Top-Rated Software for Mortgage Underwriting: Close Loan Quicker

The mortgage industry is moving faster than ever, yet the underwriting process often feels stuck in the past. In my years of working with loan files, I've seen how manual guideline research and "stare-and-compare" data entry can kill a deal's momentum. We've all been there, spending hours digging through 500-page handbooks just to find one nuance for a self-employed borrower.

Today, high-speed software isn't just a luxury. It's the only way to stay profitable. In this guide, I'll share the best mortgage underwriting tools for 2026 that actually help us clear conditions and close loans in record time.

People Also Read

- Top Loan Origination Systems to Streamline Workflow

- Best Loan Origination Software for Mortgage [Never Miss]

- Best Mortgage CRM for Brokers, Lenders, MLOs

What Features to Consider In Advance?

Before you commit to a new platform, I recommend looking beyond just the price tag. From my experience, the real value lies in Source Transparency. If an AI tool gives you an answer but can't show you exactly where it found that rule in the FHA or Jumbo handbook, it's a liability, not a help.

Second, check for SOC 2 Type II compliance. We are handling sensitive borrower data. Enterprise-grade security is non-negotiable. Third, look for LOS/POS Integration. You shouldn't have to jump between five tabs to calculate a DTI ratio. Lastly, prioritize tools that handle Non-QM and complex scenarios. While Fannie and Freddie have their own engines, the real "bottleneck" usually happens with non-traditional loans where manual work typically spikes.

7 Best Software for Mortgage Underwriting in 2026

The landscape has shifted. We now have a mix of "Legacy Giants" that set the rules and "AI Agents" that help us navigate them. Here are my top picks.

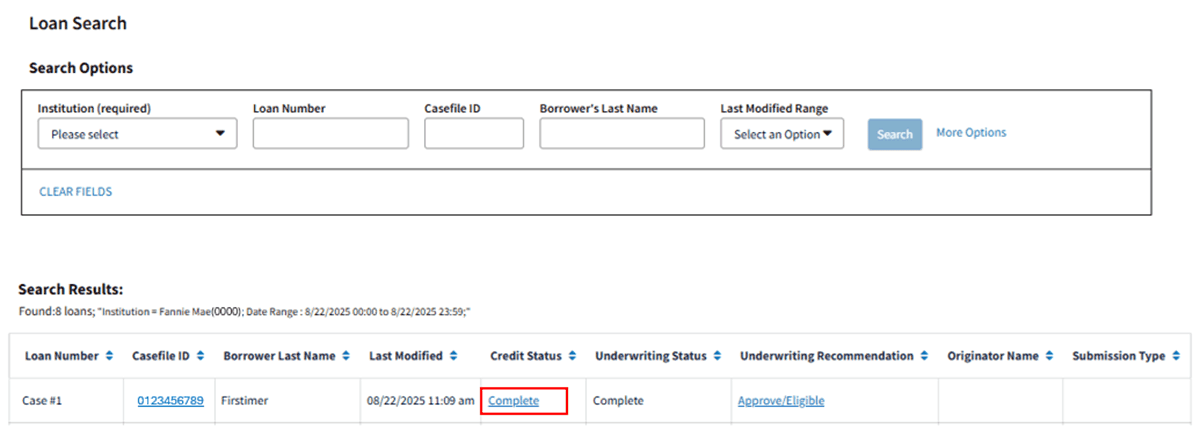

Fannie Mae Desktop Underwriter® (DU®)

Verdict: The essential industry standard for any conventional loan professional.

I can't talk about underwriting without starting here. DU is the backbone of the industry. It's the primary tool I use to see if a loan meets Fannie Mae's eligibility requirements. In 2026, DU has become even more automated, focusing heavily on "Day 1 Certainty" by pulling asset and income data directly from source vendors. It's reliable because it is the rulebook. However, it's strictly for conventional products, so don't expect it to help you with a complex DSCR or bank statement loan.

Pros:

- The "gold standard" for GSE compliance and salability.

- Seamless integration with almost every LOS on the market.

- Continuous updates to reflect the latest market policies.

- Reduces the need for physical documentation through automated validation.

Cons:

- Strictly limited to Fannie Mae-compliant products.

- Can feel like a "black box" when a loan is referred for manual underwriting.

- Requires clean, structured data to function correctly.

