Max LTV: Learn the Limits by Loan Types

Scraping together a down payment is often the most stressful part of buying a house. Everyone wants to know: what's the absolute minimum cash I have to bring to the closing table? The answer lies in your Max LTV (Loan-to-Value) limit.

But there isn't a one-size-fits-all number. Your ceiling depends entirely on the specific loan type you choose. Sure, reading up on the rules helps, but taking the guesswork out of the equation is much safer. You can easily reach out to experienced, local loan officers at Bluerate for a free consultation to see exactly what you qualify for.

Key Takeaways

- Not all loans are equal: Government-backed options (like VA or USDA) can fund 100% of your home, while conventional mortgages usually max out around 97%.

- Appraisals rule the math: Your ratio is based on the appraised value or the purchase price---whichever happens to be lower.

- Personal finance matters: High credit scores and low debts are the real keys to unlocking these maximum limits.

What is a Max LTV?

In simple terms, a Maximum Loan-to-Value (LTV) ratio is the hard cap a bank sets on how much they are willing to lend you against a property's worth. Think of it as a lender's personal risk thermometer. They divide your loan amount by the home's value to get a percentage.

But here is a massive detail people miss: lenders always use the purchase price or the appraiser's valuation---whichever is lower. If you agree to buy a place for $400,000, but the appraiser says it's only worth $380,000, the bank uses that $380k to do the math. The higher your LTV climbs, the riskier the deal looks to the lender.

