When to Lock in a Mortgage Rate: A Loan Officer's Guide

As a loan officer for over a decade, I see the same panic in my clients' eyes every time the market shifts. You finally found the perfect house, but the daily news about inflation makes you sweat. I get it. The anxiety is real.

But here is my honest advice: timing the market perfectly is impossible, but making a smart financial decision isn't. If you're wondering exactly when to lock in a mortgage rate, let's skip the confusing financial jargon. I'll show you exactly how professionals approach this, so you can sleep soundly at night.

Key Takeaways

-

A rate lock protects you: It guarantees your interest rate won't jump before closing.

-

Focus on your budget, not the market: Lock when the monthly payment comfortably fits your income.

-

Timing matters: A common approach is to lock about 30 to 45 days before your scheduled closing, but the right timing depends on your lender and closing timeline.

-

Ask about a float-down: This secret weapon lets you grab a lower rate if the market suddenly drops.

What is a Mortgage Rate Lock?

Think of a mortgage rate lock as a financial safety net. It's a formal agreement between you and your lender that freezes your interest rate for a specific period, often 30, 45, or 60 days, though some lenders offer longer terms.

Even if national rates rise after you lock, your rate is protected as long as you close within the lock period and your application does not change materially. Just keep in mind that once it expires, you might have to pay extension fees to keep that safety net intact.

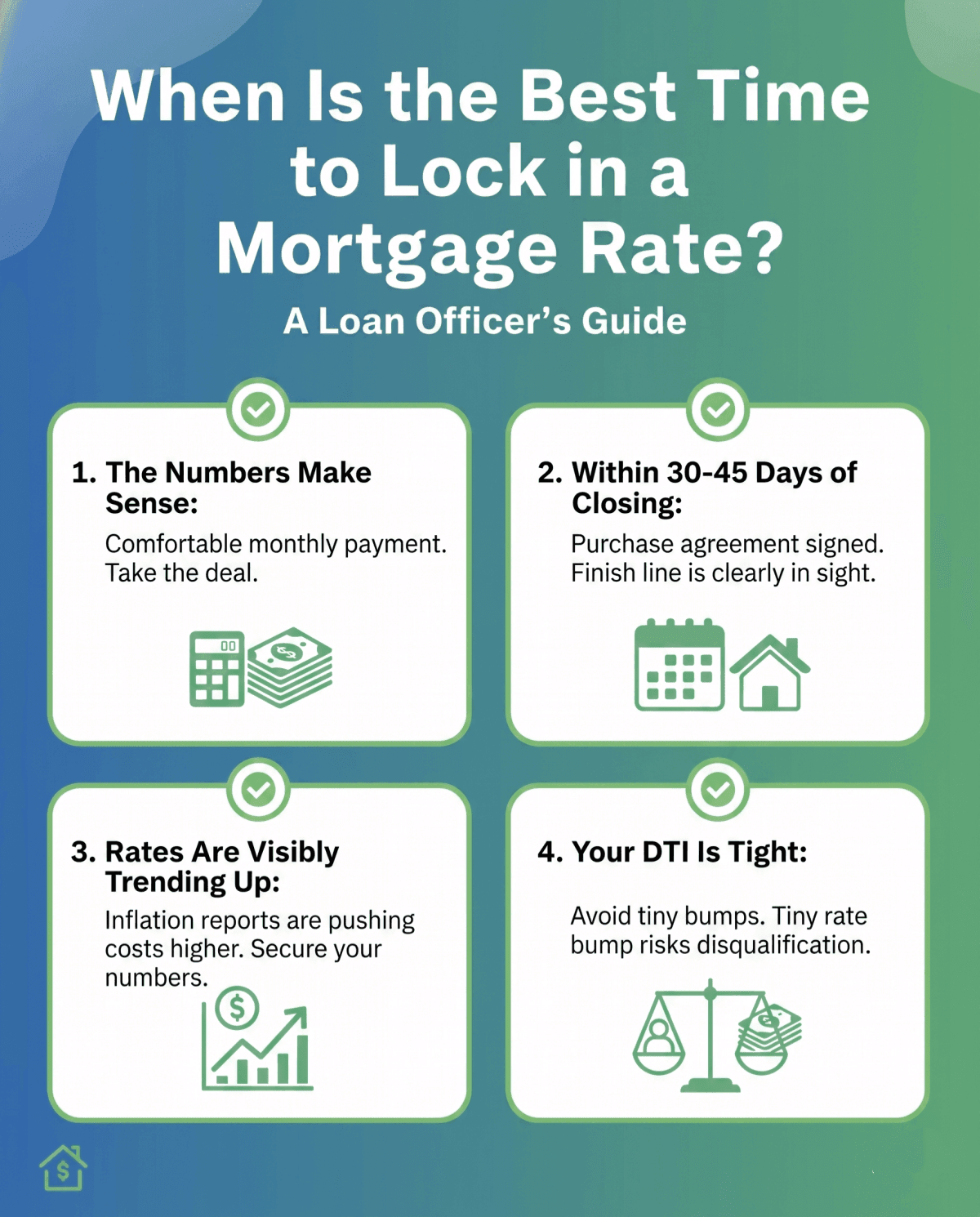

When Is the Best Time to Lock in a Mortgage Rate?

