【2026】Non-Warrantable Condo Loan: Which to Choose?

You found your perfect condo, but your bank just denied your mortgage, leaving you stranded. They said the building is "non-warrantable"—a term that leaves many buyers feeling completely hopeless. I understand your frustration. Over the years, I have helped countless borrowers navigate this exact roadblock. The good news is that you still have excellent options. Let me guide you through the best non-warrantable condo loans available today.

Key Takeaways

-

Non-warrantable condos do not meet Fannie Mae or Freddie Mac condominium eligibility standards.

-

You can still secure financing using specialized portfolio or Non-QM loans.

-

Expect slightly higher interest rates and down payments between 15% and 25%.

-

Working with an experienced local loan officer will streamline your approval process.

What is a Non-Warrantable Condo Loan?

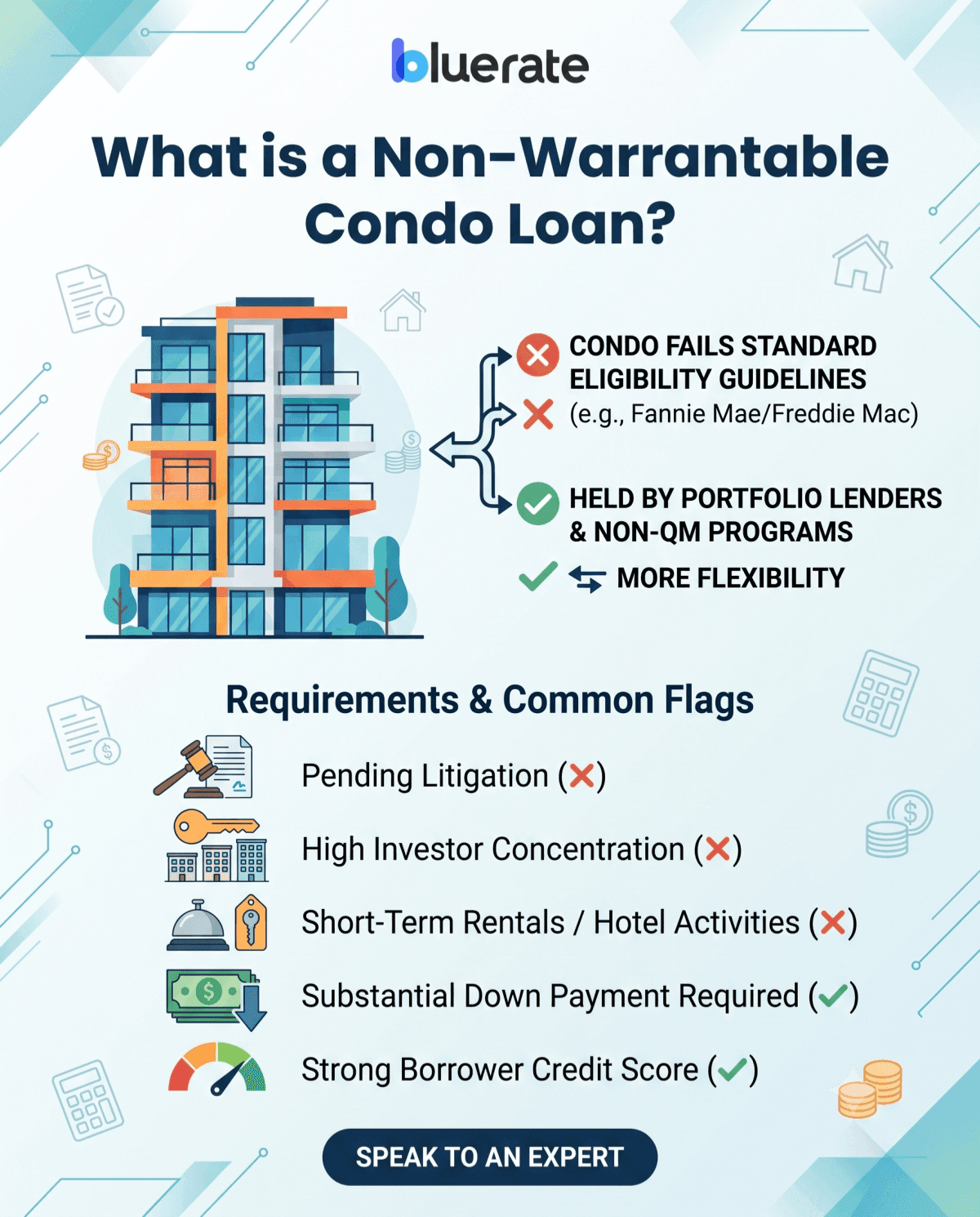

In my professional experience, the biggest misconception about non-warrantable condos is that they are structurally unsafe or bad investments. That is simply not true. A condo is considered non-warrantable when it fails to meet the condominium project eligibility guidelines used by government-sponsored enterprises such as Fannie Mae and Freddie Mac. Because standard agency lenders cannot package and sell these mortgages on the secondary market, they decline them.

To buy a unit in one of these properties, you need a non-warrantable condo loan. These loans are often offered through portfolio lending or Non-QM programs. Private lenders or portfolio banks choose to keep these loans on their own balance sheets rather than selling them. Because they retain the loan, they can apply their own underwriting standards within their risk policies.

