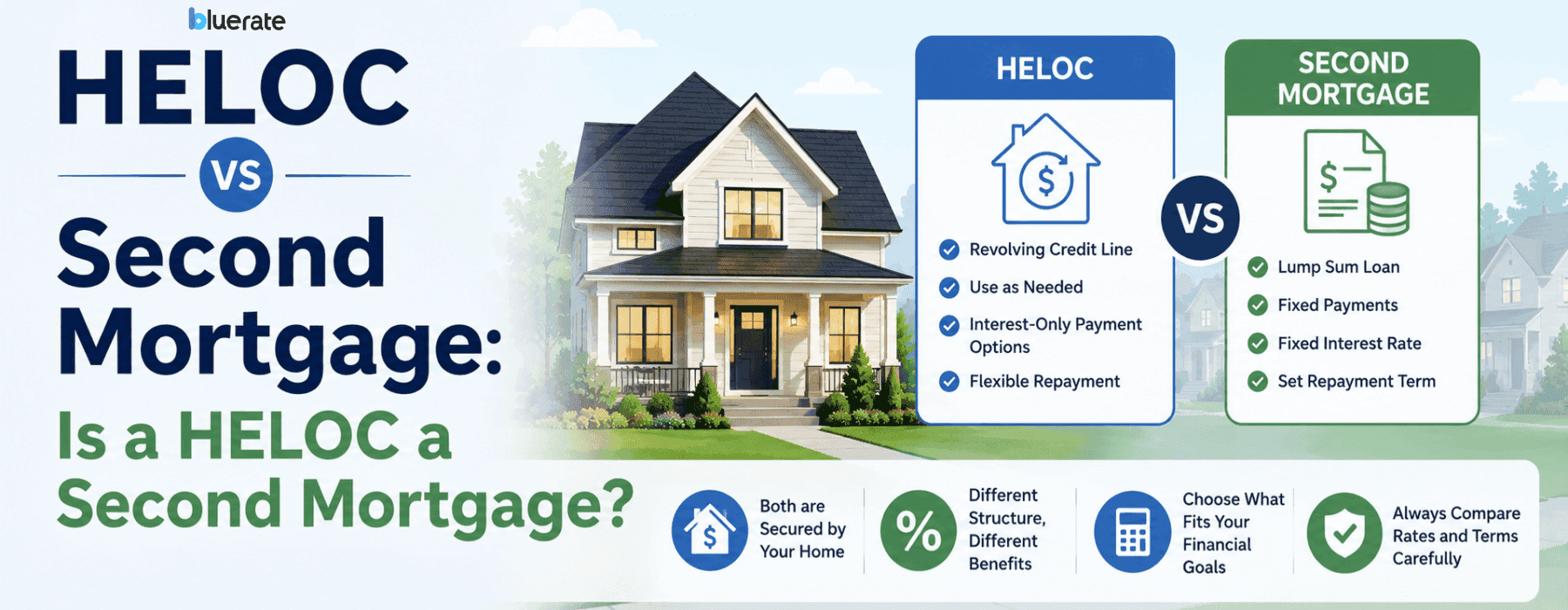

HELOC vs Second Mortgage: Is a HELOC a Second Mortgage?

When you need to tap into your home equity, the terminology gets confusing fast. I notice even savvy folks on Reddit frequently debate whether a HELOC is a true second mortgage or if they should choose a home equity loan instead. To help you make the right choice for your finances, let us clear up this confusion once and for all.

Key Takeaways

-

A HELOC can be a type of second mortgage when it is secured by your home and held in a junior lien position behind your first mortgage.

-

Funding styles differ. A second mortgage is an umbrella term for a loan secured by your home that is junior to your first mortgage. A home equity loan is one common type of second mortgage and typically provides a lump sum.

-

Rates and terms vary. Home equity loans are commonly fixed-rate loans, while HELOCs are typically variable-rate products, though some lenders also offer fixed-rate or hybrid HELOC features.

-

The right fit depends on your project. Fixed-rate home equity loans are often a better fit for one-time, known expenses, while HELOCs are often better for ongoing or less predictable expenses.

