Mortgage Underwriter: Role, Responsibilities, and Tips

Are you searching for a stable, high-paying career in finance but want to avoid the constant pressure of sales? When I first started exploring the housing market, I kept hearing about mortgage underwriters—the invisible decision-makers who approve or deny home loans. If you've wondered what this vital role actually entails and how to break into the industry, let me guide you through everything you need to know.

Key Takeaways

-

Behind-the-Scenes Role: Underwriters analyze borrowers' financial files to evaluate lender risk instead of selling.

-

The "4 Cs" Standard: Evaluation focuses strictly on** Capacity, Credit, Capital, and Collateral**.

-

High Compensation: Average pay typically ranges from** $65,000 to $85,000** annually, depending on location, experience, and data source.

-

Tech-Driven Careers: Modern professionals use tools like Bluerate and Zeitro to boost output.

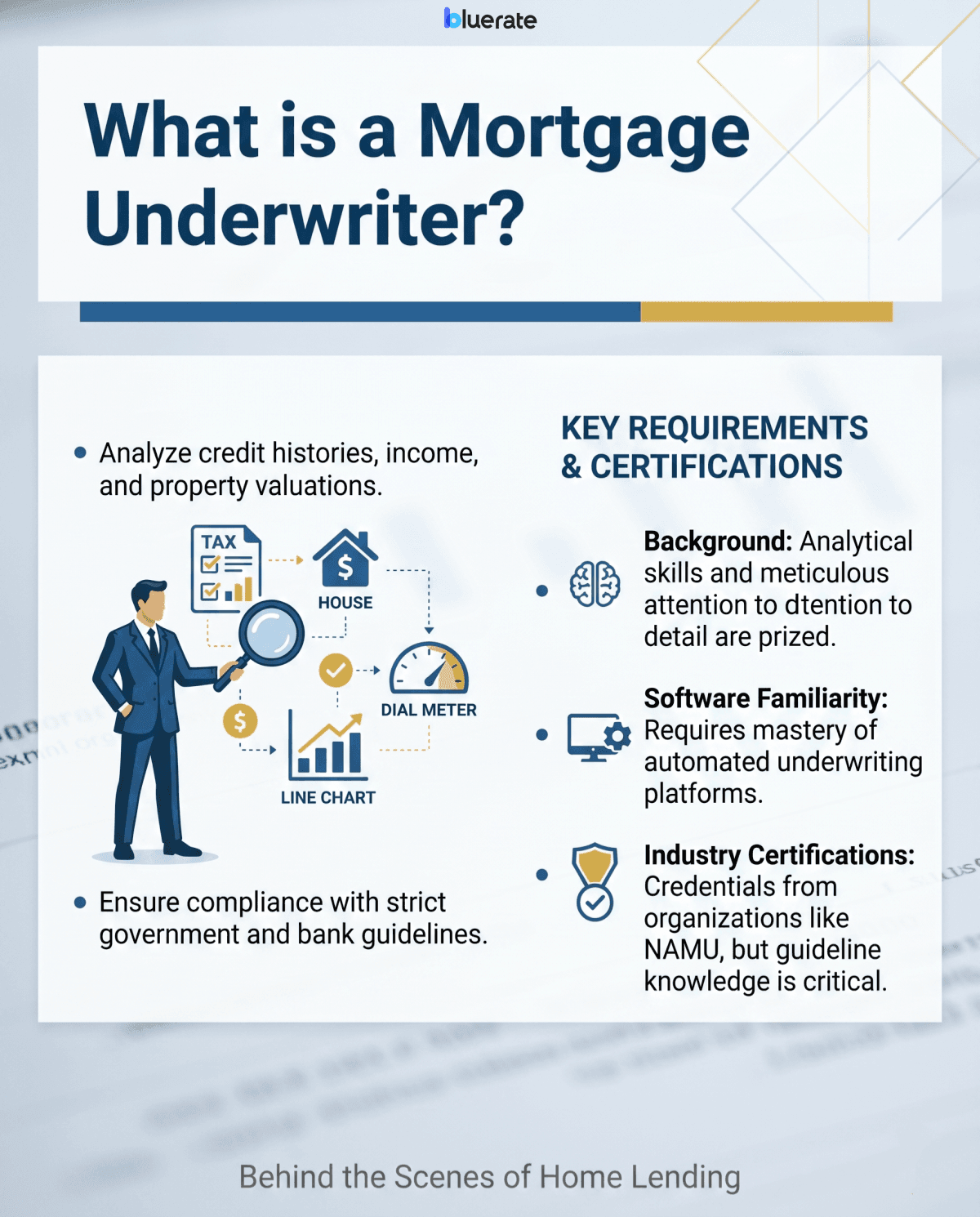

What is a Mortgage Underwriter?

A mortgage underwriter is a financial risk detective who operates behind the scenes for lending institutions. Unlike client-facing agents, my colleagues in mortgage underwriting analyze complex credit histories, income structures, and property valuations to determine if a borrower qualifies for a home loan under strict government and bank guidelines.

To thrive in this analytical environment, you must meet specific baseline requirements and acquire the right professional credentials:

-

Background: While a college degree helps, analytical skills and attention to detail are what hiring managers truly value.

-

Software Familiarity: You must master automated underwriting platforms.

-

Industry Certifications: Credentials from organizations such as NAMU may help demonstrate knowledge, though most employers place greater emphasis on hands-on experience and familiarity with mortgage guidelines.

What Does the Mortgage Underwriter Do?

In my years in this industry, I've seen that an underwriter's day revolves around translating mountains of raw financial documents into safe lending decisions. Far from just looking at numbers, they verify that loans comply with complex federal and agency rules.

Here is what their daily responsibilities look like:

-

Analyzing Income and Taxes: Carefully examining pay stubs, W-2 forms, business tax returns, and asset bank statements to spot inconsistencies.

-

Running Automated Systems: Feeding applicant profiles into Automated Underwriting Systems (AUS) like Fannie Mae's Desktop Underwriter (DU) or Freddie Mac's Loan Product Advisor (LPA).

-

Issuing Underwriting Conditions: Approving loans conditionally (e.g., requesting a missing tax form) and granting the final "Clear to Close" designation once satisfied.

What Do Underwriters Evaluate in a Mortgage? (The 4 Cs)

To make an informed decision, I always tell newcomers to focus on the traditional pillars of risk assessment known as the "4 Cs". These four pillars help paint a complete picture of a borrower's financial reliability:

-

Capacity: Checking employment stability and calculating the debt-to-income (DTI) ratio, typically targeting around 36%, though many loan programs allow higher ratios (often up to 43% or more, depending on approval systems).

-

Credit: Reviewing FICO credit scores and payment history to evaluate historical dependability.

-

Capital: Examining bank and investment accounts to guarantee the applicant has sufficient liquid funds for down payments and cash reserves.

-

Collateral: Analyzing the home appraisal report to confirm the property's market value justifies the requested mortgage amount in case of default.

Average Mortgage Underwriter Salary

When I analyze career transitions, compensation is always a top priority. In 2026, mortgage underwriters enjoy a highly competitive pay structure. Industry data from major job boards like Indeed indicates that the national average base salary hovers around $78,850 annually. Meanwhile, ZipRecruiter reports a broad median range between $55,500 and $97,500 for residential roles.

Your earning potential climbs significantly depending on experience and credentials. While entry-level processors transitioning into underwriting might start around $55,000, senior underwriters holding government endorsements, such as FHA Direct Endorsement (DE) or VA Staff Appraisal Reviewer (SAR), frequently earn over $115,000 in competitive metropolitan markets. This variance makes continuous learning incredibly rewarding.