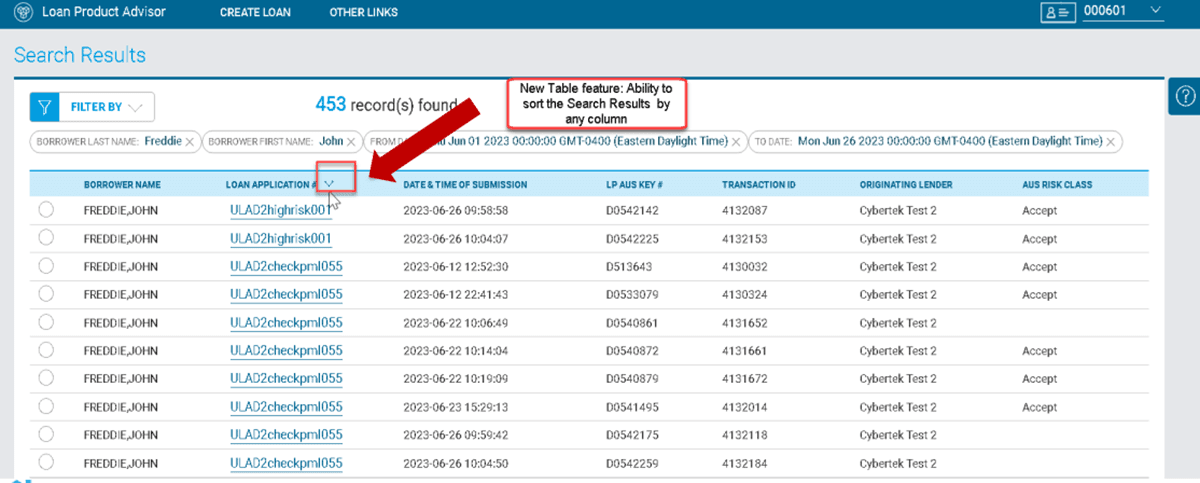

Freddie Mac Loan Product Advisor® (LPA®)

Verdict: The best alternative to DU, offering unique flexibilities for specific borrower profiles.

While DU is more famous, I often find that LPA (formerly LP) can be a lifesaver for certain borrowers. It operates similarly but uses Freddie Mac's specific logic. I've noticed that sometimes a file that struggles in DU might get a cleaner "Accept" in LPA due to slight differences in how they view credit depth or reserves. It's an absolute must-have in your toolkit to ensure you aren't leaving any options off the table for your clients.

Pros:

- Excellent for First-Time Homebuyer programs and HFA loans.

- Provides clear, actionable feedback messages for clearing conditions.

- Strong automation for asset and income verification.

- Often more forgiving on specific "borderline" credit scenarios.

Cons:

- Like DU, it is restricted to Freddie Mac products.

- Interface can feel a bit dated compared to modern AI tools.

- Validation errors can sometimes be cryptic to troubleshoot.

