Beginner's Guide: What is Mortgage Underwriting?

Once you submit your first mortgage application, a quiet, nerve-wracking waiting period begins. Suddenly, your loan officer mentions your file has "gone to underwriting," and you're left wondering what that actually means.

Honestly, it's not a secret trial. After years of guiding borrowers through this milestone, I've learned that demystifying this behind-the-scenes step is the fastest way to replace your anxiety with confidence. Let's break it down.

Key Takeaway

- Fact-checking process: Underwriting reviews your financial documents and other loan data to assess the lender's risk.

- The core criteria: Lenders focus heavily on your capacity, credit, capital, and collateral.

- Freeze your habits: Don't open credit cards, switch jobs, or transfer large funds during this time.

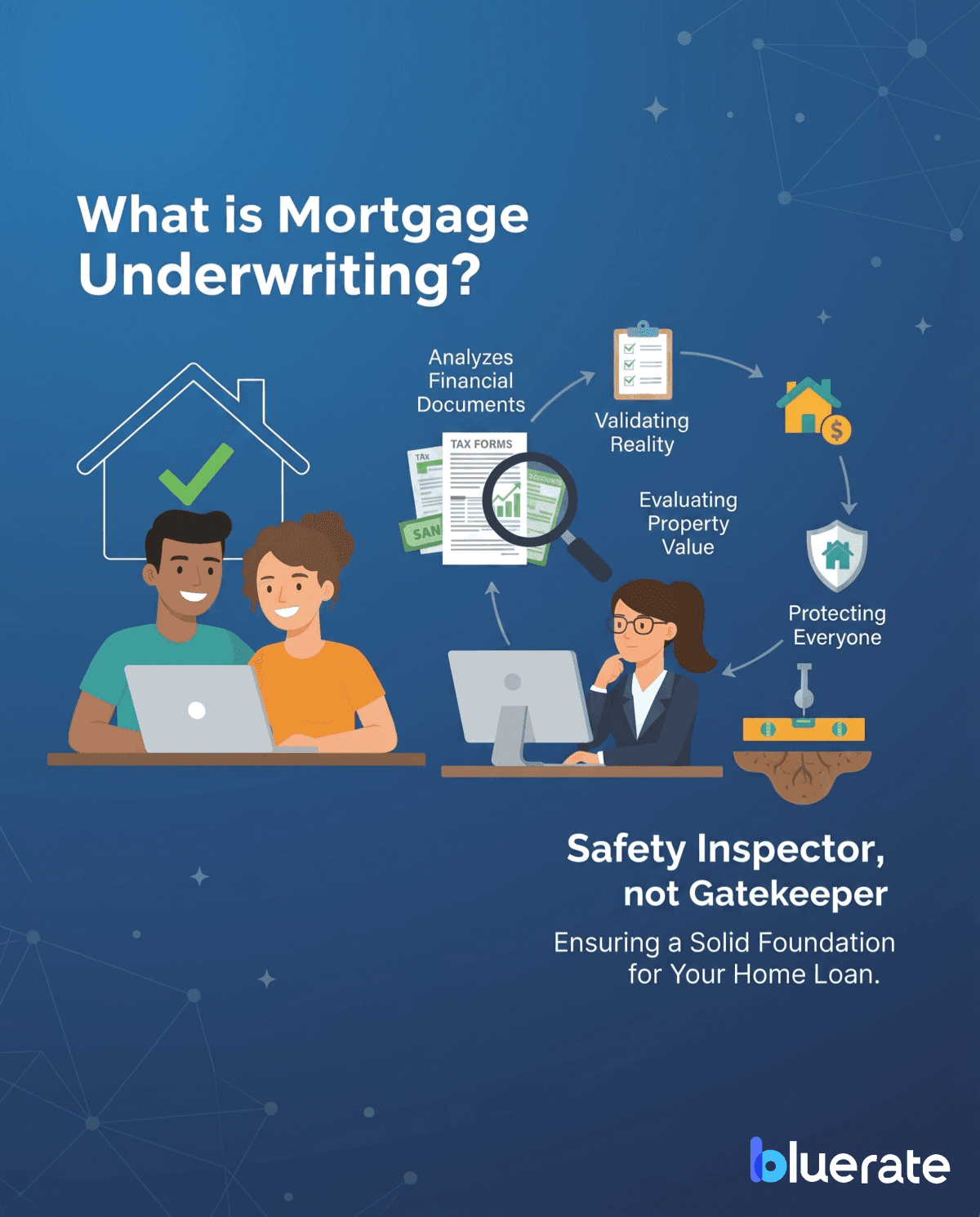

What is Mortgage Underwriting?

Getting pre-approved is exciting, but it's only the dress rehearsal. The real show begins with underwriting—the rigorous process where a lender decides if they can safely hand you hundreds of thousands of dollars to buy a home.

