Mortgage APR Explained: What Is It & Fees Included

When I bought my first house, the Loan Estimate completely threw me off. My eyes kept bouncing between the interest rate and the Annual Percentage Rate (APR). Why were they different? And which one actually decided my monthly bill? If you're staring at your paperwork feeling just as lost, don't worry. Let's break down exactly what mortgage APR means so you can spot hidden fees.

Key Takeaways

-

APR (Annual Percentage Rate) shows your total cost of borrowing. It mixes your base rate with lender fees.

-

While the interest rate sets your monthly payment, the APR gives you the big picture of your loan's price tag.

-

Always use APR to compare similar loan offers (same type and term), as it provides a more complete picture of costs under those conditions.

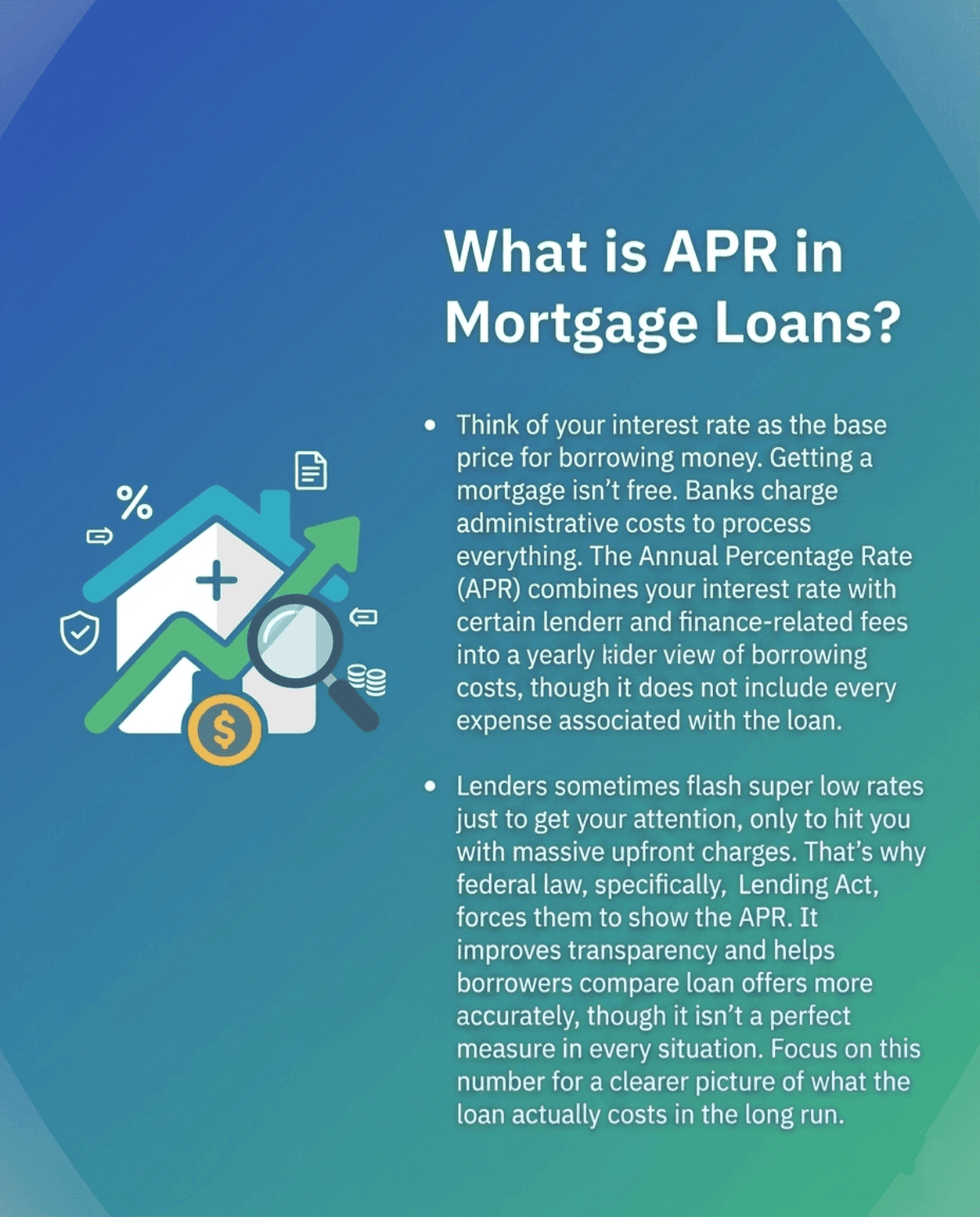

What is APR in Mortgage Loans?

