Explained: What is a USDA Loan? Types, Requirements & FAQs

If saving up for a 20% down payment feels impossible right now, I completely understand. I've been there. You might think your only option is to keep renting, but that's where the USDA loan comes in as a game-changer. It's one of the last remaining true "zero-down-payment" mortgage programs in the country, backed by the U.S. Department of Agriculture.

And here's the best part: you don't need to buy a working farm to qualify. Many suburban neighborhoods just outside city limits are eligible, but not all of them automatically qualify. You must verify your specific address using the official USDA eligibility map.

Let's explore how this hidden gem of a mortgage can help you buy a home sooner than you thought.

Key Takeaways

Before we dive into the details, here are the core highlights you need to know:

- $0 Down Payment: You can finance 100% of the home's purchase price.

- Location Restrictions: Properties must be in USDA-approved rural or suburban areas.

- Income Limits Apply: Your household income cannot exceed 115% of the local median income.

- Lower Fees: Mortgage insurance costs are significantly cheaper than FHA alternatives.

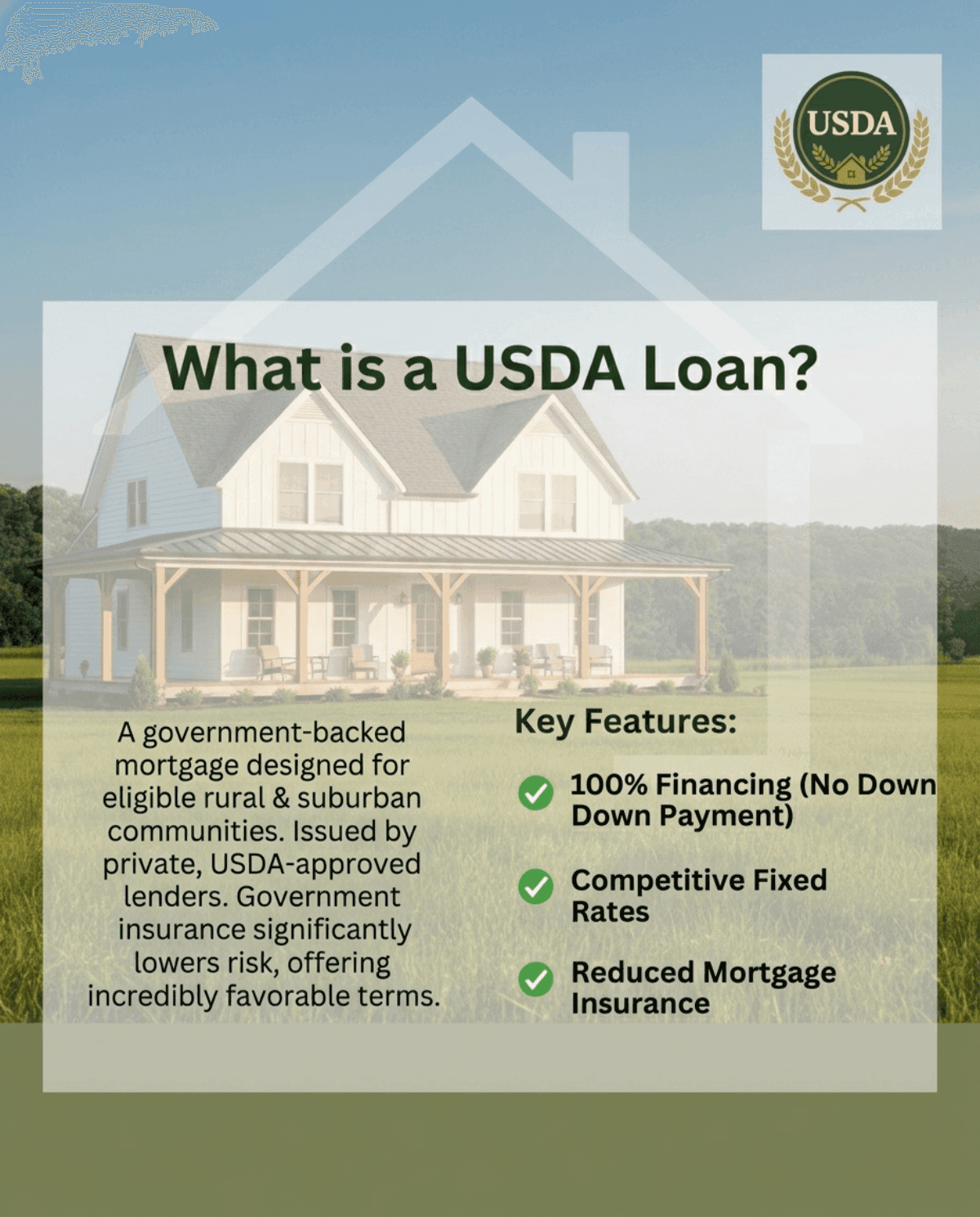

What is a USDA Loan?

