Bridge Loans Explained: Every Detail You Want to Know in 2026

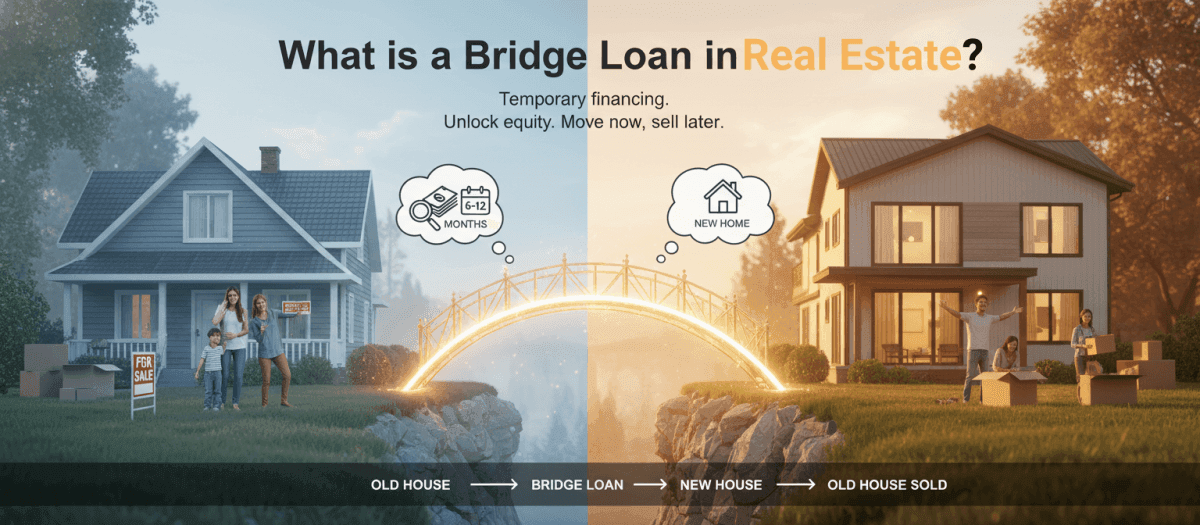

What is a bridge loan? Simply put, it is a short-term financing tool designed to "bridge" the financial gap between buying a new property and selling your current one. Instead of waiting months for your old house to sell, you can tap into its equity immediately to fund your next down payment.

In today's fast-moving 2026 real estate market, timing is everything. However, before jumping into any financial commitment, getting a free consultation with a licensed loan officer in your local neighborhood is the smartest first step to see if this product actually fits your needs.

Definition: What is a Bridge Loan in Real Estate?

During my years as a mortgage expert, I have noticed that many buyers feel stuck when they find their dream home but haven't sold their current residence. A bridge loan solves this exact problem. It acts as temporary financing, typically lasting anywhere from 6 to 12 months, using the equity tied up in your existing house as collateral.

The primary audience for this type of mortgage includes two main groups. First, everyday homeowners who want the convenience of moving into a new place before packing up and listing the old one. Second, real estate investors who need rapid capital to acquire a fix-and-flip property or secure an off-market deal before securing long-term financing. Because it is designed purely for transition, the focus is on speed and accessing equity rather than a 30-year commitment. Also Read: Commercial Bridge Loan Explained: Definition, Pros & Cons, When

How Does a Bridge Loan Work?

The mechanics of bridging finance might sound complicated, but it generally boils down to how much you currently owe on your home. Depending on your Bridge Loan lender, the process works in one of two main ways:

-

Holding Two Mortgages: If you already have a substantial first mortgage, the lender simply adds a second loan on top of it. This new lump sum covers the down payment for your upcoming purchase. You will then juggle your regular mortgage payments alongside the new bridge loan until the old property sells.

-

One Large Consolidated Loan: Alternatively, the lender might issue a single, massive loan that pays off your existing mortgage completely, with the leftover funds acting as your new down payment.

Most of these setups require interest-only monthly payments, meaning you won't pay down the principal until your original property officially closes. At that point, you make one large balloon payment to settle the debt.

