Mortgage Rate Lock Explained: Meaning, Strategies, Risk & FAQs

Navigating the home-buying process can feel overwhelming, especially when mortgage rates shift daily. In my experience, one of the best tools to protect yourself from these sudden spikes is a mortgage rate lock. Simply put, it secures your interest rate so it won't increase before you close on your new home.

It gives you the peace of mind to focus on moving rather than market panic. Navigating mortgage rates can be stressful, but you don't have to do it alone. Platforms like Bluerate connect you with expert loan officers for free consultations to help you navigate this successfully.

Key Takeaways

-

Protection, not gambling: A rate lock shields your monthly budget from unexpected market spikes before closing.

-

Standard timeline: Most lenders lock your rate for 30 to 60 days.

-

Float-down options exist: If rates drop significantly, a float-down provision lets you grab the lower rate.

-

Stability is required: Your lock can be voided if your income, credit score, or loan type changes.

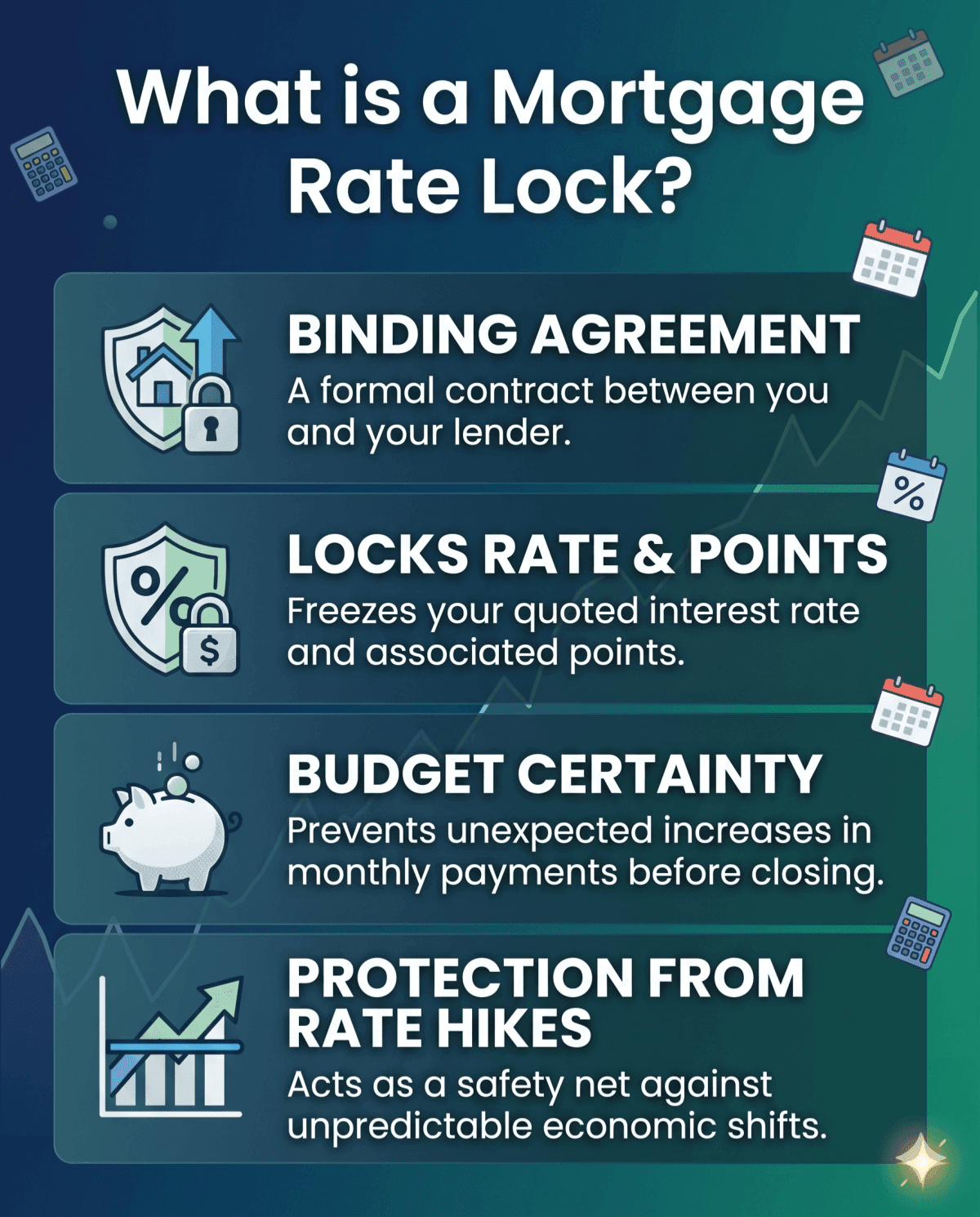

What is a Mortgage Rate Lock?

