Second Mortgage Explained 2026: Learn Everything Here

If you are like many homeowners I work with, you might need extra cash for home renovations or to pay off high-interest debts. Rather than selling your home, you can tap into its built-in value. This is where a second mortgage comes in. Let me walk you through how this financial tool works so you can decide if it is right for your wallet.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute professional financial advice. Please consult with a licensed financial advisor before making any borrowing decisions.

Key Takeaways

-

A second mortgage lets you borrow against your home's equity while keeping your primary mortgage.

-

You can choose between a fixed-rate home equity loan or a variable-rate HELOC.

-

Your home serves as collateral, meaning you could face foreclosure if you default on payments.

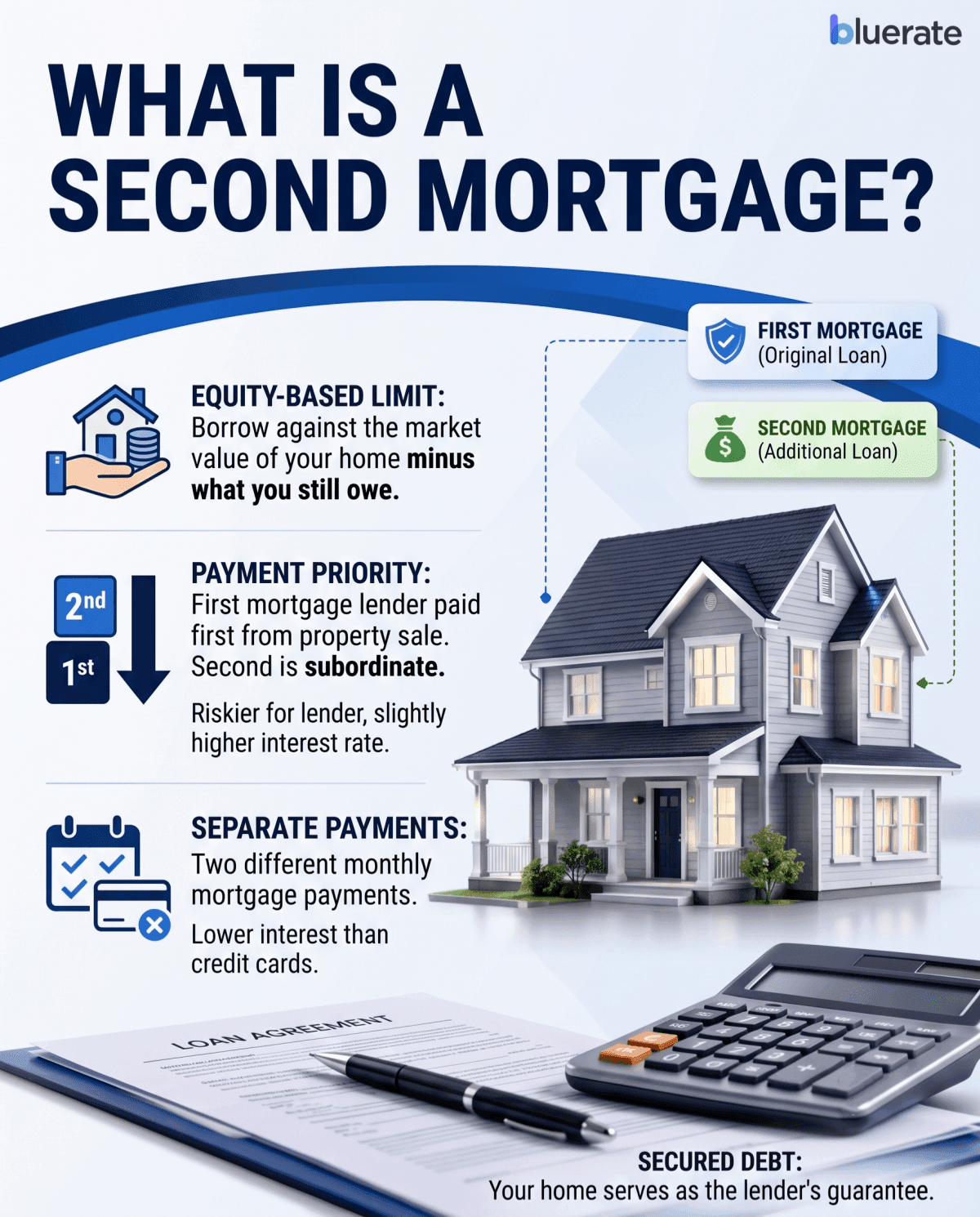

What is a Second Mortgage?