While your loan officer helps you build your application and roots for you, the mortgage underwriter is the impartial decision-maker behind the scenes. They don't just take your word for it. They analyze your financial documents to verify you can actually handle the debt.

Essentially, underwriting serves three critical purposes:

- Validating reality: It ensures your tax returns, bank accounts, and employment history match the numbers on your application.

- **Evaluating property value: ** It checks whether the home's appraised value supports the loan amount.

- Protecting everyone: It stops you from taking on a mortgage that could lead to foreclosure while protecting the lender from bad debt.

I always tell my clients to view underwriters as safety inspectors rather than gatekeepers. They're just making sure the foundation of your loan is completely solid.

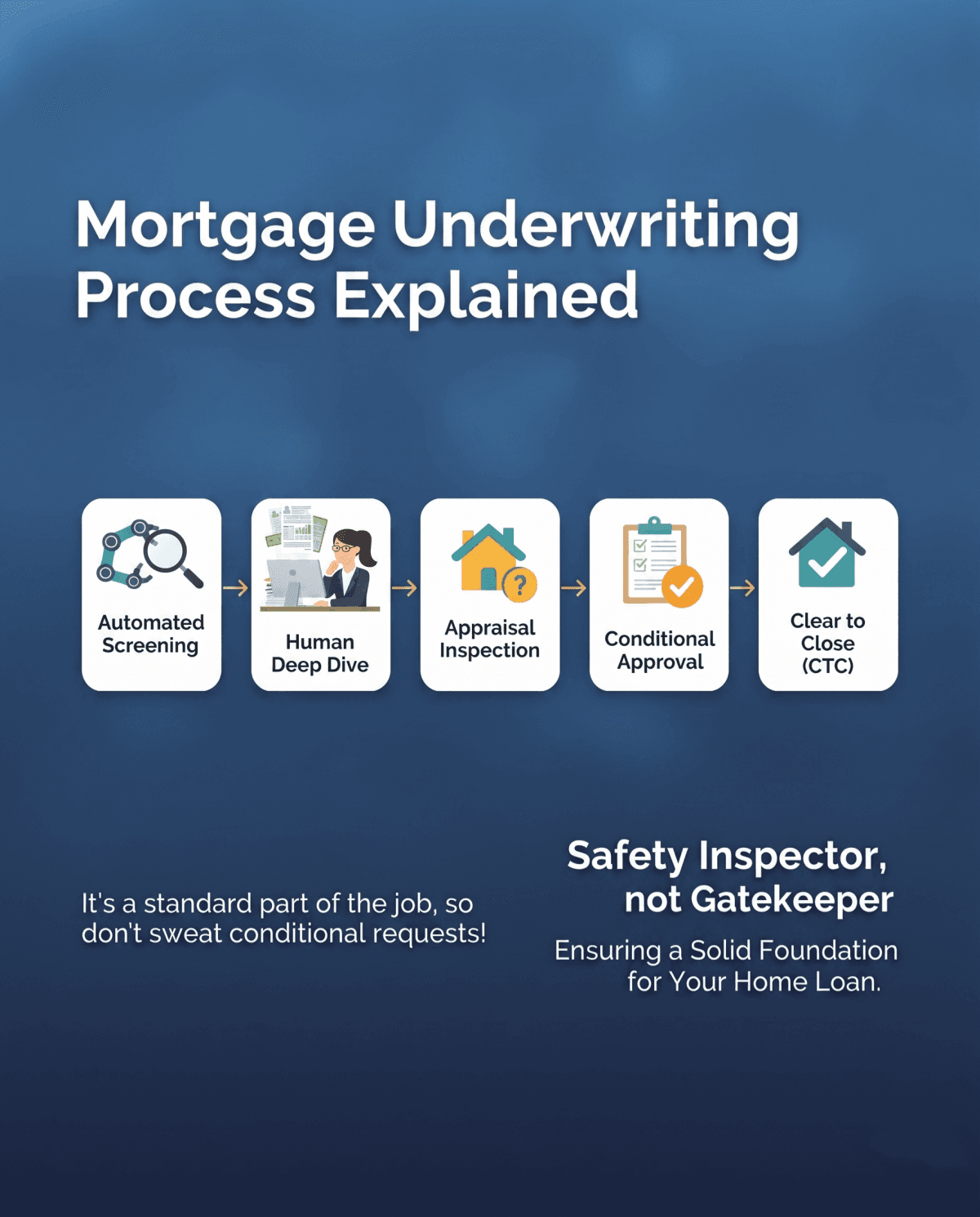

Mortgage Underwriting Process Explained

The underwriting process often includes automated review, manual review, conditional approval, and then clear to close, though the exact sequence can vary by lender and loan type.