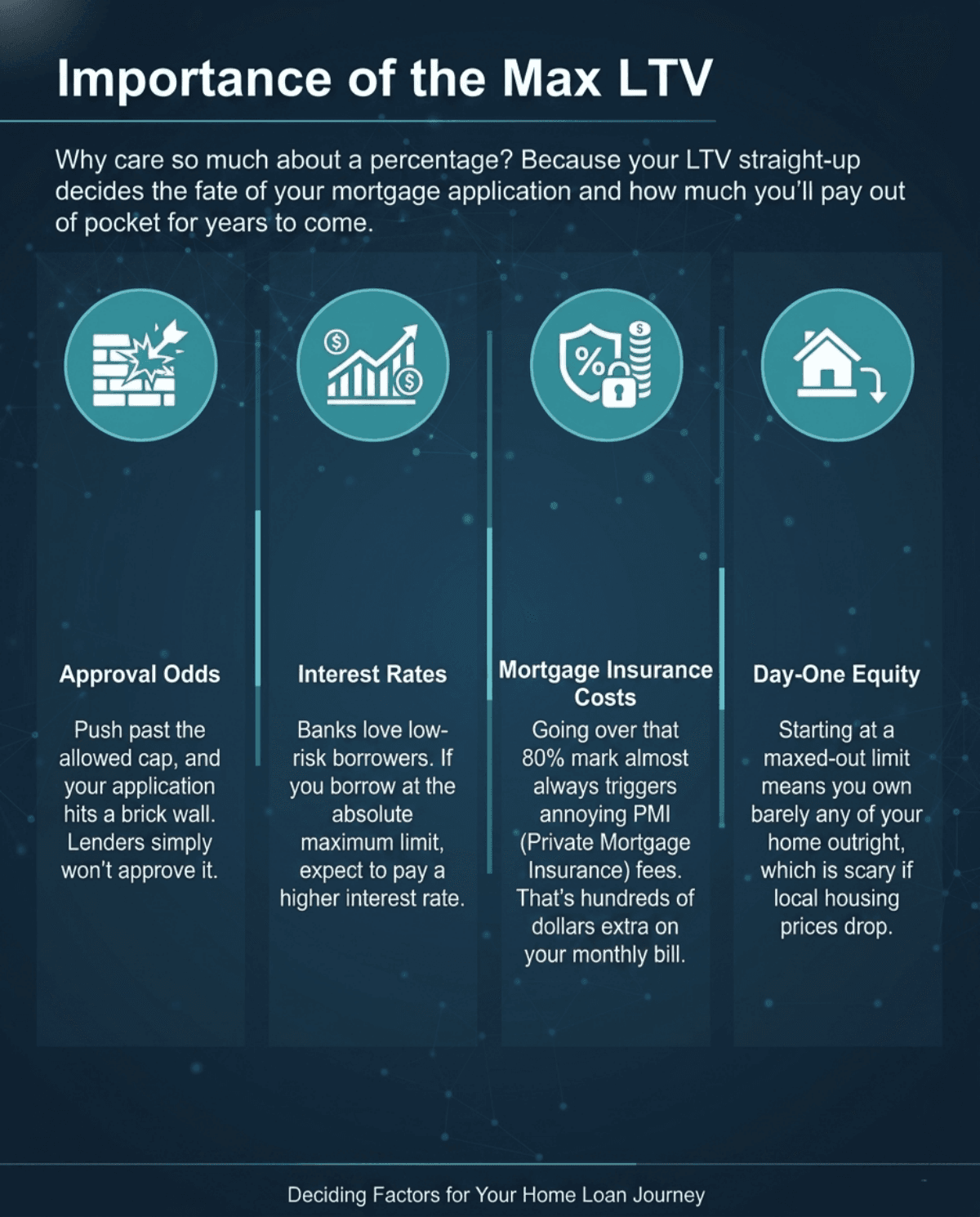

Importance of the Max LTV

Why care so much about a percentage? Because your LTV straight-up decides the fate of your mortgage application and how much you'll pay out of pocket for years to come.

- Approval Odds: Push past the allowed cap, and your application hits a brick wall. Lenders simply won't approve it.

- Interest Rates: Banks love low-risk borrowers. If you borrow at the absolute maximum limit, expect to pay a higher interest rate.

- Mortgage Insurance Costs: Going over that 80% mark almost always triggers annoying PMI (Private Mortgage Insurance) fees. That's hundreds of dollars extra on your monthly bill.

- Day-One Equity: Starting at a maxed-out limit means you own barely any of your home outright, which is scary if local housing prices drop.