I always tell my buyers that deciding when to pull the trigger is less about Wall Street and more about your personal wallet. You shouldn't try to outsmart economists. Instead, look for these green lights. It's time to lock a mortgage rate when:

-

The numbers make sense: If the current rate gives you a monthly payment you are entirely comfortable with, take the deal. Greed can backfire.

-

You are within 30 to 45 days of closing: This is the ideal window. Your purchase agreement is signed, and the finish line is clearly in sight.

-

Rates are visibly trending up: If inflation reports are pushing costs higher across the board, secure your numbers before they price you out of the home.

-

Your Debt-to-Income (DTI) ratio is tight: If your budget is stretched to the maximum limit, even a tiny 0.25% bump could disqualify you from getting the loan entirely. Don't risk your approval over a fraction of a percent.

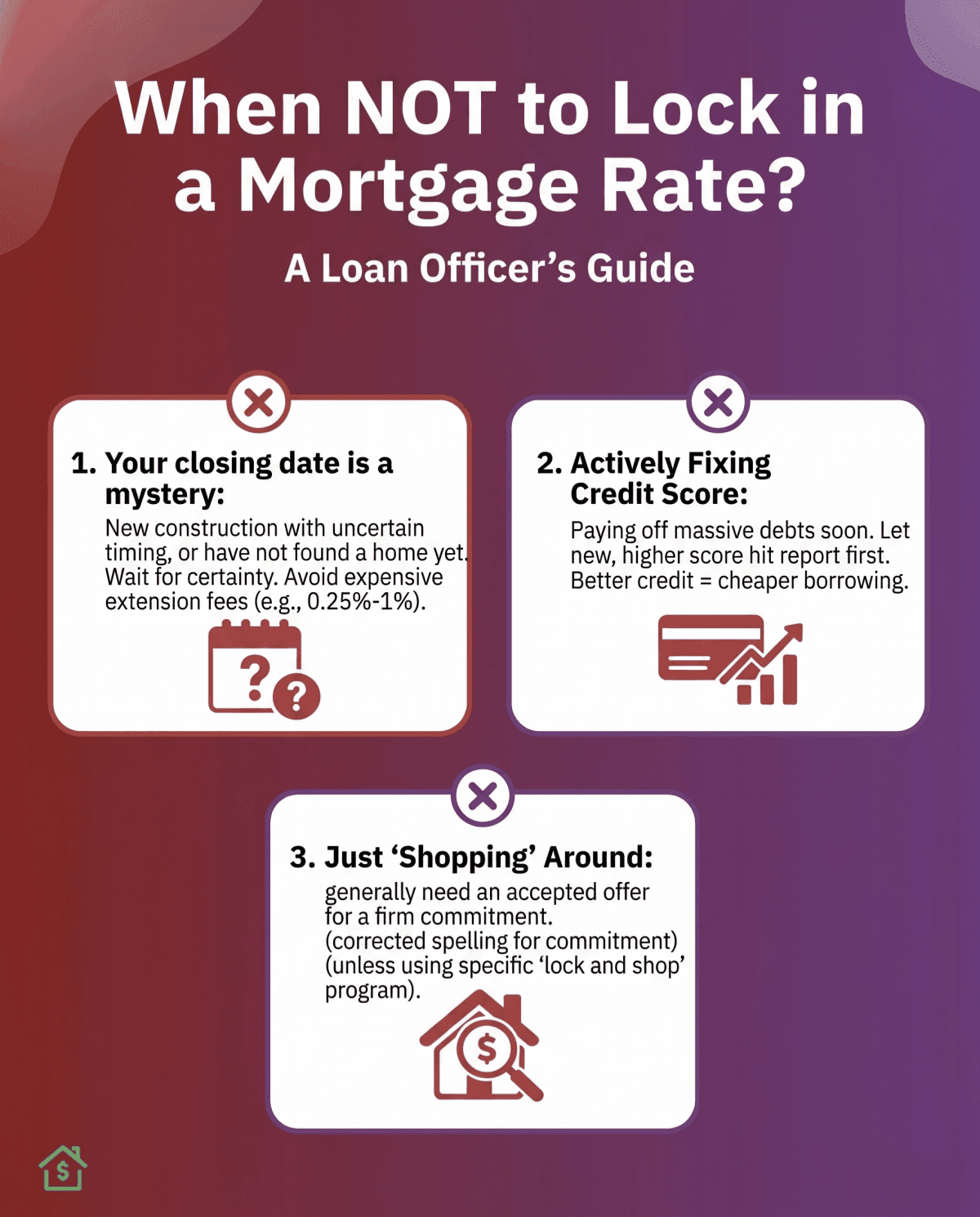

When NOT to Lock in a Mortgage Rate?

