How Long Can You Lock in a Mortgage Rate? Check Timeline

I remember staring at my phone, watching interest rates tick upward while my home purchase was still weeks away from closing. It's a gut-wrenching feeling. If you're anxious about market swings, you are probably wondering exactly how long you can freeze that perfect number. Let's break down the timeline and costs. If you're still unsure after reading, reaching out to a loan officer can save you thousands.

Key Takeaways

-

Most lenders offer standard rate locks lasting 30 to 60 days.

-

Lock length often affects cost. Shorter periods are sometimes free or cheaper, while longer periods may come with higher fees or a slightly higher rate, depending on the lender.

-

If your closing gets delayed, you can request an extension, but prepare for potential fees.

-

You may be able to use a float-down option to lower your locked rate if market rates drop, but availability, timing rules, and fees vary by lender.

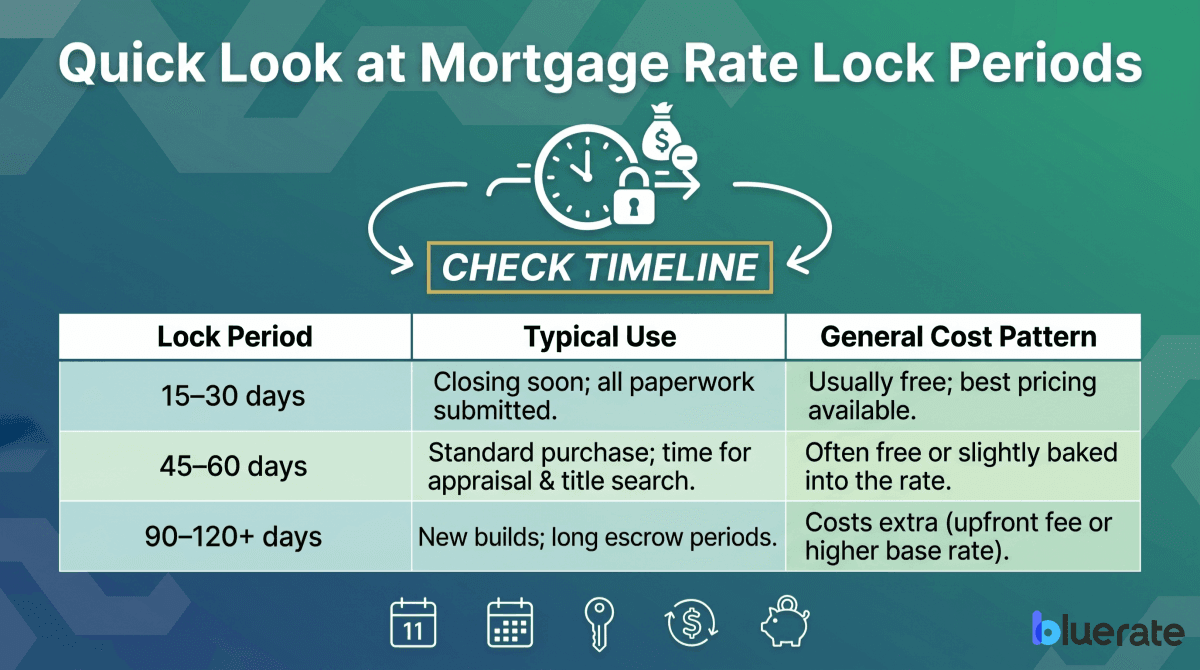

Quick Look at Mortgage Rate Lock Periods

Picking the right timeframe isn't a guessing game. It heavily depends on where you stand in your homebuying journey. I learned the hard way that locking too early can be just as risky as locking too late. Here is a handy breakdown of typical timelines so you can map out your strategy:

How Long Can You Lock in a Mortgage Rate?

Lenders may offer lock periods ranging from as short as 15 days to much longer terms in special cases, but 30, 45, and 60 days are the most common options. However, these windows are categorized based on risk and processing time. Let's dive into what each tier means for your wallet.

Also Read: Mortgage Rate Lock Explained: Meaning, Strategies, Risk & FAQs

Short-Term Locks (15--30 days)

When you are just a few weeks away from getting your keys, a 15 to 30-day window is your best friend. This tier is often priced more favorably than longer locks, but it is not always free, and the cost can be built into the rate or points. It is specifically designed for buyers who already have an accepted offer, signed purchase agreements, and are just waiting on the final underwriter sign-off.

