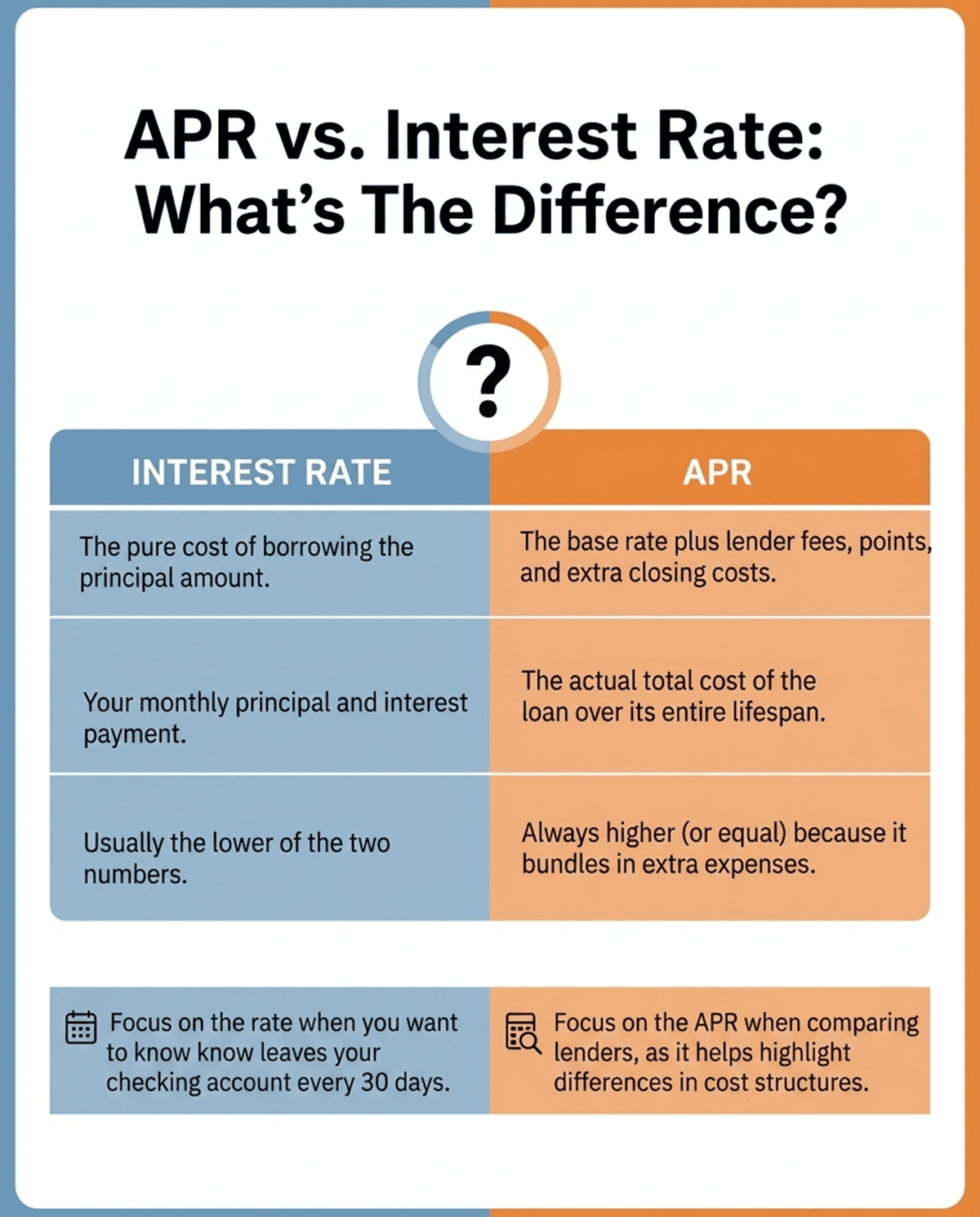

To put it simply, the interest rate dictates your month-to-month cash flow, while the APR provides a standardized annualized measure of borrowing cost, making it easier to compare loans, rather than representing the exact total amount you will pay over the life of the loan.

