![[Explained] What is a Float Down Option on Mortgage?](/_next/image?url=https%3A%2F%2Fdynamic-light-ab6e2536d6.media.strapiapp.com%2Ffloat_down_option_banner_1efd5e82b5.png&w=3840&q=75)

[Explained] What is a Float Down Option on Mortgage?

I remember helping a client panic over rising interest rates just weeks before closing. It's a terrifying spot for any homebuyer. You want to lock your rate to avoid paying more, but what if rates suddenly drop? That's exactly where a float-down option comes in handy.

Before making a move, I always tell folks to consult local loan officers (LOs). Local loan officers can provide more tailored guidance based on your market and loan program, but their advice is not always better than online resources. Consultation fees and policies vary by lender.

Key Takeaways

-

A float-down option lets you lock a mortgage rate while retaining the chance to snag a lower one if the market dips.

-

It guarantees you won't pay more, but you still have a ticket to pay less.

-

Be prepared for upfront costs, usually 0.25% to 1% of the loan amount.

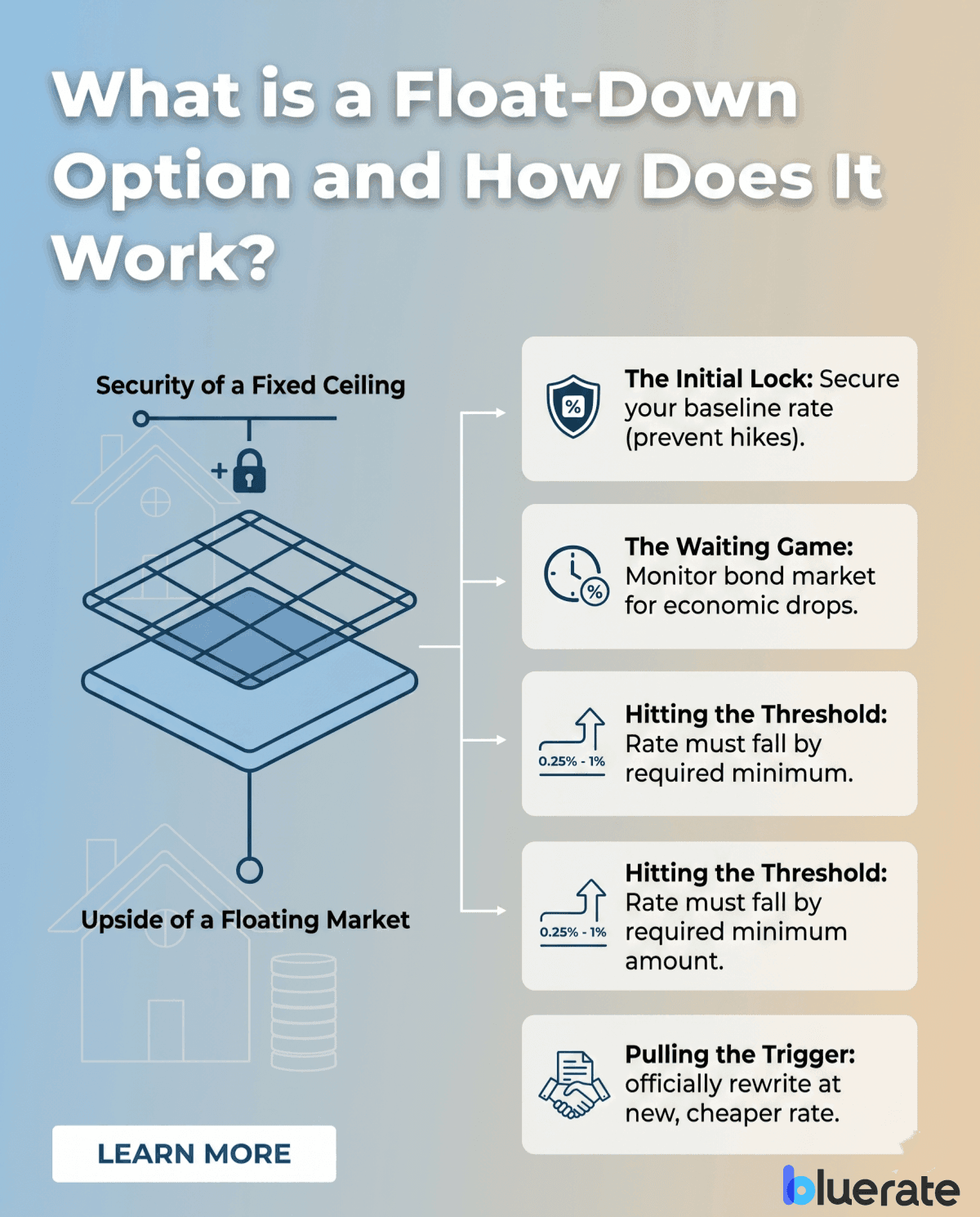

What is a Float-Down Option and How Does It Work?

