How to Become a Mortgage Underwriter with No Experience?

When I first looked into the mortgage industry, breaking in with zero experience felt nearly impossible. If you are trying to kickstart your career but keep hitting the "experience required" wall, you are not alone. Luckily, mortgage underwriting does not necessarily require a finance degree. I discovered that with a targeted approach, basic training, and modern software, anyone can learn to spot risks and approve loans from scratch.

Key Takeaways

-

Start in entry-level processing roles to build baseline industry knowledge.

-

Master core agency guidelines like Fannie Mae and Freddie Mac.

-

Leverage modern AI tools to streamline income calculation and policy verification.

-

Obtain a respected certification to show employers you are serious.

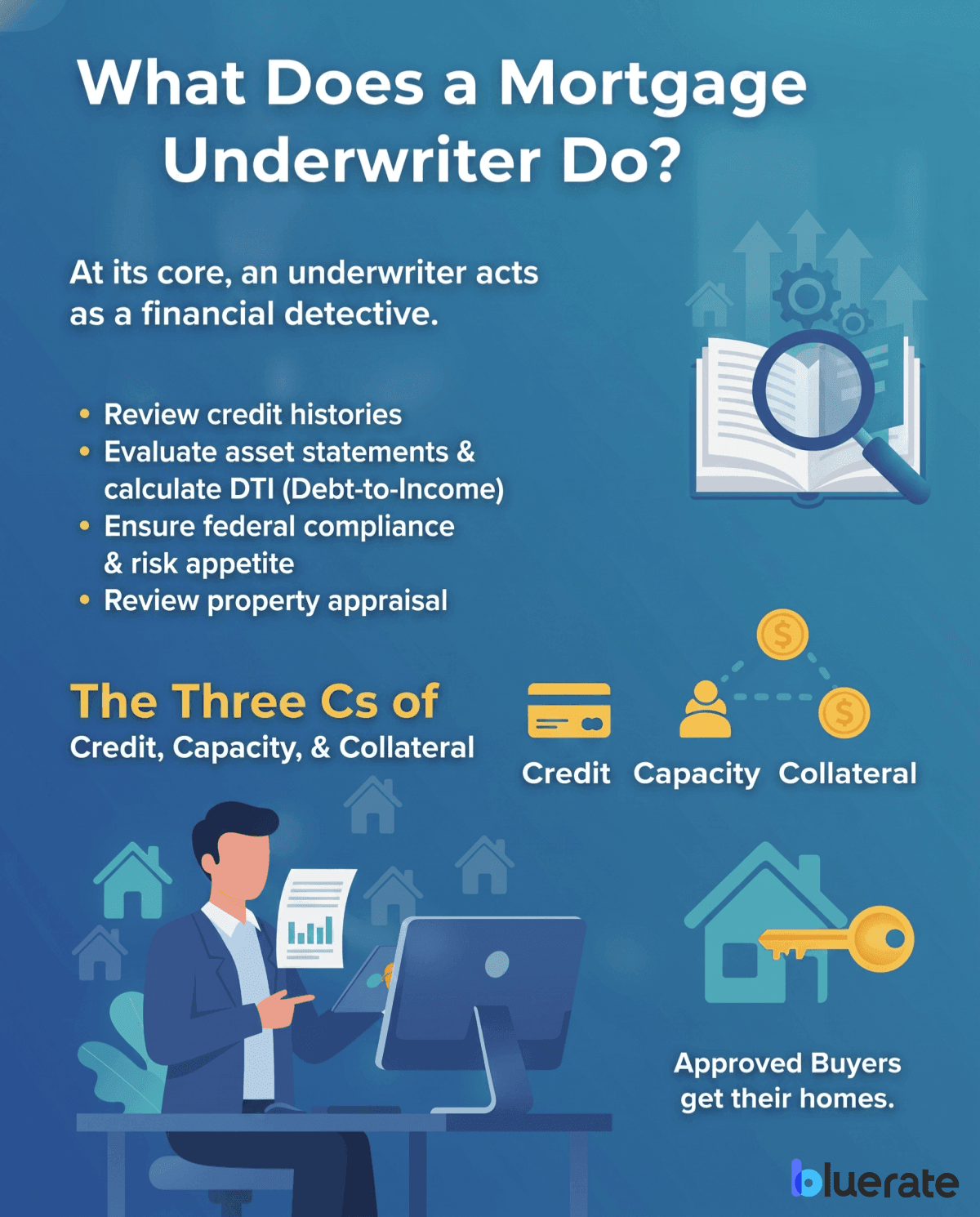

What Does a Mortgage Underwriter Do?

Before mapping out your journey, it helps to understand what the day-to-day work actually involves. A mortgage underwriter acts as a financial detective. You are the one who analyzes a home loan application to decide whether a bank should approve or deny the request.

