How to Compare Mortgage Rates? Tips for First-Time Homebuyers

When I bought my first place, my head was spinning looking at online rate tables. Like most first-time buyers, I thought grabbing the absolute lowest percentage was the ultimate goal. I quickly learned that a cheap interest rate can hide massive, upfront fees that wipe out any savings. This guide shares exactly what I wish someone had told me back then so you can compare offers like a pro.

Key Takeaways

- Focus on APR: The APR reflects your interest rate plus certain lender fees and upfront costs, giving a broader (but not complete) picture of the loan's annual cost.

- Collect 3+ Loan Estimates: Hard evidence is better than quotes. Actual written estimates reveal hidden charges.

- Use Smart Matching: Find verified local lenders with privacy-focused tools that won't sell your phone number to spammers.

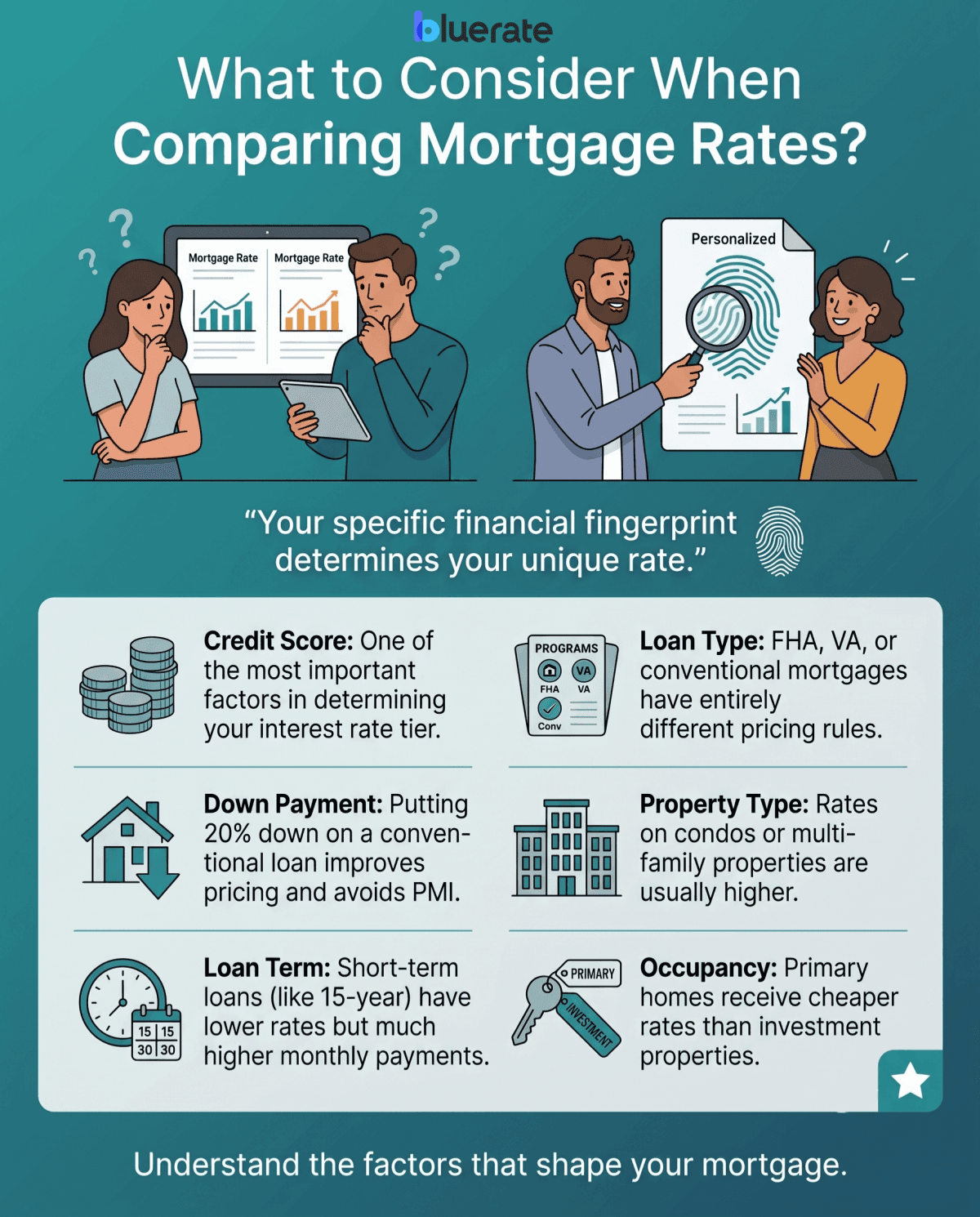

What to Consider When Comparing Mortgage Rates?

I used to think lenders handed out the same standard rates to everyone. The truth is, mortgage pricing is highly personal. Lenders build your quote based on your specific financial fingerprint. Here are the core factors they look at to decide your rate:

- Credit Score: One of the most important factors in determining your interest rate tier.