Bridge Loan Example

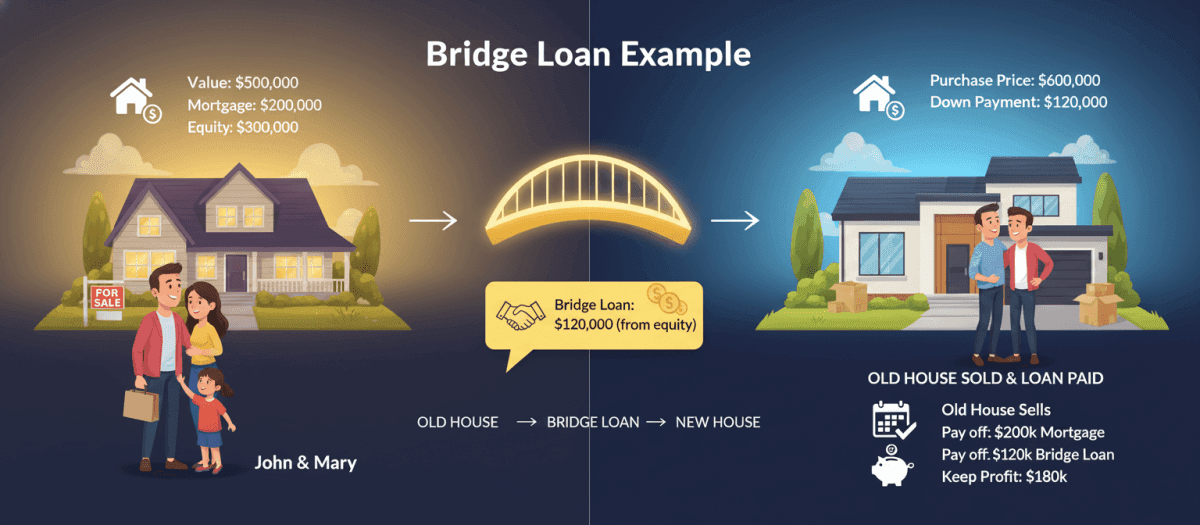

Let me give you a practical example I see quite often. Imagine John and Mary own a house valued at $500,000. They currently owe $200,000 on their mortgage, leaving them with $300,000 in solid equity.

They spot a beautiful new home for $600,000 but need a $120,000 down payment to secure it. Since their cash is trapped in the old house, they take out a bridge loan against their $300,000 equity. The lender approves the $120,000. John and Mary buy the new house immediately, move in peacefully, and list their old property. Six months later, the $500,000 house sells. They use the sale proceeds to pay off the original $200,000 mortgage, clear the $120,000 bridge loan, and pocket the remaining profit.

Who Offers Bridge Loans?

Finding the right provider can be tricky because not every financial institution carries these specialized products. If you are shopping around, you will typically encounter three sources:

-

Traditional Banks and Credit Unions: They offer the lowest interest rates but move incredibly slowly. Their strict underwriting guidelines often make approval difficult.

-

Hard Money/Private Lenders: These companies focus heavily on the asset itself rather than your credit score. They fund deals in days, making them popular with real estate investors, but they charge steep interest rates.

-

Specialized Mortgage Brokers and Loan Officers: This is usually the sweet spot for regular homebuyers. A well-connected broker has access to multiple wholesale lenders and can find a tailored product with reasonable terms.

Pros and Cons of Bridge Loans

Like any financial vehicle, bridging finance carries distinct advantages and drawbacks. Here is an honest breakdown of what to expect:

| Pros | Cons | |---|---| | Move into your new home immediately without waiting for the old one to sell | High interest rates (9%-12%) compared to standard mortgages | | Avoid contingent offers that put you at a disadvantage in bidding wars | Expensive origination fees (1%-3% of loan amount) | | Leverage your existing equity without liquidating assets | Carries the burden of holding two mortgages simultaneously | | Faster funding timelines than traditional mortgages (days to weeks) | Risk of being stuck with both properties if the old one doesn't sell quickly | | Gives you negotiating power in competitive markets | May trigger personal financial strain from double payments |

