How Long Does Mortgage Underwriting Take? Check Here

Signing a home purchase contract is incredibly exciting, but waiting for the loan approval can feel like an agonizing waiting game. I remember staring at my phone, constantly wondering how long the mortgage underwriting phase would actually take.

Typically, the underwriter's review can take anywhere from a few days to a few weeks, while the full loan-to-closing process often takes about 30 to 45 days. Let's look at exactly what goes on behind the scenes and how to speed things up.

Key Takeaways

- The Sweet Spot: Core mortgage underwriting generally takes 3 to 14 days, while the entire closing process averages 41 days.

- Main Bottlenecks: Delays usually stem from missing financial records, property appraisal backlogs, or complex self-employment income.

- Proactive Action: You can accelerate approval by responding to requests within 24 hours and keeping your credit strictly frozen.

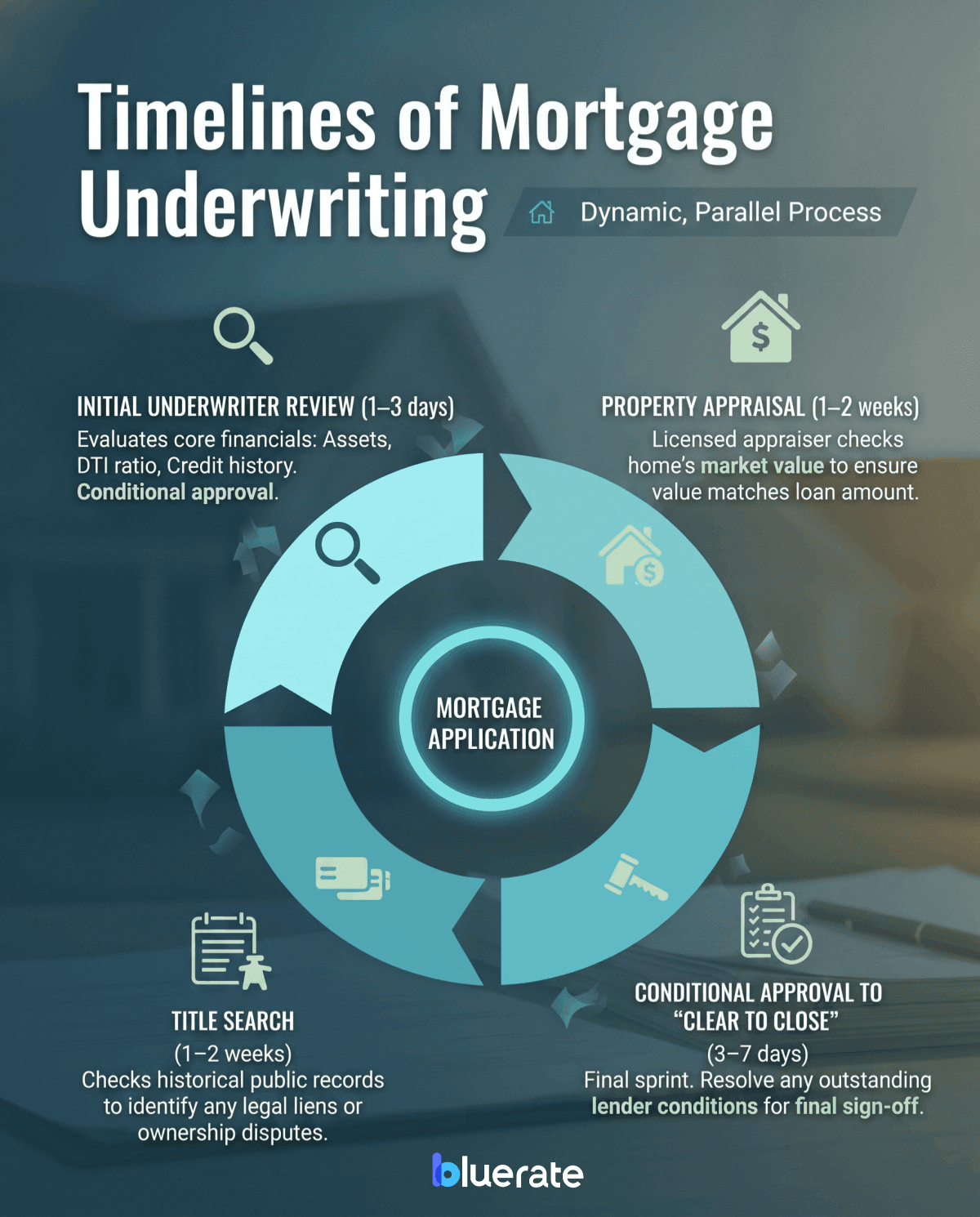

Timelines of Mortgage Underwriting

Once you submit your application, it doesn't just sit in a folder. It enters a dynamic, parallel process where several moving parts operate simultaneously rather than in a slow, linear queue.

- Initial Underwriter Review (1–3 days): The underwriter evaluates your core financial profile, reviewing your assets, debt-to-income (DTI) ratio, and credit history, and may issue a conditional approval if the file otherwise meets guidelines.

- Property Appraisal (1–2 weeks): A licensed third-party appraiser assesses the home's market value to ensure the property matches the loan amount.

- Title Search (1–2 weeks): A title company checks historical public records to help identify any legal liens or ownership disputes before the transfer.

- Conditional Approval to "Clear to Close" (3–7 days): This is the final sprint. Once you resolve any outstanding conditions requested by the lender, they authorize the final sign-off.