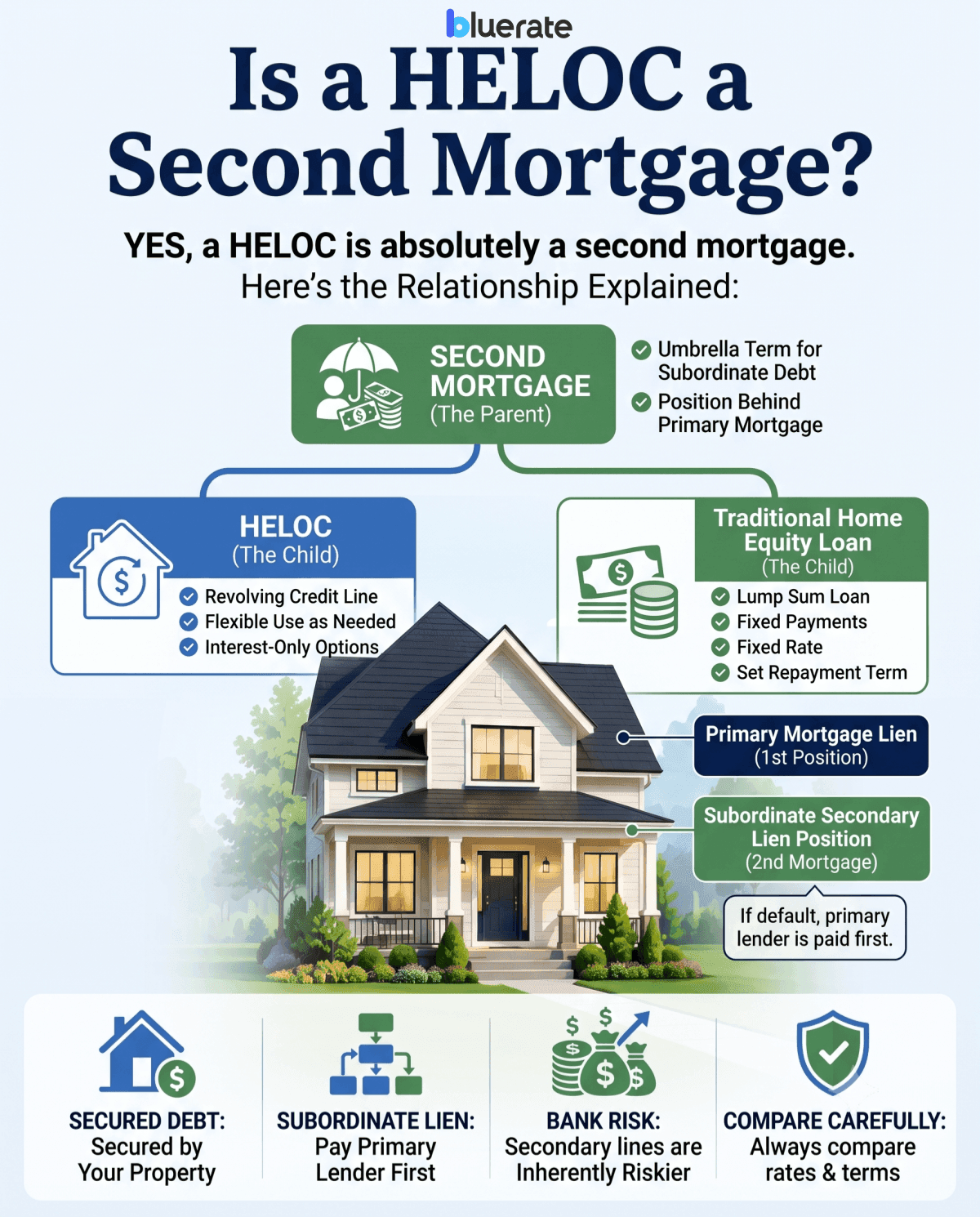

Is a HELOC a Second Mortgage?

Yes, a HELOC is absolutely a second mortgage. In my years of working with homeowners, I have found that people often treat these terms as two entirely different options. In reality, "second mortgage" is just an umbrella term for any debt that sits behind your primary mortgage in what we call a subordinate lien position.

Think of it like a parent-child relationship: "second mortgage" is the parent, and both HELOCs and traditional home equity loans are the children. If you default on your home payments, your primary lender gets paid first, which is why these secondary lines are inherently riskier for banks.

What is a Second Mortgage?

A second mortgage is a loan you take out against your property while your first mortgage is still active. Essentially, you are borrowing against the equity you have already built up over years of making monthly mortgage payments. This allows you to pull out large amounts of cash without touching your original, potentially low-interest first mortgage.

These loans are secured by your home as collateral, meaning you risk foreclosure if you cannot keep up with the extra payments. The two most common types of second mortgages you will encounter are:

-

Home Equity Loans: A closed-end option that provides cash in one single payout.

-

Home Equity Lines of Credit (HELOCs): An open-end, revolving credit limit you can use repeatedly.

