All Differences Between Mortgage Underwriter vs Loan Officer

When I first entered the mortgage world, I realized how confusing the home-buying process is for everyday borrowers. Many clients come to me thinking that the person who helps them apply for a loan is also the one who decides whether they get the house.

But that is not how it works. In reality, you are dealing with two entirely different professionals: the Loan Officer and the Mortgage Underwriter. While both are essential to getting you the keys to your new home, they play completely different roles. I want to clear up this confusion so you know exactly who does what and how to navigate your mortgage journey smoothly.

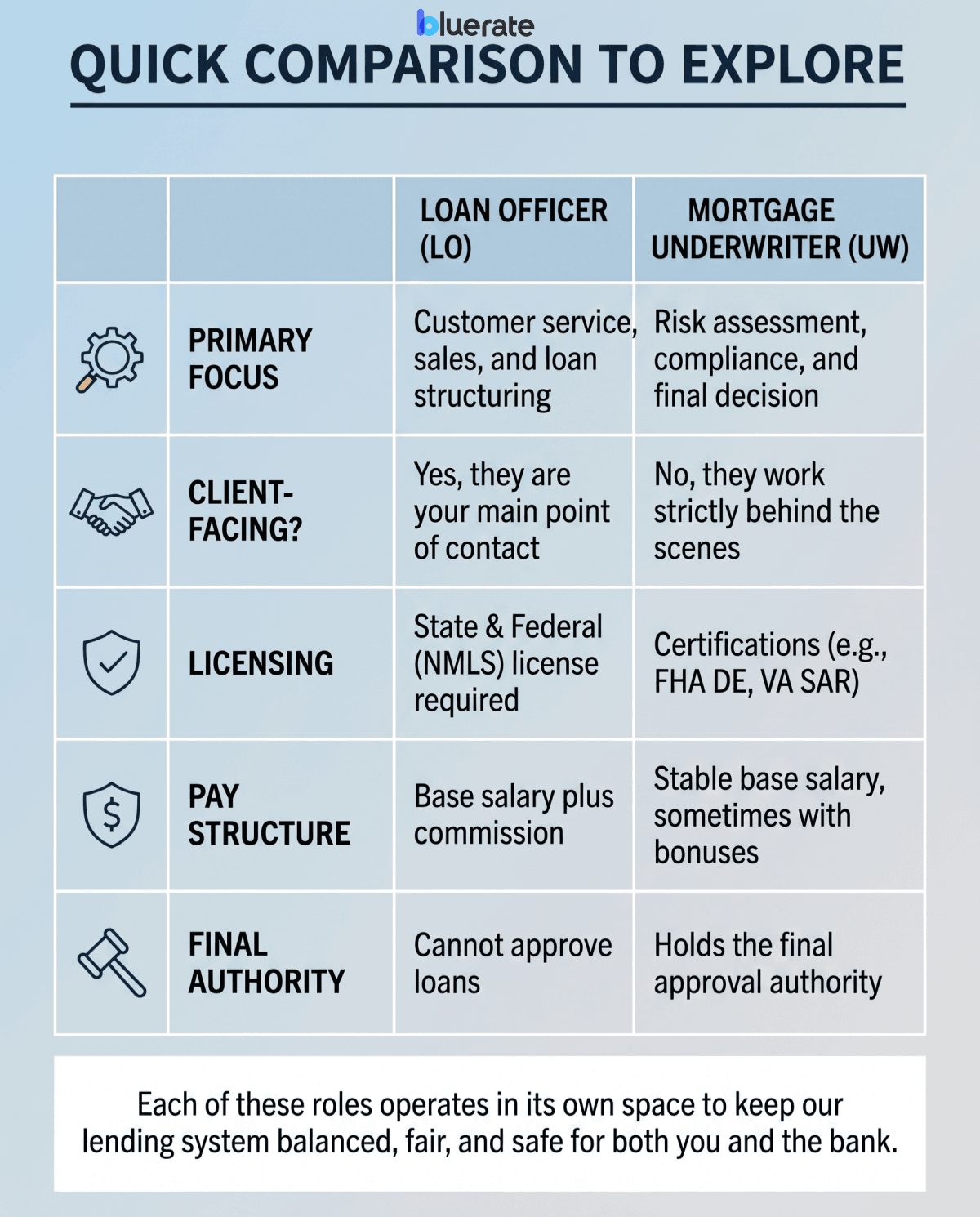

Quick Comparison to Explore

To help you understand the big picture quickly, I put together a direct comparison of these two roles. In my day-to-day work, I find that visualizing their differences side-by-side helps clients understand why they are asked for so much paperwork, and who is actually reviewing it.