Also Read: How Much Does a Mortgage Underwriter Make? Salary Here

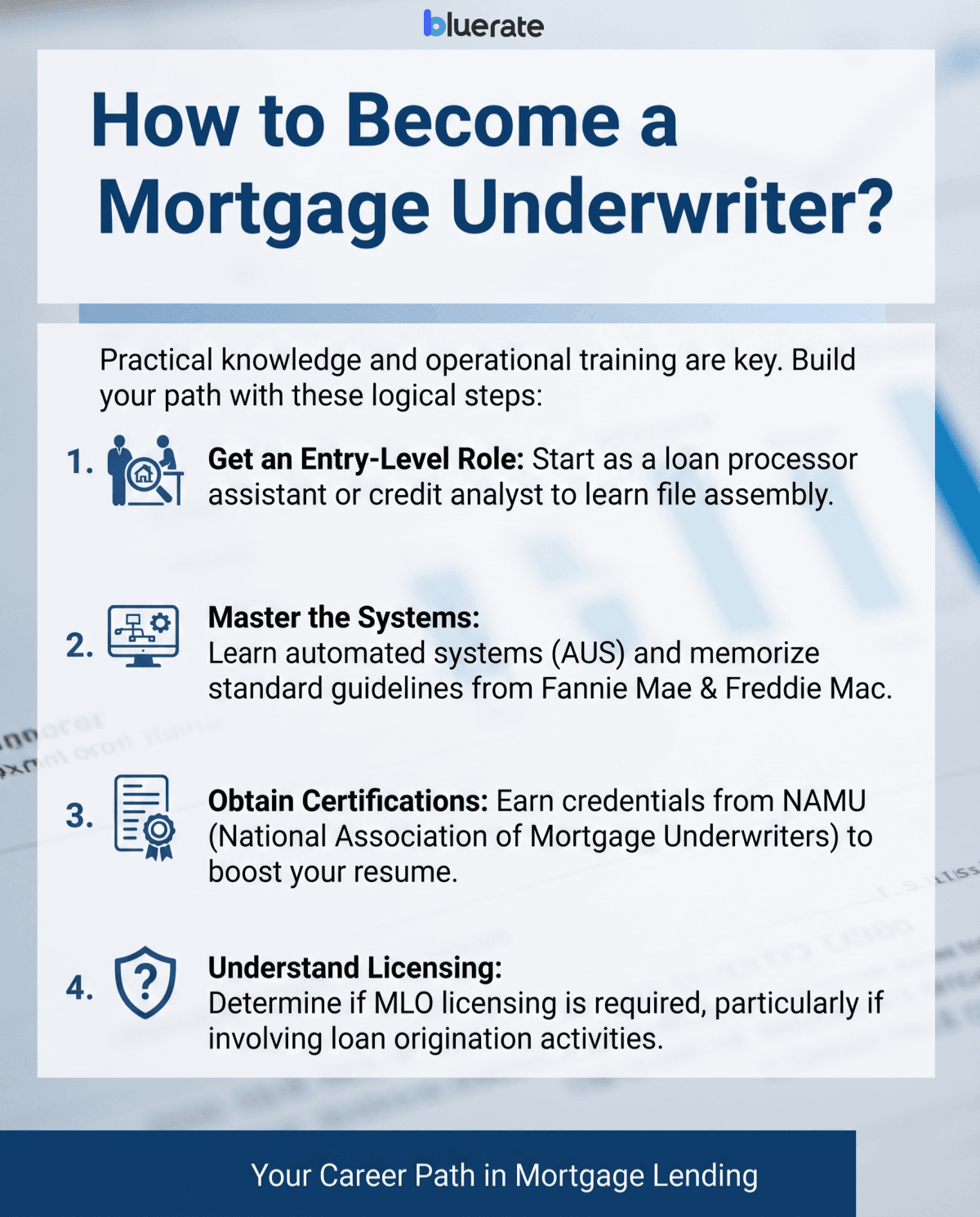

How to Become a Mortgage Underwriter?