What is a Home Equity Loan?

A home equity loan is what most people are actually referring to when they use the term "second mortgage." With this product, the bank hands you a lump sum of money upfront. You then pay it back over a fixed term, usually between** 10 and 30 years**, with a fixed interest rate. Because your monthly payment never changes, it is incredibly easy to budget. From my perspective, it is a highly predictable, straightforward financial tool that takes the guesswork out of borrowing.

What is a HELOC?

A Home Equity Line of Credit (HELOC) works much like a credit card backed by your house. Instead of receiving a lump sum, you get access to a maximum credit limit. During the draw period, which is often about 10 years but varies by lender, you may be able to borrow, repay, and borrow again. Many HELOCs require interest-only payments during this period. Once the draw period ends, the loan enters the repayment period, and monthly payments often rise because principal and interest must be repaid.

Pros:

-

Only pay interest on what you actively use.

-

Extremely flexible for ongoing, unpredictable expenses.

-

Variable rates can drop if market index rates fall.

Cons:

-

Variable rates make monthly payments unpredictable.

-

A risk of "payment shock" when the repayment period kicks in.

-

Easy to overspend since the credit line is revolving.

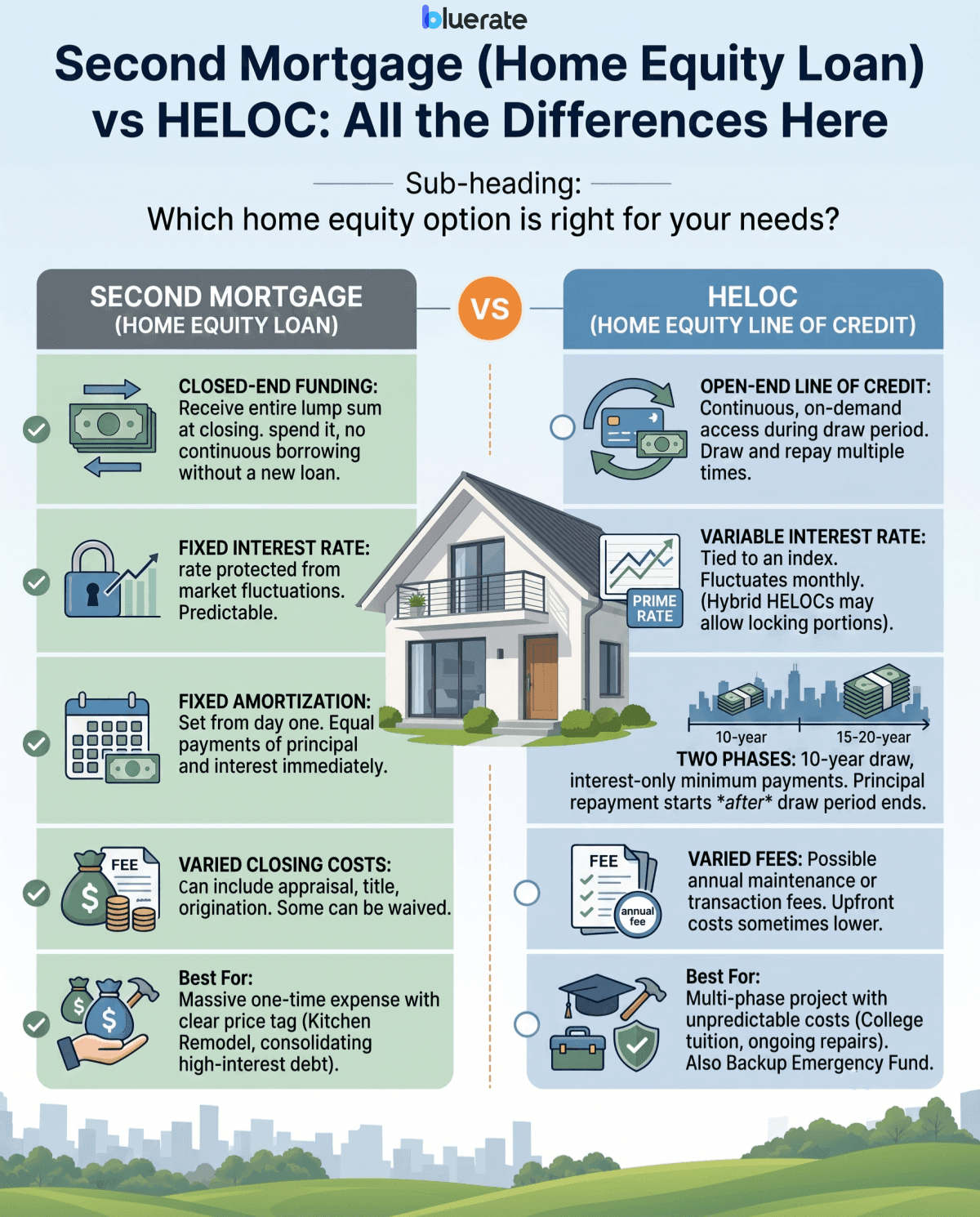

Second Mortgage (Home Equity Loan) vs HELOC: All the Differences Here

Funding Structure

The way you receive your money is the biggest practical difference. A home equity loan is a closed-end product, meaning the lender transfers the entire loan amount to your bank account at closing. Once you spend it, you cannot borrow more without applying for a new loan.

On the flip side, a HELOC is an open-end line of credit. You can pull out fifty dollars today, pay it back next week, and then borrow five thousand dollars next month. It gives you continuous, on-demand access to your money during the draw period, making it far more adaptable.

Interest Rates

Home equity loans almost always feature a fixed interest rate, protecting you from sudden market spikes. HELOCs, however, typically carry variable interest rates tied to an index like the Prime Rate. This means your payments can fluctuate monthly.

However, a major development I have seen recently is that many lenders now offer hybrid or fixed-rate HELOCs. These products allow you to lock in a fixed interest rate on specific portions of your balance, giving you the flexible borrowing power of a HELOC alongside the rate safety of a traditional loan.

Repayment Structures

Repayment timelines follow completely different rules. With a home equity loan, your amortization schedule is set from day one. You make equal payments of principal and interest immediately. A HELOC divides your repayment into two phases. For the first decade, your minimum monthly payment is incredibly low because you are only required to pay interest on the money you drew.

But beware of the transition. When the draw period ends, your monthly bill will rise significantly as you begin paying down the actual principal balance over the remaining 15 to 20 years.

