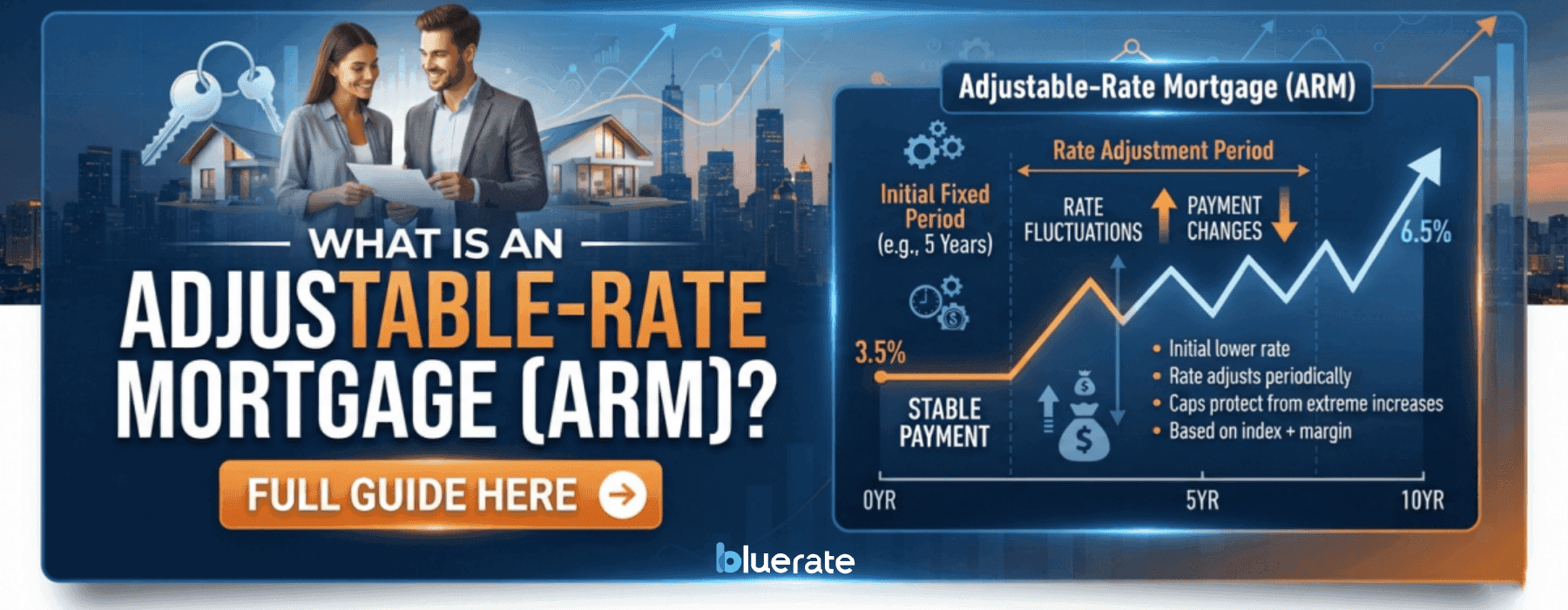

What is an Adjustable-Rate Mortgage (ARM)? Full Guide Here

When my partner and I bought our first place, mortgage jargon felt like a brick wall. I kept hearing about "ARMs" but had no clue what they actually were. If you're feeling just as lost, I wrote this down-to-earth guide for you. To make things easier, you can also reach out to a local Loan Officer for free advice.

Key Takeaways

- Lower start: You get cheaper monthly payments at the beginning of the loan.

- Rate shifts: Your rate moves up or down later based on market indexes.

- Safety nets: Built-in rate caps protect you from massive payment shocks.

- Best fit: It's ideal if you plan to move or refinance soon.

