Warrantable vs Non-Warrantable Condo: Detailed Guide 2026

In my years helping buyers navigate the housing market, I have seen many dream home purchases fall through at the last minute because of condo warrantability. Simply put, whether a condo is warrantable or non-warrantable determines if you can secure a standard, low-cost mortgage. This updated 2026 guide clarifies these critical differences and details how recent agency shifts affect your purchasing power today.

Key Takeaways

-

Warrantable condos meet Fannie Mae and Freddie Mac guidelines, making them eligible for conventional financing. Some may also qualify separately for FHA or VA approval.

-

Non-warrantable condos carry higher lender risk, requiring specialized financing like non-QM or portfolio loans.

-

Stricter 2026 rules have made building safety, reserve funds, and structural integrity primary deciders of a condo's warrantability.

What is a Warrantable Condo?

I often tell my clients that a warrantable condo is the safest bet for a hassle-free loan process. In the eyes of mortgage lenders, these properties represent low financial risk. Because the homeowners association (HOA) maintains solid financial health and keeps the property in good shape, conventional lenders are happy to finance individual units. These loans are typically packaged and sold to government-sponsored enterprises (GSEs) such as Fannie Mae and Freddie Mac.

If you are looking at a warrantable condo, you will typically find these characteristics:

-

High Owner-Occupancy: A sufficient percentage of units are owner-occupied, typically around 50% or higher, depending on project and loan type.

-

Strong Reserves: The HOA allocates at least 10% of its annual budget to reserve funds.

-

Clean Litigation Record: There are no major active lawsuits against the HOA.

What is a Non-Warrantable Condo?

When a development fails to meet federal guidelines, it is classified as non-warrantable. In my practice, I find these properties often look identical to warrantable ones from the outside, but their legal or financial structures present too much risk for standard lenders. Because Fannie Mae and Freddie Mac will not buy mortgages on these buildings, traditional banks avoid them. You will instead have to seek specialized financing.

A non-warrantable condo usually has one or more of these features:

-

High Investor Concentration: A single developer or investor owns too many units, or renters dominate the building.

-

Short-Term Rental Friendly: The HOA allows hotel-like operations or daily/weekly rentals (often called condotels).

-

Significant Commercial Presence: More than approximately 35% of the total square footage is used for commercial purposes.

