Fixed vs Adjustable Rate Mortgage: Full Comparison Here

When I bought my first home, the sheer volume of mortgage options felt overwhelming. You might be sitting at your kitchen table right now, staring at a screen, trying to decode the difference between a fixed-rate and an adjustable-rate mortgage (ARM). I've spent years helping buyers navigate this exact crossroads. Let's cut through the financial jargon together and break down which loan structure actually fits your life and budget.

Key Takeaways

- Fixed-rate mortgages offer predictable payments, protecting you from market spikes over the long haul.

- Adjustable-rate mortgages (ARMs) offer lower initial rates, saving you cash if you plan to move soon.

- Rate caps act as a critical safety net, limiting how high your ARM interest can climb.

- Your choice depends on your financial timeline and how much risk you can comfortably sleep with at night.

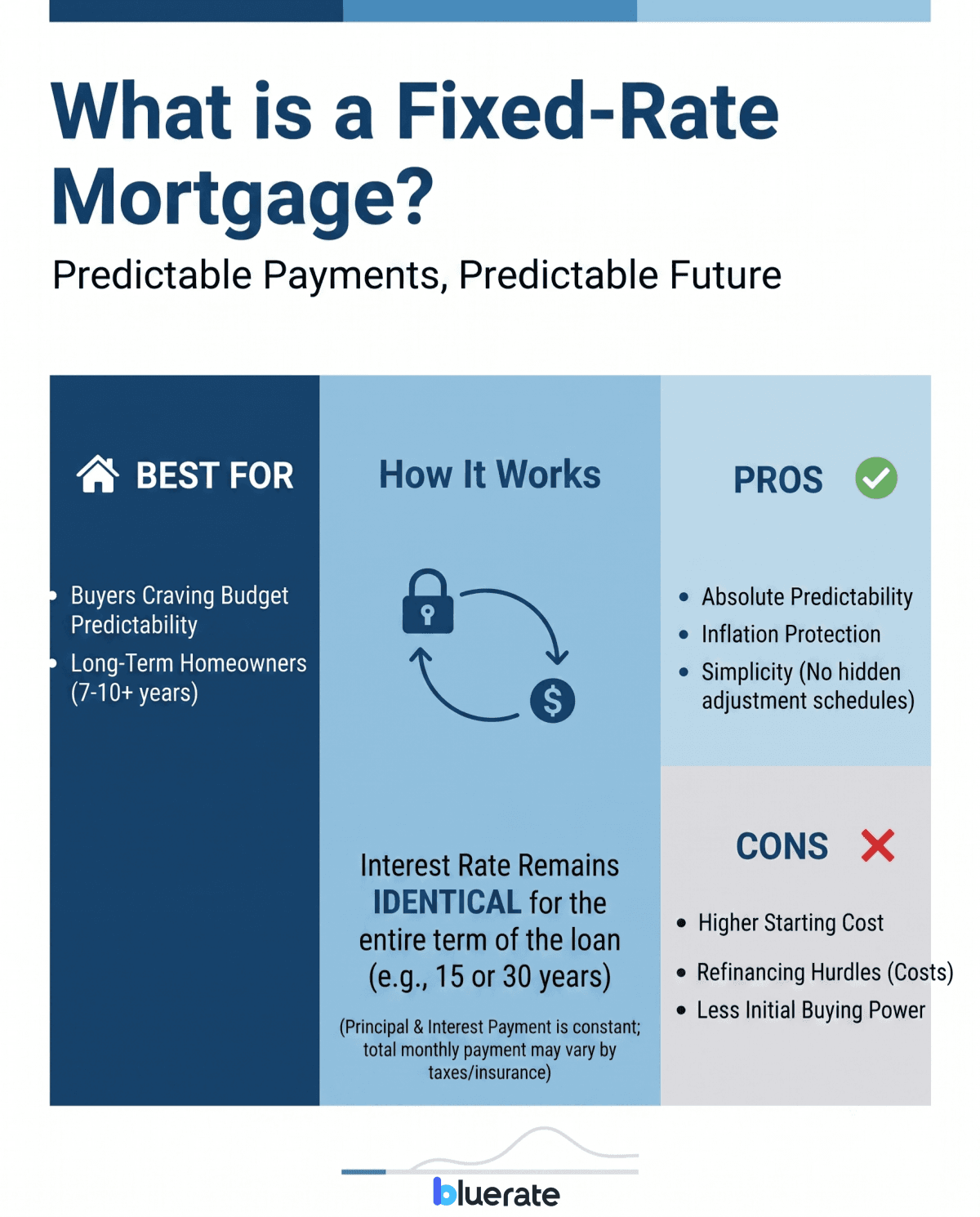

What is a Fixed-Rate Mortgage?

