What is a Fixed-Rate Mortgage? 2026 Guide for You

I still remember the anxiety of buying my first home, staring at confusing loan sheets and wondering if my monthly payments would suddenly spike. If you are feeling that exact dread, a fixed-rate mortgage might be your saving grace. Let's break down how it works. If you want to skip the guesswork, you can always connect with a vetted local loan officer for free.

Key Takeaways

- Constant rate: Your interest rate stays locked for the entire loan life.

- Budget security: Monthly principal and interest payments never fluctuate.

- Refinancing required to drop rates: If market rates drop, your rate won't fall automatically.

- Escrow can vary: Property taxes and insurance might still alter your overall payment.

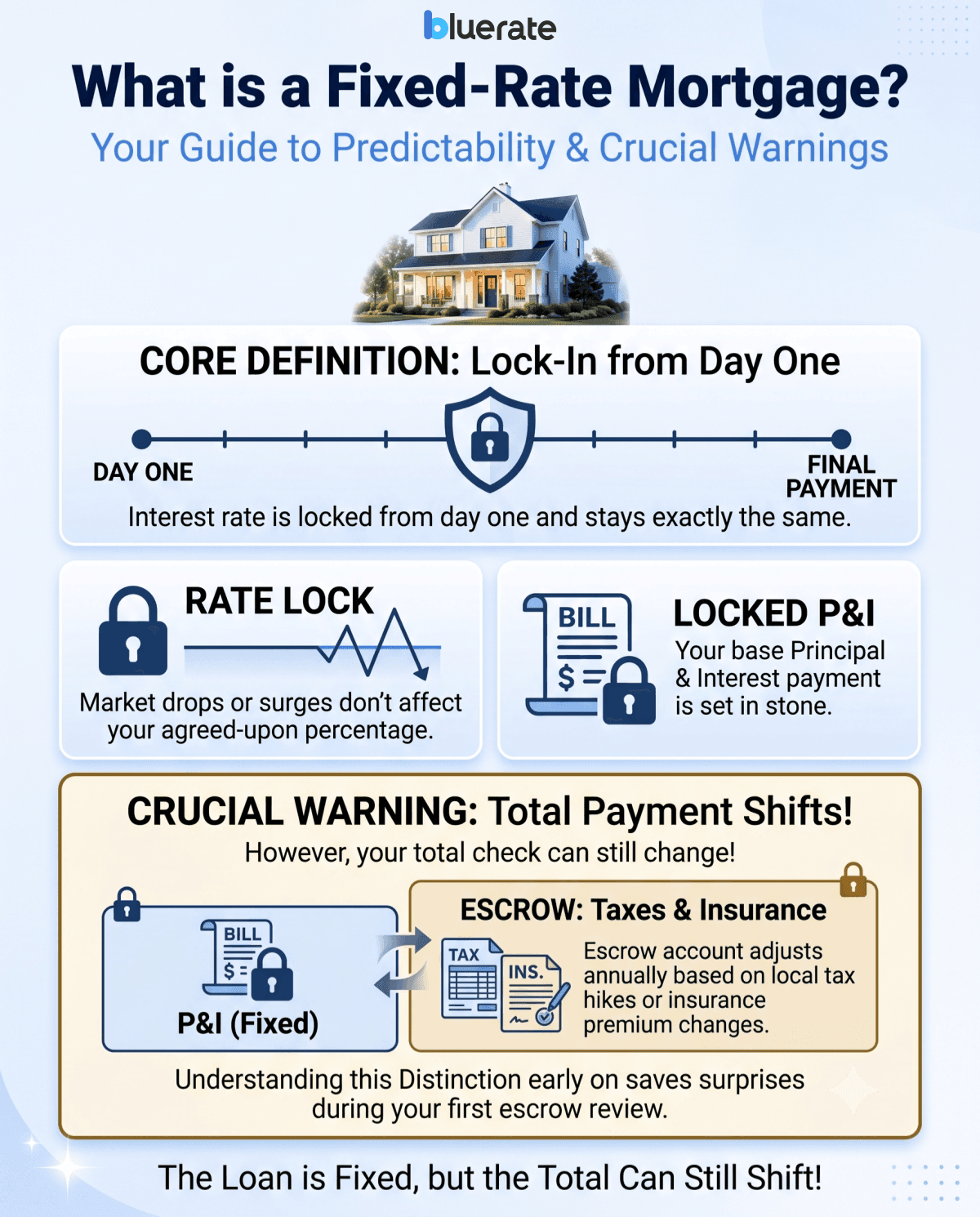

What is a Fixed-Rate Mortgage?