Bridge Loan Requirements 2026

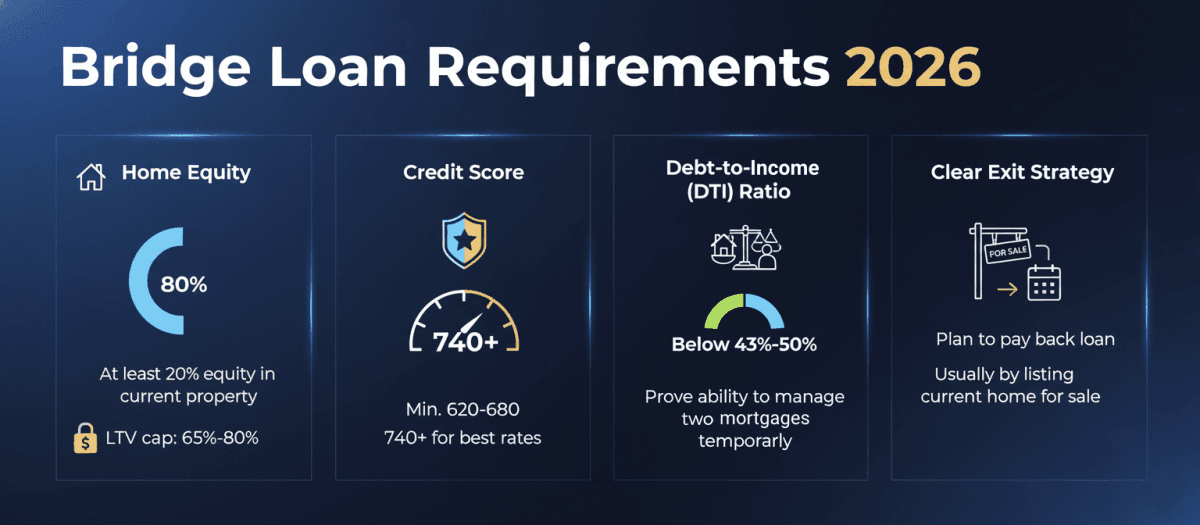

Lending standards have shifted slightly heading into 2026. While traditional home loans obsess over your W-2s, bridge lenders care immensely about your property's equity and your exit strategy. Here are the standard benchmarks you need to hit this year:

-

Home Equity: You typically need at least 20% equity in your current property. Most lenders cap the Loan-to-Value (LTV) ratio around 65% to 80%.

-

Credit Score: While hard money lenders are lenient, standard residential lenders usually look for a minimum credit score of 620 to 680, though 740+ gets you the best rates.

-

Debt-to-Income (DTI) Ratio: Since you might hold two mortgages temporarily, lenders want to know you won't default. A DTI below 43% to 50% is generally preferred.

-

A Clear Exit Strategy: You must prove exactly how you intend to pay the money back, usually by listing your current home for sale.

How to Get a Bridge Loan?

Securing this type of financing requires a bit of upfront preparation. I always recommend following a structured approach so you do not waste time or damage your credit score with multiple hard inquiries.

Step 1: Calculate Your Usable Equity

Before applying, determine your current home's realistic market value and subtract your outstanding mortgage balance. If your equity falls below 20%, you will likely struggle to find approval.

Step 2: Gather Financial Documentation

Even though these loans focus on assets, residential lenders still want to verify your financial stability. Prepare your recent pay stubs, W-2s, tax returns, and a copy of the listing agreement for your current home to prove your exit strategy.