However, be careful here. If a sudden title issue pops up or the seller delays the move-out date, this short window can easily expire. I only recommend going this tight if your closing date is practically set in stone.

Standard Locks (45--60 days)

This is the industry's sweet spot. A 45 to 60-day timeframe gives you ample breathing room to handle the most unpredictable parts of buying a house: the appraisal and the title search. When I bought my second property, my lender automatically suggested a 45-day lock because it covers normal processing delays without piling on extra costs.

Many lenders offer this standard period at no separate charge, though the cost may be reflected in the quoted interest rate or points. For the vast majority of standard home purchases, this is the safest and most practical route to take.

Extended Locks (90--120+ days)

Building a new home from the ground up or dealing with a complicated, long escrow? You will likely need an extended timeline. Some lenders even offer "Lock and Shop" programs that let you secure a rate for up to 270 or 360 days.

But this convenience doesn't come cheap. Because the bank is taking on a massive risk that the market might shift over several months, they will pass that cost to you. Depending on the lender, you may pay an upfront fee, sometimes around 0.25% to 1% of the loan amount, or accept a higher rate in exchange for the longer lock period.

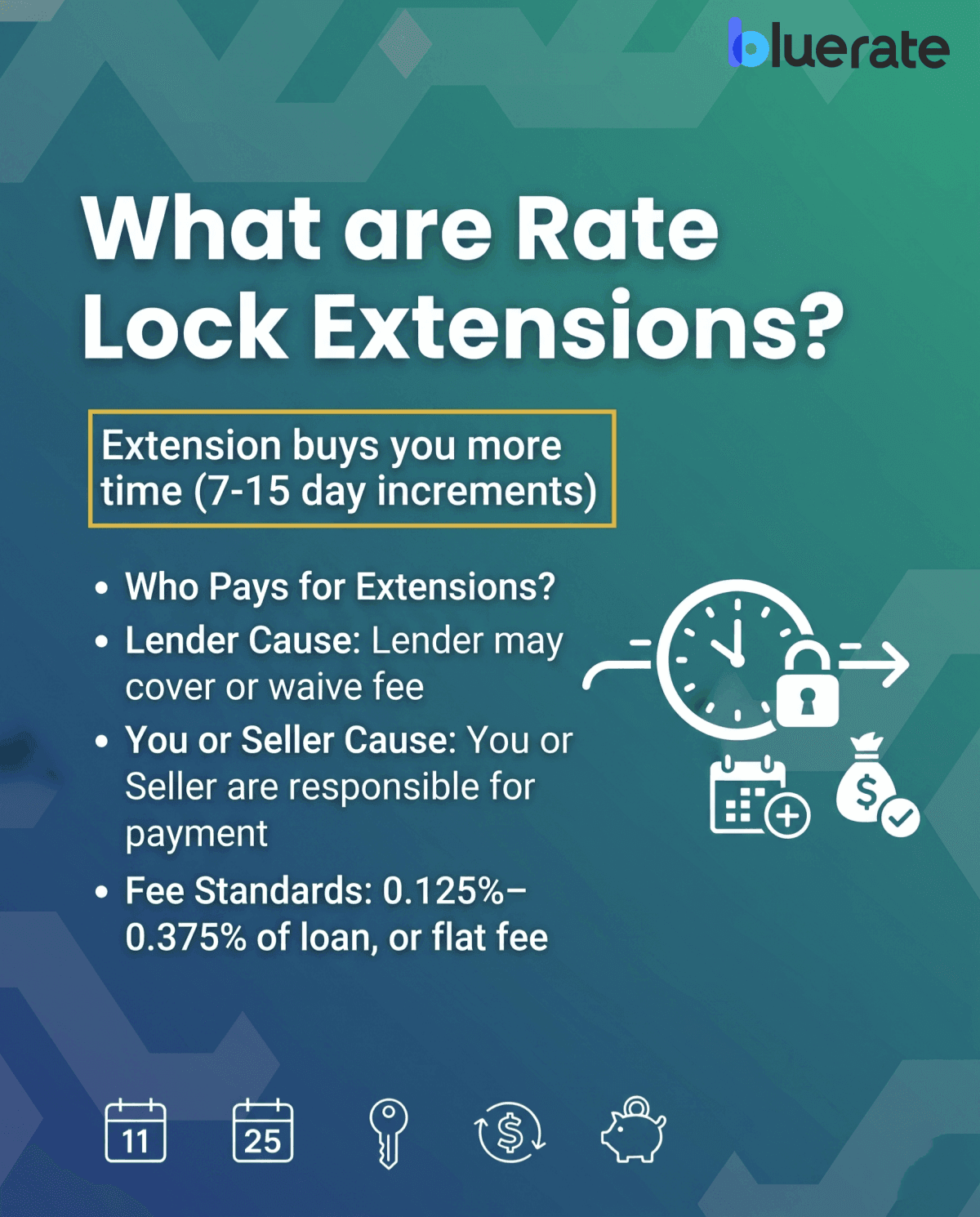

What are Rate Lock Extensions?

Sometimes, despite your best efforts, things go wrong. Maybe the appraiser is backed up, or the seller needs to fix a leaky roof before you take ownership. When this pushes your closing past your original deadline, you'll need a rate lock extension.

Simply put, an extension buys you more time, typically in 7 to 15-day increments, to keep your original rate intact. The big question is: who pays for it? If the delay is caused by the lender, the lender may waive or cover the extension fee, but policies vary. But if the hold-up falls on your shoulders or the seller's, expect to pay an extension fee. According to current market standards, extension fees vary by lender and can be charged as a flat fee or as a percentage of the loan principal, often ranging from about 0.125% to 0.375%.