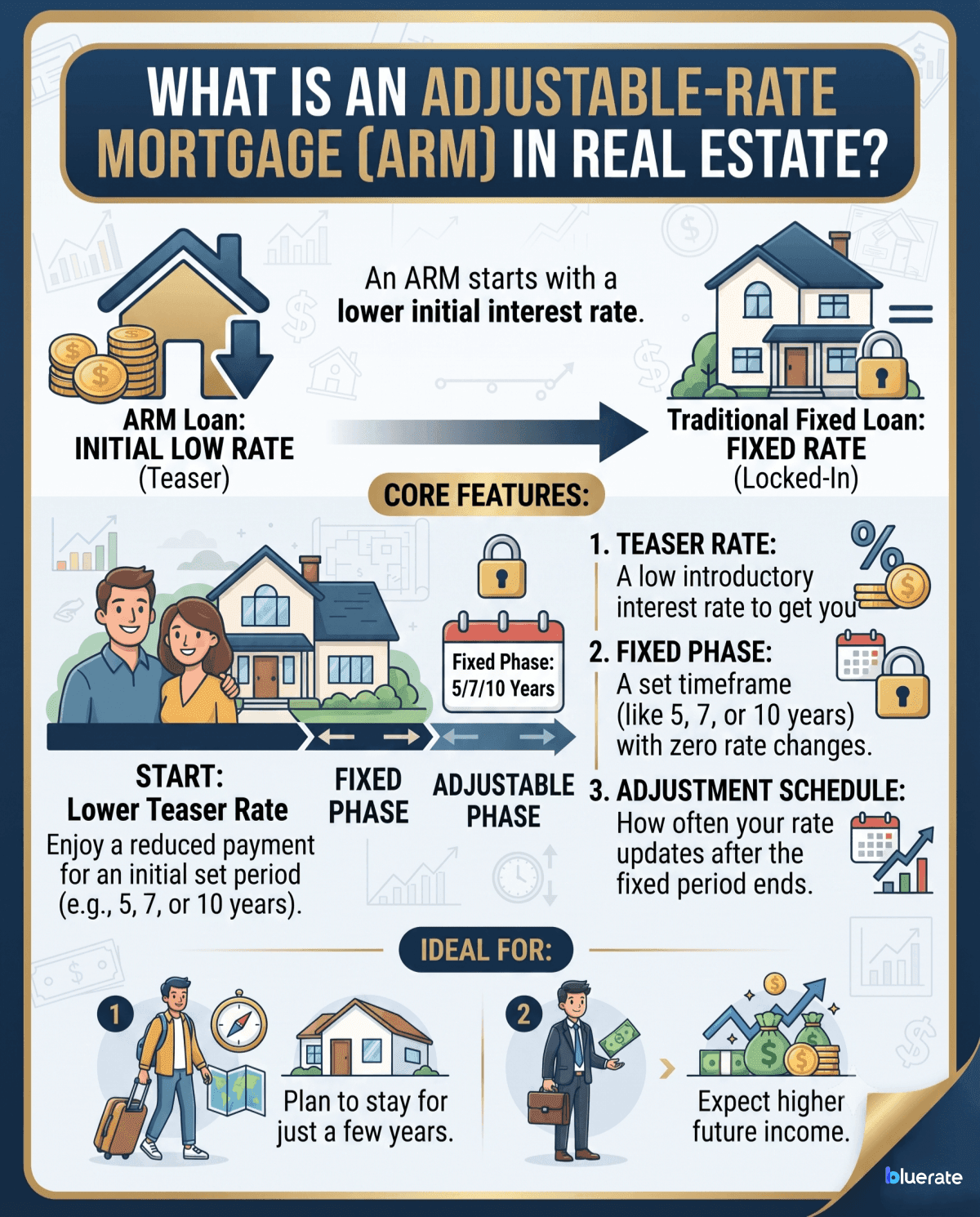

What is an Adjustable-Rate Mortgage (ARM) in Real Estate?

Simply put, an adjustable-rate mortgage (ARM) is a home loan where your interest rate doesn't stay the same forever. Unlike a traditional 30-year fixed loan where your payment is locked in, an ARM starts you off with a lower interest rate for a set period. After that, your rate shifts up or down depending on the market.

I usually see ARMs work best for people who plan to stay in their home for just a few years, or those who expect to make a lot more money down the road. Here are the core features:

- Teaser rate: A low introductory interest rate to get you started.

- Fixed phase: A set timeframe (like 5, 7, or 10 years) with zero rate changes.

- Adjustment schedule: How often your rate updates after the fixed period ends.

What is an Example of an Adjustable-Rate Mortgage?

Let's look at a 5/6 ARM, which is a common option in the US. I used to think these numbers were just random codes, but they actually tell you exactly how your loan behaves.