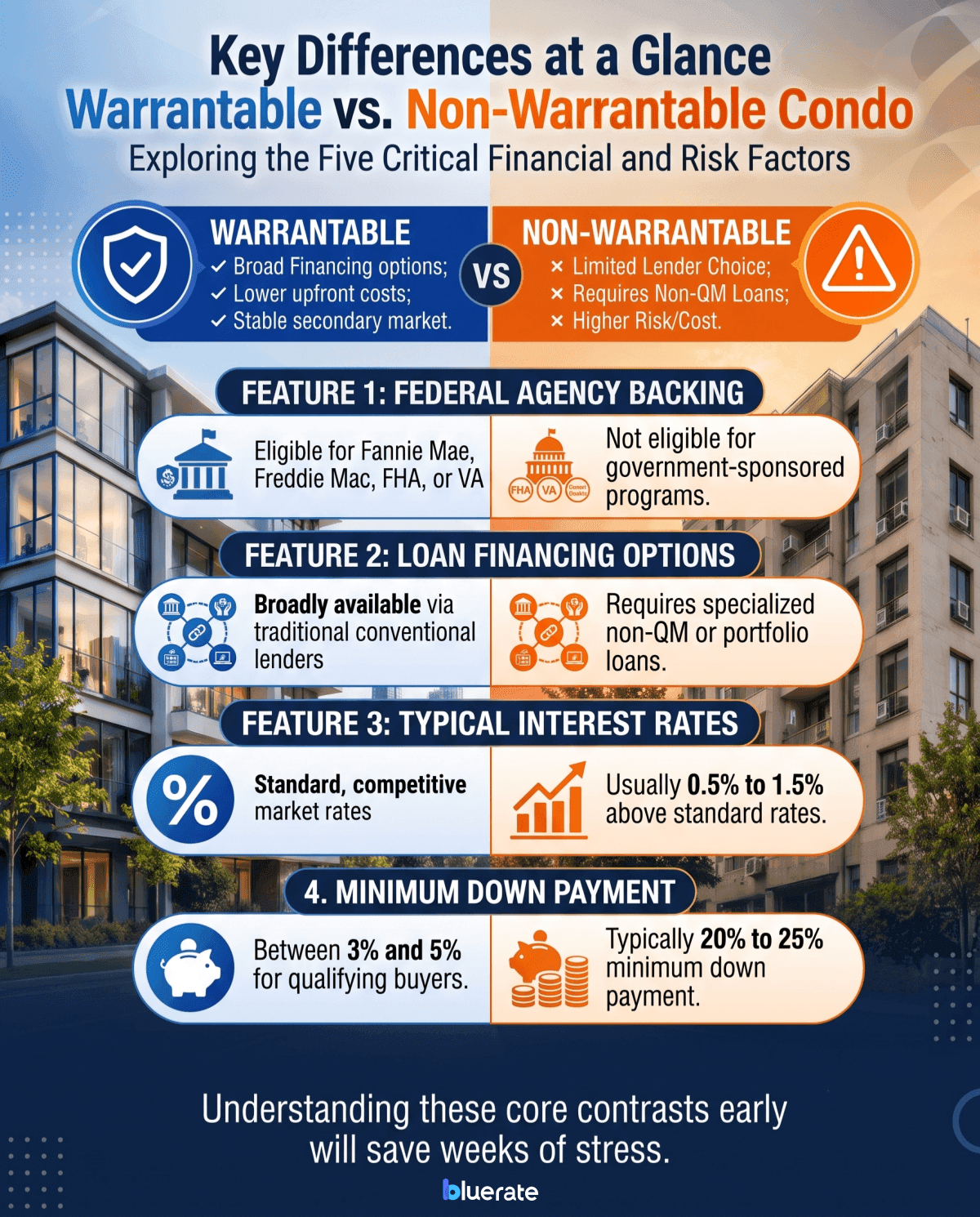

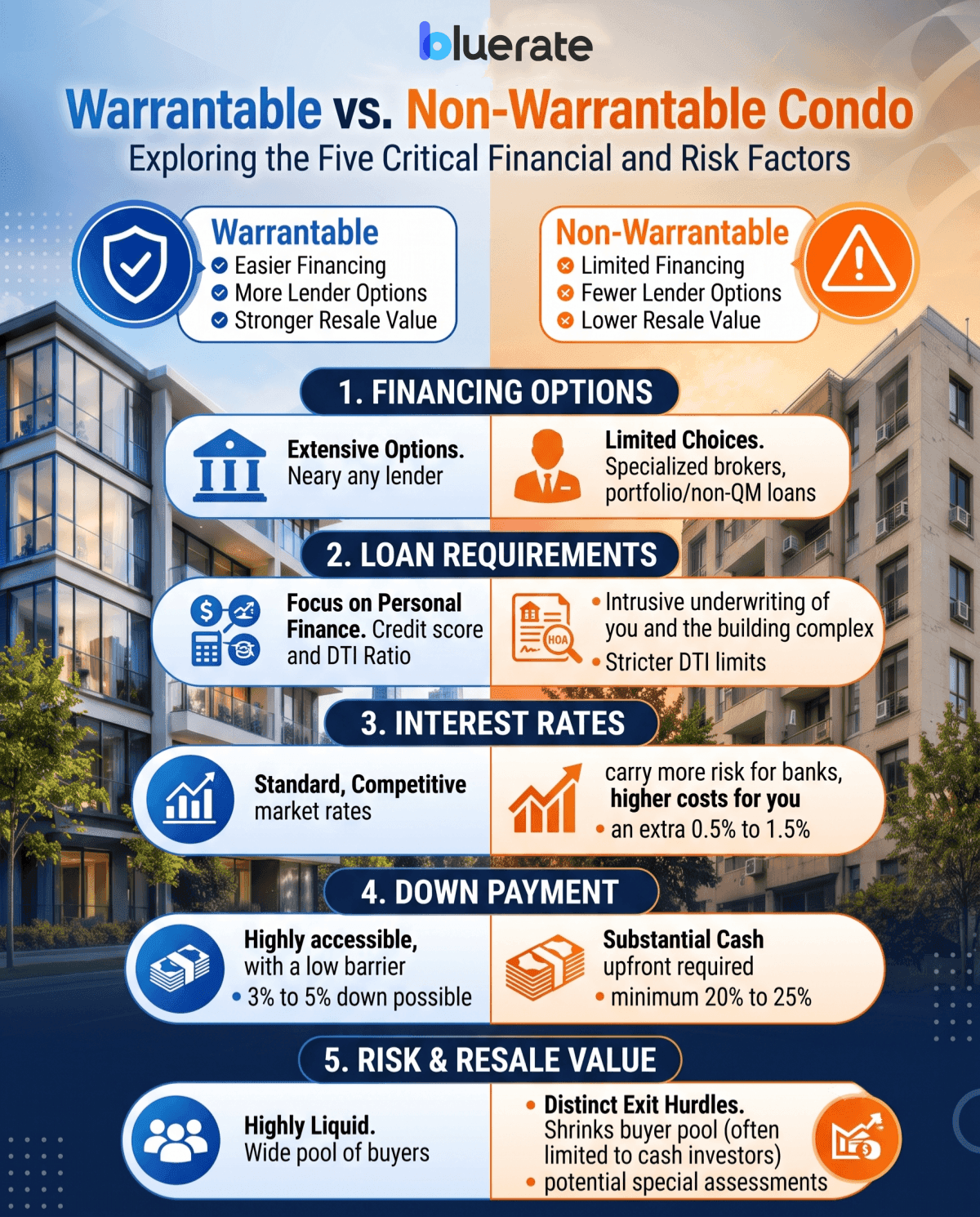

Key Differences at a Glance

Understanding these core contrasts early in your property search will save you weeks of stress. I have put together this clear, side-by-side comparison table to outline exactly how warrantability impacts your financing options, interest rates, and upfront cash requirements in today's mortgage market:

Comparison: Warrantable vs. Non-Warrantable Condo

Let's explore how these differences play out in real-world buying scenarios, focusing on the five most critical financial and risk factors.

Financing Options

When you purchase a warrantable condo, your funding options are extensive. Nearly any bank, credit union, or online lender can offer you a conventional mortgage. However, if the complex is non-warrantable, your choices shrink. Because these loans cannot be easily sold on the secondary market, many traditional lenders limit their exposure or offer them only through portfolio lending.

You will need to seek out specialized mortgage brokers who offer portfolio loans, where the bank keeps the loan on its own books, or non-QM (non-Qualified Mortgage) loans. Finding these lenders requires extra research, and you will have to deal with a much smaller pool of financial institutions.

Loan Requirements

In my experience, getting approved for a non-warrantable condo involves a far more intrusive underwriting process. Conventional loans focus primarily on your personal financial health, checking your credit score and debt-to-income ratio. But with a non-warrantable property, lenders review both you and the entire building complex.