When I review loan estimates, I always separate the two mentally to understand what I am really paying. Here is a quick breakdown to help you visualize the contrast:

-

Focus on the rate when you want to know what leaves your checking account every 30 days.

-

Focus on the APR when comparing lenders, as it helps highlight differences in cost structures, though it does not by itself indicate whether a lender is overcharging.

Mortgage Interest Rate vs. APR Examples

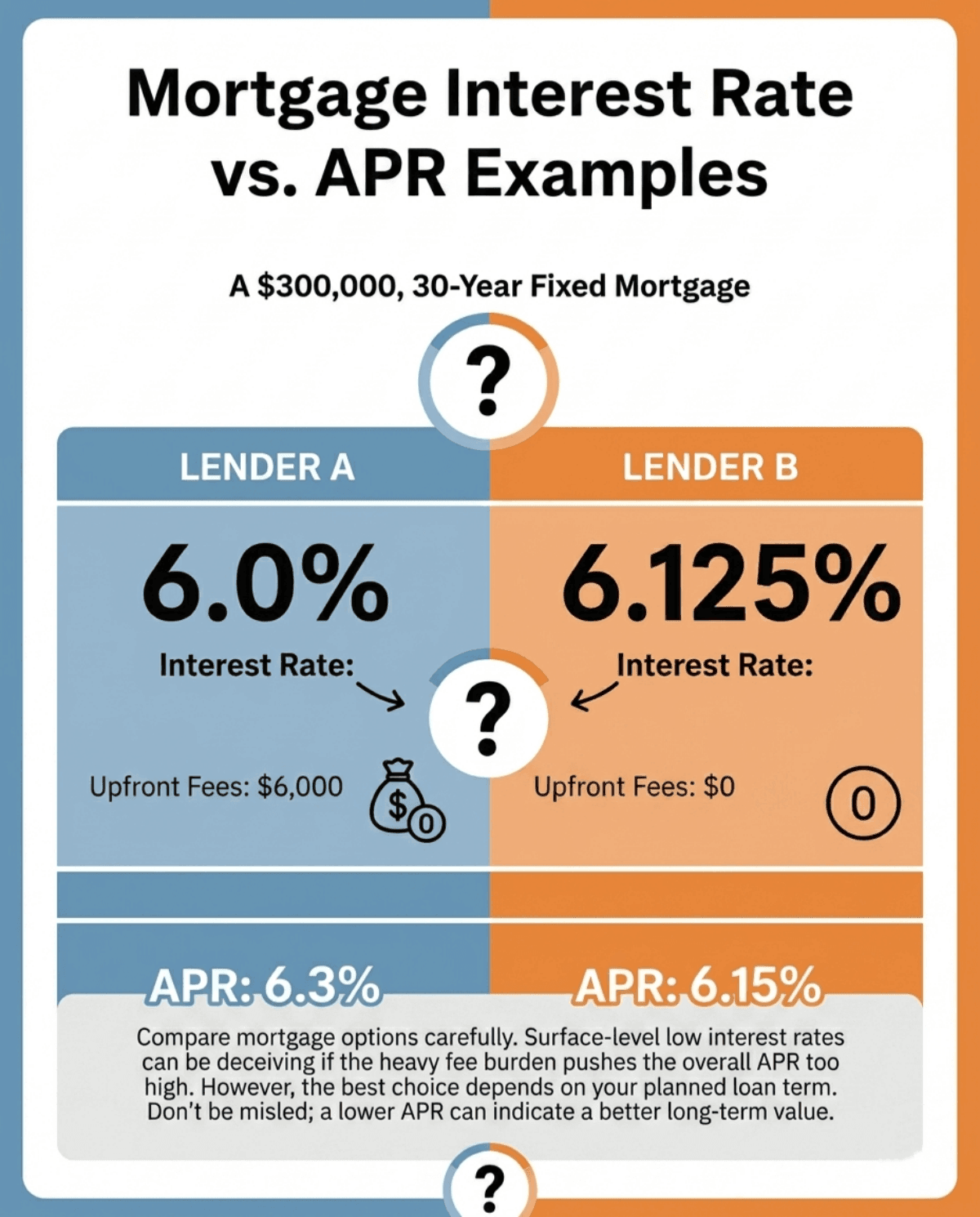

Let me share a realistic scenario to show why comparing these metrics matters. Imagine you need a $300,000, 30-year fixed mortgage in today's market.