Best for: Buyers who crave budget predictability and plan to stay in their home for at least seven to ten years.

A fixed-rate mortgage keeps your interest rate identical from your very first payment to your last. Whether you choose a 15-year or 30-year term, your principal and interest payment remains the same over the life of the loan, although total monthly payments may change due to taxes and insurance.

Pros:

- Absolute predictability: Your monthly housing costs are locked in, making household budgeting stress-free.

- Inflation protection: Provides protection against rising interest rates, since your loan rate remains fixed even if market rates increase.

- Simplicity: The loan is straightforward, with no hidden adjustment schedules to track.

Cons:

- Higher starting cost: You pay a premium for stability, meaning your initial rate is typically higher than an ARM's.

- Refinancing hurdles: If market interest rates drop, you typically need to pay closing costs to refinance, although some options may reduce or roll these costs into the loan.

- Less initial buying power: Higher initial monthly payments might limit the maximum loan amount you qualify for.

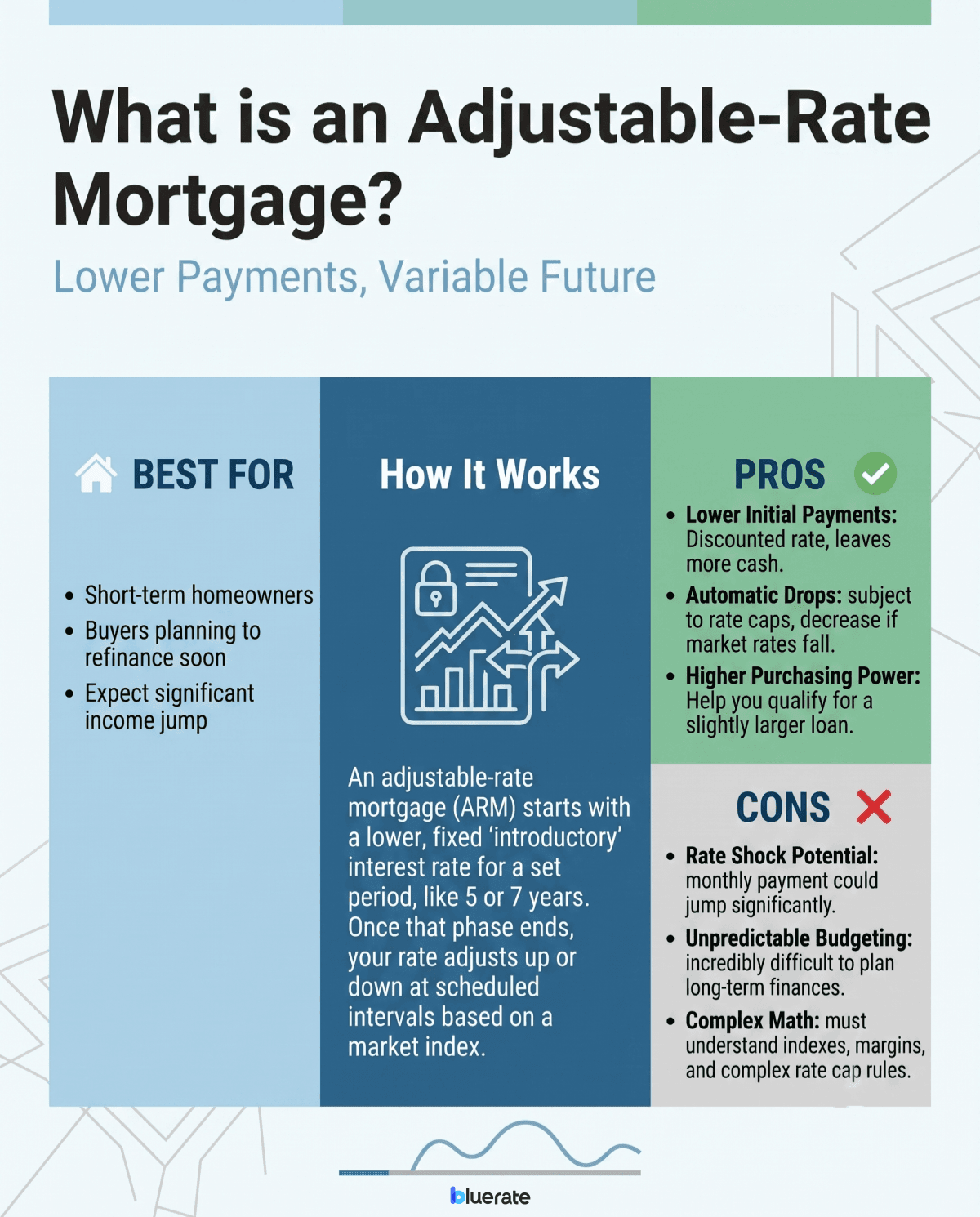

What is an Adjustable-Rate Mortgage?

Best for: Short-term homeowners, buyers planning to refinance soon, or those expecting a significant income jump.

An adjustable-rate mortgage (ARM) starts with a lower, fixed "introductory" interest rate for a set period, like 5 or 7 years. Once that phase ends, your rate adjusts up or down at scheduled intervals based on a market index.

Pros:

- Lower initial payments: You enjoy a discounted rate at the start, leaving more cash in your pocket.

- Automatic drops: If market rates fall, your rate and payment may decrease at scheduled adjustment periods, subject to rate caps.

- Higher purchasing power: The lower initial payment can help you qualify for a slightly larger loan.

Cons:

- Rate shock potential: After the introductory period, your monthly payment could jump significantly.

- Unpredictable budgeting: It is incredibly difficult to plan long-term finances when your housing costs keep shifting.

