Non-Warrantable Condo Explained: Pros and Cons for Buyers

Picture this: you put an offer on a gorgeous condo, only for your mortgage lender to call with bad news—the building is "non-warrantable." It is a frustrating setback I see all the time. But does this mean your dream of homeownership is dead? Not necessarily. Let's look at what this term actually means for your mortgage options and how we can still make the deal work.

Key Takeaways

-

Definition: A non-warrantable condo does not meet strict Fannie Mae or Freddie Mac standards, making it ineligible for traditional conventional loans.

-

Common Triggers: High investor ownership, vacation rental activity, active litigation, or poorly funded HOA reserves often cause this classification.

-

Financing: Buyers can still secure financing using specialized portfolio or Non-QM loans, though these require higher down payments.

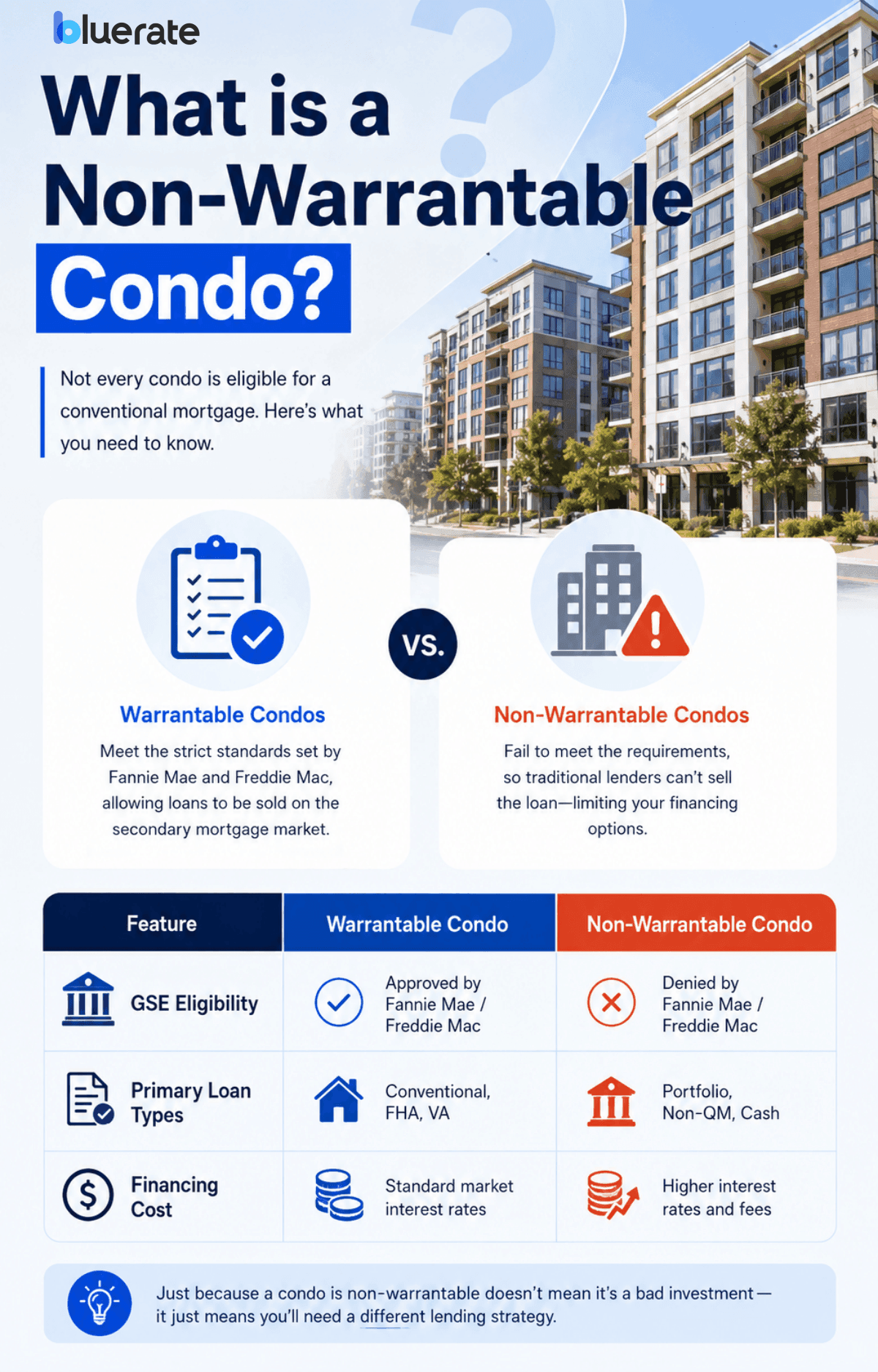

What is a Non-Warrantable Condo?