- Down Payment: Putting 20% down on a conventional loan usually improves pricing and avoids private mortgage insurance (PMI), though rules differ for FHA and VA loans.

- Loan Term: Short-term loans (like 15-year) have lower rates but much higher monthly payments.

- Loan Type: Programs like FHA, VA, or conventional mortgages have entirely different pricing rules.

- Property Type: Rates on condos or multi-family properties are usually higher than single-family homes.

- Occupancy: You will always get a cheaper rate for a primary home than an investment property.

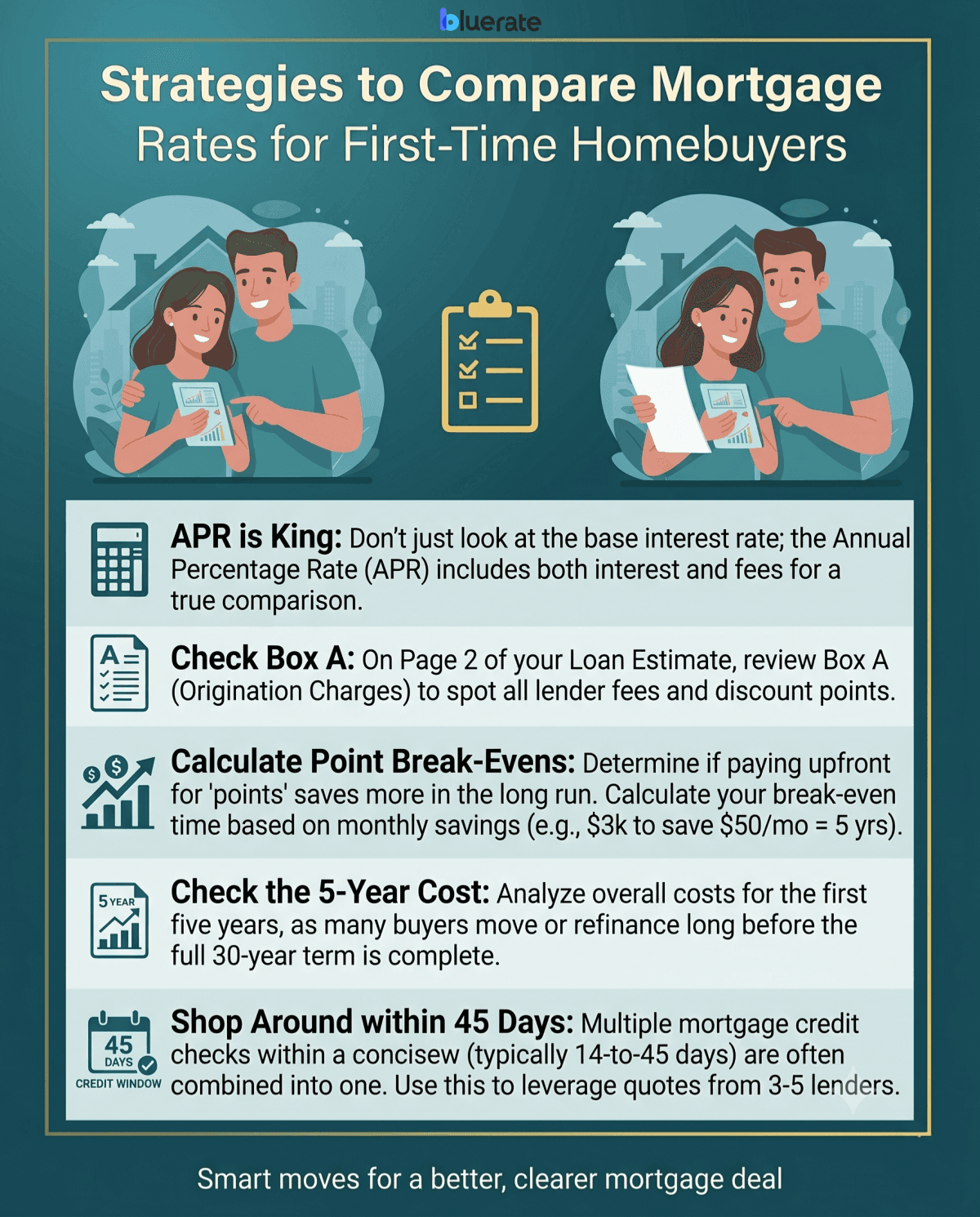

Strategies to Compare Mortgage Rates for First-Time Homebuyers

Don't trust basic rate sheets on lender websites. To actually get a good deal, you have to look at the paperwork. Here are the steps I use to compare offers:

- APR is King: Don't just look at the base interest rate. The Annual Percentage Rate (APR) includes both the interest rate and the fees. If Loan A has a 6.0% rate with high fees, and Loan B has 6.1% with zero fees, Loan B might actually be cheaper in the long run.