Step 3: Find the Right Loan Officer & Compare Rates

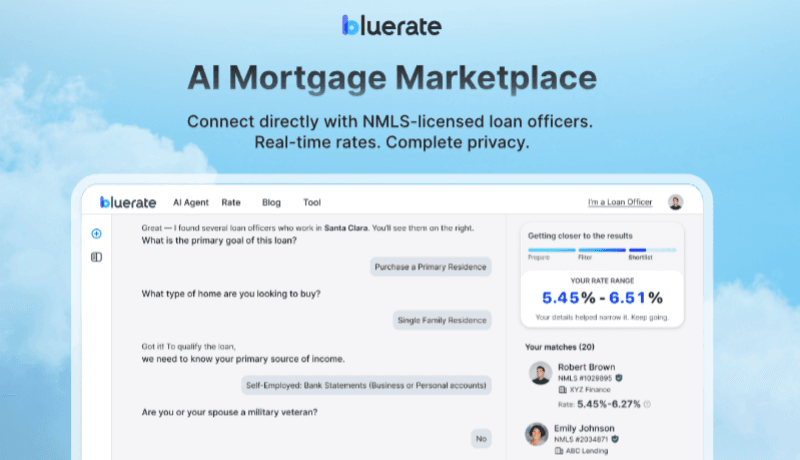

This is where most buyers hit a wall. Searching for niche loan providers manually is exhausting. That is why I highly suggest leveraging a platform like Bluerate. Instead of filling out endless forms and getting bombarded with spam calls, you can use the Bluerate AI Agent—your personal, 24/7 AI Loan Officer Assistant.

By initiating a simple, natural chat on their website, you just enter your location and answer a few basic financial questions (like your estimated home value and goals). The AI analyzes your profile without any judgment and instantly matches you with verified, NMLS-licensed loan officers in your specific area. Bluerate is a completely free, transparent marketplace that lets you securely compare real-time personalized rates from over 30 lenders while keeping your privacy strictly protected.

FAQs About Bridge Loans

Q1. How long does it take to get a bridge loan?

Funding timelines vary, but they are generally much faster than standard mortgages. A traditional lender might take two to three weeks, while private or hard money lenders can often wire funds in just a few days.

Q2. How much does a bridge loan cost?

These products carry premium pricing. You can expect to pay origination fees, usually 1% to 3% of the loan amount, alongside closing costs. Because it is a short-term convenience, the overall setup is more expensive than a 30-year fixed rate.

Q3. HELOC vs. Bridge Loan: What's the Difference?

A Home Equity Line of Credit (HELOC) acts like a credit card tied to your house. You draw funds as needed over several years. A bridge loan delivers a single lump sum specifically meant to be paid off completely within a few months once your house sells. Also Read: HELOC vs Bridge Loan: What are the Differences? Full Guide

Q4. Bridge Loan vs Construction Loan: What's the Difference?

Construction loans disburse money in staged "draws" to pay builders as work progresses on a new structure. A bridge loan gives you cash upfront to facilitate a transitional real estate transaction, like buying a new pre-built home before selling the old one.

Q5. What does a bridging loan do?

It literally bridges a temporary cash-flow gap. By borrowing against your current real estate assets, it provides the immediate liquidity needed to secure a new property without waiting for your existing one to liquidate.

Q6. How long do you have to pay back a bridging loan?

Most residential contracts mandate repayment within 6 to 12 months. If you are a commercial investor, some lenders might extend the timeline up to 18 or 24 months, depending on the scope of the project.

Q7. How long is the repayment period for a bridge loan?

While the maximum term is usually under a year, the actual repayment structure is unique. You generally make interest-only monthly payments during that period. The entire principal balance is due as one massive balloon payment when the term ends or your home sells.

Q8. What are the risks of a bridge loan?

The biggest danger is your old property sitting unsold for months. If the market cools down, you could be forced to drastically lower your asking price or risk facing foreclosure from carrying two heavy mortgage obligations simultaneously.

Q9. What are the alternatives to a bridge loan?

If you want to avoid high fees, consider a HELOC or a standard Home Equity Loan. Another popular choice is an 80-10-10 piggyback loan, or even borrowing against a 401(k) retirement account to secure your down payment temporarily.

Q10. What is the typical interest rate for a bridge loan?

Rates are inherently higher than conventional mortgages. As of early 2026, average rates hover between 9% and 12%, generally landing around the Prime rate plus two percentage points, depending heavily on your LTV and credit profile.

Conclusion: Are Bridge Loans a Good Idea?

If you hold significant equity and are trying to navigate a highly competitive real estate market, a bridge loan is an incredibly powerful tool. It removes the stress of contingent offers and allows for a seamless, perfectly timed move. However, that convenience comes at a premium price, and holding two mortgages simultaneously isn't for the faint of heart.

You should never guess your eligibility or blindly accept high fees. If you want to explore your options safely, head over to the Bluerate homepage and click "Chat with AI." Let the intelligent AI Agent securely analyze your financial scenario, verify your rates, and instantly connect you with a trusted local loan officer—all without risking your privacy or dealing with high-pressure sales calls.