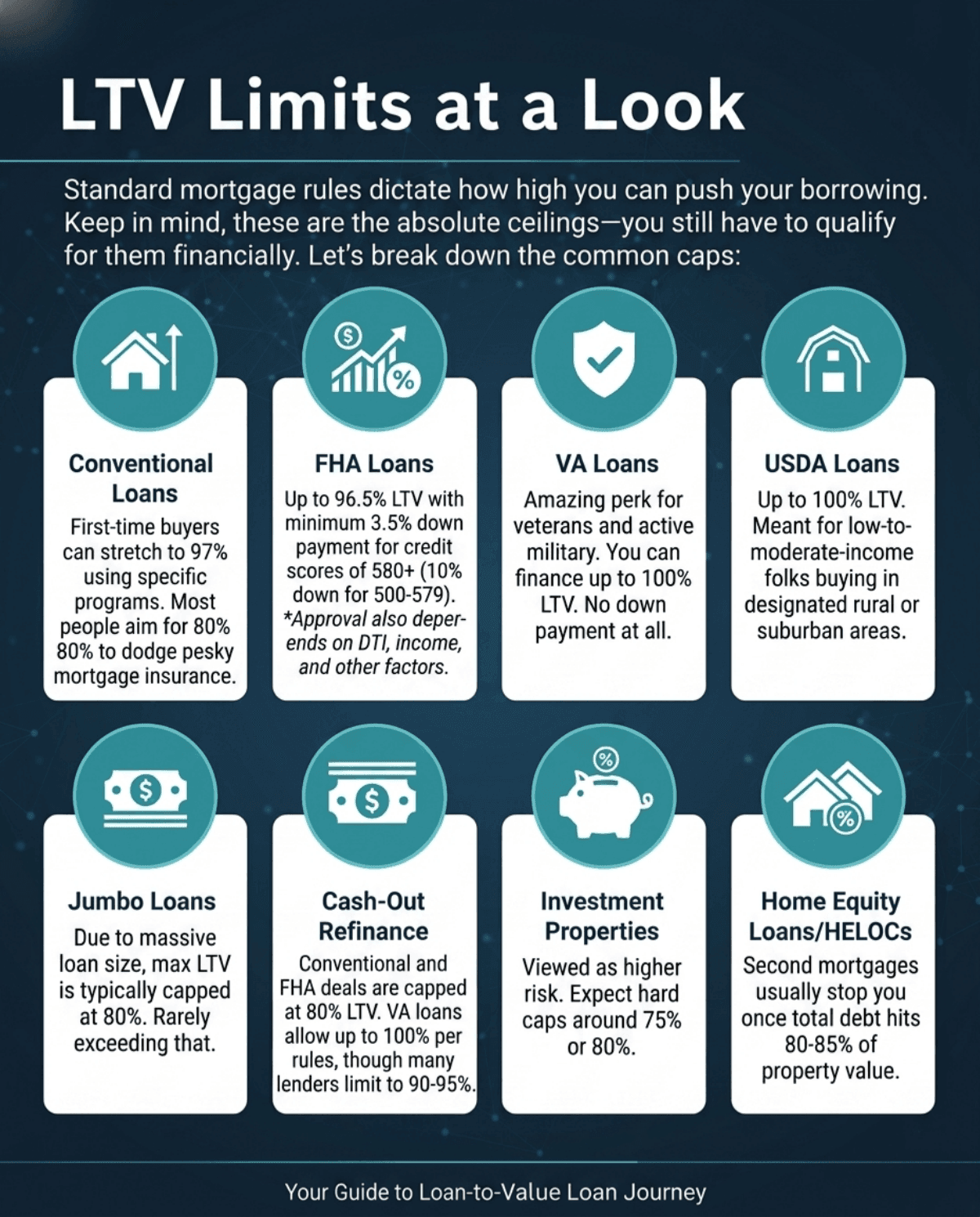

LTV Limits at a Look

Standard mortgage rules dictate how high you can push your borrowing. Keep in mind, these are the absolute ceilings---you still have to qualify for them financially. Let's break down the common caps:

- Conventional Loans: First-time buyers can stretch to 97% using specific programs. But honestly, most people try to aim for 80% so they can dodge that pesky mortgage insurance.

- FHA Loans: Extremely popular because they allow up to 96.5% LTV with a minimum 3.5% down payment for credit scores of 580 or higher (10% down required for 500-579). However, approval also depends on DTI, income, and other factors.

- VA Loans: An amazing perk for veterans and active military. You can finance up to 100% of the home's cost. No down payment at all.

- USDA Loans: Also allow 100% LTV. These are meant for low-to-moderate-income folks buying houses in designated rural or suburban areas.

- Jumbo Loans: Borrowing massive amounts of money makes banks nervous. Due to the size, maximum LTV is typically 80%, rarely exceeding that.

- Cash-Out Refinance: Want to tap your equity? Most conventional and FHA cash-out deals are strictly capped at 80%. VA loans allow up to 100% LTV per program rules, though many lenders limit to 90-95% based on overlays.

- Home Equity Loans/HELOCs: If you're taking out a second mortgage, lenders usually stop you once your total debt hits 80% or 85% of the property's value.

- Investment Properties: Buying a rental? You're viewed as a flight risk if things go south financially. Expect hard caps around 75% or 80%.

Factors that Affect Max LTV

Here is the reality check: just because a program allows a 97% ratio doesn't mean the lender will actually hand it to you. Banks are obsessed with managing default risk. Several things in your personal life can drastically lower your approved ceiling:

- Credit Score (FICO): Got a bumpy credit history? Lenders will definitely force you to put more money down, dropping your LTV.

- Debt-to-Income (DTI) Ratio: If your paycheck is already eaten up by car loans and credit cards, the bank won't let you borrow to the absolute max.

- Property Type: A standard single-family home gets the best terms. Condos or multi-family properties face way stricter limits.

- Loan Purpose: Buying a primary home gives you more leeway than pulling cash out of one you already own.