In my years of helping clients navigate home financing, I often describe a second mortgage as an additional loan secured by your property. It sits right alongside your original home loan. The term "second" does not mean it is less important. Rather, it refers to its payment priority if things go wrong.

If a borrower defaults and the home is sold, the first mortgage lender gets paid first. Because of this subordinate position, lenders take on more risk, which is why rates are slightly higher than primary mortgages. However, they are still much cheaper than credit cards.

Here are the primary features of these loans:

-

Equity-Based: Your borrowing limit depends entirely on the market value of your home minus what you still owe.

-

Separate Payments: You will make two different mortgage payments each month.

-

Secured Debt: Your home is the guarantee for the lender.

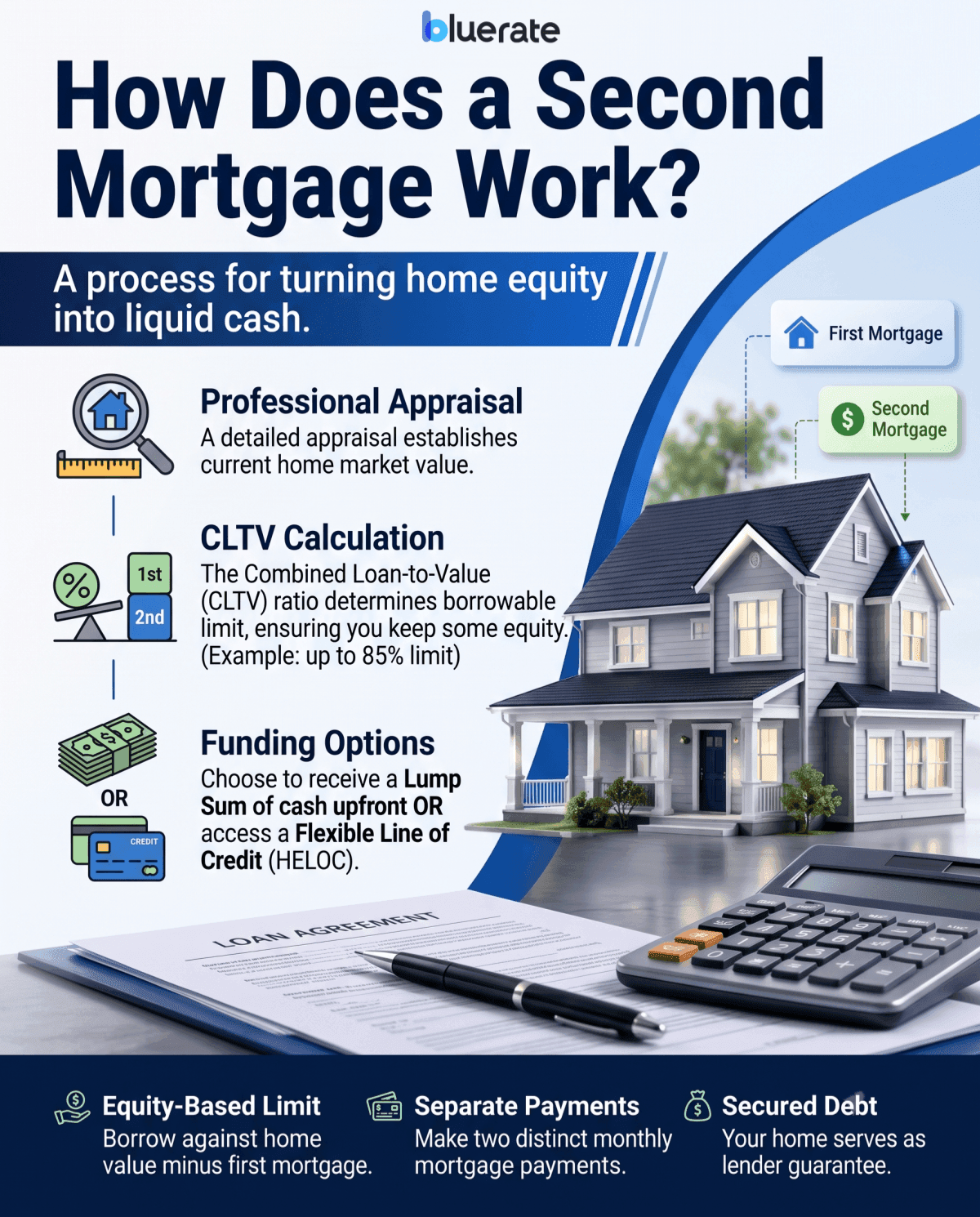

How Does a Second Mortgage Work?