- Complex math: You have to understand indexes, margins, and complex rate cap rules.

Important ARM Protections

If you are leaning toward an ARM, don't panic about your rate spiraling out of control. Lenders apply strict safety guards called "caps" to protect your wallet. I always advise my clients to look closely at these three limits on their loan estimate:

- Initial Cap: Dictates the absolute maximum your interest rate can jump the very first time it adjusts after your introductory period ends.

- Subsequent Cap: Restricts how much your rate can shift during any single scheduled adjustment period later on.

- Lifetime Cap: Establishes the hard ceiling your rate can never exceed over the entire life of your loan.

Example of Fixed-Rate vs. Adjustable-Rate Mortgage

Let’s look at a real-world scenario to see how the numbers play out. Imagine you are taking out a $400,000 home loan and comparing your options using average rates:

- 30-Year Fixed: At a 6.5% interest rate, your monthly principal and interest payment is fixed at $2,528.

- 5/1 ARM: At a 5.75% initial rate, your payment is just $2,334 for the first five years.

By choosing the ARM, you save $194 every single month—totaling $11,640 over five years. However, in year six, if market rates spike, your monthly payment could quickly climb past that original fixed payment.

Similarities between fixed- and adjustable-rate mortgages

While these loans behave differently over time, they share the exact same foundation. In my experience, buyers often overlook how much common ground they actually have. For starters, both options generally follow similar underwriting standards, although specific requirements may vary depending on the loan type and lender, including credit score checks, debt-to-income limits, and professional home appraisals.

Furthermore, you can use either loan structure to buy a primary residence, vacation home, or refinance an existing mortgage. Finally, both options allow you to pay down your principal early, and most modern conventional loans do not include prepayment penalties, though some specialized loan products may still have them. Many loans include property taxes and insurance in a monthly escrow account, though this is not always required.