- Check Box A on Your Loan Estimate: Legally, lenders must send you a standard Loan Estimate. Flip directly to Page 2 and look at Box A (Origination Charges). These are the lender's origination charges, including items like underwriting, processing, and any discount points. This is where you spot who is overcharging you.

- Calculate Point Break-Evens: Lenders often ask you to pay "points" upfront to buy down your interest rate. If they charge $3,000 for a point to save you $50 a month, it will take you 60 months (5 years) just to break even. If you plan to move before then, reject the points.

- Check the 5-Year Cost: Look at the overall costs you will pay in the first five years. Many buyers move or refinance before their 30-year term is up.

- Shop Around within 45 Days: Credit bureaus let you shop around for a mortgage without hurting your credit score. If you get all your credit checks within a limited window (typically** 14 to 45 days**, depending on the credit scoring model), they are often treated as a single inquiry. Use this to get quotes from** 3 to 5 different lenders **to leverage the best deal.

What is the Best Way to Compare Mortgage Rates?

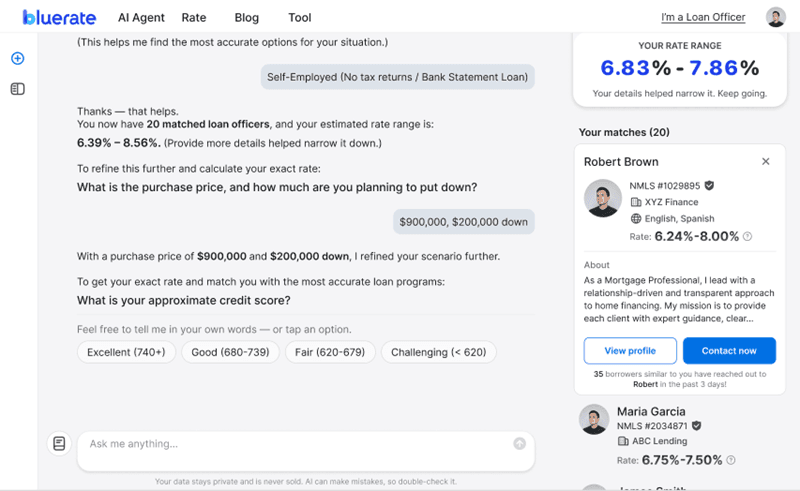

If you have ever filled out a rate comparison form online, you probably know the nightmare that follows: your phone starts ringing off the hook with dozens of pushy lenders. I hate that. That is why I recommend Bluerate. It is a US-focused marketplace built to protect your privacy while matching you with top local loan officers.

Their secret weapon is the Bluerate AI Agent, an interactive chat assistant that acts like a neutral guide. It helps you get accurate rate quotes and matches you with verified professionals. Here is what makes it stand out:

- Personalized Real-Time Quotes: It pulls actual rates from over 100 lenders for condos, townhomes, and single-family houses.

- Local Specialist Matches: It connects you with loan officers who specialize in your specific loan program, whether it is FHA, VA, or non-QM.

- Spam-Free Experience: Your contact details are kept private. You get to decide when and who to contact.

FAQs About Mortgage Rate Comparison

Q1. Will looking for rates hurt my credit score?

No. While credit bureaus run a "hard check" to give you an official estimate, credit models treat all mortgage-related inquiries within a limited window (typically 14 to 45 days depending on the credit scoring model), they are often treated as a single inquiry. You can shop around without hurting your score.

Q2. Why is the APR different from the advertised rate?

The advertised rate is just the interest on the principal. The APR is a more comprehensive measure of cost because it includes the interest rate plus certain fees, but it does not capture every expense involved in the loan.

Q3. How many quotes should I actually get?

Aim for at least three to five Loan Estimates. Getting multiple written offers not only shows you who is charging the lowest fees but also gives you leverage to negotiate.

Q4. Should I pay extra fees to lock my rate?

A mortgage rate lock keeps your interest rate from rising before you close on the house. Many lenders offer a **30- to 45-day **rate lock once you are under contract, though the cost may be built into the pricing.

Q5. Is it worth buying points to lower my rate?

Only if you plan to stay in the home for a long time. Calculate your monthly savings and divide it by the upfront cost of the points to find your break-even month. If you will move before then, skip them.

Final Word

Getting your first set of keys is an incredible feeling, but you have to do the legwork upfront to protect your wallet. Comparing rates is easily the most rewarding step in the whole homebuying process.

Don't let pushy salespeople rush you, and don't settle for the first quote you get. Try using the Bluerate AI Agent—it is a free, secure, and stress-free way to explore your options, lock in competitive rates, and meet local experts on your own terms.

People Also Read

- What is Break Even Point in Mortgage? Learn Here

- Mortgage Interest Rate vs. APR: What's the Difference?

- When to Lock in a Mortgage Rate: A Loan Officer's Guide

- Guide: How to Lock in a Mortgage Rate?

- [[Explained] What is a Float Down Option on Mortgage?](https://www.bluerate.ai/blog/float-down-option)