HELOC vs Bridge Loan: What are the Differences? Full Guide

Have you ever wondered: What is the difference between a HELOC and a bridge loan? I get this question constantly from homeowners who want to tap into their home's equity, especially when they're trying to buy a new house before selling their current one. While both options let you access major cash, they serve entirely different purposes.

Because your financial situation is unique, there's no universal "best" choice. That's why I always recommend chatting with a local expert. You can get a free consultation with nearby loan officers through Bluerate to ensure you get accurate, customized advice. Let's dive into how these two loans actually compare.

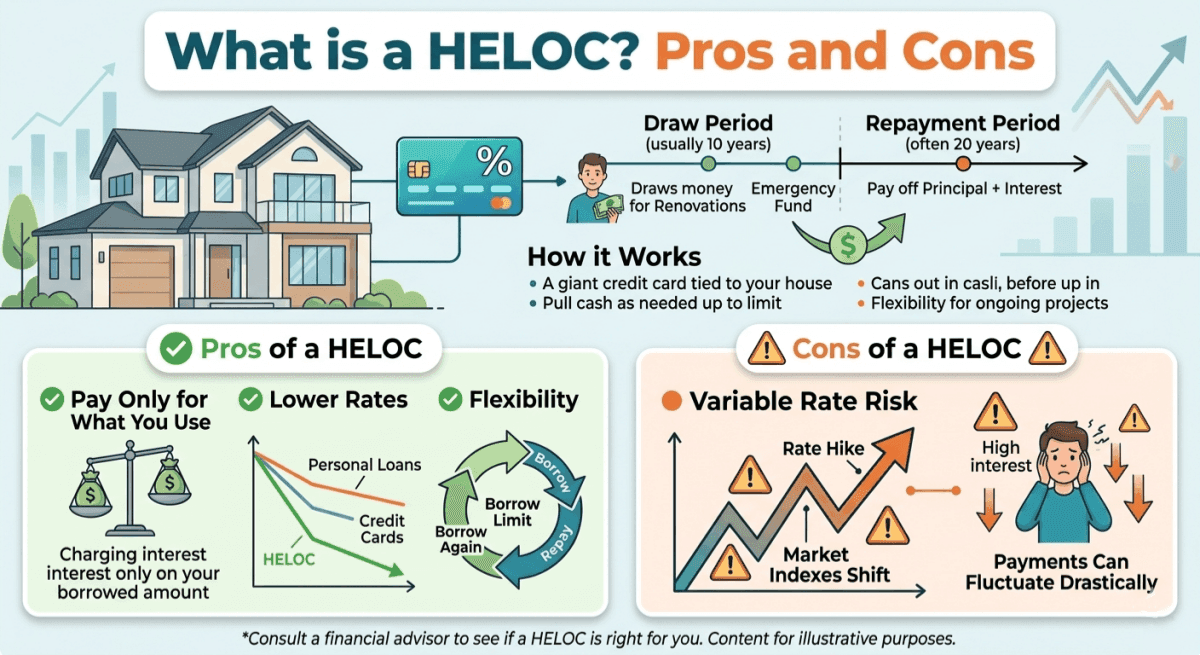

What is a HELOC? Pros and Cons

A Home Equity Line of Credit (HELOC) works much like a giant credit card tied to your house. During the initial "draw period" (usually 10 years), you can pull cash out as needed up to your approved limit. Afterward, you enter a "repayment period" (often 20 years) to pay down the principal and remaining interest. I find this option incredibly popular among people tackling ongoing home renovations or those simply wanting an emergency safety net.

Pros of a HELOC:

- Pay only for what you use: You're only charged interest on the exact amount you borrow, not the entire credit line.

- Lower rates: Historically, these lines offer lower interest compared to standard personal loans or credit cards.

- Flexibility: You can borrow, repay, and borrow again during the draw window.

Cons of a HELOC:

- Variable rate risk: Payments can fluctuate drastically as market indexes shift.

- Collateral on the line: Because your property secures the debt, you risk losing your home if you fail to make payments.