Here is what my typical daily task list looks like:

-

Reviewing credit histories to assess the borrower's reliability.

-

Evaluating asset statements and calculating debt-to-income (DTI) ratios.

-

Ensuring the loan profile strictly matches federal regulations and institutional risk appetites.

-

Reviewing the property's appraisal to confirm it supports the loan as collateral.

Essentially, you are evaluating the three Cs of underwriting: credit, capacity, and collateral. It is about analyzing data to protect the lender from costly defaults while helping qualified buyers get their keys.

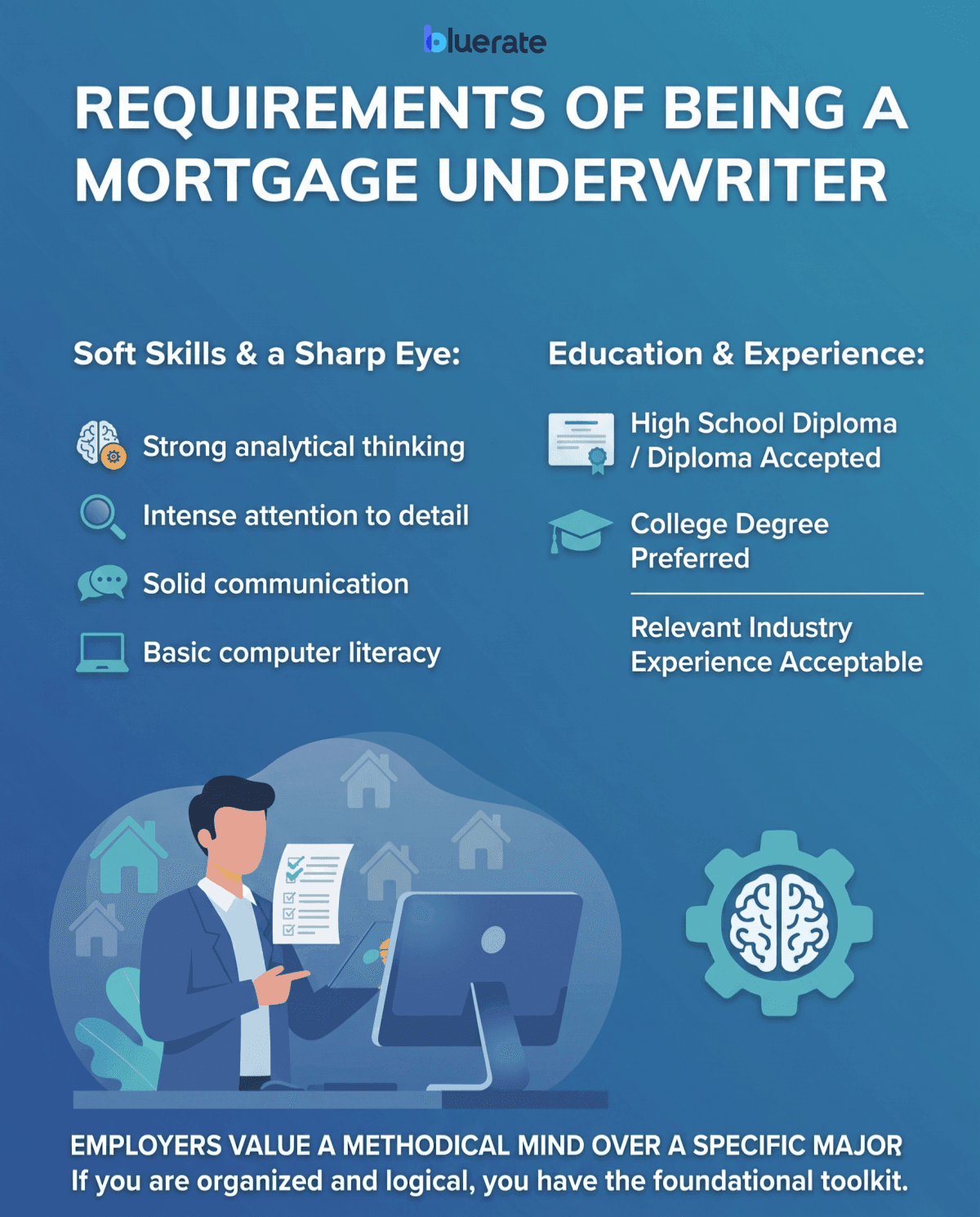

Requirements of Being a Mortgage Underwriter

You might think you need a master's degree in economics, but the actual requirements are much more practical. Some employers may accept a high school diploma, though many prefer a college degree or relevant industry experience.

The real qualifiers for this job are soft skills and a sharp eye:

-

Strong analytical thinking: You need to spot inconsistencies in massive files.

-

Intense attention to detail: Missing a single line on a tax return can ruin a deal.

