2026 Guide: How to Lock in a Mortgage Rate?

If you've been watching the US housing market lately, you already know 2026 has been quite a rollercoaster. With 30-year fixed rates fluctuating around the mid-6% mark, the fear of sudden spikes can easily keep you awake at night. I remember refreshing market charts daily during my own house hunt, terrified my monthly payment would suddenly become unaffordable.

That's exactly why understanding how to secure your borrowing costs is crucial right now. Let's walk through exactly how to lock in a mortgage rate, so you can stop stressing and start packing.

Key Takeaways

-

A mortgage rate lock guarantees your borrowing cost for a set period, protecting you from sudden market hikes.

-

Most lenders offer standard lock periods of 30, 45, or 60 days.

-

Always check if your lender includes a "float-down" option in case rates drop before you close.

-

Not sure about the timing? It's always smart to consult a loan officer for free to help you decide.

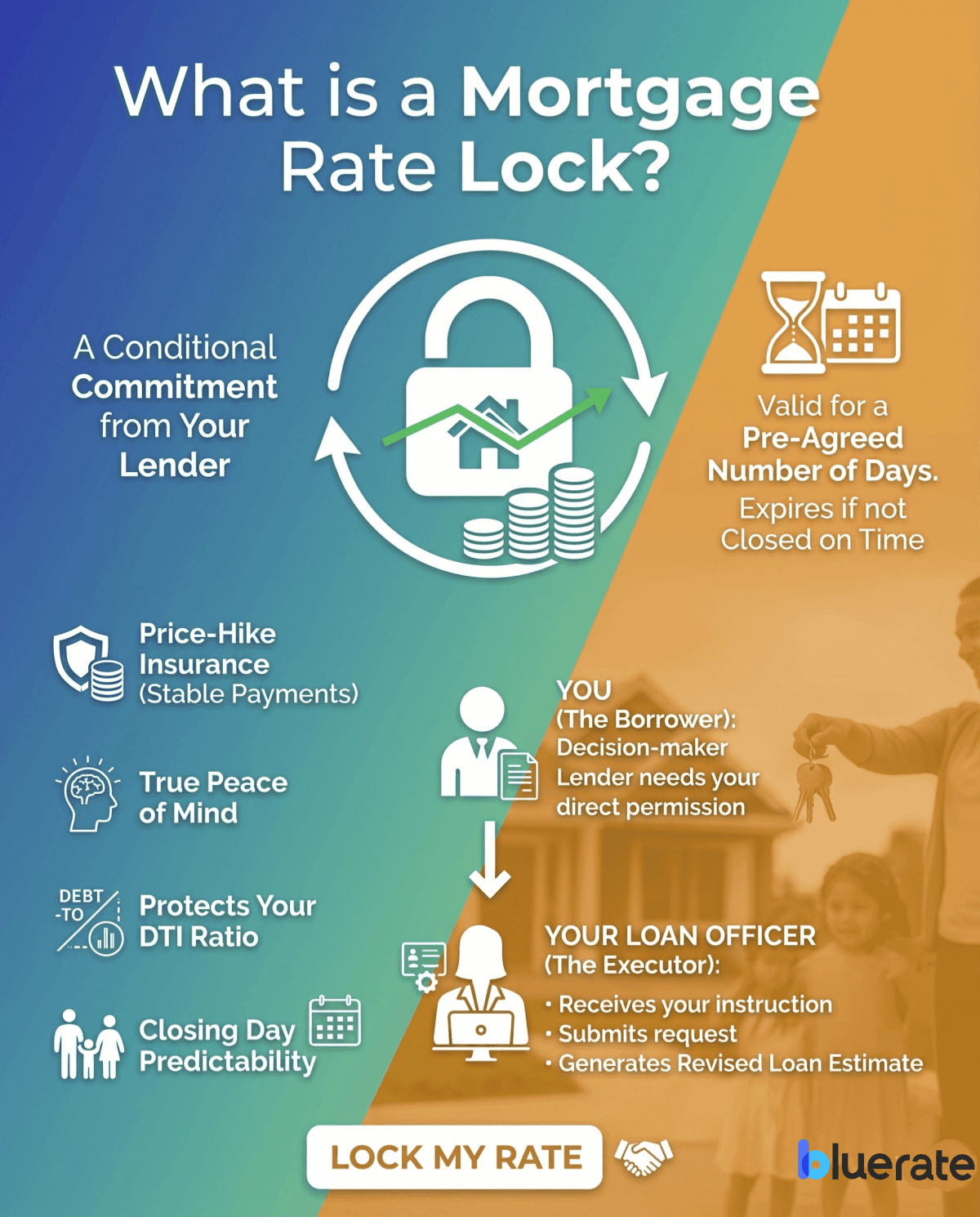

What is a Mortgage Rate Lock?