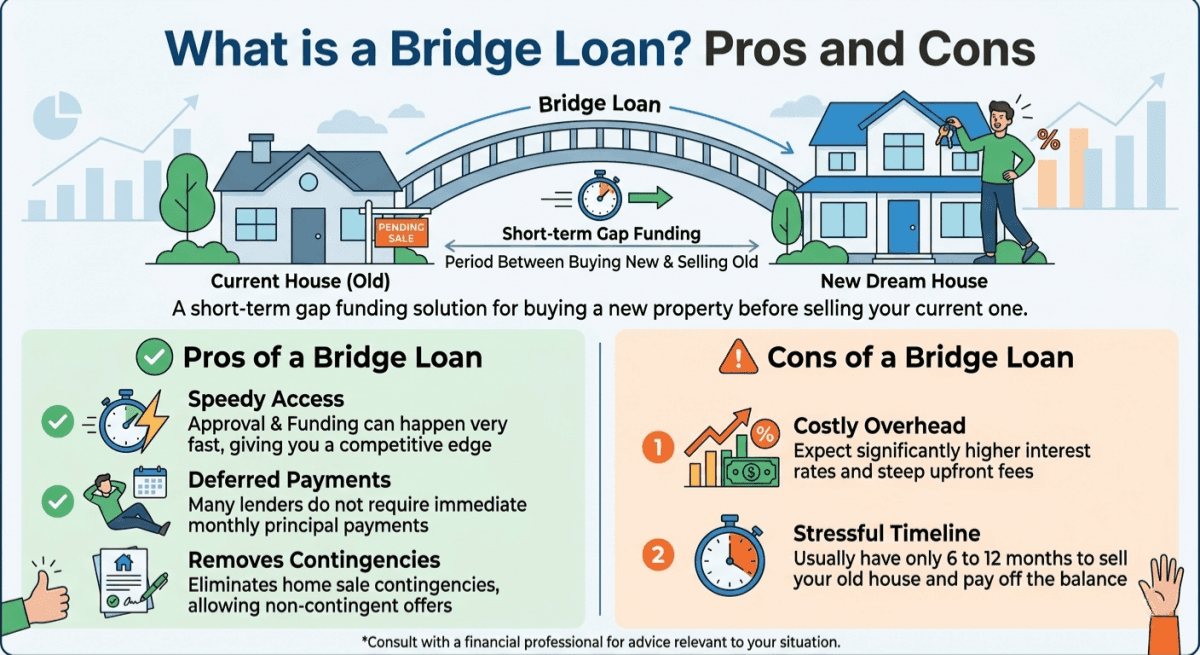

What is a Bridge Loan? Pros and Cons

If you've ever found your dream home but haven't sold your current one yet, you've probably looked into a bridge loan. Simply put, this is short-term gap funding. It effectively "bridges" the period between buying a new property and selling the old one. My clients who use this are usually in highly competitive housing markets where they need to make an aggressive, non-contingent offer fast.

Pros of a Bridge Loan:

- Speedy access: Approval and funding happen incredibly fast, giving you a cash-buyer-like edge.

- Deferred payments: Many lenders don't require immediate monthly principal payments, letting you focus on the move.

- Removes contingencies: You won't lose out on a new house just because your old one is still sitting on the market.

Cons of a Bridge Loan:

- Costly overhead: Expect significantly higher interest rates and steep upfront fees.

- Stressful timeline: You typically only have 6 to 12 months to sell your old house and pay off the balance.