To get a second mortgage, you are essentially turning your home's equity into liquid cash. When I analyze a borrower's file, I look at the difference between the home's current appraised value and the balance left on the first mortgage. Lenders do not let you borrow 100% of this difference. Instead, they use a metric called the Combined Loan-to-Value (CLTV) ratio to set your limit, ensuring you keep some skin in the game.

Here is a breakdown of how the mechanics work in practice:

-

**CLTV Rule: **Many lenders use combined loan-to-value limits and usually require you to keep some equity in the home.

-

Appraisal Requirement: A professional appraiser must verify what your home is worth today.

-

Funding Options: Depending on the setup you choose, you either receive a lump sum of cash upfront or get a flexible line of credit to use over time.

Types of Second Mortgages

Choosing the right type of second mortgage depends entirely on your spending goals. I always tell my clients that if they have a single, fixed cost, like a kitchen remodel, they should treat it differently than ongoing expenses like college tuition. In the U.S., the most common home equity borrowing options are a cash-out refinance, a home equity loan, and a HELOC. A piggyback loan is a separate purchase-financing structure.

Here are the main types and how they differ:

-

Home Equity Loan: This provides a lump sum with a fixed interest rate, which is typically fixed for the life of the loan.

-

Home Equity Line of Credit (HELOC): This works like a credit card, allowing you to draw cash up to your credit limit. It features variable rates, which average around 7.4% today.

-

Piggyback Loan: Also known as an 80-10-10 loan, this is typically used at home purchase to split the financing into two loans and may help avoid PMI.