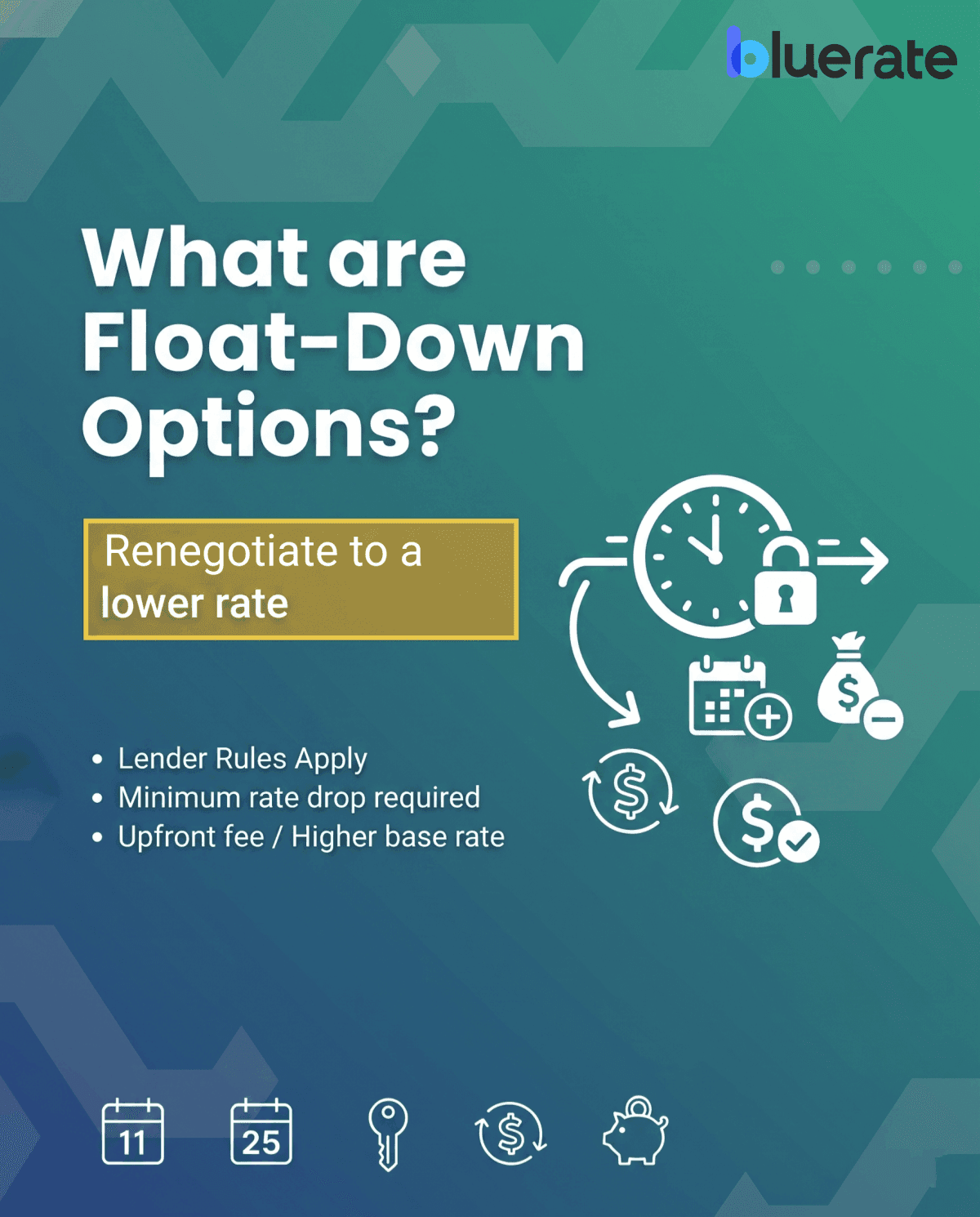

What are Float-Down Options?

I hear this anxiety a lot: "What if I lock today, and the market drops tomorrow?" That's exactly where a float-down option comes into play.

A float-down provision allows you to renegotiate and grab a lower market rate before you close, even though you are already locked in. It sounds like magic, but it comes with strict rules. Most lenders set a minimum rate drop you must meet before exercising a float-down, and the threshold varies by lender. Also, keep in mind that this isn't a free lunch. Lenders generally charge an upfront, non-refundable fee to add this clause to your contract, or they might offer you a slightly higher base rate in exchange for the flexibility.

When to Lock a Mortgage Rate?

Timing the market perfectly is impossible, even for Wall Street experts. Instead of obsessing over daily charts, I always advise basing your decision on your personal transaction status. You should seriously consider when to lock a mortgage rate:

-

You have a signed purchase agreement and a clear path to closing.

-

The quoted monthly payment fits comfortably within your budget right now.

-

Your closing date is confirmed with the seller and the title company.

-

Economic news points toward high volatility or rising inflation.

The golden rule here is to secure a number you can afford today, rather than gambling on the chance of a slightly cheaper payment next month.

How Long Should You Lock in a Mortgage Rate?

So, how do you decide the exact number of days? My favorite decision-making framework is simple: take your estimated closing timeline and add a 10 to 15-day buffer.

For example, if your real estate agent and lender estimate that it will take 30 days to close, don't just ask for a 30-day lock. Request a 45-day window. Different property types and local county recording speeds can easily throw off your schedule. Paying for a slightly longer timeframe upfront is usually much cheaper and far less stressful than begging for an emergency extension at the last minute.

FAQs About the Timeline of a Mortgage Rate Lock

Q1. What happens if my rate lock expires?