Think of a mortgage rate lock as price-hike insurance for your future home. Once triggered, it's a conditional commitment from your lender that your interest rate will not change during the lock period, as long as your loan details remain unchanged and you close on time for a specific time frame, even if national averages shoot up the next day.

This guarantee is an absolute lifesaver because it gives you true peace of mind. You'll know exactly what your monthly payments will look like, protecting your debt-to-income ratio right up until closing day. The whole point is predictability. Just keep in mind that this protection only lasts for a pre-agreed number of days. If you don't close the deal before the clock runs out, that locked-in number might expire.

Who is Responsible for Locking Your Mortgage Rate?

When it comes to pulling the trigger, it's a team effort, but the ultimate power rests in your hands.

-

You (The Borrower): You are the primary decision-maker. Your lender cannot arbitrarily freeze your rate without your direct permission. You dictate when to execute this step based on your comfort level.

-

Your Loan Officer (The Executor): Once you give the green light, your loan officer handles the backend work. They submit the formal request into their system and generate a revised Loan Estimate. This document serves as a formal confirmation of your locked terms, though the final legally binding agreement is established at closing.

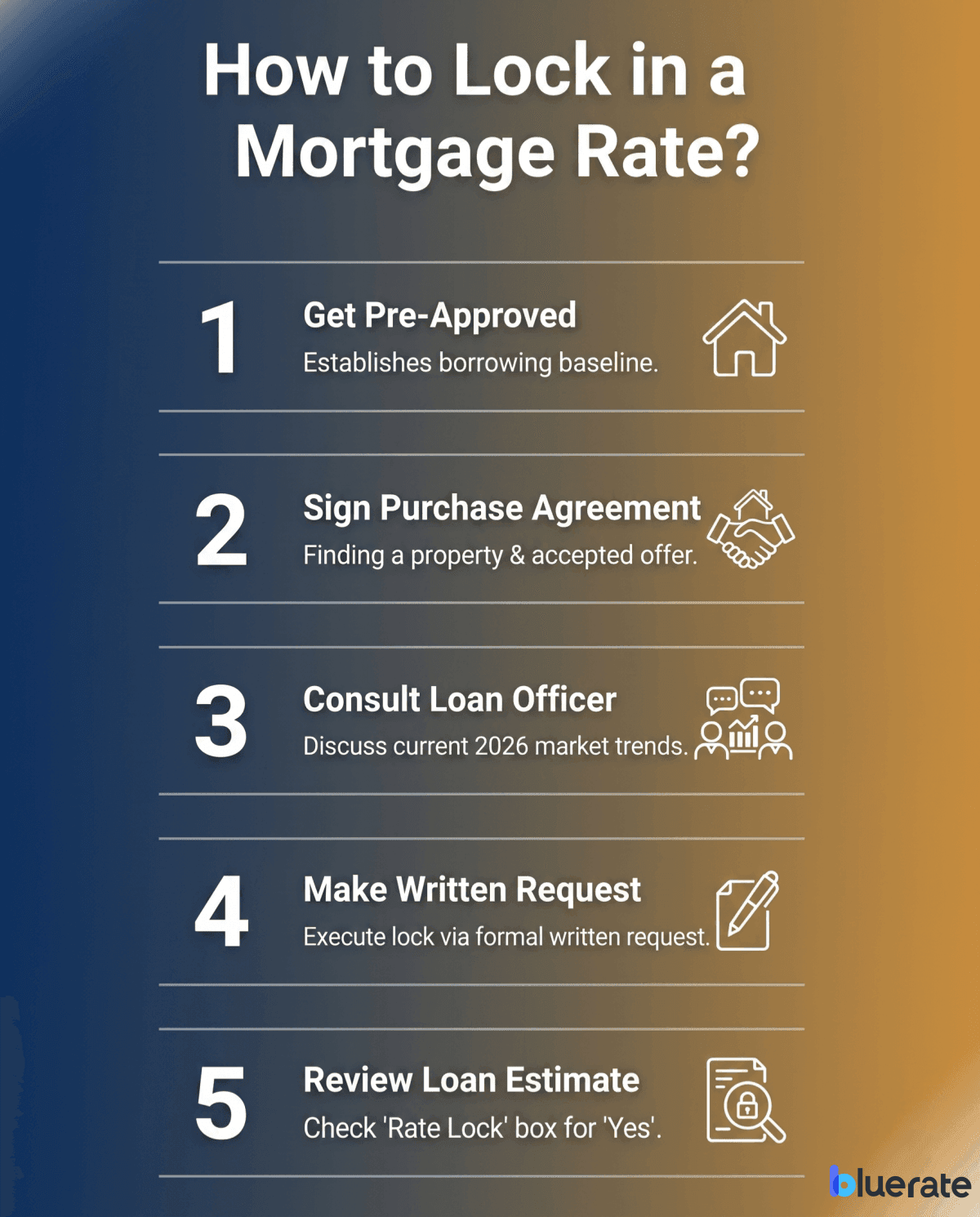

How to Lock in a Mortgage Rate?

Securing your rate happens right in the middle of the loan origination process. You don't just click a button online. It requires a few sequential steps:

-

Get pre-approved: This establishes your borrowing baseline, though you usually can't secure a firm rate yet.

-

Sign a purchase agreement: Finding a property and getting an accepted offer is the standard green light. Lenders need an actual address and closing date to finalize the timeline.

-

Consult your loan officer: Discuss current 2026 market trends to decide if you should lock immediately or float for a few days.

-

Make a written request: Verbally agreeing isn't enough. Ask your lender to execute the lock.

-

Review your Loan Estimate: Check page one of this official document. The "Rate Lock" box must clearly say "Yes" alongside the expiration date.

How Long Does a Mortgage Rate Lock Last?

The timeframe to lock a mortgage rate entirely depends on how far out your closing date is. You want a window that safely covers the appraisal, underwriting, and final sign-off.

-

Standard periods: Most homebuyers go with 30, 45, or 60 days. These shorter windows are typically free.

-

Extended locks: If you're buying new construction, you might need 90 days or even longer.

Be careful with your timeline. If the seller delays the closing and your protection expires, you'll likely need a "lock extension." This isn't usually free. Lenders often charge an extension fee to keep the original rate alive.