On the flip side, acting too early can cost you heavily. I once had a client insist on locking six months out for a new build, and the delay fees were brutal. Hold off if you fall into these categories:

-

Your closing date is a mystery: If you are buying new construction with uncertain timing or you have not found a home yet, consider waiting unless you have a longer lock period or a lender-approved lock strategy. Lenders may charge extension fees if your lock expires before closing, and these fees vary by lender, often ranging from about 0.25% to 1% of the loan principal, or a flat fee.

-

You are actively fixing your credit score: Paying off a massive credit card balance next week? Let that new, higher score hit your report first. Better credit equals cheaper borrowing.

-

You're just "shopping" around: Unless you are using a specific "lock and shop" program, you generally need an accepted offer on a property to get a firm commitment from a bank.

Key Factors to Consider Before Locking in Your Rate

Before signing that rate agreement, we need to look at the bigger picture. Here are the objective details I review with every client:

-

Closing Timeline: Is the seller highly motivated, or is there a complicated title issue? Your locked days must easily cover the entire escrow period.

-

Economic Indicators: While we can't predict the future, paying attention to the Federal Reserve's major announcements or recent inflation data helps gauge the overall wind direction.

-

Lock Fees: Many lenders do not charge a separate fee for a standard 30-day lock, although the cost may be reflected in the rate or points. However, requesting a 90-day or 120-day safeguard will likely require an upfront fee. Always ask about the cost first.

How Long Before Closing Should You Lock in a Rate?

A common rookie mistake is waiting until the week of closing to secure your financing. Don't do that! Most successful buyers lock in their numbers right after signing the official purchase agreement.

Realistically, you should do this anywhere from 15 to 60 days before you get the keys. Just remember the golden rule of lending: the longer the guarantee period, the more expensive it becomes.

A 30-day window is standard and cost-effective, giving underwriters plenty of time to process your paperwork.