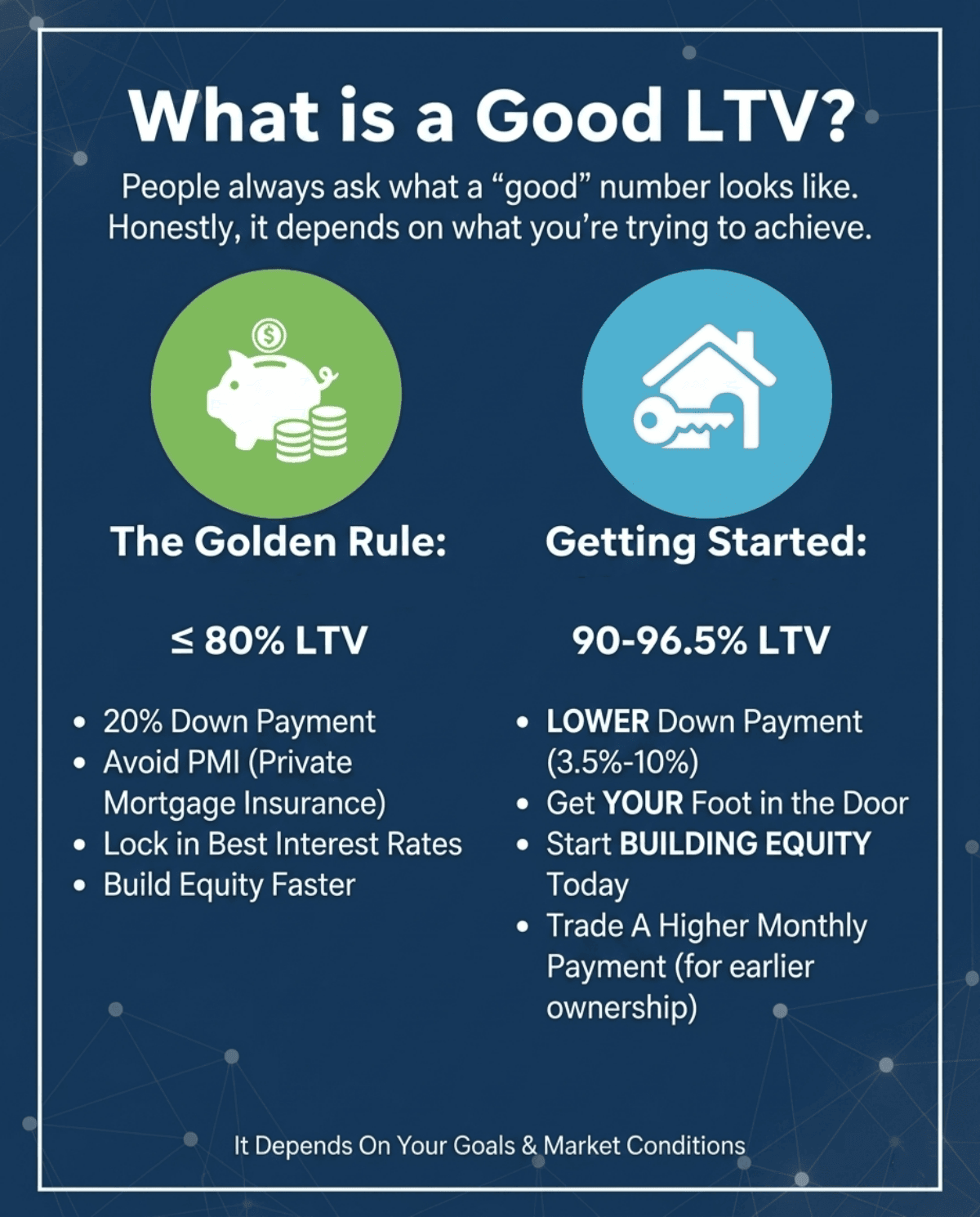

What is a Good LTV?

People always ask what a "good" number looks like. Honestly, it depends on what you're trying to achieve.

In traditional real estate circles, the golden rule is 80% or lower. Hitting that 80% mark means you've put down a solid 20%. You won't have to pay mortgage insurance, and you'll lock in the absolute best rates.

But let's be real for a second. Saving up a 20% down payment is brutal right now. For a lot of folks, especially first-time buyers, sitting around trying to hit 80% means watching housing prices skyrocket out of reach. In that case, a 90% or even 96.5% LTV is still fantastic. Why? Because it actually gets your foot in the door. You trade a slightly higher monthly payment for the chance to start building equity today.

FAQs About Max LTV

Q1. How do you calculate the Loan-to-Value ratio?

To estimate your LTV ratio, you can divide your loan amount by the home's appraised value (or purchase price, whichever is lower). Borrowing $240,000 on a $300,000 house equals 80% (or $240k ÷ $300k).

Q2. Can I get a mortgage with 100% LTV?

Yes. VA loans for veterans and USDA loans for designated rural homes allow 100% financing, meaning zero down payment if you qualify.

Q3. What happens if the home appraises for less than the purchase price?

Since lenders use the lower appraisal value, your LTV will spike. You must either pay the cash difference upfront or negotiate a lower price with the seller.

Q4. Does a lower LTV mean a better interest rate?

Almost always. More equity means less risk for the bank. They usually reward that safety with cheaper interest rates.

Q5. How can I lower my LTV?

Bring a larger down payment before closing. If you already have a mortgage, paying extra on your principal balance or waiting for your home's market value to appreciate will naturally lower the ratio.

Conclusion

Figuring out your Max LTV completely shapes your homebuying timeline. Whether you're trying to hit that 80% sweet spot on a conventional mortgage to drop PMI, or leaning on a 96.5% FHA loan to get keys in your hand faster, these rules dictate your budget.

But honestly, balancing these ratios with your credit score and monthly cash flow gets incredibly confusing. You shouldn't do the guesswork alone. Head over to Bluerate to connect with knowledgeable, local loan officers. It's totally free to chat with them, and they can pinpoint the exact loan type and maximum limits that actually make sense for your financial situation.