- Automated Screening: Your application first goes through an automated underwriting system (AUS) like Fannie Mae's DU to check basic eligibility.

- The Human Deep Dive: An actual underwriter manually reviews your W-2s, bank statements, and tax returns for any red flags.

- Appraisal Inspection: The underwriter evaluates the home appraisal to ensure the property matches the loan value.

- Conditional Approval: You receive an initial "yes," but with a request for more documents (like an updated paystub or proof of a deposit).

- Clear to Close (CTC): Once you submit those final pieces, you get the official green light to sign your papers.

I rarely see a file go through without at least one or two conditional requests. It's a standard part of the job, so don't sweat it when they ask for more paperwork. Also Read: How Long Does Mortgage Underwriting Take? Check Here

What are Mortgage Underwriting Guidelines?

Think of underwriting guidelines as the official rulebook for home loans. These rules are set by government agencies and entities like Fannie Mae, Freddie Mac, the FHA, and the VA to keep the mortgage market safe and predictable. On top of these national rules, individual lenders usually add their own stricter rules, which we call "overlays."

Specifically, these guidelines help to:

- Prevent risky lending practices.

- Standardize loan quality across the country.

Pro Tip: Keeping up with constantly shifting rules is incredibly tough. That is why many loan officers and underwriters use Zeitro Strata*, ***an AI tool that lets them instantly look up and verify complex guidelines across various programs.

Also Read:

- Mortgage Eligibility Checker - Best Helper for Loan Pros

- Zeitro Strata Review: World's No.1 Best Mortgage Guidelines Checker

How Long Does Underwriting Take for a Mortgage?

In many cases, the active underwriting phase takes about 3 to 14 business days, but the exact timeline can be shorter or longer. The exact timeline depends heavily on your financial setup and how fast third parties move.

If you have a straightforward W-2 job, things usually move pretty fast. But if you're self-employed, have complex business tax returns, or own multiple properties, the underwriter has to do a lot more math.

The best way to avoid delays is to respond quickly when your lender requests additional documents. Whenever your loan officer asks for a document, getting it to them within a couple of hours can shave days off your closing timeline.

Why is a Mortgage Loan Denied in Underwriting?

Even with a strong pre-approval, things can go wrong during underwriting. Lenders can—and do—deny loans at this stage if they spot sudden changes. Here are the most common culprits:

- New credit activity: Financing new furniture or opening a credit card right before closing.

- Mystery deposits: Large, unexplained cash going into your bank accounts without a clear paper trail.

- Employment shakeups: Quitting your job, switching industries, or going from a salary to commission.

- Debt-to-Income spikes: aking on a new car payment that pushes your DTI beyond the loan program's limits.

My advice? Keep your credit and bank accounts completely frozen in place until you have the keys in hand.