-

Lender A offers you an incredibly tempting 6.0% interest rate. But to get it, they charge $6,000 in upfront origination fees and discount points. This heavy fee burden pushes your APR up to 6.3%.

-

Lender B offers a slightly higher interest rate of 6.125%, but they charge absolutely zero upfront origination fees. Because there are no hidden costs, their APR sits closely at 6.15%.

At first glance, Lender A looks better because of the lower 6.0% base number. Lender B's loan appears cheaper overall based on its lower APR, especially if you plan to keep the loan long-term. However, the better option can change depending on how long you hold the mortgage. Surface-level low rates can be deceiving if hidden charges are exorbitant.

When to Use APR or Interest Rate?

Knowing the difference is great, but how do you actually use this information? Honestly, there isn't a single "winner" here. It all depends on how long you plan to stay in the house.

-

When to focus on the Interest Rate: Look closely at this number if your main goal is controlling your monthly cash flow. It's also the most critical metric if you plan to sell or refinance within three to five years. Since you won't live there long enough to recoup high upfront fees, keeping your monthly payment low is the priority.

-

When to focus on the APR: Rely on this percentage when you want an apples-to-apples comparison across multiple banks, assuming you intend to hold the property long-term. It brilliantly exposes lenders who advertise rock-bottom rates but secretly inflate their closing costs to make up the difference.

FAQs About Mortgage Interest Rate vs APR

Q1. How to get a lower interest rate?

To secure a better percentage, start by aggressively improving your credit score and lowering your debt-to-income ratio. Lenders reserve their best offers for low-risk borrowers. Additionally, you can bring a larger down payment to the table or choose to pay upfront "discount points" to artificially buy down your rate.

Also Read:

Q2. Can I lower my APR?

Yes, absolutely. Since the APR is heavily influenced by lender fees, you can lower it by shopping around and negotiating those specific closing costs. Ask lenders to waive their application or origination fees. Alternatively, you can opt for a "no-fee" mortgage where fewer extra costs are rolled into your total balance.

Q3. Why is my APR higher than my interest rate?

Your APR is higher because it calculates your base interest rate plus the extra closing costs you pay at the start of the loan. When you bundle broker fees and discount points into the math, the overall percentage naturally increases.

Q4. What is a good APR?

There is no single magic number, as the economy shifts constantly. A "good" APR depends entirely on current macroeconomic trends, your personal credit profile, and the loan term length. Instead of chasing an arbitrary target, compare your offers against the current national average APR for your specific loan type to ensure fairness.

Q5. What is a good interest rate?

Similar to the APR, a competitive rate fluctuates daily. For example, a 6.4% rate on a 30-year fixed loan might be normal in 2026, but high compared to historical lows. A genuinely good interest rate is simply the lowest percentage you can personally qualify for right now without paying exorbitant, unnecessary fees.

Q6. Do I use APR or interest rate to calculate a mortgage?

You should always use the interest rate to calculate your monthly mortgage payment. The APR is not used to directly calculate your monthly payment. That is based on the interest rate and loan terms, although the APR is derived from those same components.

Conclusion: Should I Go by APR or Interest Rate?

Ultimately, you shouldn't strictly choose one metric over the other. Both numbers tell a crucial part of your financial story. I personally rely on the interest rate to ask myself, "Can I comfortably afford this monthly bill?" while I use the APR to answer, "Am I actually getting a fair overall deal from this bank?"

My biggest piece of advice is to never settle for the first offer. Apply with at least three different lenders, request their official Loan Estimates, and compare both percentages side-by-side. It takes a little extra effort, but doing the math could save you thousands of dollars over the life of your mortgage.

Chat with Local LOs and Compare Quotes Now.

Disclaimer: This article is for informational purposes only and is based on personal experience and current market research. Please consult a licensed financial advisor or mortgage broker for personalized advice regarding your specific situation.