A mortgage rate lock is a binding agreement between you and your lender. It generally guarantees that the interest rate you are quoted will remain the same through closing, as long as there are no material changes to your application, loan terms, or property. When I talk to new buyers, I always emphasize that it's all about certainty. Once you lock, your expected monthly payment won't suddenly skyrocket right before closing.

Keep in mind that a lock doesn't just freeze the percentage rate. It also locks in the associated discount points. This means the costs directly tied to your interest rate, such as discount points, remain predictable, though other closing costs may still vary. Ultimately, this agreement gives you a safety net, ensuring your carefully planned homebuying budget won't blow up at the very last minute due to unpredictable economic shifts.

How Does a Mortgage Rate Lock Work?

Getting your rate locked isn't just a verbal handshake. It involves a formal process. Typically, you request a lock through your loan officer once you are under contract for a home. Here is how it usually unfolds:

-

Have an accepted offer: Many traditional lenders require a signed purchase agreement to initiate the lock, although some offer programs that allow you to lock before finding a home.

-

Get written confirmation: Never rely on a verbal promise. Always demand a formal rate lock agreement.

-

Check your Loan Estimate: This is a crucial step. Look at the very first page of your official Loan Estimate document. At the top right, there is a specific box labeled "Rate Lock." You must ensure this is clearly checked "Yes."

Once activated, the clock starts ticking until your scheduled closing day.

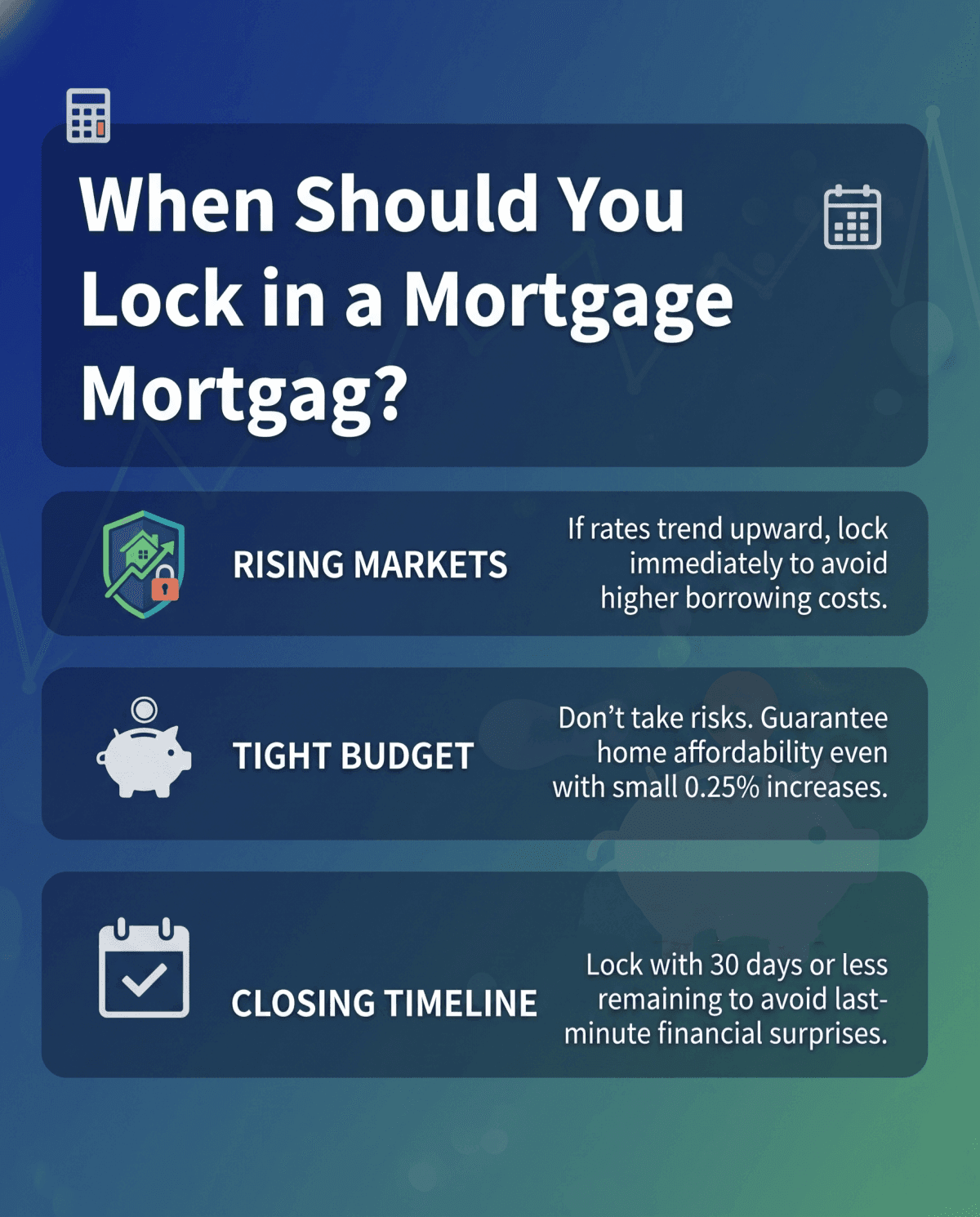

When Should You Lock in a Mortgage Rate?