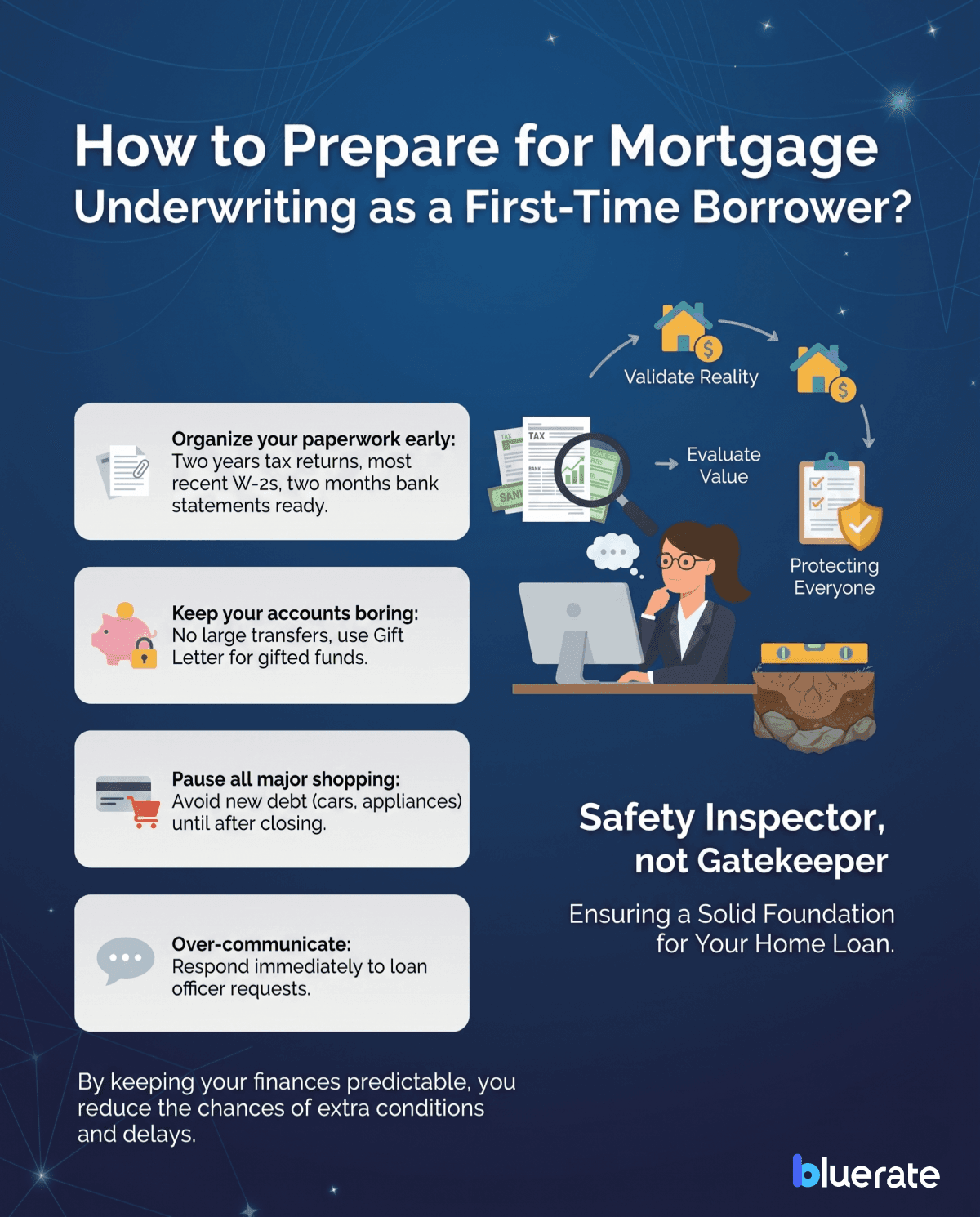

How to Prepare for Mortgage Underwriting as a First-Time Borrower?

You don't have to just sit back and hope for the best. Being proactive can make your underwriting experience incredibly smooth. Here is what I tell all my first-time buyers to do:

- Organize your paperwork early: Have two years of tax returns, your most recent W-2s, and two months of bank statements ready.

- Keep your accounts boring: Don't move money around between banks. If a relative is gifting you funds, make sure you get a signed Gift Letter first.

- Pause all major shopping: Save the credit card swipes for after the loan funds. No cars, no appliances, no new debt.

- Over-communicate: If your loan officer asks for something, reply immediately.

By keeping your finances predictable, you reduce the chances of extra conditions and delays.

FAQs About Mortgage Underwriting

Q1. Should I be worried about underwriting?

Not if you were honest from the start. If you provided accurate documents during the pre-approval phase and your loan officer vetted your file properly, underwriting is just a routine check to cross the t's and dot the i's.

Q2. What is the role of a mortgage underwriter?

Think of them as risk managers. Your loan officer is your advocate who helps you apply, but the underwriter is the objective judge who verifies that your file complies with the lender's risk rules and federal laws.

Q3. What are the 4 C's of underwriting?

Underwriters analyze four main pillars to assess your risk:

- Capacity: Your income, job stability, and DTI ratio.

- Capital: Your down payment source and post-close cash reserves.

- Collateral: The home's actual worth determined by an appraisal.

- Credit: Your credit score and track record of paying back debts.

Q4. Is underwriting the final approval?

No. You'll first get a conditional approval. The final green light is "Clear to Close" (CTC). Some lenders may re-check credit before funding to confirm that no major changes have occurred.

Q5. What is the 3 7 3 rule?

It's a federal consumer protection timeline:

- 3 Days: Lenders must give you a Loan Estimate (LE) within three business days of applying.

- 7 Days: You cannot close your loan until at least seven business days after getting your LE.

- 3 Days: If your APR changes significantly before closing, you must get a new disclosure and wait three business days before signing.

Conclusion

Surviving the underwriting process comes down to preparation, keeping your finances incredibly boring, and working with a professional you trust.

If you want to skip the stress of your first loan, I highly recommend checking out Bluerate. It is an AI-powered mortgage marketplace designed by Zeitro that prioritizes your privacy. Instead of selling your contact info to aggressive telemarketers who will spam your phone, Bluerate securely matches you with highly rated, local Loan Officers. They'll walk you through the entire underwriting process step-by-step, giving you peace of mind and keeping your inbox spam-free.

People Also Read

- Must-Read: How Long is a Mortgage Preapproval Good for?

- 10 Tips: First-Time Home Buyer Tips and Advice for You

- Must Read: Minimum Down Payment for House First-Time Buyer

- Best First-Time Home Buyer Programs: Which One to Apply?

- Best First-Time Home Buyer Lenders: Find Your Perfect Match

- How to Become a Mortgage Underwriter with No Experience?