Each of these roles operates in its own space to keep the lending system balanced, fair, and safe for both you and the bank.

Each of these roles operates in its own space to keep the lending system balanced, fair, and safe for both you and the bank.

Learn Differences Between a Loan Officer and an Underwriter

Let's dive a bit deeper into the mechanics of both positions. Having worked alongside both sides of the aisle, I can tell you that understanding these seven core areas will completely change how you view your loan application process.

Responsibilities

As a Loan Officer, my primary job is to be your advisor and advocate. I help you choose the right mortgage program, calculate your budget, and gather your initial documents. I am essentially the bridge between you and the lender.

On the other side of the firewall sits the Underwriter. Their responsibility is purely analytical. They do not look at you as a friendly face. They look at your numbers. They verify your income, evaluate your credit history, check your debt-to-income ratio, and analyze the property appraisal. Their job is to protect the bank by making sure you meet every single guideline of the loan program and are highly likely to pay back the debt. We need both: one to guide you in, and one to make sure the math actually works.

Licensing & Qualifications

The legal requirements for these jobs are very different. Loan Officers must be licensed under the Nationwide Multistate Licensing System (NMLS). I had to pass a strict federal exam (the SAFE Act test), go through background checks, and complete continuing education every year to keep my license active.

Underwriters generally do not need an NMLS license unless they work as independent contract underwriters. Instead, their credentials are focus-specific. To approve certain government loans, they must earn specialized designations. For example, to sign off on an FHA loan, they need a Direct Endorsement (DE) certification. For VA loans, appraisal reviews are conducted by a Staff Appraisal Reviewer (SAR), which is a separate role from the underwriter. This means their qualifications are deeply rooted in risk management rather than sales law.

Salary

How these professionals get paid greatly influences their daily work. According to the U.S. Bureau of Labor Statistics (BLS) May 2024 data, the median annual wage for loan officers was $74,180. However, I must point out that most Loan Officers work on a commission-heavy structure. In a booming housing market, a top-producing LO can make several hundred thousand dollars, but their income can drop significantly when rates rise.

Underwriters, categorized closely with credit analysts by the BLS, earned a median annual wage of $79,420 in May 2024. Underwriters usually earn a steady salary. They do not have to worry about commission, which ensures their decisions remain objective and are not influenced by a need to close transactions just to get paid.

Workflow

The workflow of a mortgage follows a strict assembly line, and these two professionals handle different shifts. I always tell my clients that a mortgage is a relay race.

First, the Loan Officer takes the baton. I help you fill out the application, run your initial credit, and package your file. Once everything looks complete, the loan is passed to a processor, who then hands it over to the Underwriter.

The Underwriter steps in during the middle and final phases of the loan. They review the file, issue a conditional approval, and list any extra items they need to see. Once those conditions are met, the Underwriter issues the final "Clear to Close." The Loan Officer does not make credit decisions but remains actively involved by coordinating documents, clarifications, and communication throughout the underwriting process.

Interaction

In my experience, the biggest operational difference is who they talk to. As a Loan Officer, I am consumer-facing. I spend my days on the phone with you, your real estate agent, and the title company to keep everyone updated.

Underwriters, however, operate in the background. Underwriters typically do not communicate directly with borrowers, as most lenders prefer communication to go through the loan officer or processor. In fact, most banks actively prevent underwriters from speaking to clients to protect their decision-making from personal bias or outside pressure. If an underwriter needs more information, they will ask the loan processor or the loan officer to request it from you.

Authority

There is a clear hierarchy of authority in the lending process. Loan Officers have zero authority to approve or deny your mortgage. When I issue a pre-qualification letter, it is simply my professional opinion based on the basic details you provided. I am saying, "This looks good on paper."