In my years of helping buyers navigate home loans, I have found that "non-warrantable" is one of the most misunderstood terms. Simply put, conventional mortgages must meet strict standards set by Fannie Mae and Freddie Mac so banks can sell them later. When a condo fails these checks, it is flagged as non-warrantable.

This does not mean the building is physically unsafe. It just means traditional banks cannot bundle the loan onto the secondary mortgage market. Because of this lending roadblock, mainstream lenders shy away, forcing us to explore creative financing avenues instead.

Also Read: Warrantable vs Non-Warrantable Condo: Detailed Guide

Why is a Condo Non-Warrantable?

In my experience, condos usually fall into this category due to specific operational or financial risks that make traditional lenders nervous. Here are the main red flags we look out for:

-

Investor Heavy: Investor ownership is high, often exceeding lender or agency thresholds for owner-occupancy or investor concentration.

-

Short-Term Rentals: The HOA allows Airbnb-style rentals, making it look more like a commercial hotel.

-

Pending Lawsuits: The HOA is locked in a legal battle, usually with the builder over construction quality.

-

Too Much Retail: More than 35% of the property's square footage is used for commercial purposes

-

Weak Reserves: The HOA does not meet the minimum reserve funding requirement, such as the 10% budgeted replacement reserve standard.

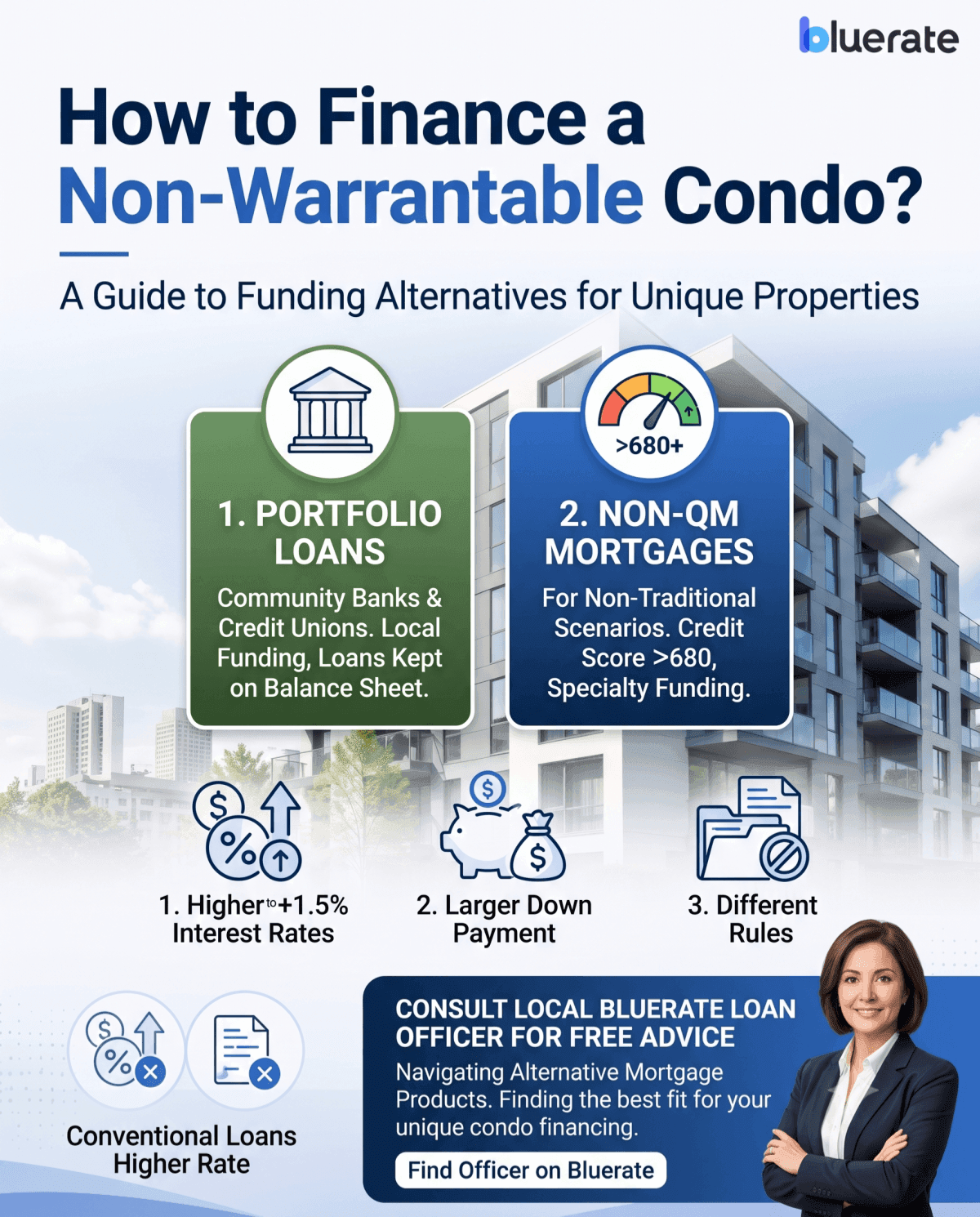

How to Finance a Non-Warrantable Condo?

If you have set your heart on one of these properties, do not throw in the towel. While conventional conforming loans are out of the question, I routinely help buyers secure funding through alternative mortgage products:

-

Portfolio Loans: Local credit unions and community banks often fund these deals because they keep the loans on their own balance sheets rather than selling them off.

-

Non-QM Mortgages: These specialty loans are designed for non-traditional situations, though you will usually need a solid credit score above 680.

Keep in mind that these options come with different rules. Since the lender is taking on more risk, they will likely charge an interest rate that is** 0.5% to 1.5%** higher than average, and they will want a much larger down payment. Working with an experienced broker is key here. Also, you can reach out to a local loan officer for a free consultation on Bluerate for a non-warrantable condo.

Also Read: Non-Warrantable Condo Loan: Which to Choose?