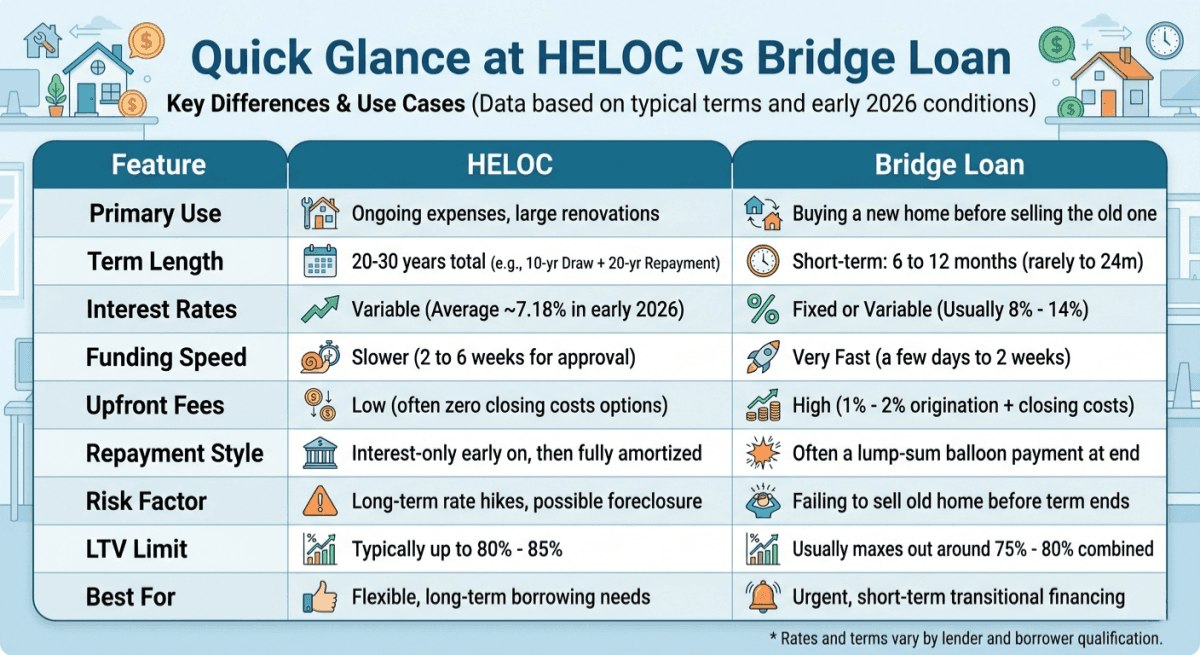

Quick Glance at HELOC vs Bridge Loan

If you're short on time and just want the bottom line, I've put together this quick comparison table breaking down the core differences.

What is the Difference between a HELOC and a Bridge Loan?

Now that you have the bird's-eye view, let's dig into the nitty-gritty. Understanding these nine specific factors will help you make a much safer financial decision for your family.

Loan Term

The time horizons for these two products couldn't be more different. A HELOC is a marathon. You generally get a 10-year draw period to use the funds, followed by a 20-year repayment phase. This typically gives you 20-30 years total to manage the debt.

Conversely, a bridge loan is a sprint. Lenders design these specifically as temporary stopgaps, usually demanding full repayment within 6 to 12 months. I've seen some stretch to 24 months, but that's rare for residential real estate. If you don't sell your house within that tight window, you could face severe financial strain or be forced to refinance the bridge loan into another high-cost product.

Interest Rate

Let's talk about the reality of borrowing costs in 2026. Right now, the U.S. Prime Rate sits at 6.75%. Since most HELOCs are tied directly to this benchmark, average HELOC rates are hovering around a very competitive 7.18% to 7.28%. They are variable, meaning your monthly bill can bounce around.

Bridge loans, however, carry a much heavier premium because the lender takes on more short-term risk. In today's market, I'm seeing bridge loan rates run anywhere from 8% to 14%. They can be fixed or variable, but they consistently sit several percentage points higher than standard mortgages or credit lines.

Credit Score

Your credit profile dictates which door you can walk through. To secure a favorable HELOC today, you really need a solid credit score---typically 680 or higher, though 740+ unlocks the best pricing. Lenders scrutinize your history because this is a long-term commitment.

Bridge lenders care about your score, but they obsess over your home equity. Even if your credit is decent, they need to ensure your Debt-to-Income (DTI) ratio is ironclad. You are essentially asking a bank to trust you with an old mortgage, a new mortgage, and the bridge loan all at once. Without a strong DTI and massive equity, you won't get approved.

Speed

When you're fighting a bidding war, timeline is everything. A HELOC usually takes its sweet time. The underwriting process mirrors a traditional mortgage, requiring a full home appraisal and thorough income verification. I tell my clients to expect anywhere from two to six weeks before seeing a dime.

Bridge loans exist specifically to bypass this waiting game. Hard money lenders and specialized bridge providers can push an approval through in a matter of days. It's entirely possible to go from application to funding in just one to two weeks. That blazing speed is exactly what allows you to swoop in and secure a new house immediately.

Cost

Closing costs can easily sneak up on you. Many modern HELOCs are incredibly cheap to open. In 2026, plenty of credit unions and online lenders offer zero-closing-cost HELOCs, though you might pay a small annual fee of $50 to $100.

Bridge loans are an entirely different beast upfront. Because lenders only make interest off you for a few months, they front-load their profits. You should expect to pay an origination fee of 1% to 2% of the loan amount, plus standard processing, appraisal, and title fees. On a $100,000 loan, you could easily swallow $2,000 to $4,000 in upfront costs alone.

Equity Requirements & Down Payment Usage

Both loans require you to have substantial skin in the game. For a HELOC, most traditional banks cap your Loan-to-Value (LTV) ratio at 80% to 85%. Once open, you can easily pull cash from this line to use as a down payment on a second home or investment property.

Bridge loans function a bit differently. Lenders usually restrict your combined LTV (accounting for both your old and new properties) to around 75% to 80%. The entire point of the bridge loan is to extract the tied-up equity from your current, unsold house and directly deploy it as the down payment for your fresh purchase.

Repayment

How you pay the money back is a crucial distinction. During a HELOC's initial draw period, you usually only have to make interest-only payments. This keeps your out-of-pocket costs remarkably low while you're actively using the funds. Only after the repayment phase kicks in do you start amortizing the principal.