-

Solid communication: You must explain complex financial decisions clearly to loan processors.

-

Basic computer literacy: Navigating digital systems is non-negotiable.

Employers value a methodical mind over a specific major. If you are organized and logical, you already possess the foundational toolkit.

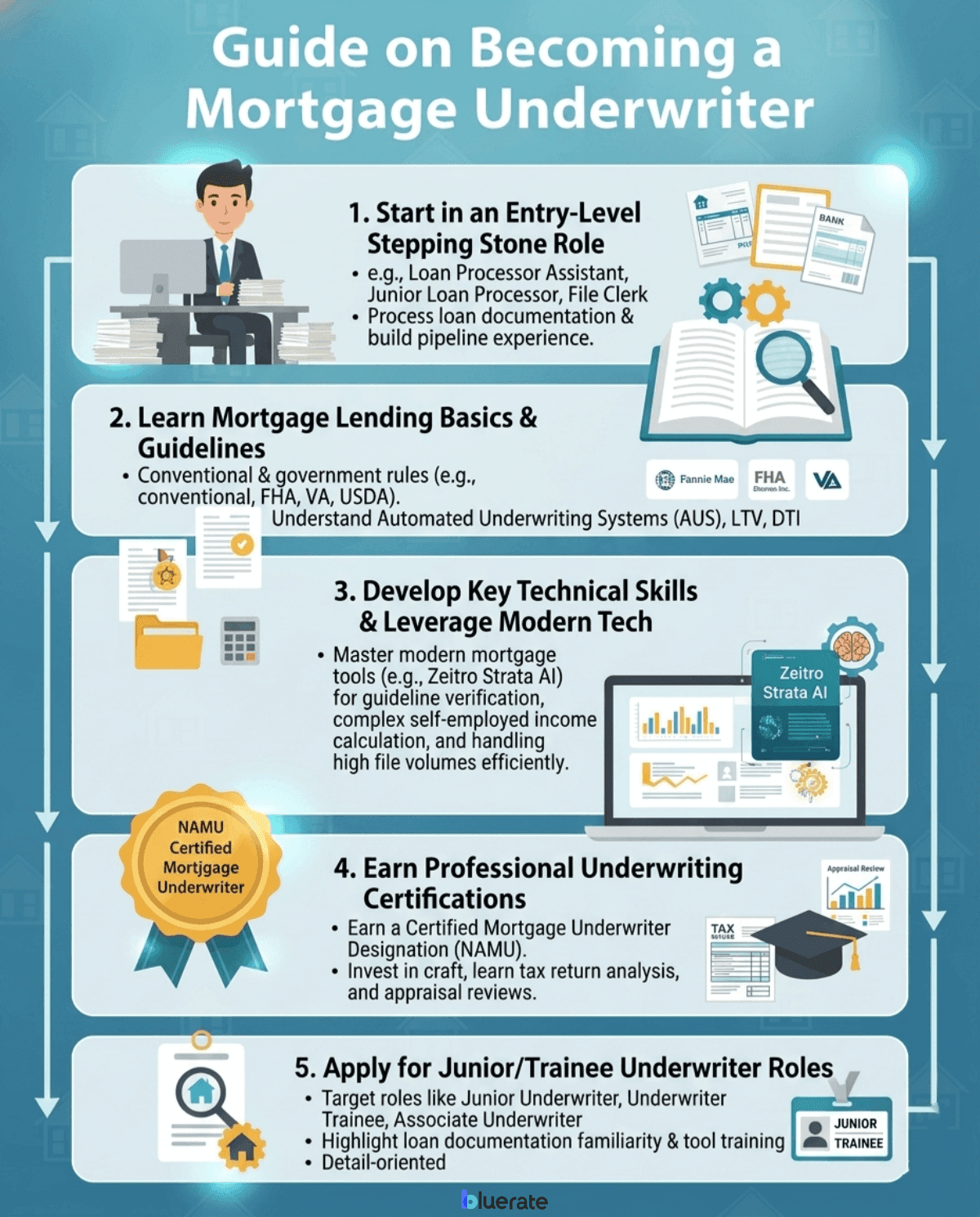

Guide on Becoming a Mortgage Underwriter

Breaking into the field is a structured process. Based on my industry observation, here is the exact step-by-step roadmap to transition from a total beginner into a competent, hired mortgage underwriter.

1. Start in an Entry-Level Stepping Stone Role

No one becomes a lead underwriter overnight. The best strategy is to secure a supporting position to learn how files move. I highly recommend applying for roles like loan processor assistant, junior loan processor, or mortgage file clerk. These entry-level positions expose you to the exact same documents underwriters review daily, such as paystubs, bank statements, and tax transcripts.