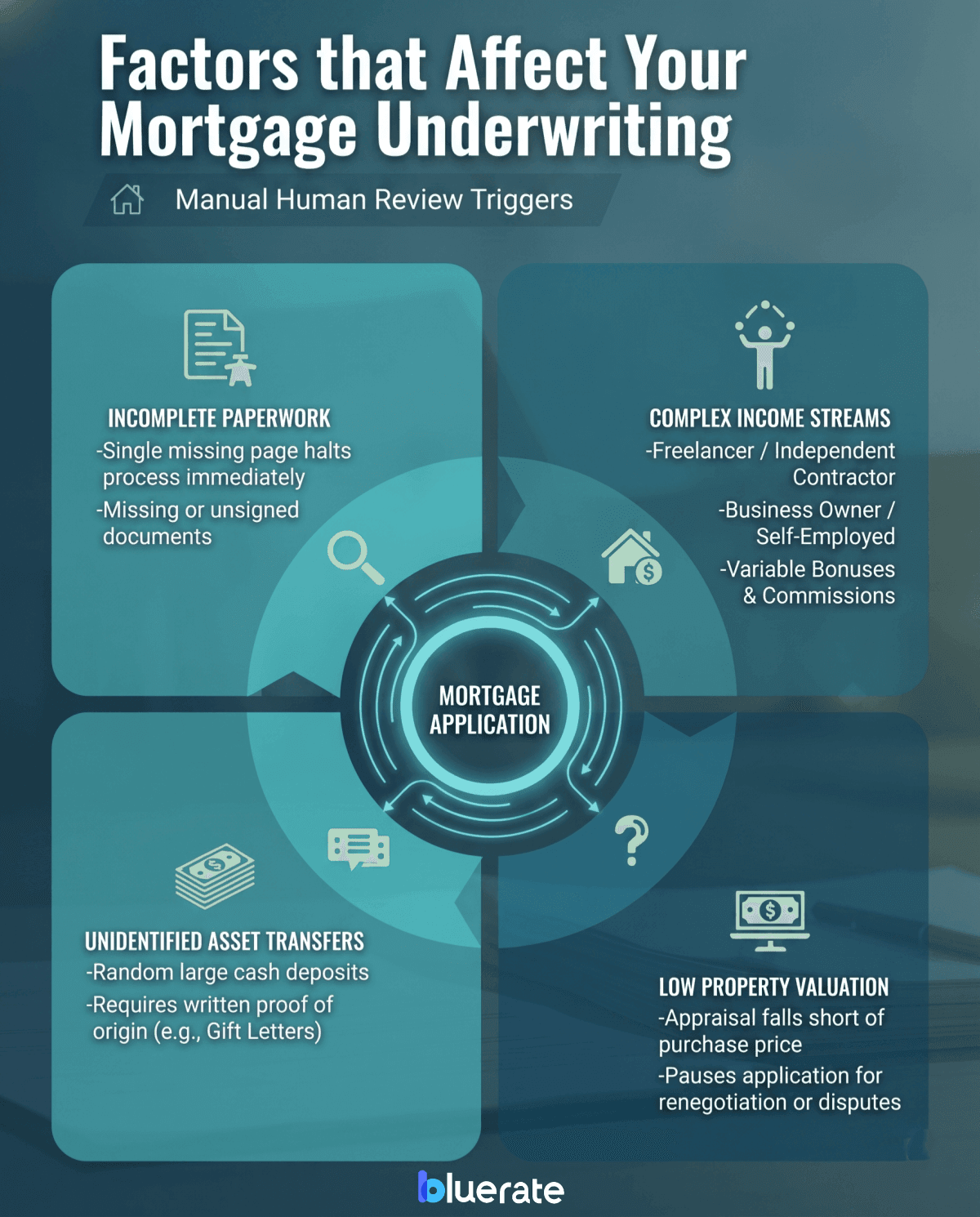

Factors that Affect Your Mortgage Underwriting

In my experience helping buyers navigate this, no two financial profiles are identical, which explains why timelines vary wildly. Automated underwriting systems can run basic algorithms in minutes, but several triggers force a deeper, manual human review:

- Incomplete Paperwork: Forgetting to send a single page of a bank statement halts the process immediately.

- Complex Income Streams: Being a freelancer, business owner, or relying on variable bonuses requires meticulous tax return verification.

- Unidentified Asset Transfers: Random, large cash deposits on your statements trigger red flags that require written proof of origin, like gift letters.

- Low Property Valuation: If the appraisal falls short of the purchase price, renegotiations or secondary disputes will pause your application.