A USDA loan is a government-backed mortgage designed to promote homeownership and development in eligible rural and suburban communities across the United States. While the U.S. Department of Agriculture's Rural Development program creates the guidelines, I want to clarify a common misconception: the government isn't usually the one lending you the cash. Instead, most of these mortgages are issued by private, USDA-approved lenders.

Because the government insures a portion of the loan, it significantly lowers the risk for these private banks. As a result, they can offer you incredibly favorable terms.

Here are the standout features you get with this program:

- 100% Financing: Absolutely no down payment is required.

- Competitive Fixed Rates: Because of the federal backing, interest rates are often lower than conventional options.

- Reduced Mortgage Insurance: The fees are much more affordable than the private mortgage insurance (PMI) you'd pay on a standard loan.

How Does a USDA Loan Work?

The secret to how a USDA loan works lies in its "government-backed" nature. By guaranteeing the mortgage, the USDA takes on the risk if a borrower defaults, which is exactly why lenders feel safe giving you a 0% down payment.

However, this protection isn't completely free. To fund the program, the USDA charges what they call a Guarantee Fee, which acts as your mortgage insurance. It comes in two parts:

- Upfront Fee: Currently set at 1% of the total loan amount. The good news? You don't have to pay this out of pocket. It can be rolled directly into your mortgage balance.

- Annual Fee: This is 0.35% of your remaining principal balance, divided by 12, and added to your monthly mortgage payment.

These fees are substantially cheaper than FHA premiums, saving you money every single month.