A mortgage float-down option is an add-on to a standard rate lock that may let you lower your interest rate before closing if market rates fall, subject to the lender's terms. Think of it as a double-layered safety net: you get the security of a fixed ceiling, plus the upside of a floating market.

Here is exactly how the process unfolds behind the scenes:

-

The Initial Lock: You secure your baseline rate to prevent any unexpected hikes during escrow.

-

The Waiting Game: We monitor the bond market together. You're simply waiting to see if economic conditions push rates lower.

-

Hitting the Threshold: Lenders won't let you adjust for a microscopic dip. In many cases, the rate must fall by at least 0.25% to 1%, though some lenders may use different thresholds.

-

Pulling the Trigger: Once we hit that required drop, you officially ask the lender to rewrite the paperwork at the new, cheaper rate.

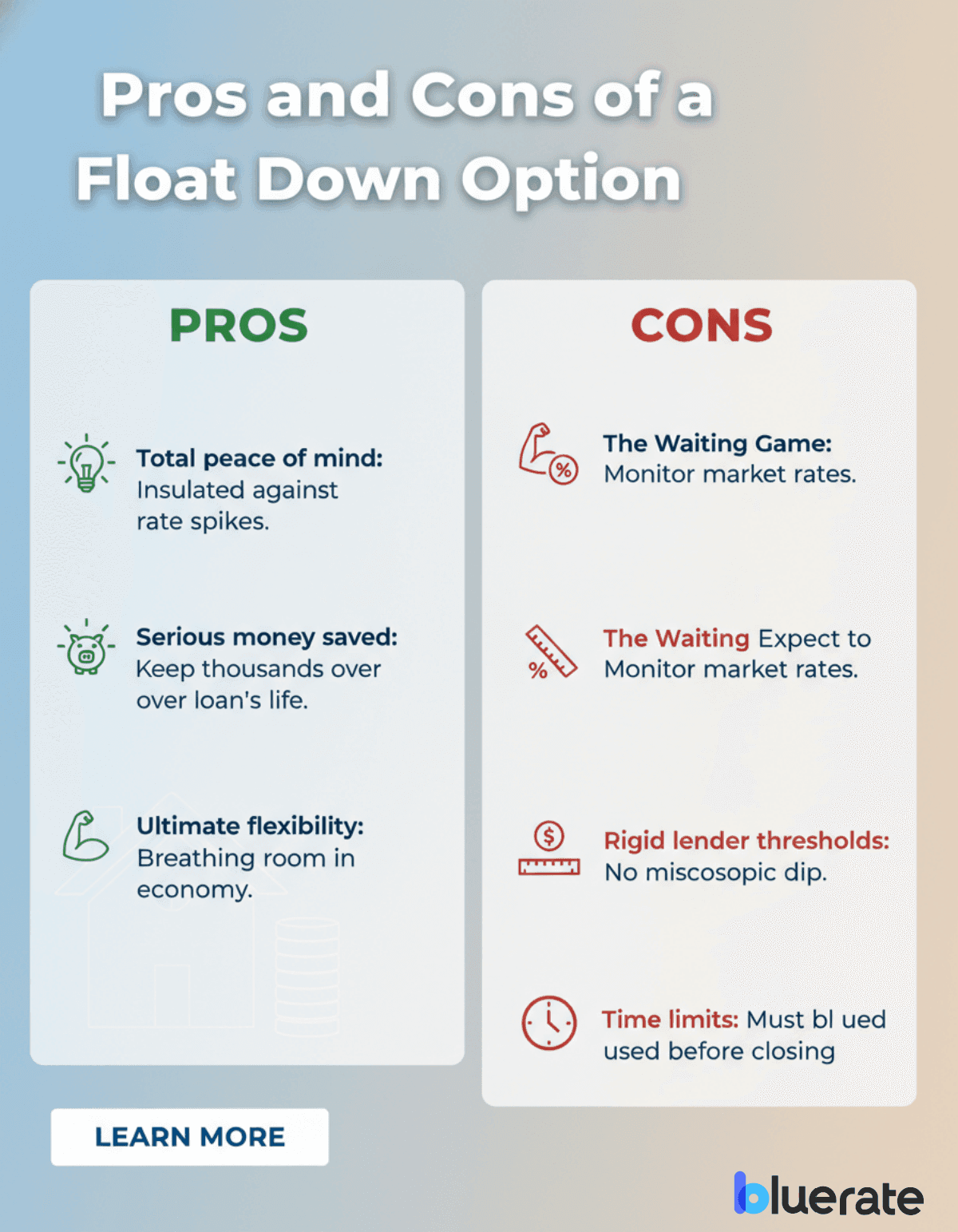

Pros and Cons of a Float Down Option

Like any financial tool, you have to weigh the good against the bad. I always urge buyers to look past the excitement of a potential rate cut and read the fine print.