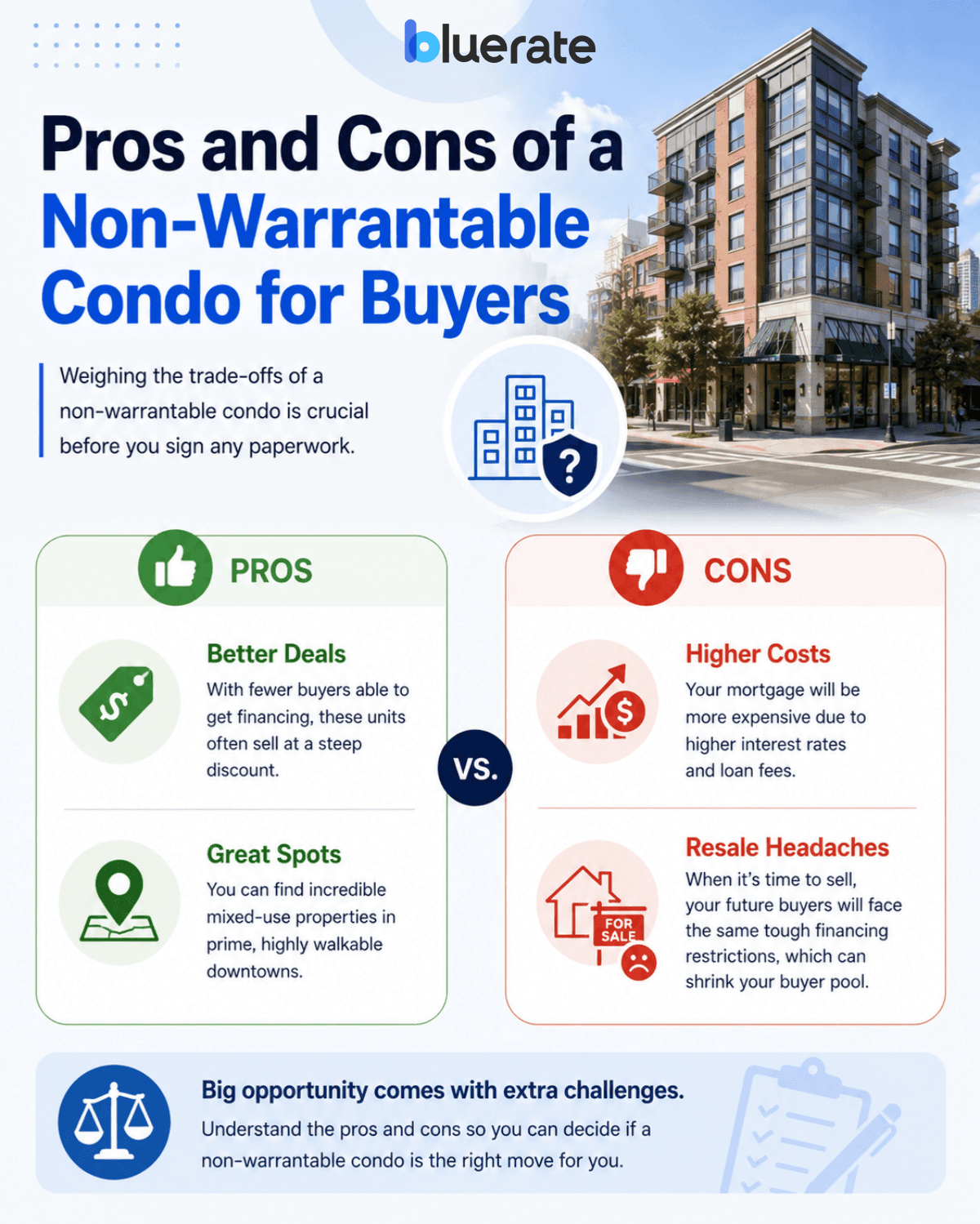

Pros and Cons of a Non-Warrantable Condo for Buyers

Weighing the trade-offs of a non-warrantable condo is crucial before you sign any paperwork.

Pros:

-

Better Deals: With fewer buyers able to get financing, these units often sell at a steep discount.

-

Great Spots: You can find incredible mixed-use properties in prime, highly walkable downtowns.

Cons:

-

Higher Costs: Your mortgage will be more expensive due to higher interest rates and loan fees.

-

Resale Headaches: When it is time to sell, your future buyers will face the same tough financing restrictions, which can shrink your buyer pool.

FAQs to Know About Non-Warrantable Condo

Q1. Is it hard to sell a non-warrantable condo?

Yes, it can be. Since regular buyers cannot get conventional mortgages, you are limited to cash buyers or those using specialty loans. This smaller buyer pool means it usually takes longer to sell and might limit your home's appreciation.

Q2. Who determines if a condo is warrantable?

Your lender's underwriting and condo review process, based on HOA documents and program guidelines, determines the result. They do this by sending a detailed questionnaire to the condo's HOA to check its insurance, budget reserves, litigation history, and owner ratios against federal standards.

Q3. Who lends on non-warrantable condos?

You will want to skip the massive national banks. Instead, look for local community banks, credit unions, or independent mortgage brokers who offer Non-QM products. These institutions are comfortable holding the loan's risk on their own books.

Q4. How to find out if a condo is non-warrantable?