The Underwriter plays a primary role in loan approval decisions (subject to lender policies and systems). They are the only ones who can officially approve your mortgage, suspend it for further review, or deny the application entirely. Their decision represents the lender's formal credit determination, subject to internal policies and potential review. If an underwriter finds an issue with your tax returns or bank statements, their ruling stands, regardless of how much your Loan Officer wants to push the loan through.

Career Path

The career paths for these roles attract different types of personalities. Loan Officers usually start as assistants (LOAs) or junior originators. Because it is a sales-driven role, career growth is measured by production volume. Successful LOs often progress to managing branches or even starting their own mortgage brokerage firms.

Underwriters usually start as loan processors or junior credit analysts. They progress to senior underwriting roles, specialize in complex products like jumbo or government loans, and eventually move into risk management. A senior underwriter might become a risk manager, underwriting director, or even a chief risk officer. It is a highly stable, analytical path focused on technical mastery rather than sales and networking.

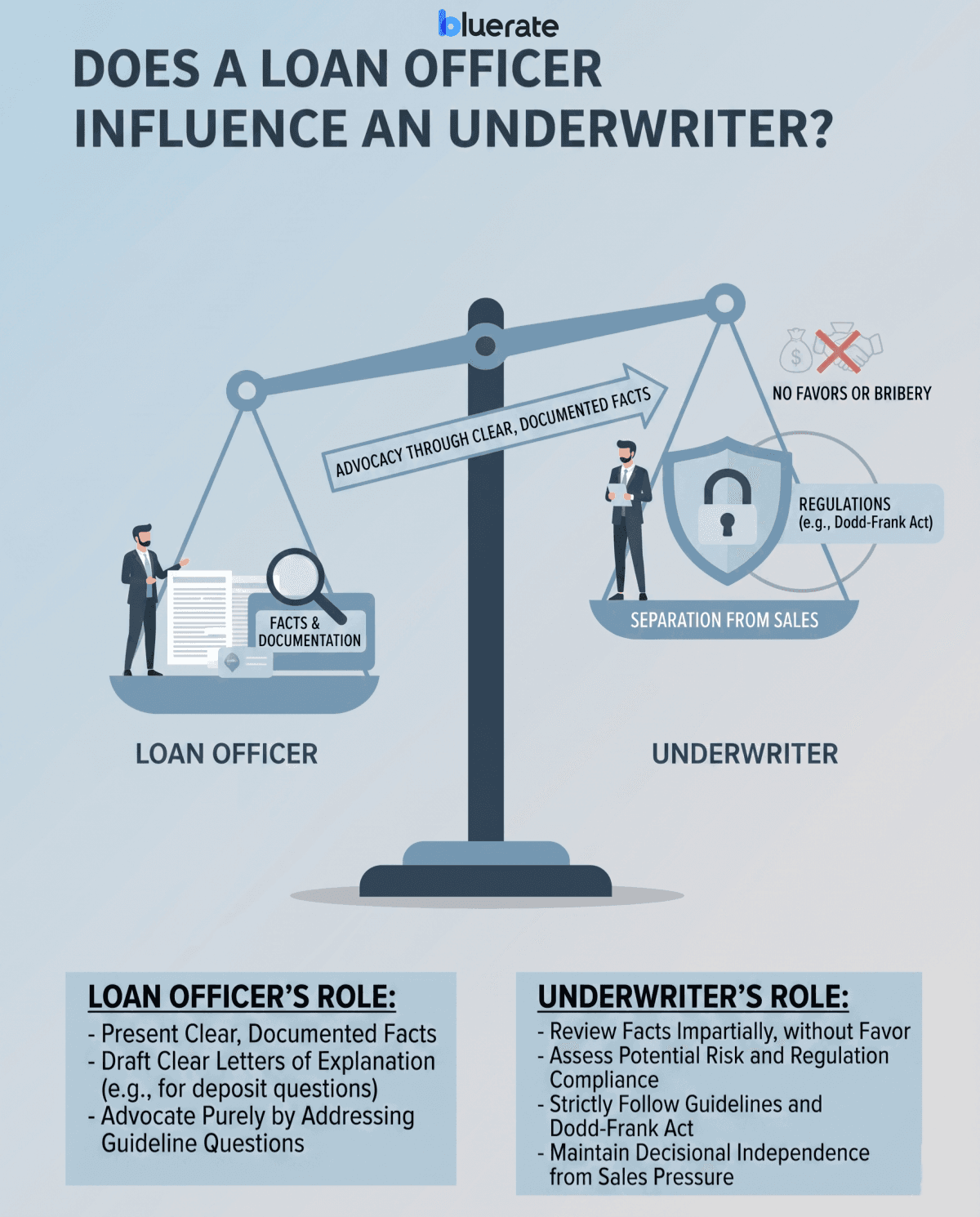

Does a Loan Officer Influence an Underwriter?

A common question I get is whether a Loan Officer can persuade an underwriter to approve a shaky loan. The short answer is: only through facts, not favors. Regulations such as the Dodd-Frank Act restrict improper influence and compensation structures, and most lenders maintain a separation between sales and underwriting to ensure compliance.

I cannot bribe or pressure an underwriter to overlook a low credit score or unstable income. However, I can advocate for you. If an underwriter questions a deposit, I can work with you to draft a clear Letter of Explanation. The influence is strictly limited to presenting clear, documented facts to satisfy underwriting guidelines.

FAQs About Mortgage Underwriter vs Loan Officer

Q1. Is a loan officer the same as an underwriter?

No, they are entirely different. A loan officer is your personal guide and salesperson who helps you apply for a mortgage and acts as your point of contact. A mortgage underwriter works behind the scenes for the lender to evaluate the risk of lending you money, verifying all your financial data to make the final approval decision. Think of the loan officer as the tour guide who shows you the ship, and the underwriter as the captain who decides if the ship is structurally safe to sail.

Q2. Who makes more, an underwriter or a loan officer?