Pros:

-

Total peace of mind: You are fully insulated against sudden rate spikes.

-

Serious money saved: Catching a downward trend means thousands kept in your pocket over the loan's lifespan.

-

Ultimate flexibility: It gives you breathing room in an otherwise unpredictable economy.

Cons:

-

Upfront costs: This insurance isn't usually free. Expect to pay a premium.

-

Rigid lender thresholds: If rates only drop 0.10% and your contract requires a 0.25% dip, you get nothing.

-

Time limits: The exercise window varies by lender, and in many cases the option must be used before closing and within the active lock period. If rates crash the week of your signing, you might be out of luck.

Float Down Option Example

Let's look at Sarah, a buyer I recently worked with. She locked a $400,000 mortgage at 7.0%. To be safe, she paid a 0.5% float-down fee, costing her $2,000 upfront. A month later, the Federal Reserve released new data, and market rates tumbled to 6.5%.

Because this easily beat her lender's 0.25% minimum drop rule, she exercised her option. Her new rate became 6.5%. That half-percentage-point difference lowered her monthly principal-and-interest payment by roughly $100 to $130, depending on loan terms. In this example, she could recoup the fee in roughly 16 months, depending on the exact loan terms. After that, it was pure long-term savings for three decades.

How Much Does a Float Down Cost?

Float-down pricing varies widely: some lenders charge a flat fee, while others charge a fraction of a point to 1% or more of the loan amount. So, on a $300,000 loan, the fee could range from $1,500 to $3,000 if the lender charges 0.5% to 1%. Some banks prefer charging a flat administrative fee instead. I also want to warn you about lenders advertising a "zero-cost" float down.

In my experience, there's no free lunch in real estate. They usually bake that cost directly into a slightly higher starting interest rate, or they make the required rate drop so steeply (like 0.5% or more) that you'll rarely get to use it.

Is It Better to Lock or Float a Mortgage?

Trying to time the mortgage market is notoriously difficult, even for Wall Street pros. Choosing your strategy really boils down to your personal risk tolerance and timeline.

When you should Lock:

-

The market is highly volatile or clearly trending upward.

-

Your budget is incredibly tight, meaning even a $50 monthly increase would ruin your finances.

-

You are less than 30 days away from your final closing date.

When you should Float (or buy the option):

-

Economic reports strongly hint that a rate cut is coming soon.

-

You are buying new construction or have a long escrow period (60+ days).

-

You have enough cash reserves to handle the upfront fee without stressing.

Also Read:

FAQs About Float Down Options

Q1. What is the typical timeframe for a float down option?

The timing window varies by lender, but the option is usually tied to the active lock period and often must be exercised before closing, giving the lender time to underwrite the new numbers.

Q2. How do I choose a lender with a float down option?

You really have to interview them. Ask specifically about their minimum rate drop requirement---is it 0.125% or a steep 0.5%? Compare their upfront fee percentages side-by-side, and clearly check if they cap how far down your new rate is allowed to go.

Q3. How does a float down option compare to locking in a rate?

A standard lock generally keeps your rate from changing during the lock period, as long as you close on time and your application does not change. A float-down is an offensive upgrade to that lock. It keeps the defensive ceiling intact but grants you a one-time permission slip to drop your rate if the market improves.

Q4. Do all lenders offer float-down options?

No, absolutely not. It's a specialty product. Not all lenders offer float-down options, so availability varies by institution. This is exactly why you need to shop around and ask upfront before committing.

Q5. How much does the rate have to drop to trigger a float-down?

Usually, the market rate must fall by at least 0.125% or 0.25% to trigger the clause. A tiny 0.05% wiggle won't cut it. Lenders enforce this threshold to ensure the rate adjustment is actually worth the administrative headache of re-doing your loan paperwork.

Final Word: Is Float Down Worth It?

So, should you pay for this feature? If you're facing an unpredictable market with a long closing timeline, it is absolutely worth considering. You're buying peace of mind with a built-in chance to save thousands. However, if your closing is next week or money is tight, skip it.

Because every mortgage scenario is drastically different, your next step should be calling a few local Loan Officers (LOs). Sit down with them, let them crunch your specific numbers, and see what makes sense.

Also Read: What are Mortgage Guidelines? How to Verify Accurately?