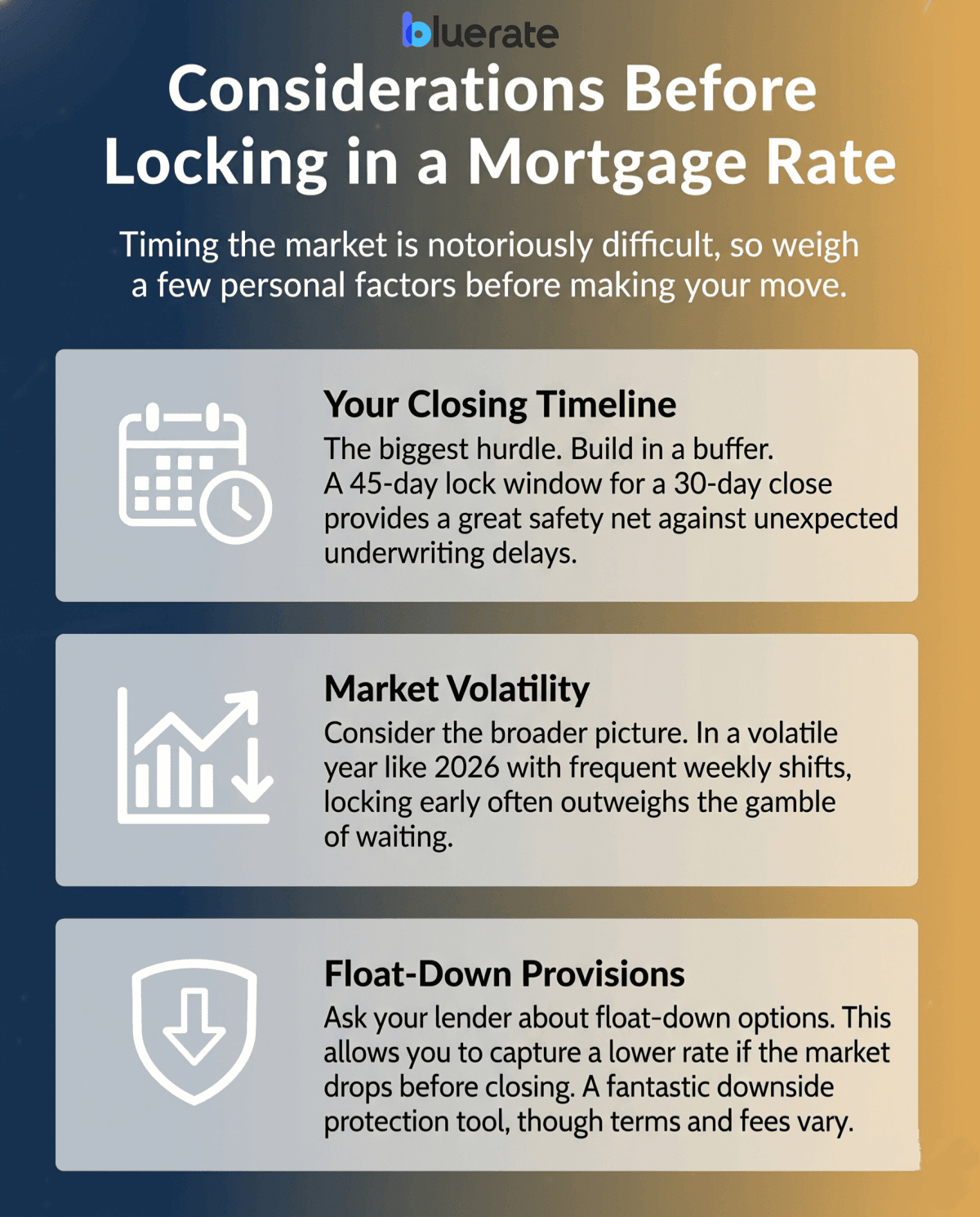

Considerations Before Locking in a Mortgage Rate

Timing the market is notoriously difficult, so you should weigh a few personal factors before making your move.

-

Your Closing Timeline: This is the biggest hurdle. Give yourself a buffer. If you expect to close in 30 days, a 45-day window provides a great safety net against unexpected underwriting delays.

-

Market Volatility: Look at the broader picture. In a volatile year like 2026 where rates frequently shift by fractions of a percent weekly, locking early often outweighs the gamble of waiting.

-

Float-Down Provisions: Ask your lender about this crucial feature. If you lock today but market averages drop significantly next week, a float-down allows you to capture that lower rate before closing. They may involve a fee depending on the lender, though some lenders offer limited float-down options at low or no cost, but it's fantastic downside protection.

FAQs About Locking in a Mortgage Rate

Q1. What is a mortgage rate lock fee?

For standard 30 to 60-day periods, lenders usually bake the cost into the rate itself, making it effectively "free." However, if you need an extended timeframe or have to buy an extension later, expect to pay an upfront deposit or a fee ranging from 0.25% to 0.5% of your total loan amount.

Q2. Can you lock in a mortgage rate before closing?

Yes, absolutely. You are not required to lock your rate before closing, but most borrowers choose to do so to avoid the risk of rising interest rates. A common approach is to lock your rate shortly after your offer is accepted, typically aligned with your expected closing timeline (often 30 to 45 days before closing).