Entering this field doesn't require a master's in finance. In my experience, practical knowledge and standard operational training are what really open doors. Here are the logical steps you can take to build your path as a mortgage underwriter:

-

Get an Entry-Level Role: Start as a loan processor assistant or credit analyst to learn how files are assembled.

-

Master the Systems: Learn automated systems (AUS) and memorize standard guidelines from agency giants like Fannie Mae and Freddie Mac.

-

Obtain Certifications: Earn credentials from organizations like the National Association of Mortgage Underwriters (NAMU) to boost your resume.

-

Understand Licensing rules: In many cases, in-house underwriters do not need an MLO license. Licensing requirements depend on job responsibilities, if the role involves loan origination activities, an MLO license may be required.

Tips for Mortgage Underwriters to Improve Efficiency

In our fast-paced industry, processing files quickly is just as important as accuracy. If you want to handle higher volumes and maximize your earnings without burning out, I recommend using these modern efficiency tips:

-

Attract Opportunities on Bluerate: Don't limit your career to traditional job boards. Creating a free profile on Bluerate lets you showcase your FHA or conventional underwriting credentials publicly. This naturally attracts lending companies and brokers looking for reliable, high-volume help.

-

Co-Pilot with AI Tools like Zeitro: Technology is a massive game-changer. I rely on AI assistants like Zeitro to verify complex lending guidelines, search local Down Payment Assistance (DPA) programs, and instantly calculate erratic borrower incomes. It saves hours of manual work and prevents errors.