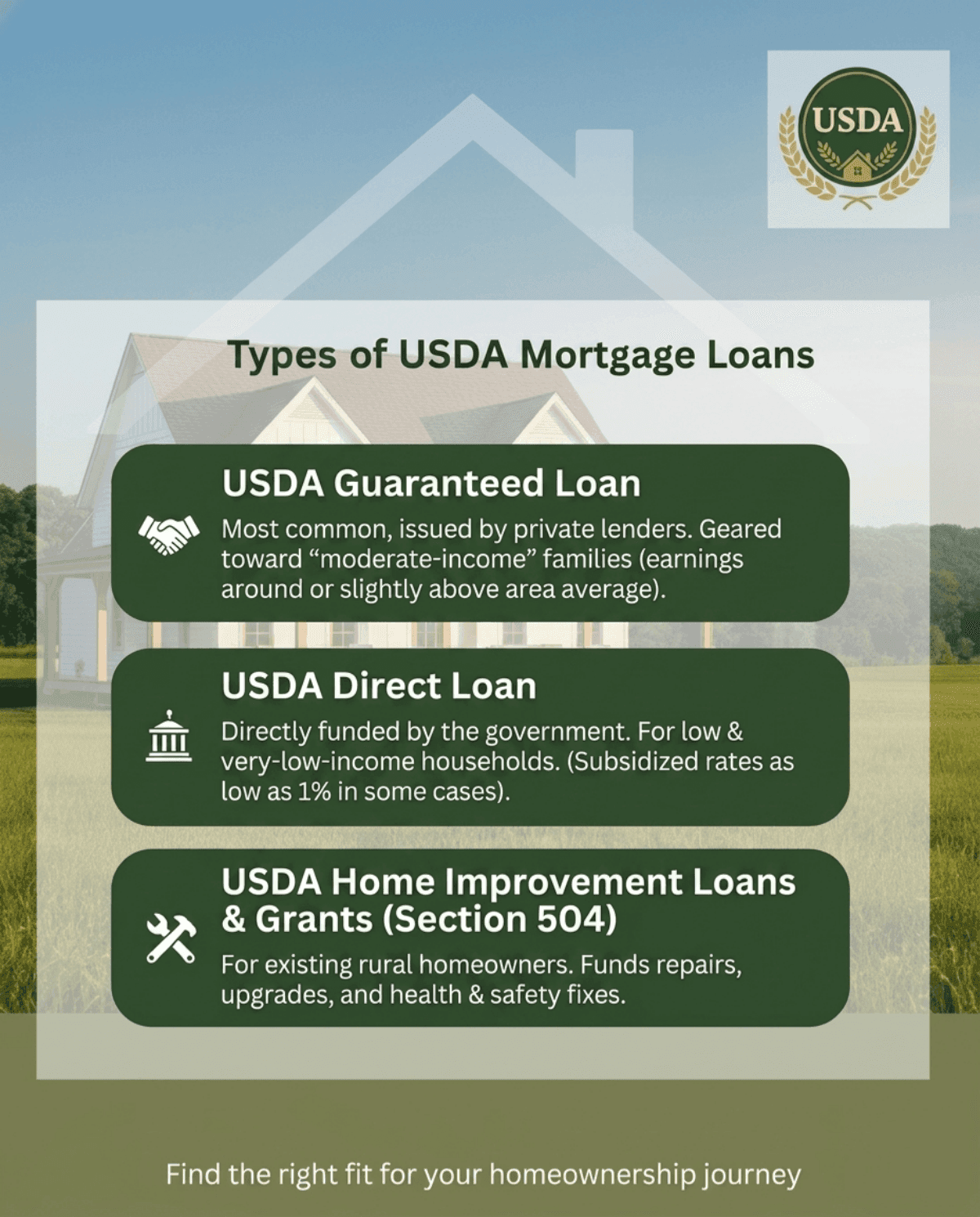

Types of USDA Mortgage Loans

Not all USDA loans are the same. Based on your household income and what you plan to do with the property, the program is split into three distinct categories.

- USDA Guaranteed Loan: This is the most common option. It's issued by private lenders and is geared toward "moderate-income" families. If your earnings are around or slightly above average for your area, this is likely the one you'll use.

- USDA Direct Loan: This one is funded directly by the government. It's specifically designed for low and very-low-income households who cannot secure financing anywhere else. In some cases, interest rates can be subsidized down to as low as 1%.

- USDA Home Improvement Loans & Grants (Section 504): If you already own a home in an eligible area, this program provides funding to repair, upgrade, or remove health and safety hazards.

Knowing exactly which bucket you fall into is the first critical step to getting approved.