Q3. How far in advance should I lock in my mortgage rate?

I always suggest handling this the moment you have a signed purchase contract and a firm closing date. Trying to aggressively time the market might backfire. If rates jump unexpectedly, your debt-to-income ratio could increase enough to ruin your loan approval.

Q4. Is it a good idea to lock in a mortgage rate?

In many cases, locking your rate can be a prudent choice, especially in uncertain market conditions, as it helps protect your monthly payment from potential increases. It guarantees you can comfortably afford your monthly payments regardless of what the Federal Reserve or the bond market does next.

Q5. If I lock in a mortgage rate, can I back out?

You aren't literally trapped, but there are catches. If you switch to an entirely different lender, your original lock vanishes. If you stay with the same lender but national rates plummet, you're stuck with your agreed-upon numbers, unless you specifically negotiated a float-down option beforehand.

Conclusion

Navigating the homebuying journey is stressful enough without playing a guessing game with financial markets. Utilizing a mortgage rate lock is the absolute best way to protect your buying power and secure predictable monthly payments. Just remember to pad your timeline against unexpected delays and ask about a float-down option in case numbers drop.

Things change fast in real estate. Rather than trying to figure it out alone, handing the heavy lifting to an expert is a smart move. If you're unsure about current trends or when to execute your lock, visit Bluerate.ai. You can explore transparent options and easily get free advice from professional loan officers ready to help you land the best possible deal.