By processing files, you learn what a clean application looks like and get comfortable with the mortgage pipeline. It is the absolute best way to get paid while building the real-world experience employers demand. Plus, companies love promoting internal processors to underwriting trainees.

2. Learn Mortgage Lending Basics

While working in a support role, you must actively study the rules of the game. Our industry relies on massive rulebooks set by government-sponsored enterprises. You need to familiarize yourself with conventional guidelines from Fannie Mae and Freddie Mac, as well as government programs like FHA, VA, and USDA. Do not worry about memorizing every page—no one does that.

Instead, focus on understanding how automated underwriting systems work. Learn how loan-to-value and debt-to-income ratios affect eligibility. Knowing where to find these rules and understanding how to interpret them is what separates a great rookie from a struggling candidate.

3. Develop Key Technical Skills

Modern underwriting is highly digital. You do not have to struggle manually with endless guidelines or calculate complicated income sheets on scratch paper anymore. To stand out, you should get comfortable with modern mortgage tools. For instance, I highly recommend using Zeitro Strata AI in your study or daily workflow.

This smart assistant helps you quickly verify guidelines across programs, calculate complex self-employed income, and instantly check down payment assistance program eligibility. It can also verify income qualifications without you having to drown in endless PDFs. Mastering tech like this proves to hiring managers that you can handle high file volumes efficiently, making up for your lack of years on the job.

4. Earn Professional Certifications

When you have no hands-on underwriter experience, a professional credential acts as your seal of approval. I suggest looking into programs offered by the National Association of Mortgage Underwriters, widely known as NAMU. Earning their Certified Mortgage Underwriter designation shows hiring managers you have invested time to learn the craft. These courses cover real-world scenarios, tax return analysis, and appraisal reviews.

Later in your career, you can pursue FHA or VA-related underwriting training and authorization, depending on employer requirements and program rules.. For a beginner, though, starting with a basic NAMU certification is a brilliant way to make your resume stand out in a stack of applicants.

5. Apply for Junior/Trainee Underwriter Roles

Once you have a baseline of processing experience and a certification, it is time to hunt for jobs. Do not search for "senior underwriter" roles just yet. Instead, look for titles like Junior Underwriter, Underwriter Trainee, or Associate Underwriter. When writing your resume, highlight your familiarity with loan documentation and mention any training with digital tools.

Emphasize your detail-oriented nature and analytical skills. During interviews, talk about your understanding of risk management and guidelines rather than your lack of experience. Show them that you are ready to learn and that you know how to leverage tools to make safe, accurate lending decisions.

How Much Do Mortgage Underwriters Make?

Even at the entry level, this career path is financially rewarding. According to recent data from Indeed, junior mortgage underwriters in the United States earn an average base salary of around $66,195 per year. As you gain experience, that number rises.

Glassdoor reports total compensation averages closer to $94,000 when bonuses are included. With more experience and senior responsibilities, some underwriters can reach six-figure compensation, depending on employer, market, and location.

Also Read:

- How Much Does a Mortgage Underwriter Make? Salary Here

- Best AI Mortgage Underwriter Software to Pick

FAQs About Becoming a Mortgage Underwriter

Q1. Is it hard to become an underwriter?

It can be challenging because there is a lot of regulatory information to learn. However, it is entirely manageable if you take it step-by-step. Starting as a loan processor and using modern lookup tools makes the learning curve far less intimidating than trying to memorize everything at once.

Q2. Do mortgage underwriters make good money?

Yes, they do. The compensation is excellent compared to many other professions that do not strictly require a college degree. Mid-level underwriters comfortably earn above-average salaries, and top-tier senior professionals often exceed $100,000 annually, especially when handling high loan volumes or earning specialized government certifications.

Q3. Is mortgage underwriting a lot of math?

You do not need advanced calculus, but you do need solid basic math and comfort with ratios, percentages, and income calculations. The daily math is limited to basic arithmetic, like percentages and division, to calculate debt-to-income ratios or monthly income. Having strong analytical logic and good reading comprehension is actually much more important than being a math genius in this role.

Q4. What is the cost of mortgage Underwriter certifications?

Individual training classes generally range from $100 to $400. For comprehensive preparation, a complete package like the official underwriter bootcamps offered by organizations like CampusMortgage and NAMU usually costs around $995. Given the massive career boost it provides to a beginner, it is a very reasonable investment in your future.

Conclusion

Transitioning into mortgage underwriting without prior experience is a realistic goal if you have a clear plan. By starting in a support role like processing, you gain the hands-on exposure that employers look for. Combining that experience with formal training, a NAMU certification, and modern efficiency tools like Zeitro Strata AI will quickly bridge the gap between you and seasoned professionals.

This career offers fantastic financial stability, a steady work environment, and room to grow. Take it one step at a time, build your foundational knowledge, and you will find yourself approving loans before you know it. The first step is simply getting your foot in the door.