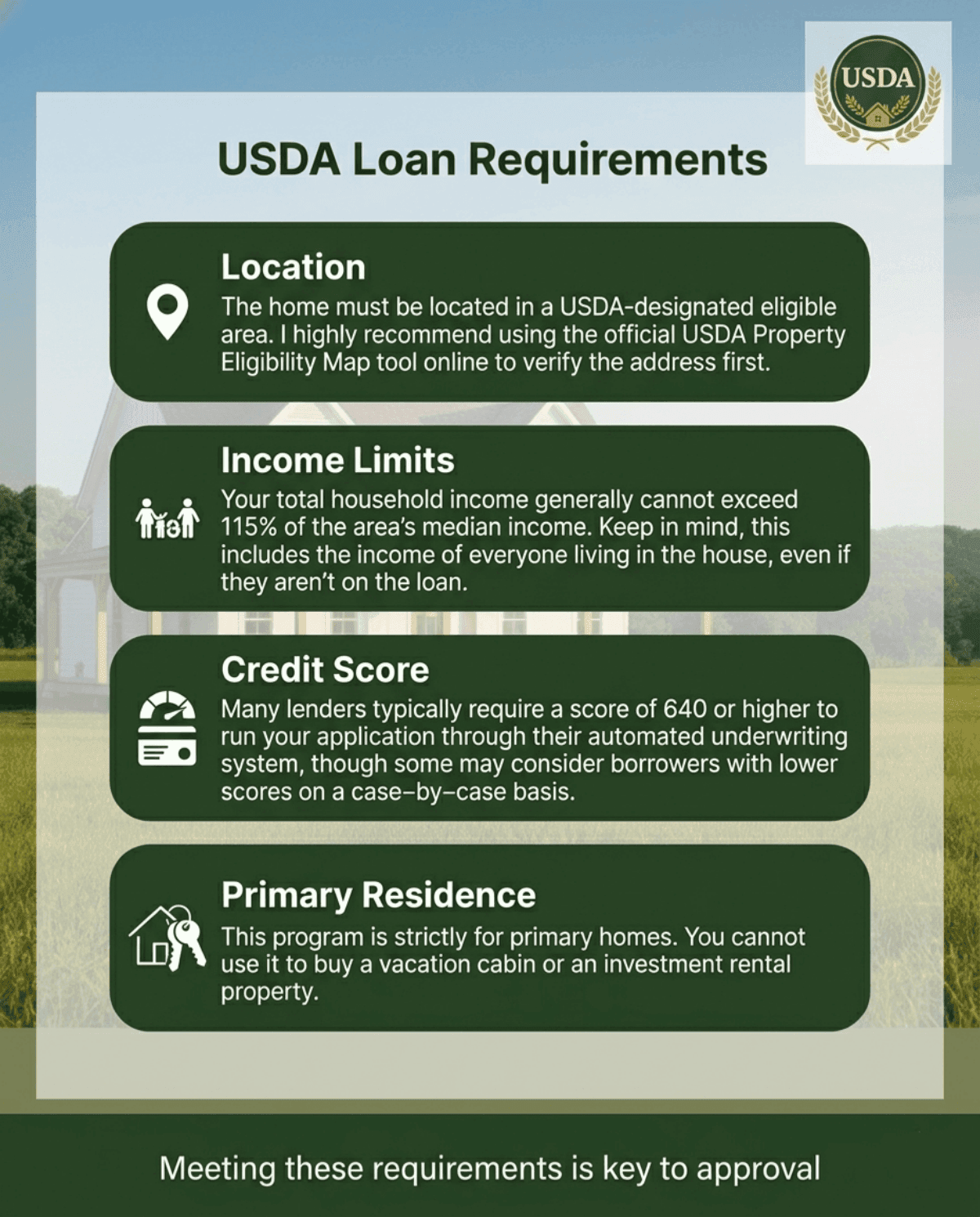

USDA Loan Requirements

While the perks are incredible, the entry barriers are strict. From my experience, you have to hit four non-negotiable requirements to get approved:

- Location: The home must be located in a USDA-designated eligible area. I highly recommend using the official USDA Property Eligibility Map tool online to verify the address first.

- Income Limits: Your total household income generally cannot exceed 115% of the area's median income. Keep in mind, this includes the income of everyone living in the house, even if they aren't on the loan.

- Credit Score: Many lenders typically require a score of 640 or higher to run your application through their automated underwriting system, though some may consider borrowers with lower scores on a case‑by‑case basis.

- Primary Residence: This program is strictly for primary homes. You cannot use it to buy a vacation cabin or an investment rental property.

