Commercial Bridge Loan Explained: Definition, Pros & Cons, When

If you've ever found a perfect commercial property but realized the "bank clock" moves way slower than the "market clock," you've felt the frustration of a funding gap. I've seen many investors lose out on prime deals because traditional underwriting took 90 days while the seller wanted to close in 30. That is exactly where a commercial bridge loan comes in.

It's a short-term, fast-acting financial tool designed to "bridge" the gap between your immediate need for cash and a long-term solution. If you're currently eyeing a time-sensitive deal, I recommend you consult with local loan officers for free on Bluerate to see what your specific numbers look like before the window closes.

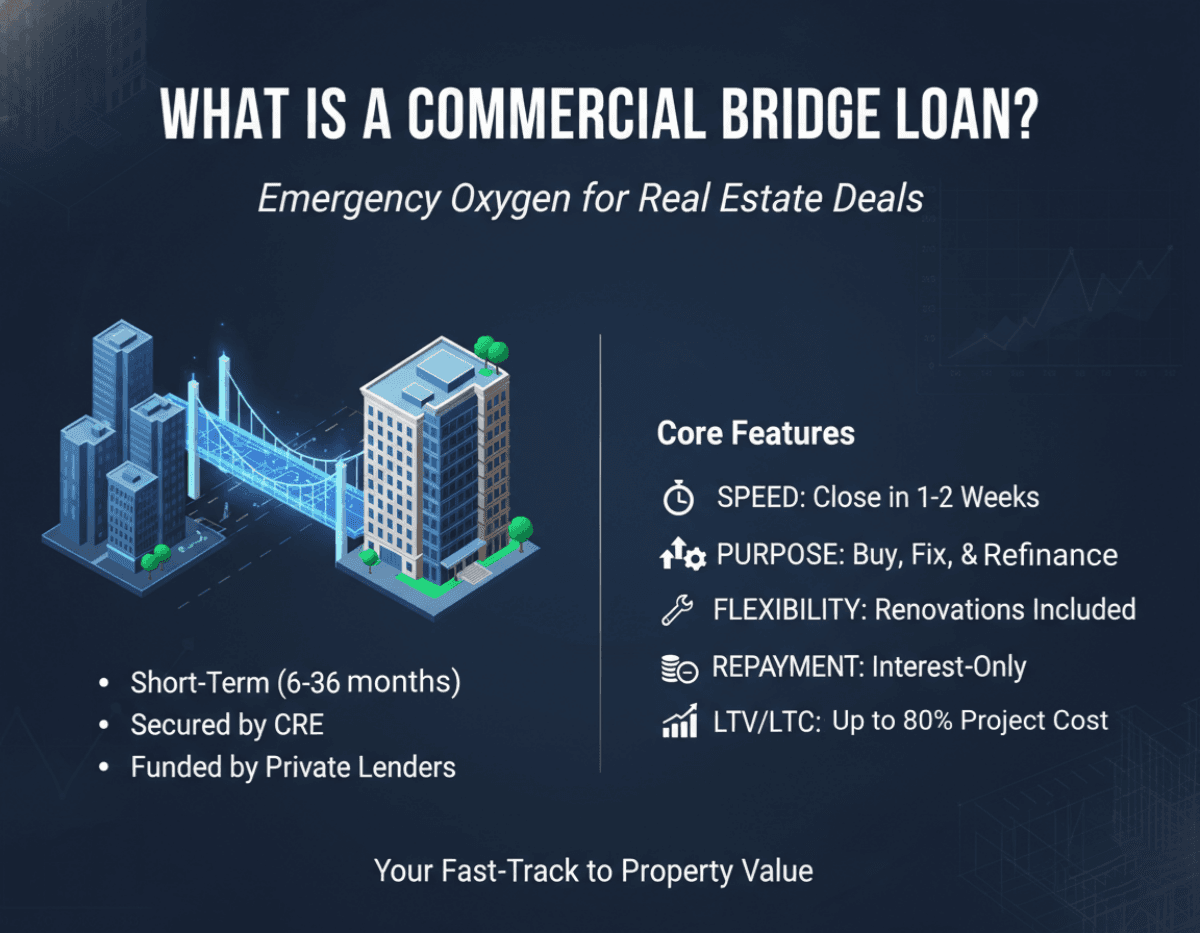

What is a Commercial Bridge Loan?