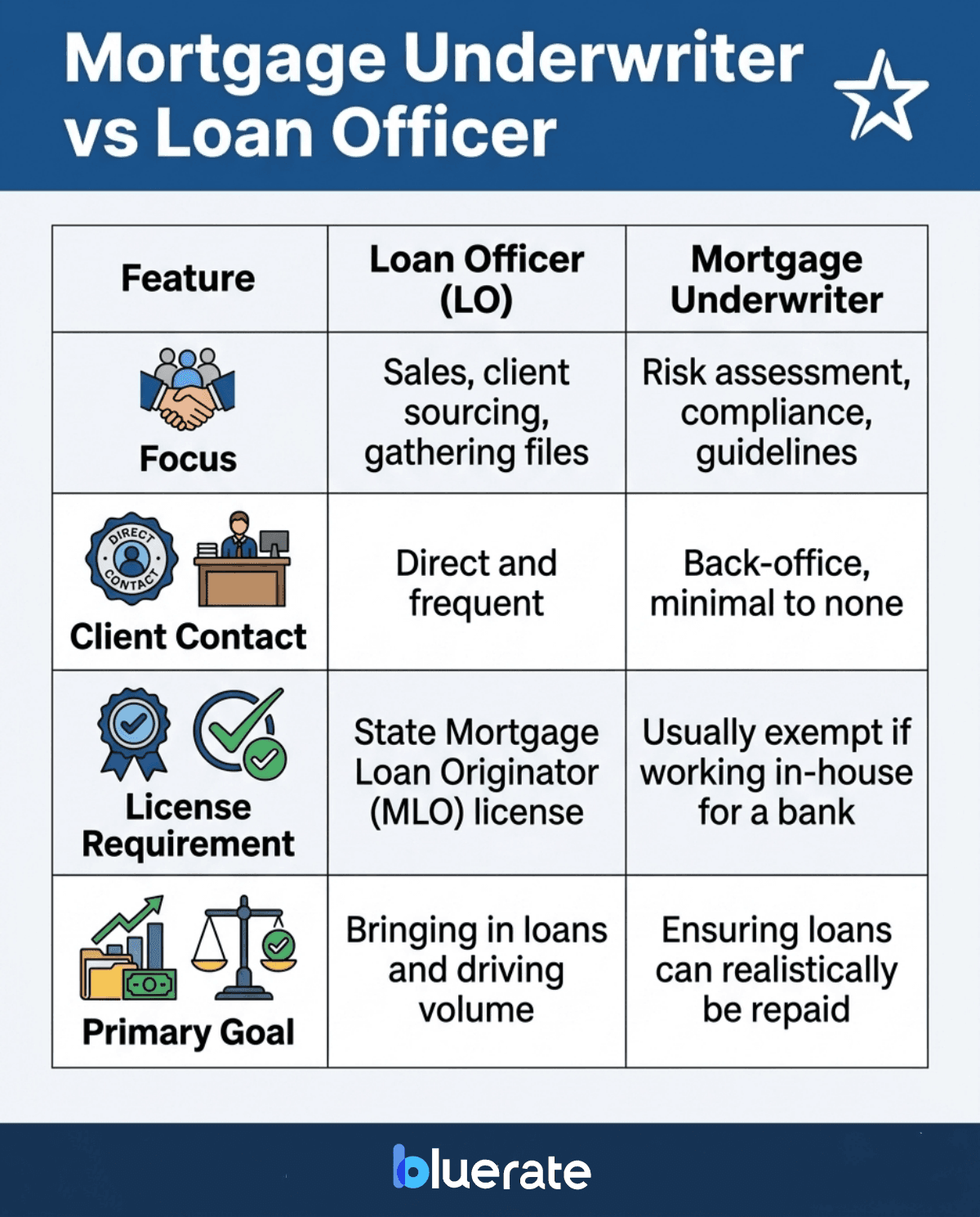

Mortgage Underwriter vs Loan Officer

People looking to break into the housing sector often ask me to clarify the differences between loan officers and underwriters. While both are critical to closing a deal, they focus on opposite ends of the transaction: loan officers are the sales-driven front office, whereas underwriters are the risk-assessing back office.

Here is a straightforward breakdown of how our roles differ:

Also Read:[ Best AI Mortgage Underwriter Software to Pick

FAQs About Mortgage Underwriters

Q1. Is it hard to become a mortgage underwriter?

It is not mathematically hard, but it does require navigating a steep learning curve. The role relies heavily on your ability to memorize complex agency guidelines and spot tiny discrepancies in massive stacks of paperwork. If you are highly organized and patient, starting in an entry-level processing position makes this transition highly manageable.

Q2. Is underwriting the last step?

No, underwriting is not the absolute final step, but it is the ultimate hurdle. Once an underwriter grants a "Clear to Close" (CTC) status, the file moves to the closing department. They will finalize legal disclosures, sign closing papers, and fund the transaction to make homeownership official.

Q3. What are red flags for underwriters?

We are trained to spot anything suggesting a borrower's financial profile is unstable or misrepresented. Major red flags include sudden, unexplained bank cash deposits, undisclosed lines of credit opened during the process, abrupt career changes right before closing, and discrepancies between their business tax returns and personal bank statements.

Q4. Will underwriting be replaced by AI?

No, AI will not replace our jobs. While modern platforms like Zeitro speed up the daily workflow by instantly parsing guidelines and calculating complex incomes, mortgage lending carries legal and financial risks requiring human accountability. AI acts as an incredibly efficient co-pilot, but human underwriters retain final signing authority.

Q5. Is underwriting a lot of math?

Not at all. You do not need a background in advanced mathematics. Most of our daily tasks involve basic algebra to calculate debt-to-income (DTI) and loan-to-value (LTV) ratios. Today, modern loan origination software and automated tools handle the math, allowing you to focus on verifying the underlying documents.

Final Word

In my view, choosing a career as a mortgage underwriter is one of the smartest, most stable moves you can make in the real estate sector. It gives you a respected back-office role that may offer remote or hybrid opportunities with plenty of room to double your salary as you gain experience and earn advanced certifications.

If you are ready to stand out and connect with leading mortgage brokers, I highly recommend creating a free profile on Bluerate. It is a fantastic, zero-cost way to market your professional skills and start attracting high-quality industry leads today. Your career transition starts with building that personal network.