The first number, 5, means your interest rate is locked in and won't change for the first five years. The second number, 6, tells you that once those five years are up, your rate will adjust every six months. If you had a 5/1 ARM, it would adjust once a year after the initial five-year fixed period. Knowing these numbers helps you plan your financial future.

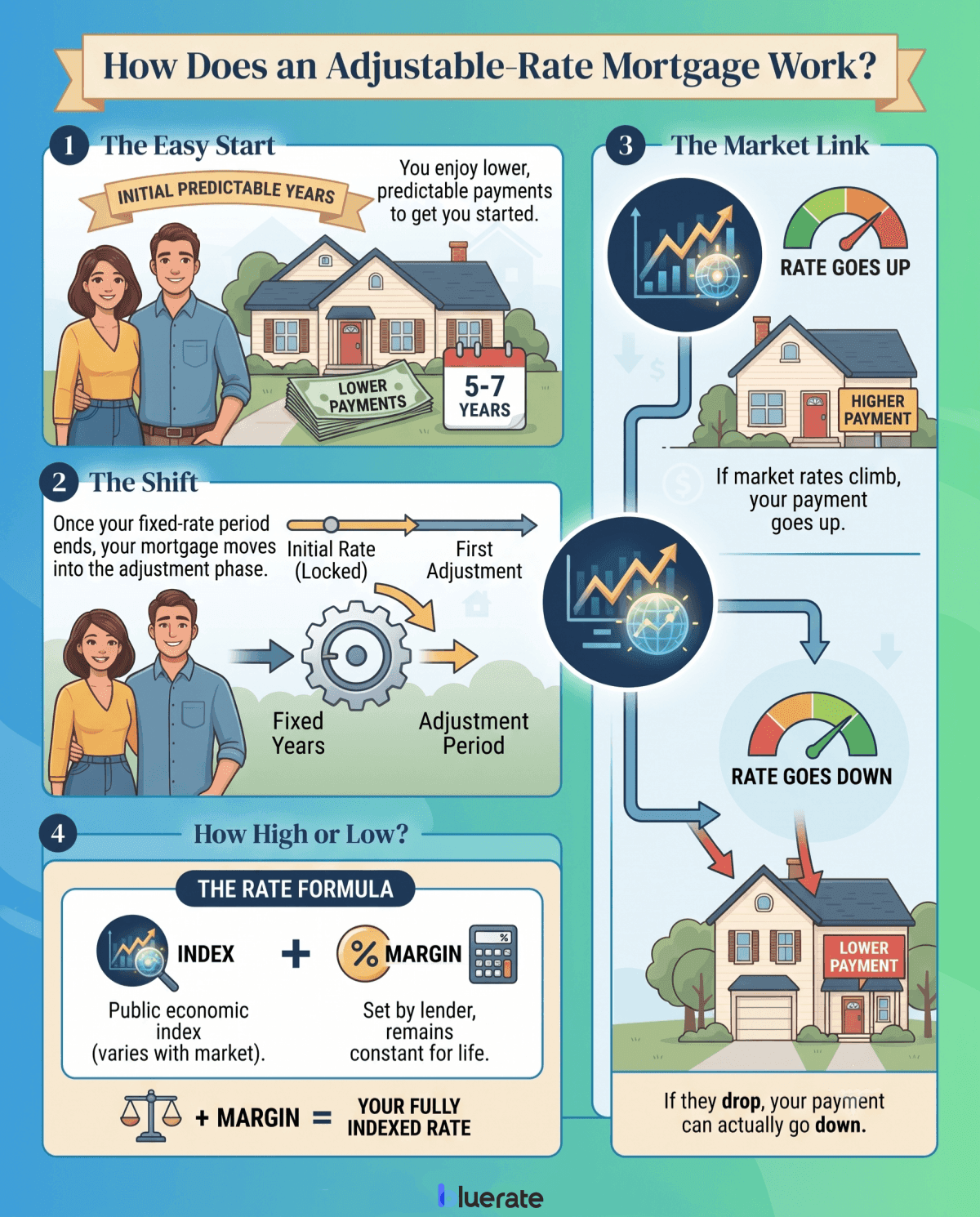

How Does an Adjustable-Rate Mortgage Work?