In my years of navigating the US debt markets, I've come to view bridge loans as the "emergency oxygen" for real estate deals. Technically, it is a short-term loan, typically ranging from 6 to 36 months, secured by commercial real estate. Unlike a standard mortgage from a big bank, these are usually funded by private or "hard money" lenders who care more about the property's potential than your personal tax returns from three years ago.

Based on current market trends, here are the core features you'll encounter:

- Speed: You can often close in 1 to 2 weeks, whereas a CMBS or bank loan might take 3 to 4 months.

- Purpose: These aren't for long-term "buy and hold." They are for "buy, fix, and refinance."

- Flexibility: Lenders are often willing to wrap renovation costs into the loan.

- Repayment: Most are interest-only, meaning your monthly overhead stays lower while you improve the asset.

- LTV (Loan-to-Value): Usually, you're looking at 65% to 80% LTV. However, many lenders now focus on LTC (Loan-to-Cost), sometimes covering up to 85% of the total project cost if the math makes sense.

Who is a Commercial Bridge Loan for?

This isn't a product for the risk-averse or the "mom-and-pop" residential landlord. From what I've seen on the ground, this is a tool for:

- Value-Add Investors: Those buying "ugly" buildings or under-managed offices that need a face-lift before a bank will touch them.

- Opportunity Hunters: If you're buying a property at a foreclosure sale or a quick auction, you need cash yesterday.

- Sellers in Transition: Owners who need to unlock equity from one property to buy another before the first one has even sold.

- Credit-Challenged Borrowers: If your credit score took a hit but you have a high-equity property, bridge lenders will often look past the score if the Exit Strategy is solid.

How Do Commercial Bridge Loans Work?

The mechanics are different from your home mortgage. First, the bridge loan lender evaluates the "As-Is" value versus the "After-Repair Value" (ARV).

The process usually follows this flow: You submit your deal, the lender does a "light" underwrite on your experience and a "heavy" underwrite on the property's cash flow (or potential cash flow). The loan amount is calculated based on the asset's value. For example, if you're buying a $1M warehouse, a lender might give you $750,000 (75% LTV).

Expect interest rates to be higher, currently ranging from 5.75% to 12.75% in the US, depending on the Fed's latest moves and your risk profile. You'll also pay "points" (1-3% of the loan amount) at closing. The most critical part of the "how" is the Exit Strategy: you must prove to the lender how you will pay them back, usually through a sale or a "take-out" permanent refinance.

Pros and Cons of Commercial Bridge Loans

I always tell my clients: bridge loans are a great servant but a terrible master.

Pros:

- Agility: You can compete with "all-cash" buyers.

- Minimal Paperwork: Compared to the SBA or big banks, the documentation is significantly lighter.

- Property Improvement: It provides the capital to turn a non-performing asset into a "stabilized" one.

Cons:

- Expense: Between the 10% interest and the origination fees, this is expensive capital.

- Maturity Risk: If the market dips or your renovation takes too long, and the loan expires, you could face foreclosure or heavy extension fees.

- Short Fuse: You are always on the clock. There is no "set it and forget it" with bridge debt.