If your deadline passes, you are essentially at the mercy of the current market. Your lender will quote you a new rate based on today's pricing, which might be drastically higher. Alternatively, you can often pay a penalty fee to extend your original terms, assuming your lender allows it.

Q2. Do longer rate locks cost more?

Yes, absolutely. Holding a rate for 90 days or more means the lender shoulders a higher risk of market fluctuations. To compensate, they pass those costs onto you. The cost may appear as an upfront fee, points, or a higher quoted rate, depending on the lender and the lock term.

Q3. Can I lock a mortgage rate before finding a house?

Yes, through specific "Lock and Shop" programs. A few lenders allow you to freeze a rate for 60 to 90 days while you actively attend open houses. Just read the fine print. These programs often require you to get under contract within a strict timeframe to keep the deal valid.

Q4. Does a rate lock guarantee my loan gets approved?

No, it does not. A lock only freezes the price of the money you want to borrow. You still must successfully pass the entire underwriting process. If you lose your job or finance a new car right before closing, your mortgage application can still be completely denied.

Q5. Can I cancel my rate lock and switch lenders?

You can, but it's rarely worth the hassle. Switching lenders means starting the entire application process over from scratch, which will inevitably delay your closing date. Plus, any money you already spent on the home appraisal or credit check fees with the first bank is a sunk cost you won't get back.

Conclusion

Navigating the homebuying process is already overwhelming enough without constantly worrying about market volatility. At the end of the day, choosing the right timeline to lock a mortgage rate is all about finding a healthy balance between upfront costs and your own peace of mind. Give yourself a reasonable buffer, lock in a monthly payment you are comfortable with, and try not to look back.

If mapping out this timeline still feels stressful, reach out to a dedicated loan officer at Bluerate today. Our experts will gladly analyze your specific homebuying scenario to help you secure the best possible terms without the guesswork.