A fixed-rate mortgage is a home loan where your interest rate is locked in from day one and stays exactly the same until your final payment.

When we look at its main features, it is all about predictability:

- Rate Lock: Market drops or surges won't touch your agreed-upon percentage.

- Locked Principal and Interest: Your base payment is set in stone.

However, I always give my clients one crucial warning: your total check to the bank can still shift. While your loan's principal and interest are fixed, your escrow account, which covers property taxes and home insurance, can adjust annually based on local tax hikes or insurance premium changes. Understanding this distinction early on will save you from unexpected surprises during your first escrow review.

How Does a Fixed-Rate Mortgage Work?

This loan type relies on a mathematical process called amortization. Here is how that plays out in your monthly routine:

- The Payment Split: Every payment you make is split between interest and principal. Early on, almost all your money goes toward interest. Over the years, the ratio flips, and you begin aggressively paying off your actual house balance.

- Flexible Timelines: Most US buyers choose a 30-year term, which offers the lowest monthly payments. However, 15-year options are highly popular for those wanting to slash their lifetime interest costs, though they require a much higher monthly cash commitment.

From my experience, understanding this interest-to-principal shift helps you see why keeping a home long-term builds significant equity.

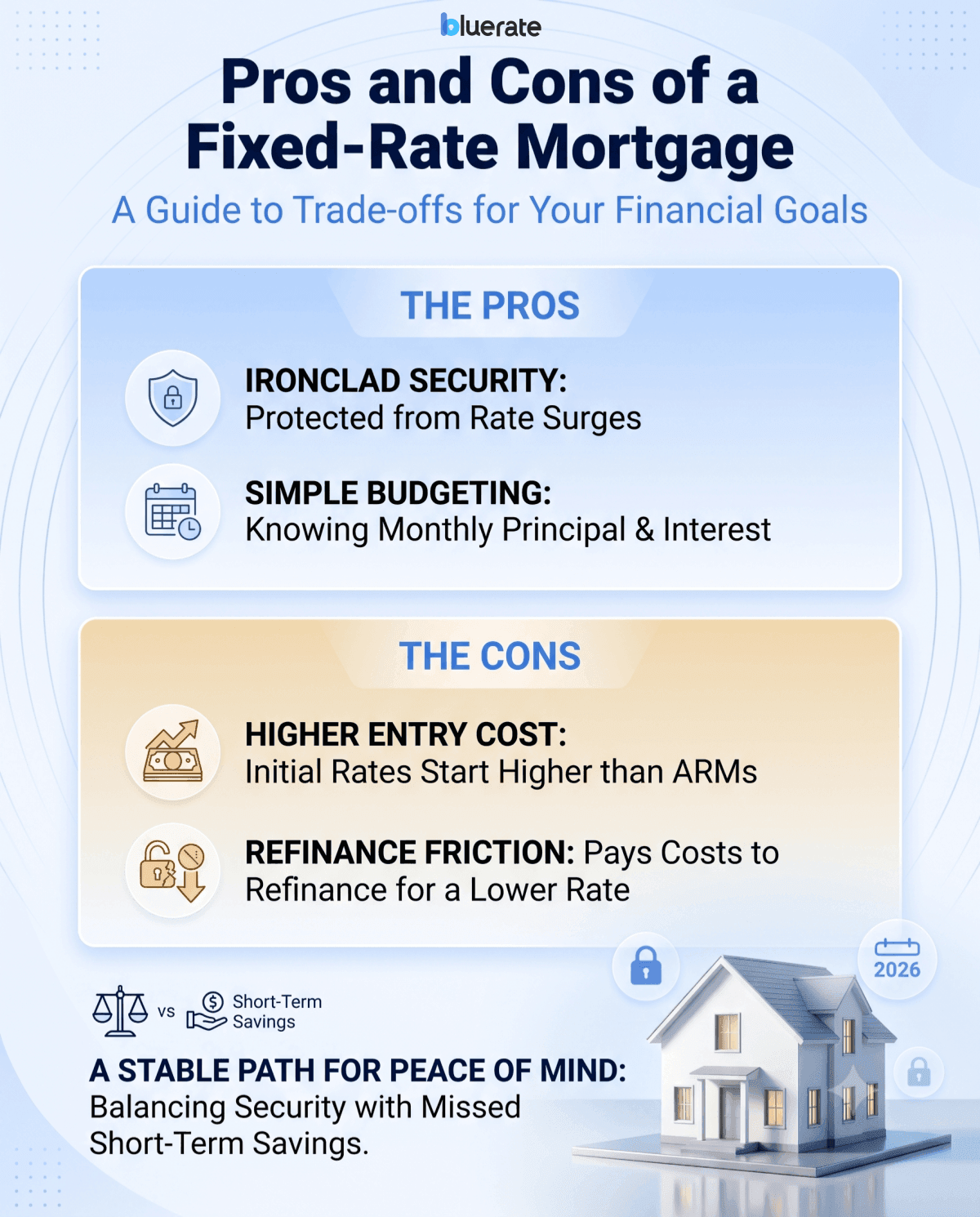

Pros and Cons of a Fixed-Rate Mortgage

Every financial product has trade-offs. Weighing these benefits and drawbacks will clarify if this fits your goals.

Pros:

- Ironclad Security: You are shielded if national interest rates skyrocket tomorrow.

- Simple Budgeting: Knowing your monthly P&I cost makes long-term planning incredibly easy.

Cons:

- Higher Entry Cost: Fixed rates start higher than introductory adjustable-rate offers.

- Refinance Friction: If market rates drop, your rate stays high. You must pay thousands in closing costs to refinance and get that lower rate.

I find that buyers who value peace of mind over playing the market usually prefer this stable path, even if it means missing out on potential short-term savings.

Example of Fixed-Rate Mortgage

To see the real-world impact, let's look at a $300,000 home loan using current mid-2026 average market rates.

- If you lock in a 30-year fixed mortgage at 6.43%, your monthly principal and interest payment is roughly $1,882. Over the loan's life, you will pay about $377,700 in total interest.

- If you opt for a 15-year fixed mortgage at 5.79%, your monthly payment jumps to $2,499. However, you only pay $149,800 in total interest.

I love sharing this math because it clearly shows the trade-off. Choosing the 15-year option saves you over $227,000 in interest but demands an extra $617 from your monthly budget.