Think of your interest rate as the base price for borrowing money. But getting a mortgage isn't free. Banks charge administrative costs to process everything. The Annual Percentage Rate (APR) combines your interest rate with certain lender and finance-related fees into a yearly percentag. It gives a broader view of borrowing costs, but it does not include every expense associated with the loan.

I realized pretty fast that some lenders flash super low rates just to get your attention, only to hit you with massive upfront charges later. That's exactly why federal law, specifically the Truth in Lending Act, forces them to show the APR. It improves transparency and helps borrowers compare loan offers more accurately, though it isn't a perfect measure in every situation. By focusing on this number, you get a much clearer picture of what the loan actually costs you in the long run.

Key APR vs. Interest Rate Differences

Telling these two apart was definitely the most confusing part of mortgage shopping for me. Here is the easiest way I learned to separate them:

-

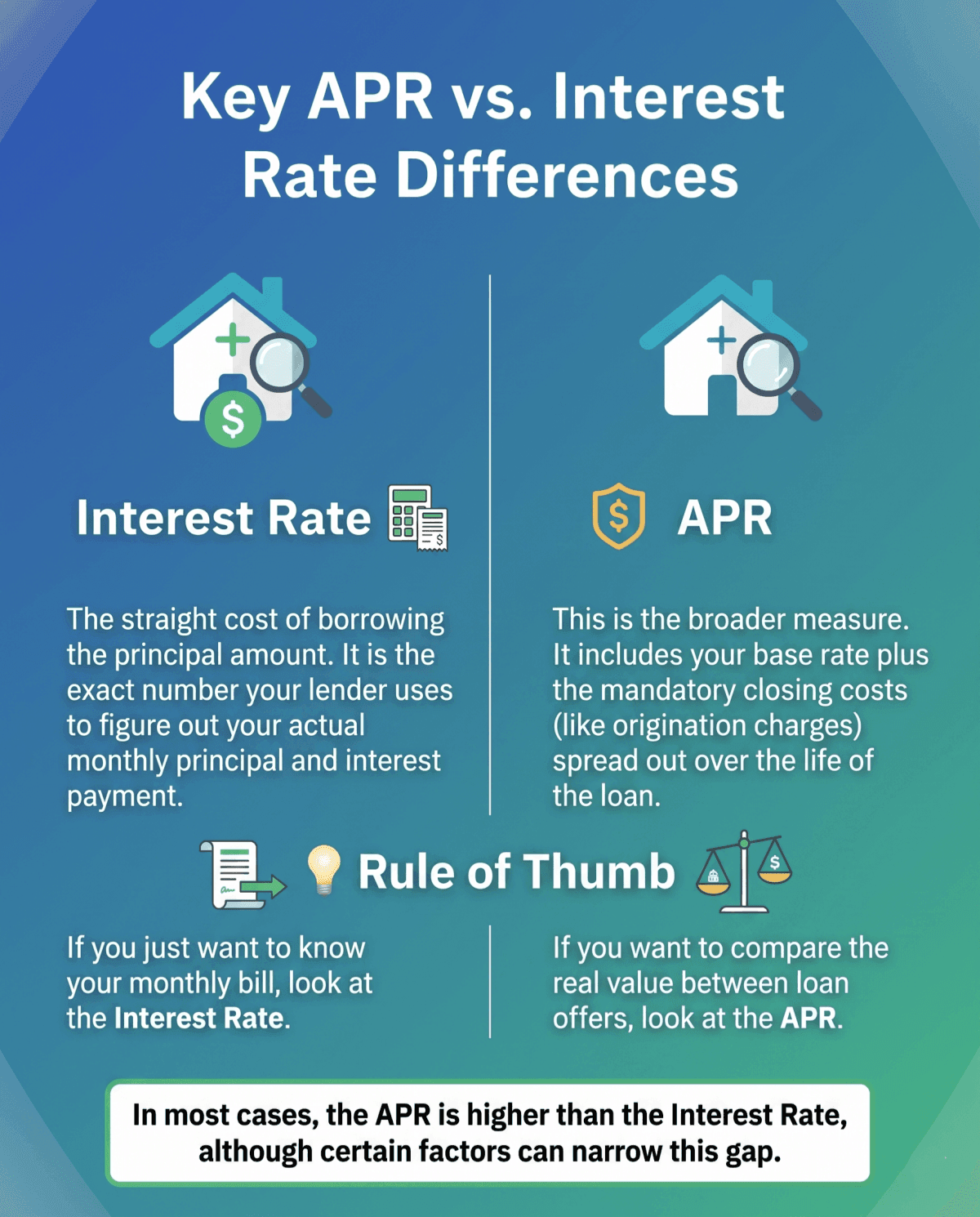

Interest Rate: This is the straight cost of borrowing the principal amount. It is the exact number your lender uses to figure out your actual monthly principal and interest payment.

-

APR: This is the broader measure. It includes your base rate plus the mandatory closing costs (like origination charges) spread out over the life of the loan.