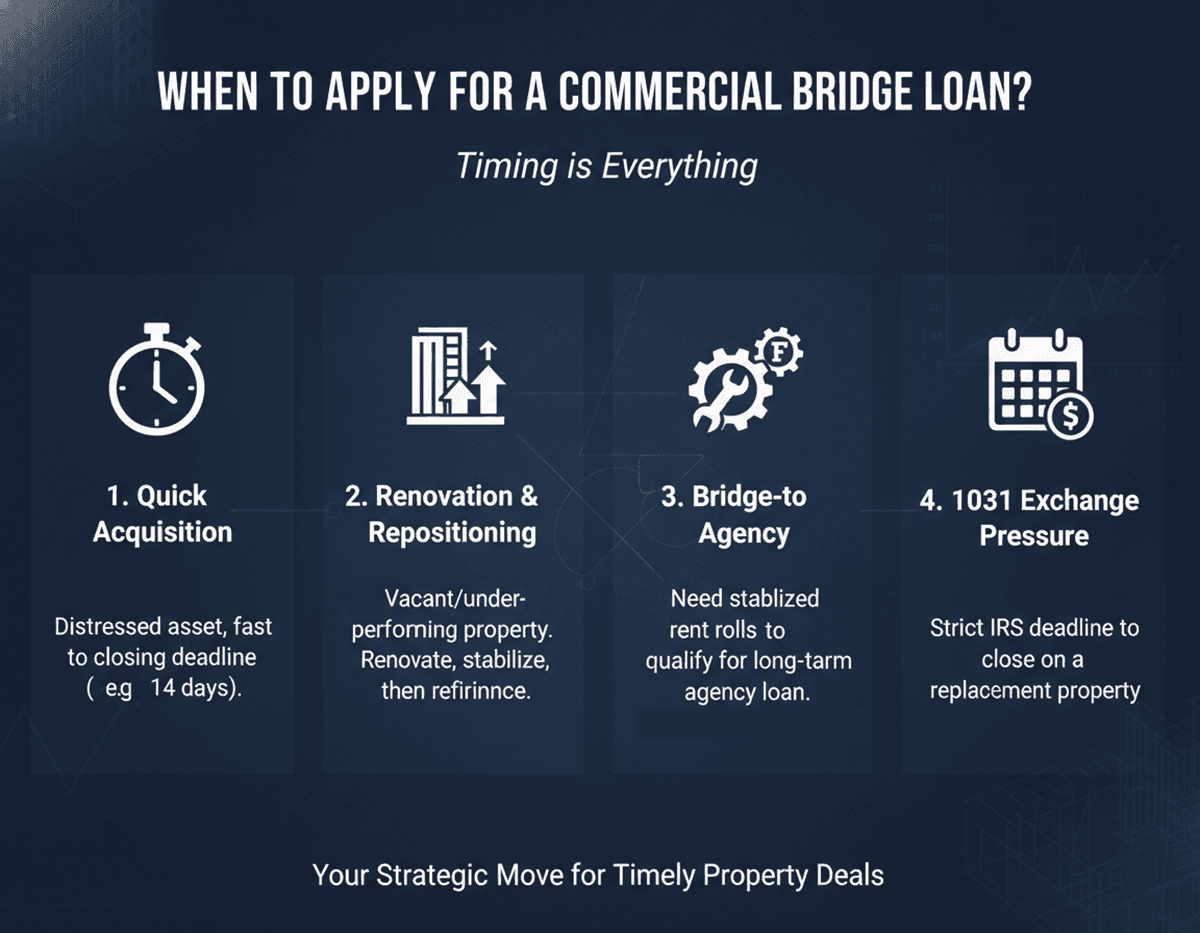

When to Apply for a Commercial Bridge Loan?

Timing is everything. In my experience, there are four specific scenarios where a bridge loan is the smartest move on the board:

- Quick Acquisition: You found a distressed asset, and the seller will give you a $200k discount if you close in 14 days.

- Renovation & Repositioning: The building is currently 40% vacant. A bank won't lend on it because it doesn't "DSCR" (Debt Service Coverage Ratio). You use a bridge loan to renovate, fill the units, and then move to a bank loan.

- Bridge-to-Agency: You're waiting to qualify for a low-interest Fannie Mae or Freddie Mac "Agency" loan, but you need a year of "stabilized" rent rolls first.

- 1031 Exchange Pressure: You have a strict IRS deadline to identify and close on a replacement property and can't wait for traditional bank red tape.

Expert Tip: Never sign a bridge loan without a clear "Plan B" for your exit. If your plan is to refinance, make sure you know exactly what cap rates and DSCR requirements banks are looking for today. To get a head start on your strategy, you can consult with local loan officers for free on Bluerate to compare current market terms.