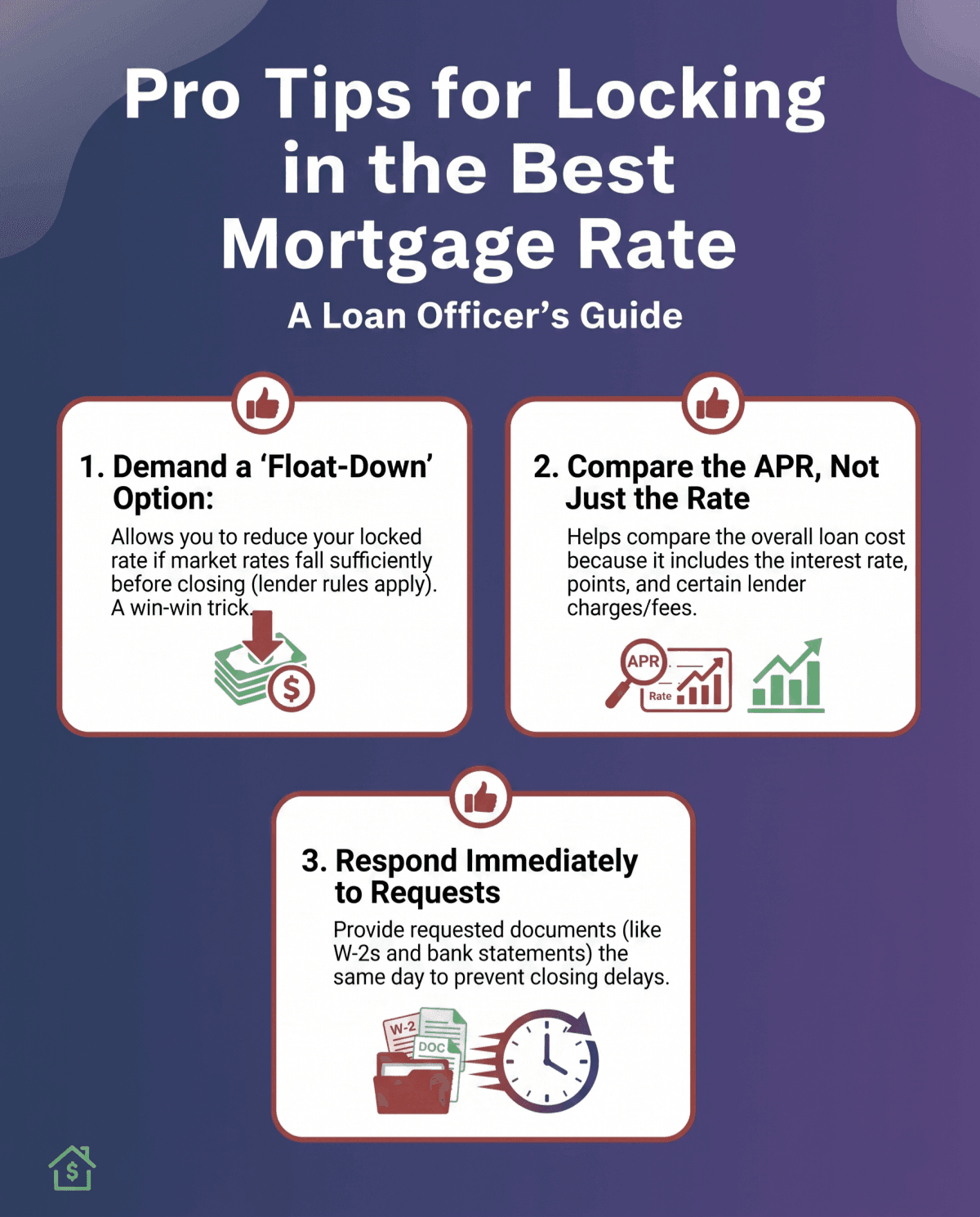

Pro Tips for Locking in the Best Mortgage Rate

Want to navigate this process like an insider? Here are a few strategies I share with my favorite clients to ensure they get the best possible deal:

-

Demand a "Float-Down" Option: This is my favorite trick. If rates fall enough before closing, a float-down option may let you reduce your locked rate, subject to your lender's rules and timing requirements. It's a win-win.

-

Compare the APR, not just the Rate: The Annual Percentage Rate (APR) helps compare the overall cost of loans because it includes the interest rate and certain lender charges, such as points and some fees.

Also Read: Mortgage Interest Rate vs. APR: What's the Difference?

- Respond to emails immediately: Once locked, the clock is ticking. Provide your W-2s, bank statements, or any requested documents to your loan officer the same day to prevent closing delays.

FAQs About Timing to Lock in a Mortgage Rate

Q1. How do I know when to lock in a mortgage rate?

Stop chasing the absolute market bottom. You know it's time when the current numbers yield a monthly payment that comfortably fits your household budget. If the math works for your family and your closing date is set, secure it and stop checking the news.

Q2. What day of the week is best to lock in a mortgage rate?

Honestly, there is no magical day like "Mortgage Tuesday." Lenders update pricing daily based on bond market trading and major economic reports. Focus on your personal readiness, your budget, and your transaction timeline rather than trying to game the calendar.

Q3. How long should you lock in a mortgage rate?

Match the duration to your closing date, but always add a safety cushion. If your contract says you'll close in 30 days, ask for a 45-day lock. Delays happen constantly in real estate, and those extra 15 days will save you from stressful extension penalties.

Q4. Can you negotiate a mortgage rate after locking?

Typically, no. A lock is a commitment, but the rate can still change if your application changes materially, if you do not close within the lock period, or if your lender's float-down policy allows a one-time adjustment.

Q5. If I lock in a mortgage rate, can I back out?

Yes, you can usually withdraw your application, but you may lose fees already paid, such as appraisal costs or other third-party charges. However, walking away means you will likely lose any upfront money you've already spent, such as the property appraisal fee or any specific lock-in deposits.

Q6. What is a mortgage rate float-down?

It's a special feature that acts as an insurance policy for your loan. If you lock your rate today but market averages drop significantly before you close, a float-down allows you to lower your locked interest rate one time. Ask your lender if they charge extra for this!

Conclusion

At the end of the day, securing your financing shouldn't feel like a trip to a casino. As a loan officer, I've seen too many buyers lose sleep trying to guess what the market will do tomorrow. Let's recap the basics:

When to lock:

-

Your monthly payment fits your budget perfectly.

-

You are within 30 to 45 days of getting the keys.

When to wait:

-

Your construction or closing timeline is completely uncertain.

-

You are actively paying down debt to boost your credit score.

Every single homebuyer's situation is unique. Instead of stressing over daily financial charts, consult with your loan officer to map out a strategy tailored to your exact timeline and goals. We are here to help you get home safely!