They will scrutinize the HOA's balance sheets, insurance policies, and board meeting minutes. You will typically need a stronger credit profile, often in the high-600s or above, depending on the lender, and a spotless borrowing history. Lenders also enforce stricter debt-to-income limits to offset the inherent risks associated with a non-conforming property.

Interest Rates

Budgeting for your monthly payment requires a realistic look at interest rates. Because warrantable mortgages easily conform to federal standards, lenders offer them at standard, competitive market rates. Non-warrantable condo loans carry more risk for banks, and that risk translates directly into higher costs for you.

Typically, you can expect interest rates on non-QM or portfolio loans to be** 0.5% to 1.5%** higher than traditional conventional rates. While this might sound small on paper, over a thirty-year term, that extra percentage point can add tens of thousands of dollars to your total cost of homeownership.

Down Payment

Your upfront cash requirement is another area of stark contrast. For a warrantable unit, first-time homebuyers can often secure financing with a down payment as low as 3% to 5%. This low barrier makes standard condos highly accessible. Conversely, if you choose a non-warrantable property, prepare to bring a substantial amount of cash to the closing table.

Lenders generally demand a minimum down payment of 20% to 25%. In my experience, if the purchase is purely an investment property, some non-QM lenders might even push that requirement up to 30%, which significantly changes your cash-on-cash return calculation.

Risk & Resale Value

I always urge buyers to look beyond the immediate purchase and consider long-term liquidity. Warrantable condos are highly liquid. When you want to sell, you can market to the widest pool of buyers who rely on easy-to-get conventional loans. Non-warrantable condos present distinct exit hurdles.