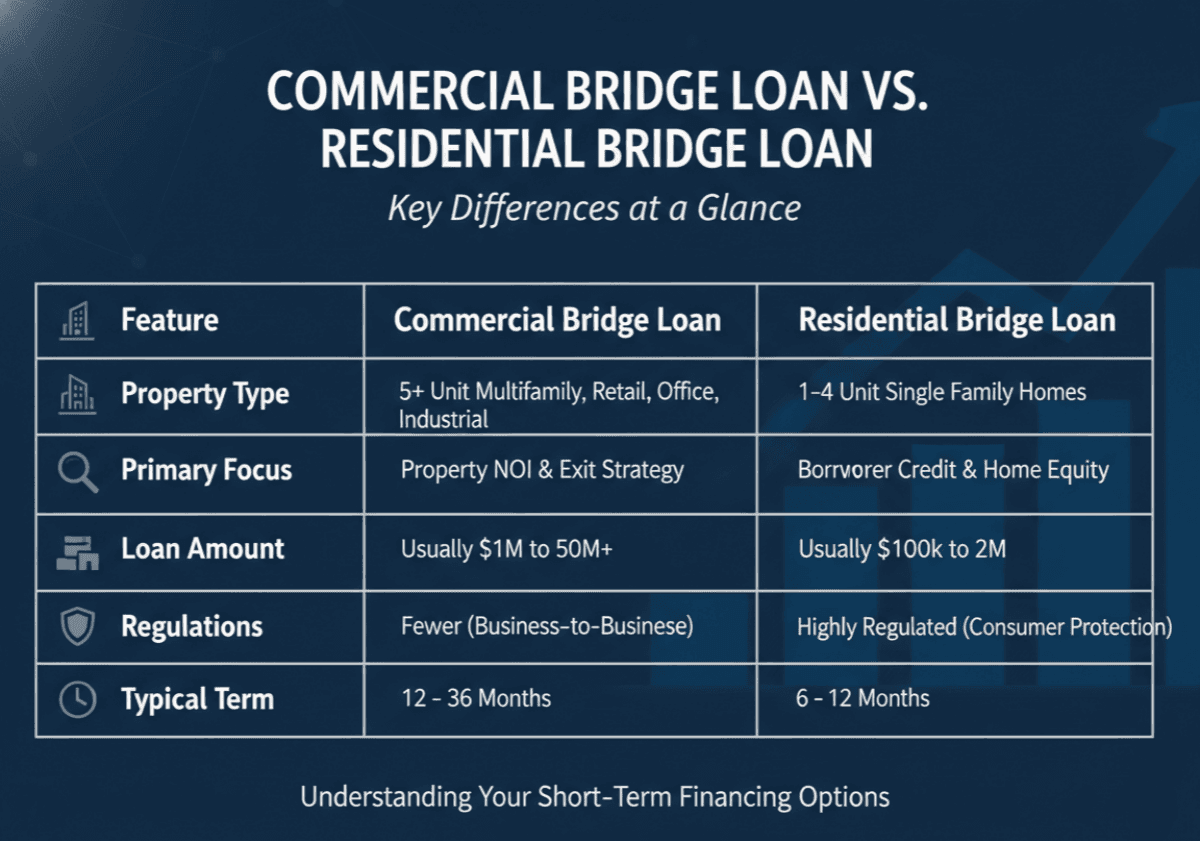

Commercial Bridge Loan vs. Residential Bridge Loan

While they share a name, they are different beasts. Residential bridge loans usually rely on your personal DTI (Debt-to-Income) and 1-4 unit properties. Commercial bridge loans are purely business-purpose.

FAQs About Commercial Bridge Loan

Q1. What are current interest rates for commercial bridge loans in the US?

As of 2026, expect rates between 5.75% and 12.75%. Top-tier borrowers with high-quality assets might see slightly lower, while "heavy-lift" renovations stay on the higher end.

Q2. Can I get a bridge loan with a 600 credit score?

Yes. Most bridge lenders are "asset-based." If the property has enough equity and a clear path to value-add, your personal credit is secondary to the deal's viability.

Q3. How fast can I actually get the money?

While some claim "days," a realistic timeline for a quality lender is 7 to 14 days. The appraisal and environmental reports are usually the "speed limit."

Q4. Are there prepayment penalties?

It depends. Many bridge loans have a "minimum interest" clause (e.g., at least 6 months of interest), but many allow you to exit early once the property is stabilized.

Q5. What is an "Exit Strategy" and why do I need one?

It is your plan to pay off the loan. Lenders won't give you a short-term loan unless they see exactly how you'll get into a long-term loan or sell the asset.

Final Word

Commercial bridge loans are the "Swiss Army Knife" of real estate finance. They aren't meant to be your permanent mortgage, but when used correctly, they allow you to seize opportunities that others have to pass on. My best advice? Don't just look at the interest rate. Look at the lender's reputation for closing on time and their flexibility if your project hits a snag. Commercial real estate is a relationship business.