Because it wraps in those extra fees, in most cases, the APR is higher than the interest rate, though certain loan structures or lender credits can narrow or occasionally reverse that gap. A good rule of thumb? If you just want to know your monthly bill, look at the rate. If you want to compare the real value between two different loan offers, look at the APR.

Also Read: Mortgage Interest Rate vs. APR: What's the Difference?

What Fees are Included in APR?

So, what exactly bumps up the APR? When you check your paperwork, specific closing costs are baked right into that number. Usually, it includes:

-

Origination fees: What the bank charges to put your loan together.

-

Discount points: The cash you pay upfront to buy down your rate.

-

Mortgage broker fees: Commissions for the middleman, if you used one.

-

Underwriting fees: The cost to verify your finances.

But knowing what isn't included is just as crucial. Some third-party costs, such as appraisal fees, title services, and notary fees, are typically not included in APR, though exact treatment can vary depending on how the fees are structured.

Figuring this out helped me see exactly where the bank was making a profit versus what were just standard third-party costs everyone has to pay.

Key Factors Influencing Your APR

Sure, the broader economy sets the stage for mortgage rates. But your personal financial situation largely determines the interest rate and fees you're offered, which in turn affect your APR. Here's what matters most:

-

Credit score: This is the biggest factor in your control. Borrowers with great credit (usually 740 and up) get lower APRs because banks see them as safe bets.

-

Down payment: Putting more money down lowers the lender's risk, which often means fewer fees and a better APR.

-

Loan term: A 15-year mortgage typically comes with a lower APR than a 30-year one.

-

Loan type: Fixed-rate loans stay the same, whereas ARMs change over time.

If your credit is a bit bumpy, lenders might charge higher origination points to cover their risk. That directly drives your APR up.

What is a Good APR Rate for a Mortgage?

Honestly, there isn't a magic "good" number because the market shifts constantly. A solid rate really just depends on the current economic climate. For example, Freddie Mac regularly publishes the national average interest rate for 30-year fixed mortgages. You can use this as a general benchmark, though it reflects interest rates rather than APR.

So, a good APR is simply one that matches or beats that current national average for someone with your credit score, without forcing you to pay crazy upfront fees. I always check Freddie Mac's weekly data to see if my offers are fair.

How to Ensure You Get a Good APR?

Landing the best deal definitely takes a little hustle. From my own house-hunting experience, these steps move the needle the most:

-

Shop around: Never take the first offer. Apply with at least three lenders and compare their Loan Estimates side-by-side.

-

Clean up your credit: A few months before buying, aggressively pay down credit card balances. Lowering your debt utilization boosts your score fast.

-

Negotiate fees: You can absolutely ask a lender to drop certain underwriting or origination fees.

When you shop around, banks know they have to compete for you. If they see you comparing offers from different places, they'll often slash their junk fees just to win your business. That's the easiest way to drop your APR.

Bonus Tip: Try Bluerate to Compare Nearby Loan Officers with Ease.

FAQs About Annual Percentage Rate

Q1. Is 7% APR too high?

It really depends on current market conditions and your credit history. While 7% feels steep compared to the weirdly low rates a few years ago, it's actually pretty normal historically. If the current national average is around 6.4%, a 7% APR just means you might have a lower credit score.

Q2. Is 4.5% a good mortgage rate?

It sounds amazing right now, but be careful. Banks don't hand out rates that far below the market average without charging hefty discount points. Always look at the APR. If the rate is 4.5% but the APR is 6%, you're getting slammed with hidden upfront costs.

Q3. Why is my APR higher than my interest rate?

Your APR will almost always be higher because it factors in the total cost of the loan. It takes your base interest rate and tacks on mandatory closing costs, like origination fees and points, spreading them out as a yearly percentage over your mortgage term.

Q4. Do I use APR or interest rate to calculate my monthly payment?

Always use the interest rate to figure out your monthly principal and interest payment. The interest rate determines your monthly principal and interest payment, while the APR reflects total borrowing costs and is mainly used for comparison.

Also Read:

Q5. Does a lower APR always mean a better deal?

Surprisingly, no. If you plan to sell or refinance in just a few years, a loan with a slightly higher rate but lower upfront fees might actually save you cash. You won't live there long enough for those expensive upfront points (which lower your APR) to pay off.

Conclusion

At the end of the day, the interest rate and APR work together to show you the real financial impact of your mortgage. My biggest piece of advice? Never look at the interest rate by itself. The APR is your best tool for uncovering hidden costs and figuring out who is actually giving you a fair deal.

So, grab a few Loan Estimates, compare those numbers side-by-side, and start shopping around to find the best possible mortgage for your new home.

Try Bluerate to Compare Nearby Loan Officers with Ease.