How do these rate changes actually happen? It isn't just your lender guessing or picking a number out of thin air. Instead, your loan follows a set market-driven process. Here is how that looks in real life:

- The easy start: You enjoy lower, predictable monthly payments during your initial years.

- The shift: Once your fixed years end, your rate moves into the adjustment phase.

- The market link: Your new rate aligns with a public economic index. If market rates climb, your payment goes up. If they drop, your payment can actually go down.

How high or low that rate goes depends on two elements: your index and your margin.

How is an Adjustable-Rate Mortgage Calculated?

Calculating your new rate is actually pretty basic math. Lenders use a simple formula:

Fully Indexed Rate = Index + Margin

- The Index: This is a public benchmark rate. Many U.S. lenders today use SOFR or a SOFR-based index for ARM calculations.

- The Margin: This is a fixed percentage set by your lender when you sign (usually around** 2% to 3%**) that never changes.

For example, if the SOFR index is at 3.5% and your margin is 2.5%, your final interest rate for that adjustment period will be 6.0%.

Protections and Limits of ARM (Interest Rate Caps Explained)

When I talk to friends about ARMs, their biggest fear is a sharp increase in interest rates. Luckily, US loans come with legal safeguards called interest rate caps to keep your payments manageable.

Most loans have three caps, though the exact limits vary by loan program.

- Initial Cap: The absolute maximum your rate can rise during your very first adjustment.

- Periodic Cap: How much your rate can jump from one adjustment period to the next (usually 1% or 2%).

- Lifetime Cap: Your loan's hard ceiling. Your rate can never go above this number, no matter how crazy the market gets.