Deciding exactly when to pull the trigger can be nerve-wracking. I always tell buyers that securing your personal financial safety is far more important than trying to outsmart Wall Street. Here are the scenarios where locking is your best move:

-

Rising Markets: If economic indicators suggest interest rates are trending upward, lock immediately to avoid higher borrowing costs.

-

Tight Budget: If even a tiny 0.25% increase would make your monthly mortgage payment unaffordable, don't take risks. Lock it in to guarantee your home remains within budget.

-

Closing Timeline: If you are fewer than 30 days away from closing, lock your rate. The closer you get to the finish line, the less you want to deal with last-minute financial surprises.

Also Read: When to Lock in a Mortgage Rate: A Loan Officer's Guide

Benefits and Risks of Locking a Mortgage Rate

While a rate lock sounds like a foolproof plan, it's important to weigh both sides objectively. Here is a breakdown of the benefits and potential downsides:

-

Benefits: The biggest advantage is absolute peace of mind. It prevents your monthly payments from increasing and allows you to budget with a high degree of certainty.

-

Risks: The primary drawback is the opportunity cost. If market rates suddenly plunge, you are stuck with your initial, higher rate. Additionally, if your home construction or closing process gets delayed beyond your lock period, you could face hefty extension fees. In worst-case scenarios, your lock might simply expire, forcing you to accept the current, potentially worse, market rate.

Understanding these pros and risks helps you navigate delays strategically.