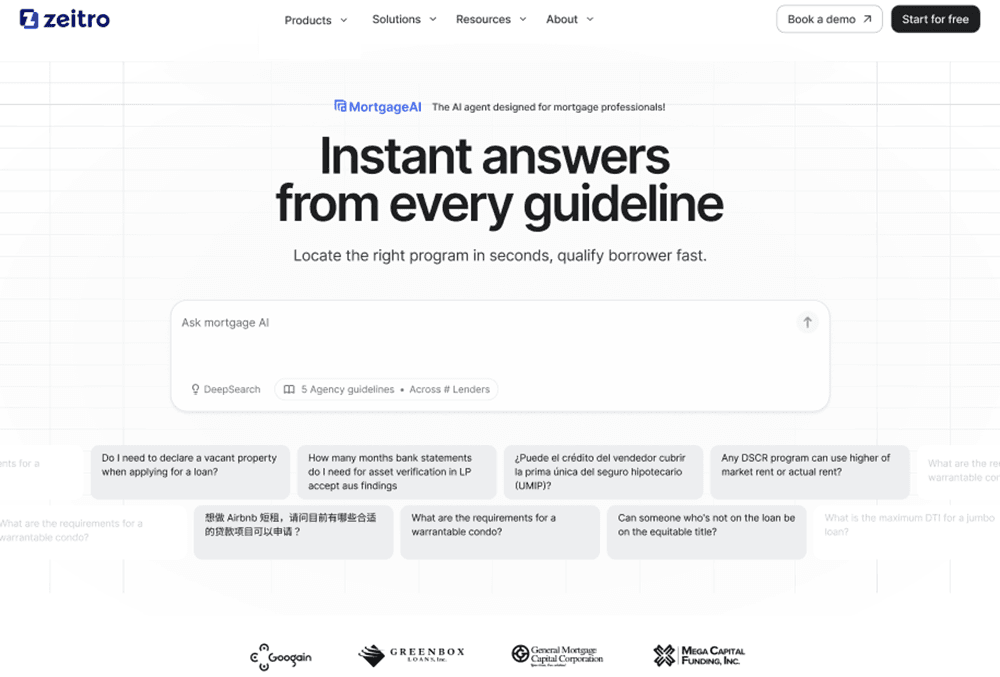

Zeitro Mortgage AI

Verdict: The most powerful AI Agent for rapid guideline verification and complex Non-QM deals.

I've been following Zeitro since they started in 2020, and they've truly changed the game for those of us handling tricky files. It's an "AI-Native" platform built by former Google and Apple engineers, which explains why the interface feels so intuitive. Their Zeitro Strata AI is a lifesaver. It acts as a guideline assistant where you can ask specific questions (even "fuzzy" ones) and get an answer with direct citations in seconds. It's especially strong for Non-QM, saving me hours of manual research.

Also Read: Zeitro Strata Review: World's No.1 Best Mortgage Guidelines Checker

Pros:

- Saves an average of 7+ hours per loan file by automating guideline research.

- Provides 100% source transparency, so you can trust the AI's answers.

- Includes a built-in Pricing Engine for both Conventional and Non-QM products.

- Offers a Digital 1003 (POS) that achieves a 90%+ completion rate.

- SOC 2 Type II certified, ensuring enterprise-grade data security.

Cons:

- Strata AI is so popular it often has a waitlist for new enterprise seats.

- The "GrowthHub" feature is great for LOs but might be extra noise for a pure Underwriter.

- Requires a mindset shift from "searching" to "chatting" with an AI agent.

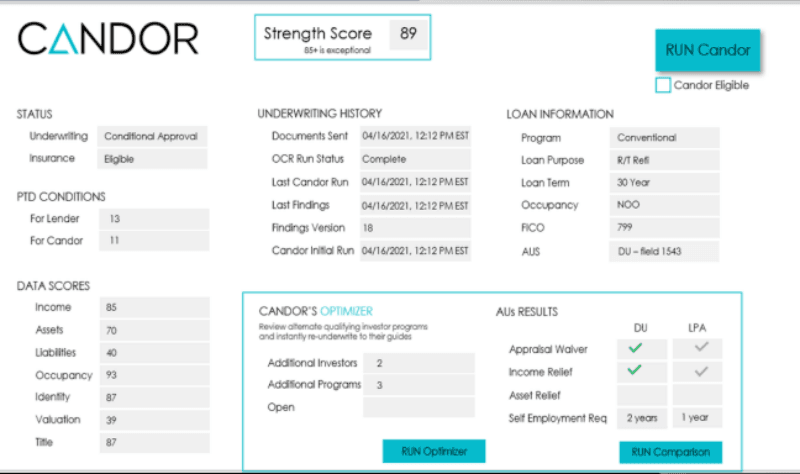

CANDOR Technology

Verdict: Best for lenders looking to automate the actual "logic" of an underwriting decision.

CANDOR doesn't just check boxes; it performs 'Cognitive Underwrite' with automated loan decision logic. I like it because it simulates the critical thinking of a human underwriter. It looks at the data, identifies cross-checks, and clears conditions autonomously. If you're a high-volume lender, this is how you scale without hiring an army of staff. It's less about "searching guidelines" and more about "making the decision" for you.

Pros:

- Significantly reduces the "touches" per loan file.

- Handles complex income calculations with high precision.

- Provides a "Cognitive Underwrite" that is backed by a warrant.

- Decreases the cost to produce a loan by automating repetitive tasks.

Cons:

- Can be a heavy lift to integrate into older legacy systems.

- Might feel "too automated" for underwriters who prefer manual control.

- Pricing is geared toward larger lending institutions.