Upfront Fees and Closing Costs

Both products may involve closing costs, but fees vary widely by lender and loan size. Some HELOCs have low or waived upfront costs, while others may charge appraisal, title, or origination fees. These fees cover property appraisals, credit checks, and title searches.

However, I often find that some lenders are willing to waive upfront HELOC closing costs to attract borrowers. In exchange, you might face ongoing maintenance charges, such as annual membership fees or transaction fees. It is crucial to review the fine print so you do not get blindsided by these quiet costs.

Best For

Choosing the right route depends on your spending timeline. In my experience, a home equity loan is ideal if you have a massive, one-time expense with a clear price tag, like consolidating high-interest credit card debt or paying a contractor for a kitchen remodel.

Conversely, a HELOC is perfect if you are managing a multi-phase project with unpredictable costs, like paying college tuition over several years or tackling ongoing home repairs. It also functions beautifully as a backup emergency fund that you hope you never have to touch.

FAQs About HELOC vs Second Mortgage

Q1. Does a HELOC replace my primary mortgage?

No, a HELOC does not replace or refinance your first mortgage. It may sit alongside your primary mortgage as a separate lien, and any monthly payment depends on whether you have drawn funds and what phase the HELOC is in.

Q2. Can I get a HELOC and a home equity loan at the same time?

While technically possible if you have massive home equity and a very low debt-to-income (DTI) ratio, it is incredibly rare. Third-lien positions are much harder to obtain because lenders face higher repayment risk.

Q3. What happens to my second mortgage or HELOC if I sell my home?

When you sell your house, both your primary mortgage and your second mortgage must be paid off in full using the sale proceeds before you can pocket any of the cash.

Q4. Why are interest rates higher on second mortgages than first mortgages?

Lenders charge higher rates because they are in a subordinate position. If you default and your home goes into foreclosure, the primary mortgage lender gets paid first, making second mortgages much riskier for banks.

Q5. Is it harder to qualify for a HELOC than a primary mortgage?

Generally, yes. Because of the higher risk, lenders have stricter requirements. You will typically need a credit score of at least 660, a debt-to-income ratio below 43%, and at least 15% to 20% equity left in your home.

Final Word

Deciding between these two home equity products comes down to your personal financial goals.

-

If you value stable, predictable payments, a traditional home equity loan is your best bet.

-

If you prefer financial flexibility and only want to pay for what you use, a HELOC is hard to beat.

Because mortgage rates and local guidelines change constantly, I highly recommend speaking with an expert. You can search for licensed Loan Officers on Bluerate to get personalized, cost-free advice for your specific situation today.