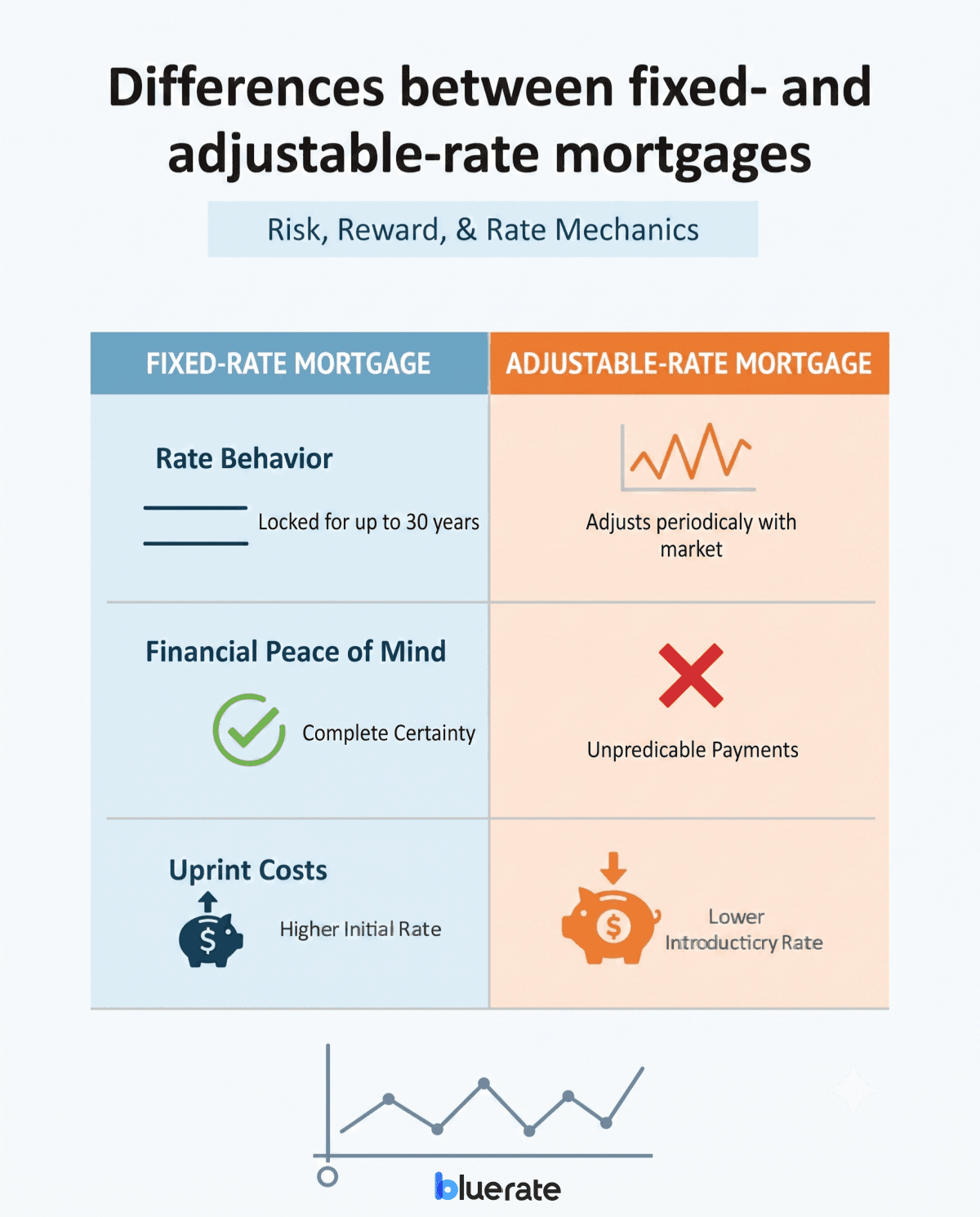

Differences between fixed- and adjustable-rate mortgages

The split between these two options comes down to risk, reward, and rate mechanics. Here is where they part ways:

- Rate behavior: A fixed-rate remains locked for up to 30 years, whereas an ARM adjusts periodically with the market after an initial term.

- Financial peace of mind: Fixed-rate loans offer complete certainty; ARMs require you to accept a level of monthly payment unpredictability.

- Upfront costs: ARMs give you a discount on your initial interest rate, while fixed mortgages carry a higher initial price tag for that peace of mind.

Which One to Choose? Adjustable or Fixed-Rate Mortgage?

Choosing between the two boils down to your personal timeline and comfort with market fluctuations. Here is the decision matrix I use with my clients:

Go with a Fixed-Rate if:

- You are moving into your "forever" home and plan to stay put for a decade or more.

- You prefer a predictable budget and want to avoid the anxiety of rising market rates.

Go with an ARM if:

- You are certain you will sell the home or refinance within the initial fixed period, such as 5 or 7 years.

- You expect your household income to grow substantially before the adjustment period kicks in.

- You want to maximize your short-term savings to tackle immediate home renovations.

Conclusion

Deciding on the perfect mortgage is deeply personal. There is no universally correct choice—only the one that aligns with your financial horizon and risk tolerance. If you want guaranteed safety, look at a fixed rate. If you want to optimize your short-term cash flow, an ARM is worth considering.

If you are still feeling unsure, I highly recommend getting a professional second opinion. At Bluerate, we can easily connect you with a licensed, expert loan officer right in your neighborhood. Our matching service is completely free, with zero pressure, helping you secure a tailored mortgage plan with confidence.