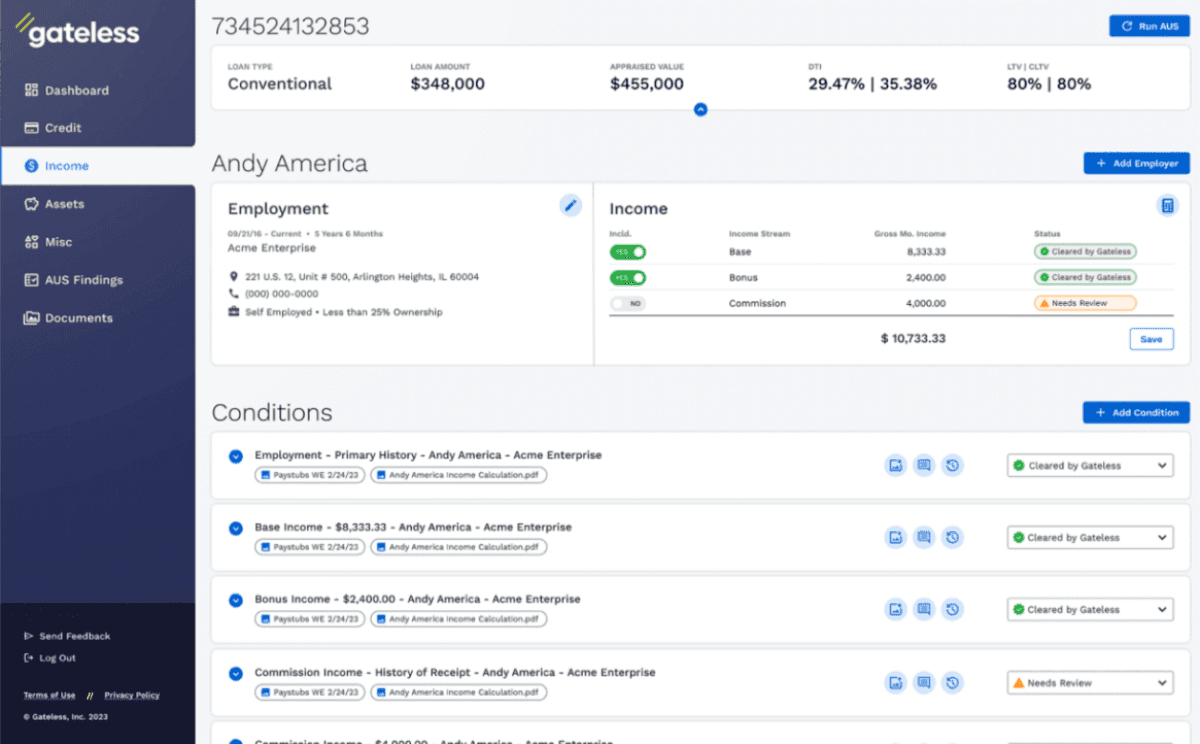

Gateless Smart Underwrite

Verdict: Best for eliminating "stare-and-compare" data entry through real-time automation.

Gateless (now part of the ICE Mortgage Technology ecosystem) focuses on clearing conditions as soon as the data hits the system. I've seen it work in real-time, as soon as a borrower uploads a document, Gateless checks it against the guidelines. It's fantastic for reducing the back-and-forth between the LO and the Underwriter. It's all about getting to that "Clear to Close" faster by identifying issues the moment they arise.

Pros:

- Integrates deeply with Encompass, the industry's leading LOS.

- Identifies data discrepancies instantly, preventing late-stage surprises.

- Speeds up the "Review" phase by pre-clearing standard conditions.

- Reduces human bias in the decision-making process.

Cons:

- Most effective when paired with other ICE products.

- Initial setup and mapping of conditions can be time-consuming.

- May be overkill for very small broker shops.