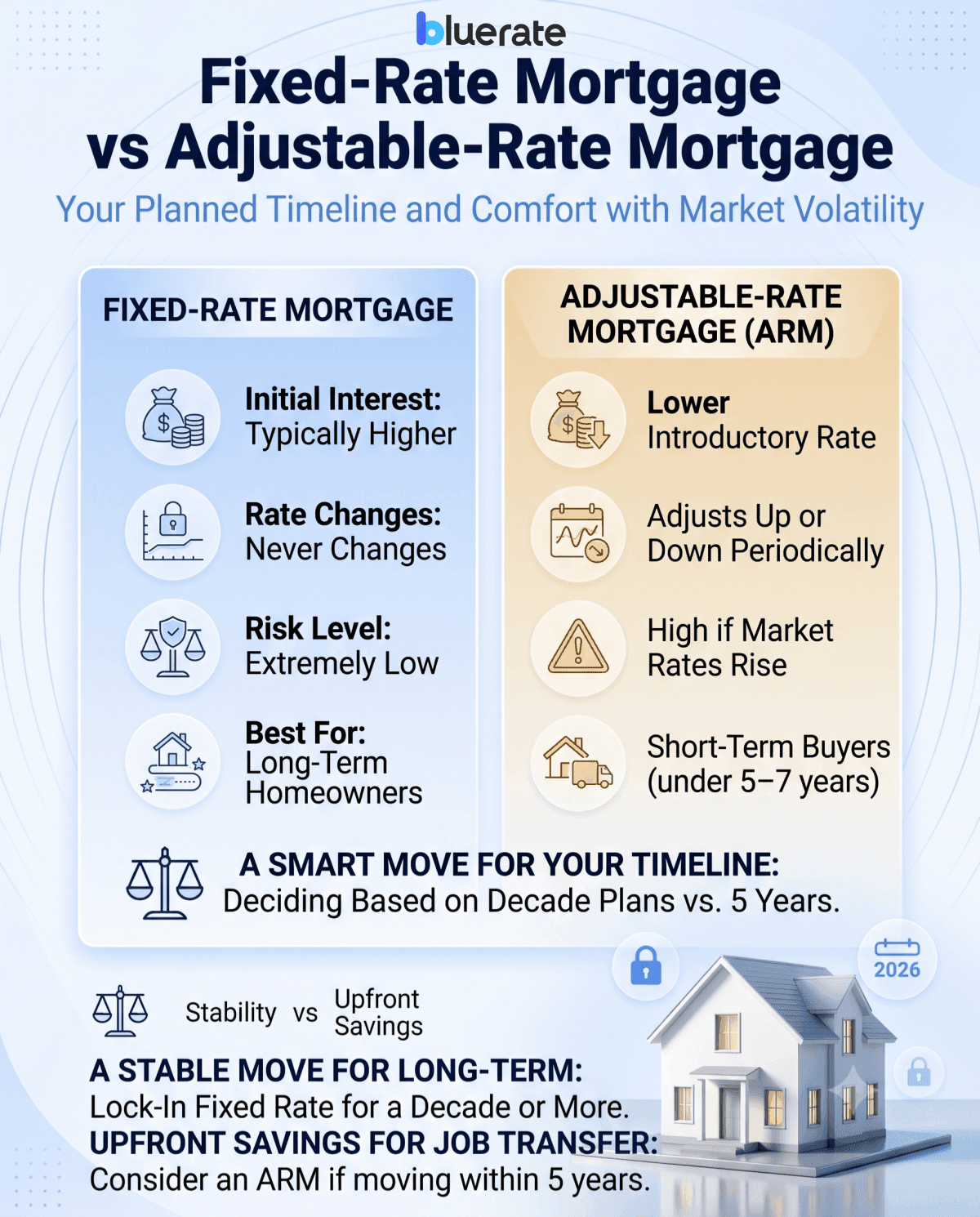

Fixed-Rate Mortgage vs Adjustable-Rate Mortgage

Deciding between these two options comes down to how long you plan to live in the home and your comfort level with market volatility.

I advise buyers that if they plan to stay in their home for a decade or more, locking in a fixed rate is almost always the smartest move. However, if a job transfer means you will move within five years, a 5-year ARM might save you thousands upfront.

Also Read:

- What is an Adjustable-Rate Mortgage (ARM)? Full Guide Here

- Fixed vs Adjustable Rate Mortgage: Full Comparison Here

FAQs About Fixed-Rate Mortgages

Q1. Can you refinance a fixed-rate mortgage?

Yes, absolutely. You can swap your current loan for a new one with a lower interest rate or a shorter term. Just remember that refinancing comes with closing costs, typically 2% to 6% of your loan amount. I recommend refinancing only if rates drop by at least 1%.

Q2. Is a 5-year fixed mortgage a good idea?

In the U.S., what people sometimes call a '5-year fixed' mortgage is usually a hybrid ARM: the rate is fixed for the first five years, then adjusts periodically after that. It's a great choice if you plan to sell the home or refinance before the five years are up. Otherwise, a standard 30-year fixed is safer.

Q3. What are the disadvantages of a fixed-rate mortgage?

The biggest drawback is the lack of automatic flexibility. If market rates fall, your rate stays high unless you spend thousands of dollars to refinance. Additionally, the initial rates are usually higher than those of adjustable-rate mortgages.

Q4. What's the difference between fixed rate and flat rate?

A fixed-rate mortgage keeps the interest rate unchanged, but each monthly payment is split between principal and interest, and the interest portion declines over time as the balance is paid down. A flat-rate loan, by contrast, is calculated on the original loan amount for the full term and is usually more expensive.

Q5. What is better, a fixed or variable mortgage?

It comes down to your sleep-at-night factor. If you want predictable, steady payments, a fixed mortgage is better. If you plan to move quickly or believe rates are going to plummet and you are comfortable with some financial risk, a variable mortgage might save you money.

Final Word

Navigating the homebuying journey can feel overwhelming, but securing a fixed-rate mortgage is one of the most reliable ways to protect your personal finances. Locking in a stable payment gives you the freedom to build a life in your new home without checking the Federal Reserve's decisions every month.

Because local rules, taxes, and loan options can vary widely across different states, you shouldn't go through this alone. I always suggest speaking with a professional. You can easily find a vetted, highly rated local loan officer in your area through Bluerate. They will help you compare options completely free of charge and find the right fit for your budget.