Bridge loans offer a different kind of relief. Many are structured so that you make zero monthly payments while the loan is active. Instead, the interest accrues, and you settle the entire balance---principal plus interest---in one massive balloon payment the exact moment your old home finally sells and closes.

Best for

Who actually benefits from these tools? I've found that a HELOC is best for the methodical planner. If you want a revolving emergency fund, plan to renovate your kitchen in stages over the next year, or want a long-term credit backstop without touching your primary low-rate mortgage, this is your winner.

A bridge loan is strictly for the aggressive mover. If you've stumbled upon your absolute dream home, your current house is already listed but hasn't closed, and you only need cash for a few months to make the transition seamless, a bridge loan is the right weapon of choice.

Risk

Neither option is bulletproof. The hidden danger of a HELOC lies in its variable rate. I've watched borrowers get squeezed when macroeconomic conditions shift and their monthly interest payments skyrocket over a 10-year span. Plus, your house is on the line. Default, and you face foreclosure.

With a bridge loan, the risk is pure timing. What happens if the housing market suddenly cools in 2026 and your old house sits empty for nine months? If that balloon payment comes due and you haven't sold the property, you're stuck carrying three massive loans at once, which can financially ruin an unprepared buyer.

Which One to Choose? Take a Look Here

Making the final call really comes down to your timeline and end goal. I always break it down into these simple scenarios for my clients:

- Choose a HELOC if: You aren't in a rush to move. You want flexible access to cash for ongoing home renovations, debt consolidation, or simply desire a reliable, long-term credit buffer. The lower interest rates make sense for money you'll carry for years.

- Choose a Bridge loan if: You are actively in the real estate trenches. You found a home you must buy right now, but your current house hasn't officially sold. You don't mind paying higher fees for a few months just to secure a competitive, contingency-free offer.

Don't let the pressure dictate your choice. Match the loan to your exact life stage.

FAQs About Bridge Loan vs HELOC

Q1. How much would a $50,000 HELOC cost per month?

At the 2026 average HELOC rate of 7.18%, an interest-only payment on a fully drawn $50,000 line costs roughly $299 per month. If your lender requires principal and interest repayment immediately, expect that monthly bill to be significantly higher, depending on your exact term length.

Q2. Why would someone want a bridge loan?

Homeowners want a bridge loan to unlock the equity in their current house before selling it. This allows them to make a strong, non-contingent cash down payment on a new home, completely avoiding the stress of missing out on a property while waiting for their old house to close.

Q3. Do wealthy people use HELOCs?

Absolutely. Wealthy individuals frequently use HELOCs as a strategic liquidity tool. Instead of liquidating high-performing stock portfolios and triggering massive capital gains taxes, they tap their home equity at a relatively low interest rate to fund business ventures, real estate investments, or large unexpected expenses.

Q4. What is a better alternative to a HELOC?

If you despise variable interest rates, a Home Equity Loan is your best alternative. It provides a lump sum of cash with a locked-in, fixed rate. Alternatively, if current 2026 mortgage rates are lower than your existing mortgage, a cash-out refinance might make more financial sense.

Q5. Are banks restricting HELOCs in 2026?

While banks aren't completely stopping HELOCs in 2026, they have tightened their underwriting standards. Lenders are strictly enforcing 80% to 85% LTV limits and closely scrutinizing Debt-to-Income ratios. However, you can still easily secure one through competitive online lenders or local credit unions if your credit is strong.

Q6. Who offers bridge loans?

While massive traditional banks sometimes shy away from them, you can easily find bridge loans through local credit unions, specialized mortgage brokers, and private "hard money" lenders. Connecting with a platform like Bluerate can quickly match you with the right local providers offering these short-term products.

Conclusion

In short, a HELOC is your long-term, flexible wallet tapped into your home equity, while a bridge loan is your fast, short-term stepping stone between two properties. Both provide serious financial leverage, but they cater to entirely different seasons of homeownership.

Here is a quick recap:

- HELOC: Best for ongoing renovations and long-term borrowing with lower, variable rates.

- Bridge Loan: Best for buying a new house before selling your old one, offering fast cash at a higher premium.

Applying blindly can severely ding your credit score. Head over to Bluerate AI for a free consultation today. Their local loan officers will assess your exact equity and deliver a customized, money-saving strategy tailored specifically for the 2026 market!

People Also Read

- [Must-Read] How Does a HELOC Work? Explore Process Here

- [Solved] How to Calculate HELOC Payment? Easy-to-Understand

- Best Bridge Loan Lenders for Homebuyers and Investors

- [Detailed Guide] How to Estimate Mortgage Refinance? Start Now

- Cash-out Refinance vs HELOC: All Differences to Learn

- HELOC vs Second Mortgage: Is a HELOC a Second Mortgage?