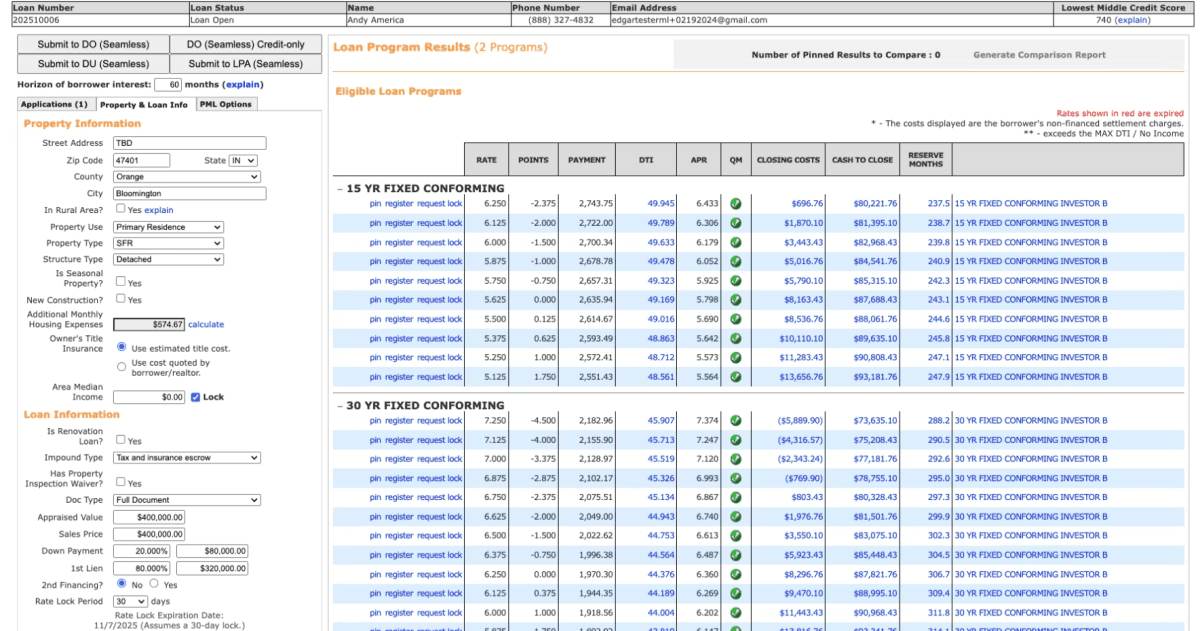

MeridianLink PriceMyLoan (PML)

Verdict: A top-tier choice for combining a pricing engine with automated underwriting.

I've used MeridianLink's PML when I need to know exactly how a specific scenario impacts both eligibility and price at the same time. It's a Product and Pricing Engine (PPE) that has underwriting "brains" built-in. It's great for the front-end, allowing LOs to run a scenario and get an instant "yes/no" based on investor overlays. It keeps the "garbage" out of the underwriter's queue by catching ineligible files early.

Pros:

- Handles complex investor overlays that DU/LPA might miss.

- Instant feedback on how a credit score change affects the rate.

- Very user-friendly for Loan Officers and Brokers.

- Excellent support for private and niche mortgage programs.

Cons:

- Not as "AI-forward" as newer tools like Zeitro.

- Guideline data is updated manually by the team, rather than via live AI crawling.

- The interface feels a bit more "tabular" and traditional.