It depends on the market. Underwriters earn a stable, higher base salary, with a median of $79,420 according to the BLS. Loan officers have a lower base but can earn substantial commission. In a strong housing market with low interest rates, a high-performing loan officer can easily make well over $150,000, outearning most underwriters. However, during market downturns, underwriters enjoy far greater financial stability because their income is not tied to how many loans they close. Both paths offer strong earning potential depending on your risk tolerance.

Q3. Can a loan officer override an underwriter's decision?

Absolutely not. A loan officer has no authority to reverse an underwriter's denial or bypass any loan conditions. If an underwriter denies your loan or requests a specific document, that decision is final. The only way to move forward is to satisfy the underwriter's conditions. If I, as a loan officer, believe the underwriter made an error in interpreting a guideline, my only option is to formally appeal the case to the underwriting manager with clear documentation. We can never simply hit "approve" ourselves.

Q4. Who has the final say on my mortgage application?

The mortgage underwriter has the ultimate, final say. While a loan officer can tell you that you look like a great candidate, only the underwriter can issue the actual commitment to lend. The process is not complete until the underwriter thoroughly reviews every pay stub, bank statement, and tax return, signs off on the appraisal, and changes your status to "Clear to Close" (CTC). Until that formal sign-off is issued, your mortgage application is technically still pending approval.

Q5. Can I talk to the underwriter directly if my loan is delayed?

In almost all cases, you cannot. Lenders deliberately keep underwriters insulated from borrowers to prevent any bias, emotional appeals, or undue pressure. If your loan is delayed, your loan officer or loan processor is your designated communicator. They will get the specific feedback from the underwriter, explain exactly what document or clarification is missing, and help you resolve the issue. If you have questions about a delay, always contact your loan officer first; we are there to handle the stress for you.

Conclusion

Navigating the home loan process is a major milestone, and understanding who is handling your paperwork can make the experience much less stressful. In my years of helping clients, I have seen how a smooth approval relies on both of these roles working in tandem. While they sit on opposite sides of the lender's desk, both are essential to getting you to the closing table safely.

To summarize their differences:

-

Loan Officer: Your direct advocate who guides you through loan programs, helps structure your application, and manages your file.

-

Mortgage Underwriter: The behind-the-scenes risk expert who verifies your documents, enforces lending guidelines, and has the final approval authority.

Understanding this division of labor makes it easier to navigate the mortgage pipeline with confidence.