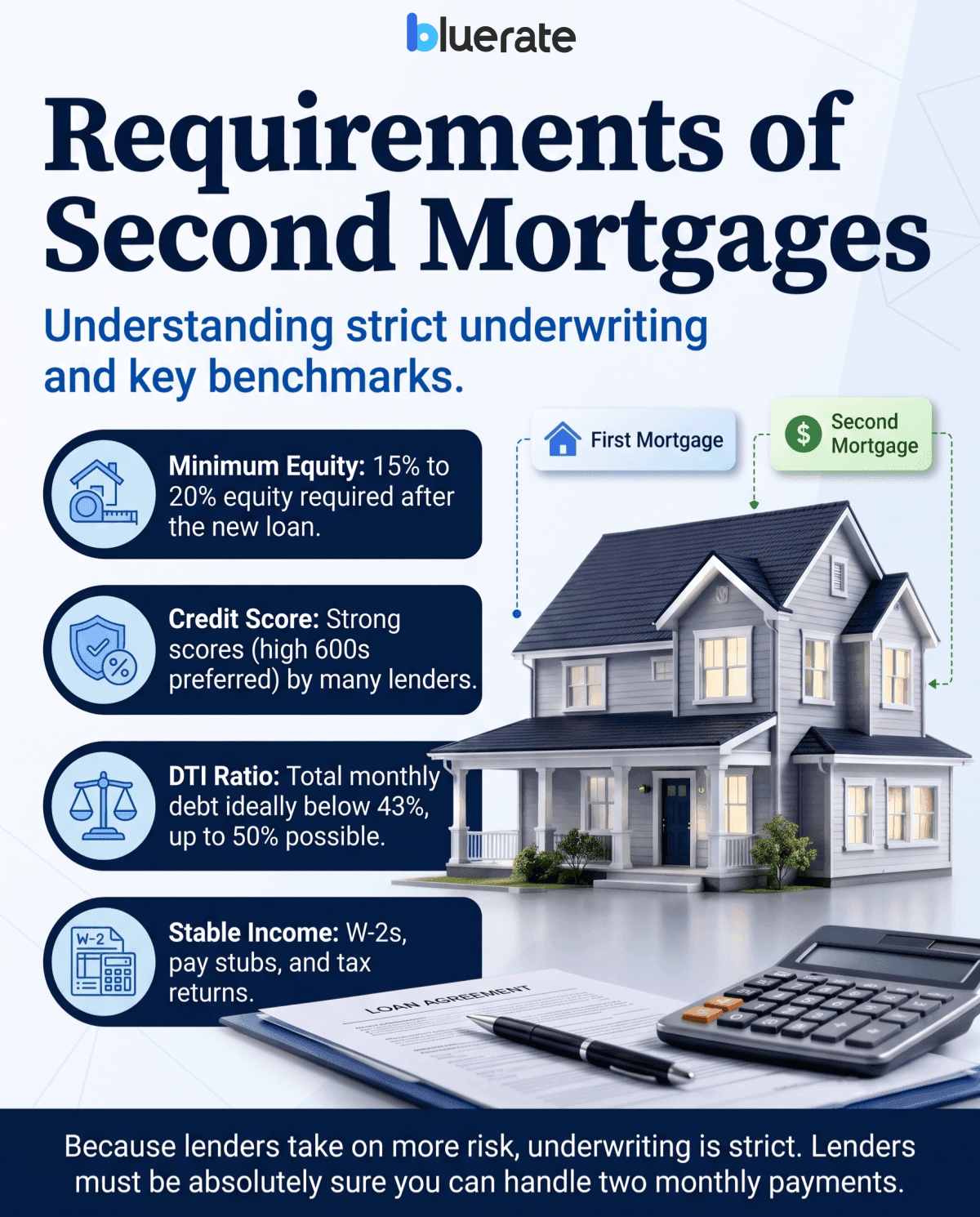

Requirements of Second Mortgages

Because second mortgage lenders stand second in line to get paid, their underwriting standards are strictly monitored. Some lenders may apply stricter underwriting standards for a second mortgage because the loan is subordinate to the first mortgage. Lenders want to be absolutely sure you can handle two monthly house payments without falling behind.

To qualify in today's market, you will generally need to meet these benchmarks:

-

Minimum Equity: You must have at least 15% to 20% equity left in your home after taking out the new loan.

-

Credit Score: Many lenders prefer stronger credit, and some may set minimum scores in the** high 600s**, though requirements vary by lender.

-

Debt-to-Income (DTI) Ratio: Your total monthly debt payments, including both mortgages, should ideally be below 43%, though some lenders go up to 50% for highly qualified borrowers.

-

Stable Income: You must provide tax returns, W-2s, and pay stubs to prove a steady, reliable stream of income.

Pros and Cons of Second Mortgages

Every financial path has trade-offs, and second mortgages are no exception. I always tell my clients to weigh the immediate cash benefits against the long-term risks. Borrowing against your home is serious business, so a balanced view is vital to protecting your financial health.

The Pros:

-

Lower Rates: Interest rates are much lower than credit cards or personal loans, saving you money on interest.

-

Large Borrowing Limits: You can access tens of thousands of dollars based on your home's actual value.

-

Tax Advantages: Under current U.S. tax rules, the interest may be deductible only if the loan proceeds are used to buy, build, or substantially improve the home that secures the loan.

The Cons:

-

Foreclosure Risk: If you default, the lender may foreclose because the loan is secured by your home, even if your first mortgage has already been paid off.

-

Closing Costs: You will have to pay closing fees, which usually range from** 2% to 5% **of the loan amount.

-

Two Monthly Payments: Managing two separate mortgage bills can strain your monthly household budget if your income drops.

FAQs About a Second Mortgage

Q1. What is the purpose of a second mortgage?

Most borrowers use a second mortgage to cover large, necessary expenses. In my practice, the most common uses are major home improvements, debt consolidation, or college tuition. Because these loans offer lower interest rates than unsecured debt, they are a smart way to pay off high-interest credit cards. However, I advise against using this equity for vacations or luxury purchases.

Q2. What is the difference between first mortgage and second mortgage?

A first mortgage is the loan you use to buy your home, and it holds primary claim over the property. A second mortgage is an additional loan you take out later using your built-in equity. If you default, the first mortgage lender gets paid first from a home sale, while the second lender gets what remains. This makes second mortgages riskier for lenders.

Q3. Can I get a second mortgage with bad credit?

Yes, but it is challenging. If your score is below 620, lenders will view you as high-risk. You might still qualify if you have a lot of home equity and low overall debt, but you should expect higher interest rates and lower borrowing limits. I usually recommend working to boost your credit score before applying to secure better terms.

Q4. Are second mortgage interest payments tax-deductible?

According to the IRS, second mortgage interest is only tax-deductible if you use the funds to buy, build, or substantially improve the home that secures the loan. If you use the cash to pay off credit cards or buy a car, the interest is not deductible. Because tax laws are complex, I highly recommend consulting a CPA.

Q5. What happens to a second mortgage if I sell my home?

When you sell your home, outstanding mortgages are typically paid off at closing from the sale proceeds, with the first lien paid before the second lien. During the closing process, the first mortgage is paid off first. Any remaining funds from the sale go directly to fully pay off your second mortgage balance. Only after both loans are completely settled will you receive the remaining profit.

Is a Second Mortgage Ever a Good Idea?

A second mortgage is a powerful financial tool, but it is only a good idea if you use it wisely. If you have stable income, a clear repayment plan, and want to build wealth, like reinvesting in your home's value, it makes complete sense. However, using your home as collateral to fund a lifestyle you cannot afford is a dangerous path. If you are ready to take the next step, I suggest checking your available equity using a reliable mortgage calculator and speaking to a licensed professional to explore your options safely.