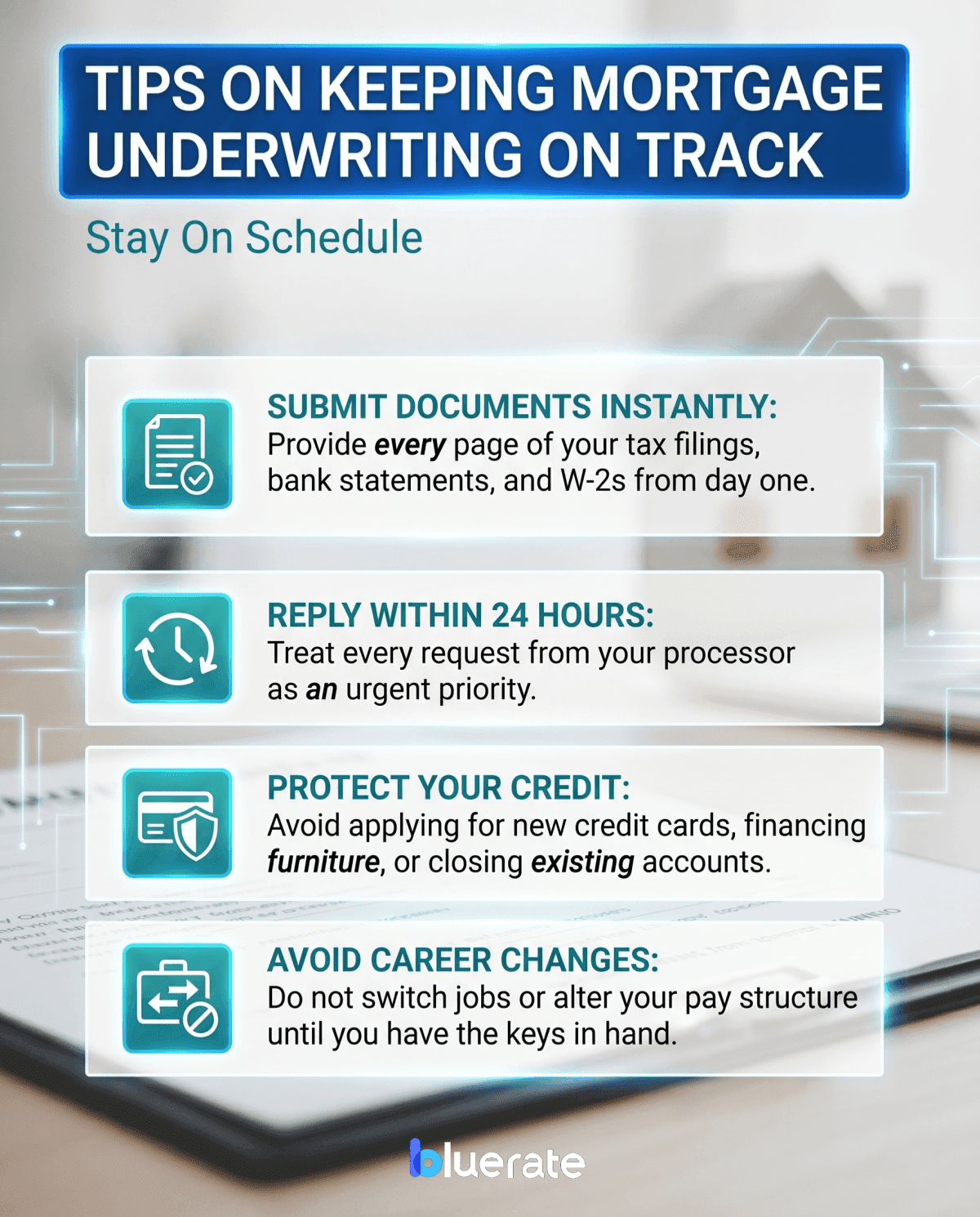

Tips on Keeping Mortgage Underwriting on Track

You actually hold a lot of leverage when it comes to keeping your loan timeline moving forward. To prevent unexpected delays and keep your closing on schedule, I highly recommend following these guidelines:

- Submit Documents Instantly: Provide every page of your tax filings, bank statements, and W-2s from day one.

- Reply Within 24 Hours: Treat every request from your processor as an urgent priority.

- **Protect Your Credit: **Avoid applying for new credit cards, financing furniture, or closing existing accounts.

- Avoid Career Changes: Do not switch jobs or alter your pay structure until you have the keys in hand.

FAQs About the Timeline of Mortgage Underwriting

Q1. Do mortgages get declined at the underwriting stage?

Yes, loans can be denied during underwriting. In many cases, the lender may first issue a conditional approval and give you a chance to address outstanding issues.

Q2. Is the underwriter the last step?

No, the underwriter is not the final step. After they approve your file, it moves to the closing department. They will prepare your closing package, verify your homeowners' insurance, and may perform a final credit check before coordinating the transfer of funds.

Q3. Can you be denied after underwriting?

Yes, you can still be denied even after receiving conditional approval. Lenders often verify your employment shortly before closing and may also perform a final credit refresh. If you finance a new car, quit your job, or significantly reduce your savings before closing, the lender may delay or deny funding.

Q4. What can ruin underwriting?

Several critical blunders can derail your approval. The biggest culprits include opening new credit lines, making undocumented cash deposits, changing jobs mid-process, or ignoring your lender's urgent requests. Additionally, a low home appraisal or unresolved title liens on the property can completely stall or ruin the transaction.

Q5. What happens after underwriting approval?

Once approved, you receive a "Clear to Close" status. Your lender must provide you with a Closing Disclosure at least three business days before closing, giving you time to review the final loan terms and closing costs. Finally, you will attend the closing meeting, sign the deeds, pay your down payment, and get your keys.

Final Word: Should I Worry During Underwriting?

It is completely natural to feel anxious while your loan is in underwriting, but you should not let the stress consume you. Underwriters ask for a lot of documents because federal lending regulations are incredibly strict, not because they are looking for a reason to deny you. In fact, no news is often good news.

By keeping your financial profile completely stable and maintaining open communication with your loan officer, you will set yourself up for a smooth transition. Take a deep breath—you are incredibly close to crossing the finish line and unlocking the door to your brand-new home.