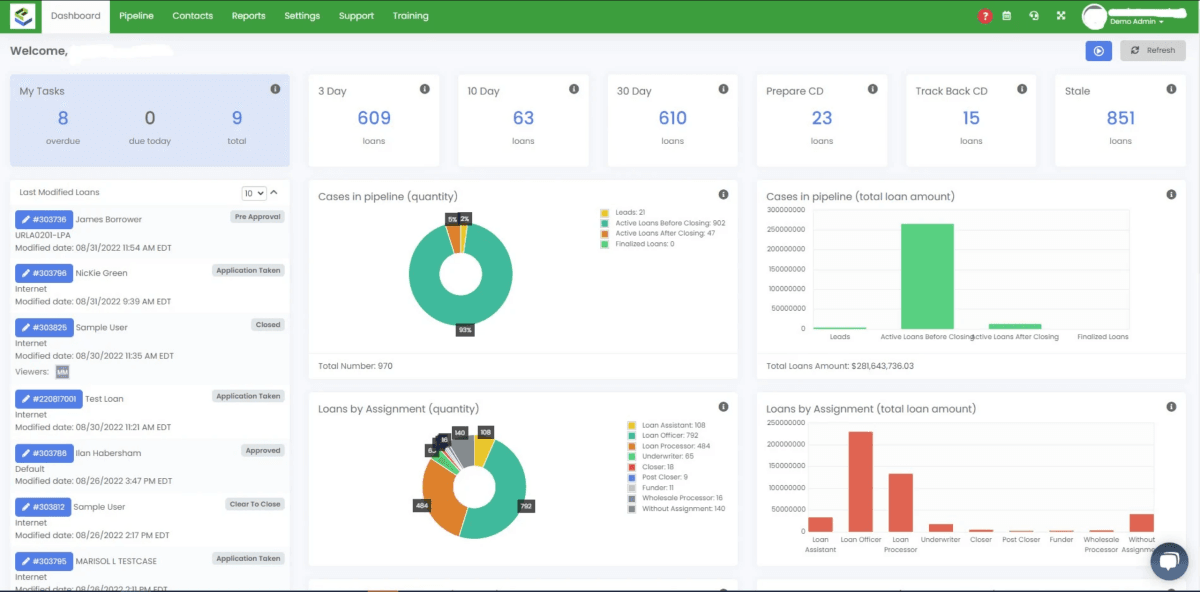

LendingPad

Verdict: Best all-in-one LOS for small-to-medium brokers who want a built-in underwriting flow.

LendingPad isn't just underwriting software. It's a full Loan Origination System (LOS), but I include it because its underwriting module is so streamlined. Being cloud-native, it's fast. I've noticed that for brokers who don't want to pay for five different subscriptions, LendingPad offers a very clean way to track conditions, run DU/LPA, and manage the file all in one screen.

Pros:

- One of the most affordable and fastest LOS options available.

- Real-time collaboration. Multiple people can be in the file at once.

- Highly intuitive condition management tracking.

- Great customer support and frequent feature updates.

Cons:

- Underwriting logic is less "automated" than CANDOR or Zeitro.

- Reporting features could be more robust for large enterprises.

- Doesn't have a native "AI Guideline Assistant."

Which Mortgage Underwriting Software to Choose?

Choosing the right tool depends on your specific role and volume. If you are a high-volume broker, you need a mix of standard compliance and modern speed. Here is how I'd break it down:

- Zeitro: Best for those who want a dedicated AI Agent to handle Non-QM guidelines and save hours of research.

- Fannie Mae DU / Freddie Mac LPA: The non-negotiable foundation for all conventional lending.

- CANDOR: Best for large lenders who want to automate the decision-making logic itself.

- LendingPad: Best for independent brokers who need a fast, cloud-based all-in-one platform.

- Gateless: Best for Encompass users looking to eliminate manual document reviews.

FAQs About Mortgage Underwriting Software

Q1. What is mortgage CRM software?

CRM (Customer Relationship Management) software like Jungo or Total Expert is for the "front end" of the business. It's used for marketing, lead generation, and keeping in touch with clients. Underwriting software, on the other hand, is for the "back end", it's used to verify data, calculate risk, and ensure the loan meets investor guidelines.

Q2. Which AI tool is used by Better Mortgage for underwriters?

Better Mortgage uses their proprietary in-house platform called Tinman. It allows them to automate large portions of the underwriting process, which is why they can often offer faster closing times than traditional retail banks.

Q3. Can AI software fully replace human mortgage underwriters?

In my opinion, no. AI acts as a "co-pilot." It can calculate income and check guidelines 10x faster than I can, but a human underwriter is still needed to handle "gray area" scenarios, detect fraud, and make the final common-sense call on a file.

Q4. Is my borrower data safe with AI agents like Zeitro?

Yes, provided you choose tools with the right certifications. Look for SOC 2 Type II certification. This means the company has undergone rigorous independent audits to ensure they handle data with the same level of security as a major bank.

Q5. What is the ROI of implementing underwriting automation?

Most lenders see a return within the first few months. By reducing "turnaround time" (TAT) by 2-5 days and saving 7+ hours of manual labor per file, you can close more loans with the same staff, significantly lowering your "cost to originate."

Conclusion

The "old way" of underwriting, scrolling through PDFs and manually calculating DTIs, is becoming a competitive liability. In 2026, the winners in the mortgage space are those who leverage technology to work smarter. I personally believe that a combination of the GSE standards (DU/LPA) and an AI-native agent like Zeitro provides the best balance of safety and speed.

By automating the "drudge work" of guideline research and data entry, you can focus on what actually matters: building relationships and closing more loans. Don't wait for the market to force your hand, and embrace these tools now to stay ahead of the curve.