When you eventually list the property, your buyer pool shrinks dramatically because most prospective purchasers cannot qualify for specialized loans or afford the massive down payment. You are often limited to cash investors, which can lengthen your time on the market. Furthermore, if the building's non-warrantability stems from structural defects or poor HOA reserves, you could face unexpected special assessments, draining your home equity and dampening your property's long-term appreciation potential.

Why Does a Condo Become Non-Warrantable?

In my daily practice, I find that a condo building rarely starts out as non-warrantable. Rather, it crosses the line due to operational shifts or aging infrastructure. Mortgage packagers flag these complexes when they present too much financial or legal liability. The primary factors that trigger a non-warrantable status include:

-

High Investor Dominance: Over half of the property is owned by real estate investors or renters instead of primary owners.

-

Severe Structural Issues: The complex suffers from unaddressed deferred maintenance, has poor structural integrity, or fails safety guidelines set by agencies like Fannie Mae in their March 2026 updates (Lender Letter LL-2026-03).

-

Active HOA Litigation: The association is embroiled in active structural or construction defect lawsuits.

-

Underfunded Reserves: Less than 10% of HOA funds go to capital repairs.

FAQs About Non-Warrantable vs Warrantable Condo

Q1: Can a non-warrantable condo become warrantable in the future?

Yes, it absolutely can. When a condo building loses its warrantability, the HOA board can take actionable steps to restore its status. For example, if the issue is a high investor concentration, wait until more units are sold to primary residents. If the obstacle is active litigation, the property typically becomes warrantable again once the lawsuit is resolved or settled.

Many HOAs also successfully restore their status by raising monthly dues or passing a special assessment to boost their reserve funds up to the required 10% threshold. I always recommend that buyers ask the HOA board if they are actively working to resolve their non-conforming status.

Q2: Do FHA and VA loans apply to non-warrantable condos?

Generally, they do not. The Federal Housing Administration (FHA) and the Department of Veterans Affairs (VA) maintain highly specific, pre-approved lists of condo communities. Because these government agencies enforce strict guidelines on owner-occupancy, financial reserves, and building safety, any complex deemed non-warrantable will fail their approval process.

If you are planning to use an FHA or VA loan, you must cross-reference your target property with the HUD or VA approved condo registries before submitting an offer, as conventional lenders will not be able to bypass these restrictions.

Q3: How can I verify a condo's warrantability status before making an offer?

Verifying warrantability early is crucial to avoiding wasted appraisal fees. First, ask your loan officer to check Fannie Mae's Condo Project Manager (CPM) tool to see if the building has a pre-existing approval or denial. Second, review the HOA's most recent meeting minutes and financial statements yourself, or have your agent request them.

Look closely for mentions of active lawsuits, underfunded reserves, or upcoming special assessments. Lastly, your lender will ultimately require the HOA to fill out a standardized Condo Project Questionnaire, which is the definitive document used to determine warrantability.

Q4: Why are interest rates higher for non-warrantable condo loans?

It all comes down to risk. Traditional lenders package and sell warrantable loans to Fannie Mae and Freddie Mac, which quickly frees up their capital to write new mortgages. Since government-sponsored enterprises will not touch non-warrantable loans, lenders are forced to hold these mortgages on their own balance sheets.

This locks up their capital and exposes them to the direct financial consequences if you default. To compensate for this elevated portfolio risk, lenders charge a premium, typically bumping up the interest rate by 0.5% to 1.5% compared to conventional financing.

Q5: Is buying a non-warrantable condo ever a good investment?

It can be, depending on your financial situation and investment strategy. If you are an all-cash buyer or can easily afford a 25% down payment, non-warrantable condos often sell at a significant discount compared to warrantable units in the same area.

This lower purchase price can yield higher cash-on-cash rental returns, especially in resort communities where short-term rentals are highly lucrative. However, you must perform exhaustive due diligence on the physical state of the building and the HOA's financials to ensure you are not buying into a structural or legal nightmare.

Final Word

Ultimately, deciding between these two options requires carefully balancing your immediate budget with your long-term real estate investment goals.

Choose a warrantable condo if you want:

-

The lowest possible interest rates and standard conventional financing.

-

A minimal down payment ranging from 3% to 5%.

-

Maximum future resale liquidity when you decide to sell.

Choose a non-warrantable condo if you:

-

Are an investor seeking undervalued vacation properties.

-

Have access to cash or non-QM portfolio financing.

-

Accept higher long-term risk for rental yield potential.