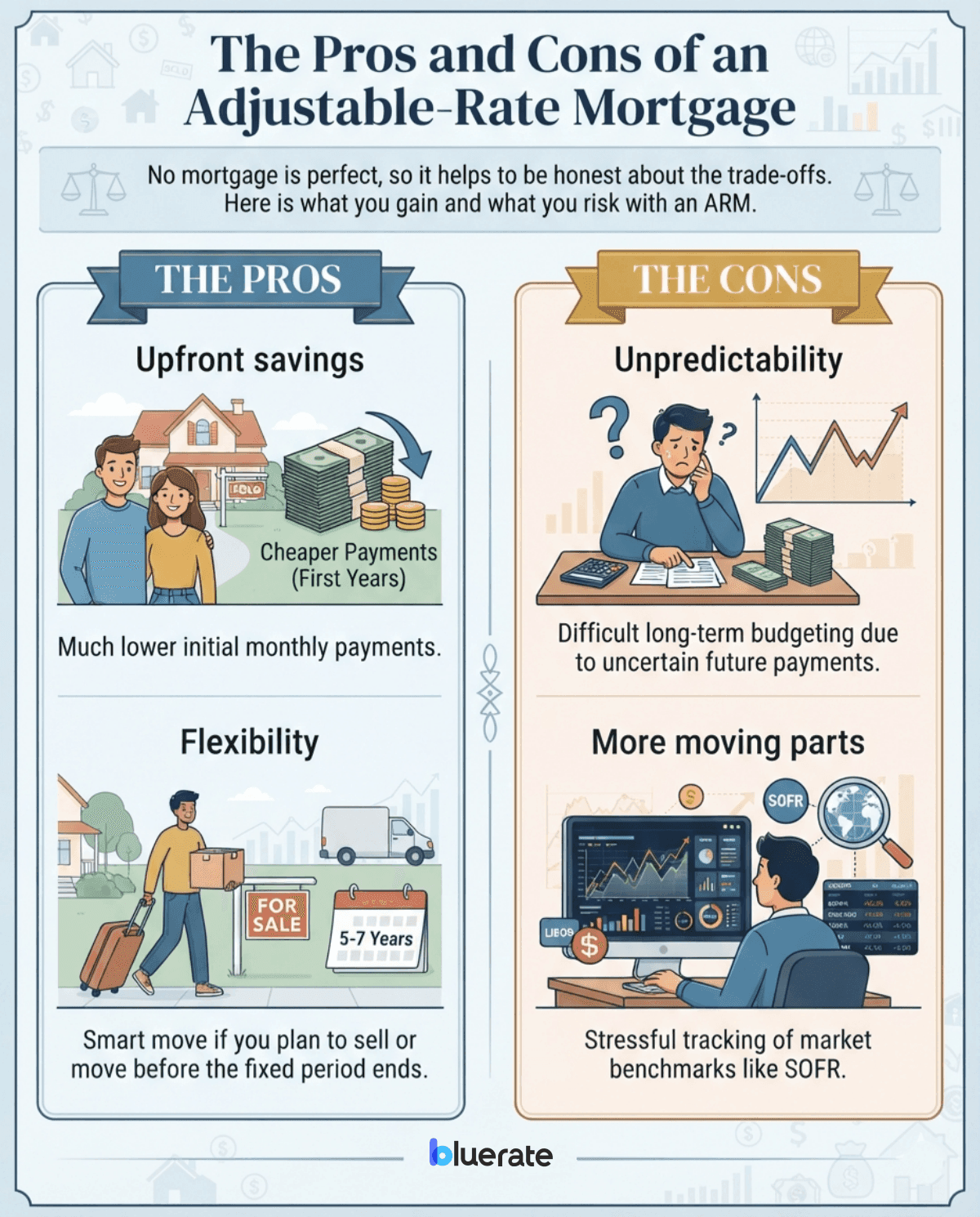

The Pros and Cons of an Adjustable-Rate Mortgage

No mortgage is perfect, so it helps to be honest about the trade-offs. Here is what you gain and what you risk with an ARM.

Pros:

- Upfront savings: You get much cheaper payments during those first few years.

- Flexibility: It is a smart move if you plan to sell or move before your fixed period ends.

Cons:

- Unpredictability: It is hard to budget long-term when you don't know your future payments.

- More moving parts: Tracking market benchmarks like SOFR can feel stressful if you prefer simple finances.

What is Better, a Fixed-Rate or Adjustable-Rate Mortgage?

There isn't a single "correct" answer here. It really comes down to your personal timeline and how well you sleep at night when rates fluctuate.

A fixed-rate mortgage is usually your best bet if you plan to raise a family and stay in the same house for 15 or 30 years. You get complete peace of mind because your payment never changes.

However, an ARM is often smarter if:

- You know you will sell the house or refinance before your fixed period ends.

- You want lower initial payments to free up cash for renovations or savings.

- You expect your income to jump up significantly in a few years.

Be realistic about your five-year plan before you sign any paperwork.

To learn more, please check: Fixed vs Adjustable Rate Mortgage: Full Comparison Here

FAQs About Adjustable-Rate Mortgage (ARM)

What is the main downside of an adjustable-rate mortgage?

The biggest issue is the risk of payment shock. If market rates spike when your fixed period ends, your monthly bill can jump up, putting a real strain on your wallet.

Why would somebody want an adjustable-rate mortgage?

Mainly to save money upfront. The lower initial interest rate lets you keep extra cash in your bank account, which is great if you plan to move quickly anyway.

What is SOFR and how does it affect my ARM?

SOFR is a widely used benchmark index that many U.S. lenders use to calculate rate adjustments. Think of it as the thermometer used to measure how much your rate should move.

Can I convert or refinance an ARM into a fixed-rate loan later?

Yes, absolutely. One possible strategy is to use the ARM during the initial fixed period and then refinance into a fixed-rate loan before the first adjustment.

What is the difference between a 5/1 and a 5/6 ARM?

Both lock in your low rate for five years. But after that, a 5/1 ARM adjusts once a year, while a 5/6 ARM adjusts every six months.

Final Word

Picking the right mortgage is a huge decision, and there is no shame in feeling a bit overwhelmed by it all. While an ARM can save you thousands of dollars early on, you really need a solid game plan for what you will do before those adjustments start.

Since everyone's budget is different, I highly suggest hopping over to Bluerate. You can easily get connected with local, experienced Loan Officers who can look at your specific numbers and guide you through the process for free. Take your time, think about your timeline, and find a loan that lets you sleep easy.

People Also Read

- 10 Tips: First-Time Home Buyer Tips and Advice for You

- [[Must-Read Tips] How Do I Get the Lowest Mortgage Rates?](https://www.bluerate.ai/blog/get-the-lowest-mortgage-rate)

- Where and How to Compare Mortgage Loan Quotes Online?