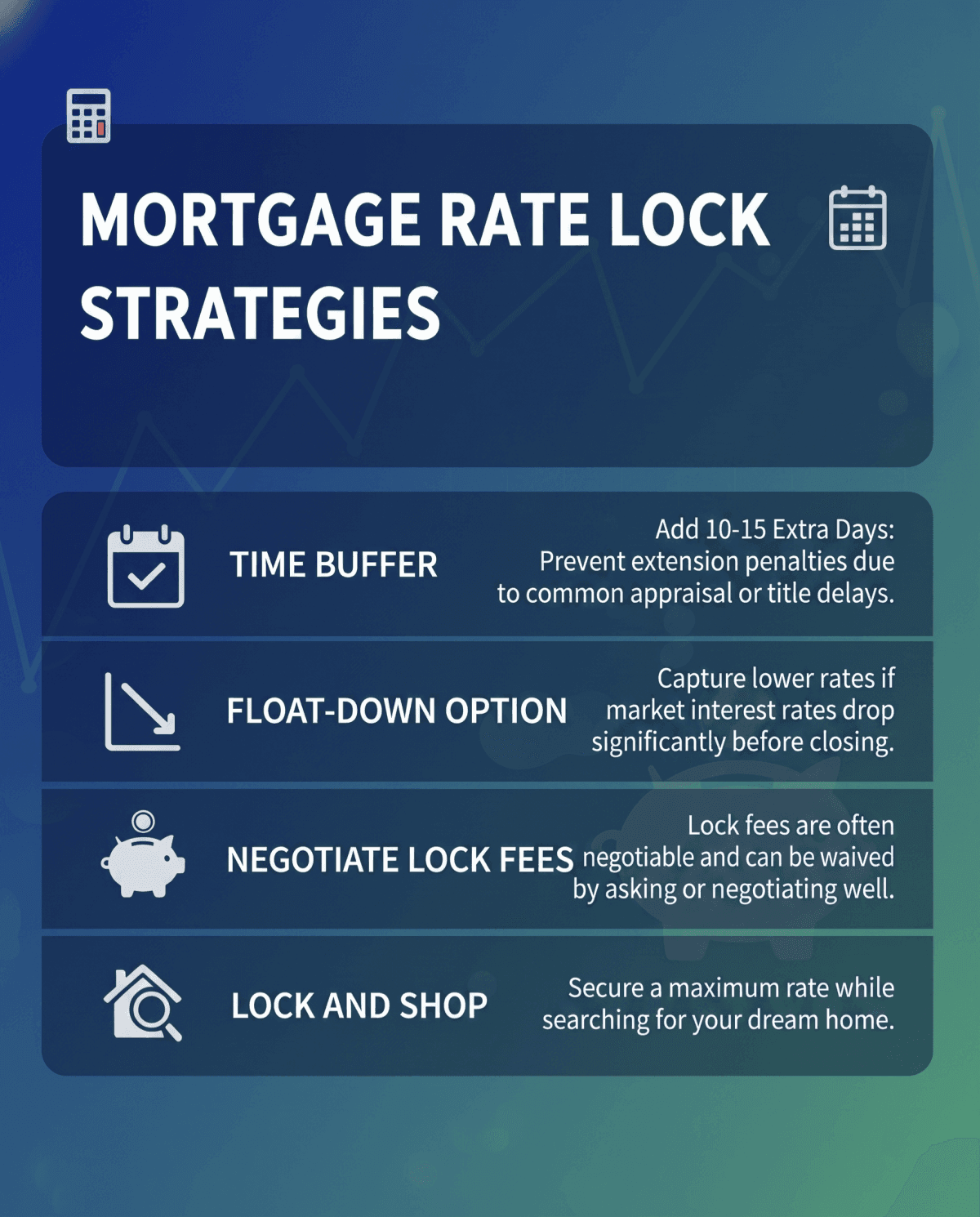

Mortgage Rate Lock Strategies

Over the years, I've learned that a smart rate lock requires a bit of strategy. Don't just blindly accept the first term offered. Here are some advanced techniques to protect your wallet:

-

Build in a time buffer: Always align your lock expiration with your closing date, but add an extra 10 to 15 days. Delays with appraisals or title work are incredibly common, and this buffer prevents expensive extension penalties.

-

Ask for a "Float-Down" option: This is a fantastic safety valve. If interest rates drop significantly before you close, a float-down allows you to capture the lower rate.

-

Negotiate lock fees: Many lenders will waive the upfront locking fee if you simply ask or negotiate well.

-

Utilize "Lock and Shop": If you haven't found a house yet but fear rising rates, look for lenders offering a "lock and shop" program. This secures a maximum rate while you hunt for your dream home.

How Long Can You Lock in a Mortgage Rate?

You can typically lock in a mortgage rate for 30, 45, or 60 days. However, if you are buying a new construction home, some lenders offer extended locks lasting anywhere from 120 to 360 days. Keep in mind that there is a direct correlation between time and cost: the longer your lock period, the more expensive the fees will generally be.

Can a Locked Mortgage Rate Change?

It is a common myth that a locked rate is absolutely set in stone. The truth is, your lock is entirely contingent on your financial stability. Your rate can still change, or the lock can be voided altogether, if your credit score drops, you switch from a 30-year to a 15-year loan, your verified income changes, or the home appraisal comes in low. Therefore, my biggest warning to buyers is this: never open new credit cards or finance a car right before closing!

FAQs About Mortgage Rate Lock

Q1. What is required to lock in a mortgage rate?

Generally, you must have a fully accepted purchase agreement outlining a specific property address. Additionally, you need to complete a formal loan application with your chosen lender. Once your credit, income, and down payment details are submitted, the lender can officially process the lock request.

Q2. What happens if I lock in a mortgage rate and the rate goes down?

If you don't have a specific float-down provision in your contract, you will typically need to proceed with the locked rate if you continue with that lender, unless your agreement includes a float-down option. Trying to abandon ship and switch lenders at the last minute can cause severe closing delays or breach of contract penalties.

Q3. How much does it cost to lock in a mortgage rate?

Many lenders market 30- to 60-day locks as "free," though the cost is usually baked into the interest rate itself. If a lender charges a separate upfront locking fee, it can vary widely by lender, sometimes around 0.25% to 1% of the loan amount, though in many cases the cost is built into the rate instead.

Q4. Can you lock a mortgage rate before finding a house?

Yes, you can use a "Lock and Shop" program. This specialized option allows house hunters to lock in an interest rate for 60 to 90 days while they actively search for a property, providing excellent protection in a rapidly rising rate environment.

Q5. What is a float-down provision?

A float-down provision is a special addendum to your lock agreement. If market interest rates drop significantly before your closing day, this feature allows you to lower your locked rate to the new, cheaper rate, usually for a small administrative fee.

Conclusion: Should I Lock My Mortgage Rate Today?

Ultimately, no one possesses a crystal ball to perfectly predict where the market is heading next. If the current interest rate allows you to comfortably afford your target monthly mortgage payment, locking it in is always a remarkably smart move. It transforms anxiety into certainty, allowing you to enjoy the home-buying journey.

Ready to explore your options or need advice on current rates? Visit Bluerate to connect with professional loan officers for a free consultation and secure the best rate for your dream home.