Ask your real estate agent to check the listing notes or contact the HOA manager directly. You can also have your loan officer run a condo review, or check FHA and VA approval lists. However, being absent from those lists does not by itself prove the condo is non-warrantable.

Q5. Can I get an FHA or VA loan on a non-warrantable condo?

FHA and VA loans have their own condo approval requirements, so many non-warrantable condos will not qualify, though eligibility depends on the specific project and program.

Q6. What are the legal considerations for non-warrantable condos?

Active lawsuits are the biggest hurdle. If the HOA is suing the developer over structural issues, lenders will back out immediately because of potential financial instability. Always have a real estate attorney review the lawsuit details first.

Q7. What is the typical down payment for a non-warrantable condo loan?

While a standard condo might only require 3% to 5% down, you should expect to put down 20% to 30% for a non-warrantable unit. Lenders require this extra equity to offset their financial risk.

Q8. Can a non-warrantable condo become warrantable?

Yes, absolutely. Once the root issue is fixed, whether the HOA settles its lawsuit, more owner-occupants move in, or the board balances its reserve funds, the building can be re-evaluated and transition back to warrantable status.

Final Word: Is It a Bad Idea to Buy a Non-Warrantable Condo?

Buying a non-warrantable condo is not inherently a bad move, but it requires careful planning. If you are an investor with cash or have a healthy down payment, you can secure a great property in a prime area for a bargain.

But if you are a first-time buyer on a tight budget, the higher rates and strict terms might stretch you too thin. I always recommend having a trusted mortgage professional and a real estate lawyer review the HOA's financial health before you make any commitments.