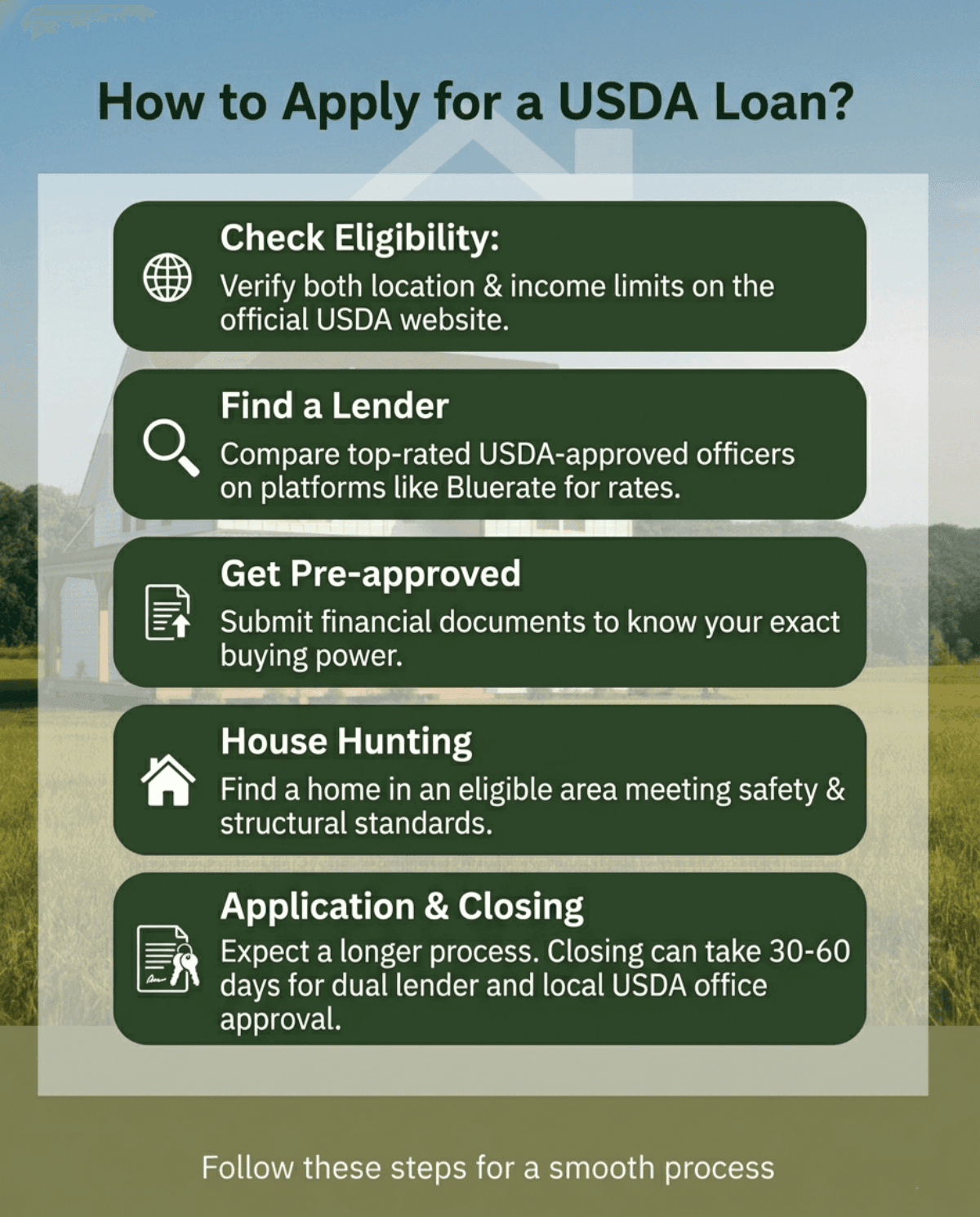

How to Apply for a USDA Loan?

Getting a USDA loan takes a little more paperwork than a conventional mortgage, but the process is highly manageable if you follow these steps:

-

Check Eligibility: Before doing anything, verify both your target location and household income limits on the official USDA website.

-

Find a Lender: Not all banks handle rural housing loans. You can easily compare top-rated USDA loan officers for free on platforms like Bluerate to find the best rates without the hassle.

-

Get Pre-approved: Submit your financial documents to your chosen lender so you know exactly your buying power.

-

House Hunting: Find a home within the eligible boundary lines that meets the USDA's safety and structural standards.

-

Application Period & Closing: Expect this to take a bit longer. Because your file needs approval from both your private lender and the local USDA office, closing can take between 30 to 60 days.

Also Read: 2026 List of USDA-Approved Lenders: Best Choices to Pick

FAQs About USDA Loans

Q1. Why is a USDA loan better?

It's superior because it requires $0 down and offers highly competitive interest rates. Plus, the USDA's annual guarantee fee (0.35%) is significantly cheaper than the mortgage insurance premiums (MIP) required by FHA loans, making your monthly payments much more affordable overall.

Also Read: USDA Loan vs FHA Loan: Which is Your Best Fit?

Q2. What is the maximum income for a USDA loan?

There isn't a single national limit. The cap is generally 115% of the local median income and varies by family size. For example, the standard income limit for a 1-to-4 person household is $119,850, while for a 5-to-8 person household it is $158,250, with higher limits in some high‑cost metro areas.

Q3. What disqualifies you from a USDA loan?

You will be disqualified if your household income exceeds the local limit or if the property is located within an ineligible urban center. Additionally, buying a home to rent it out, or purchasing a property whose primary purpose is an active, income‑producing farm, will generally result in an immediate denial.

Q4. What is the 20% rule for USDA?

This rule is often misunderstood. It reflects the idea that if your liquid assets are substantial enough that you could comfortably make a 20% down payment on a conventional mortgage, a lender may question whether you really need a USDA zero‑down loan and could decide to place you on a different program.

Q5. Do USDA loans have PMI?

No, they don't have Private Mortgage Insurance (PMI). Instead, they charge a "Guarantee Fee." This includes a 1% upfront charge, which is usually rolled into the total mortgage, and a 0.35% annual fee that is broken down and added to your monthly mortgage payment.

Conclusion

Navigating the mortgage market can feel overwhelming, but a USDA loan remains one of the most powerful tools available for middle-income homebuyers. If you want to escape the rent trap without draining your savings account, this 0% down payment solution is hard to beat. Just remember to double-check that eligibility map and keep an eye on those income limits.

Ready to make your homeownership dream a reality? Navigating USDA lenders can be tricky, but Bluerate.ai makes it completely effortless. You can compare experienced loan officers today, secure the best rates, and confidently get started on your journey home.