Also Read: Warrantable vs Non-Warrantable Condo: Detailed Guide

Requirements of a Non-Warrantable Condo Loan

When we look at requirements, we must analyze both the property itself and your personal financial profile. If the homeowners association (HOA) fails certain tests, the building is flagged. To secure the loan anyway, you must meet the lender's custom criteria:

-

High Investor Concentration: A large share of the units is owned by investors or non-owner-occupants, which may make the project ineligible.

-

Pending Litigation: The HOA or condominium project is involved in unresolved legal action that may affect eligibility.

-

Short-Term Rentals: Some hotel-like rental activity or transient rental operations can make the project ineligible.

-

Borrower Credit Score: Minimum credit requirements vary by lender, but stronger credit is usually needed.

-

**Down payment: **Many lenders require about 20% or more, though requirements vary by lender and product.

Types of Non-Warrantable Condo Loans

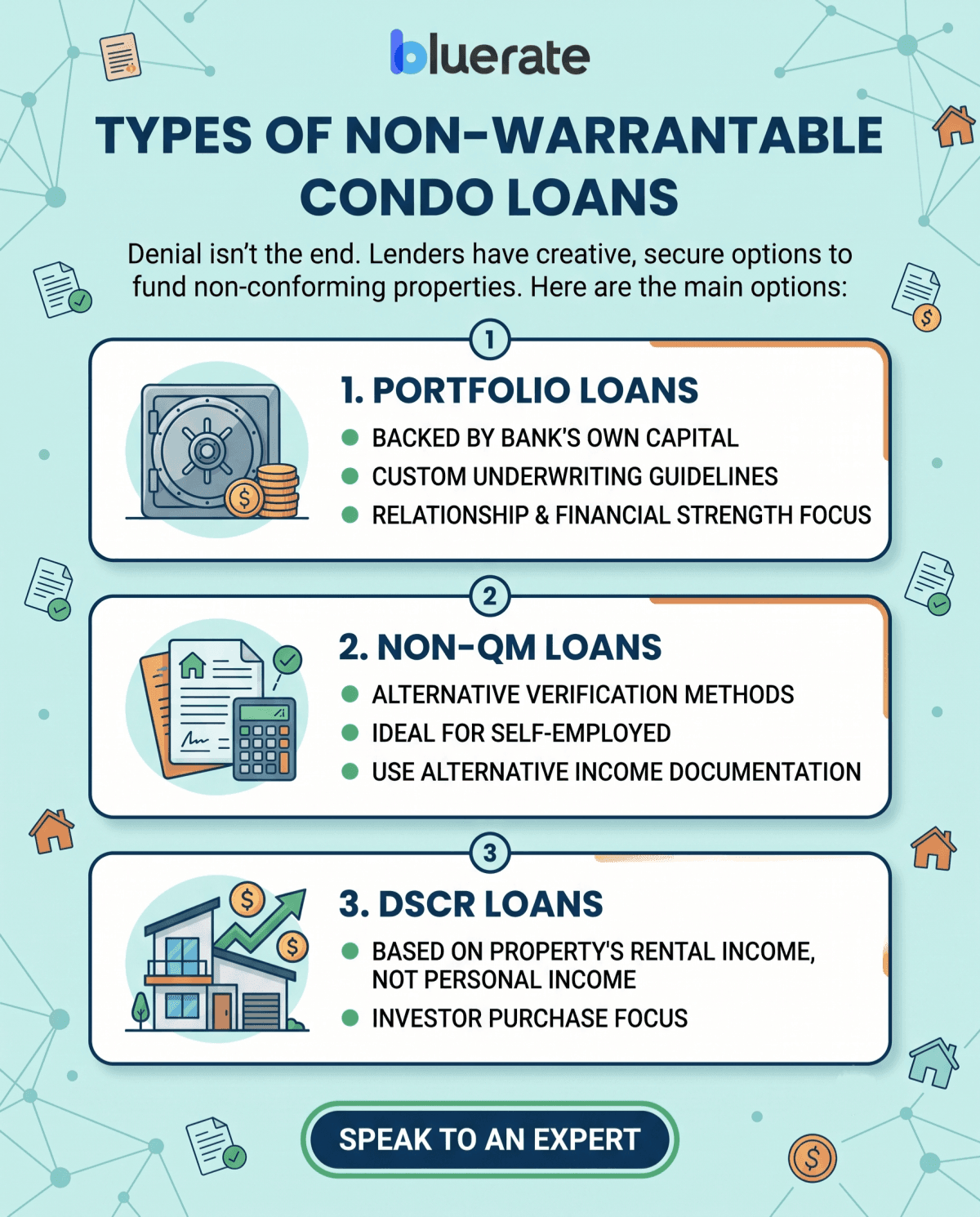

In my practice, I always tell clients that being denied a conventional mortgage is not the end of the road. Lenders have designed highly creative, secure loan types to fund these non-conforming properties. Here are the three main options you can choose from:

-

Portfolio Loans: These are mortgages backed by the bank's own capital. Since they do not sell the loan to Fannie Mae, the bank designs its own underwriting guidelines, focusing on your overall relationship and financial strength.

-

Non-QM (Non-Qualified Mortgage) Loans: These loans use alternative methods to verify your financial health. They are commonly used by self-employed borrowers and others who may benefit from alternative income documentation.

-

DSCR (Debt Service Coverage Ratio) Loans**: For investor purchases, these loans are primarily underwritten based on the property's rental income rather than the borrower's personal income. **Instead, we qualify you based solely on the projected rental income of the property.

Tips to Pick a Non-Warrantable Condo Loan

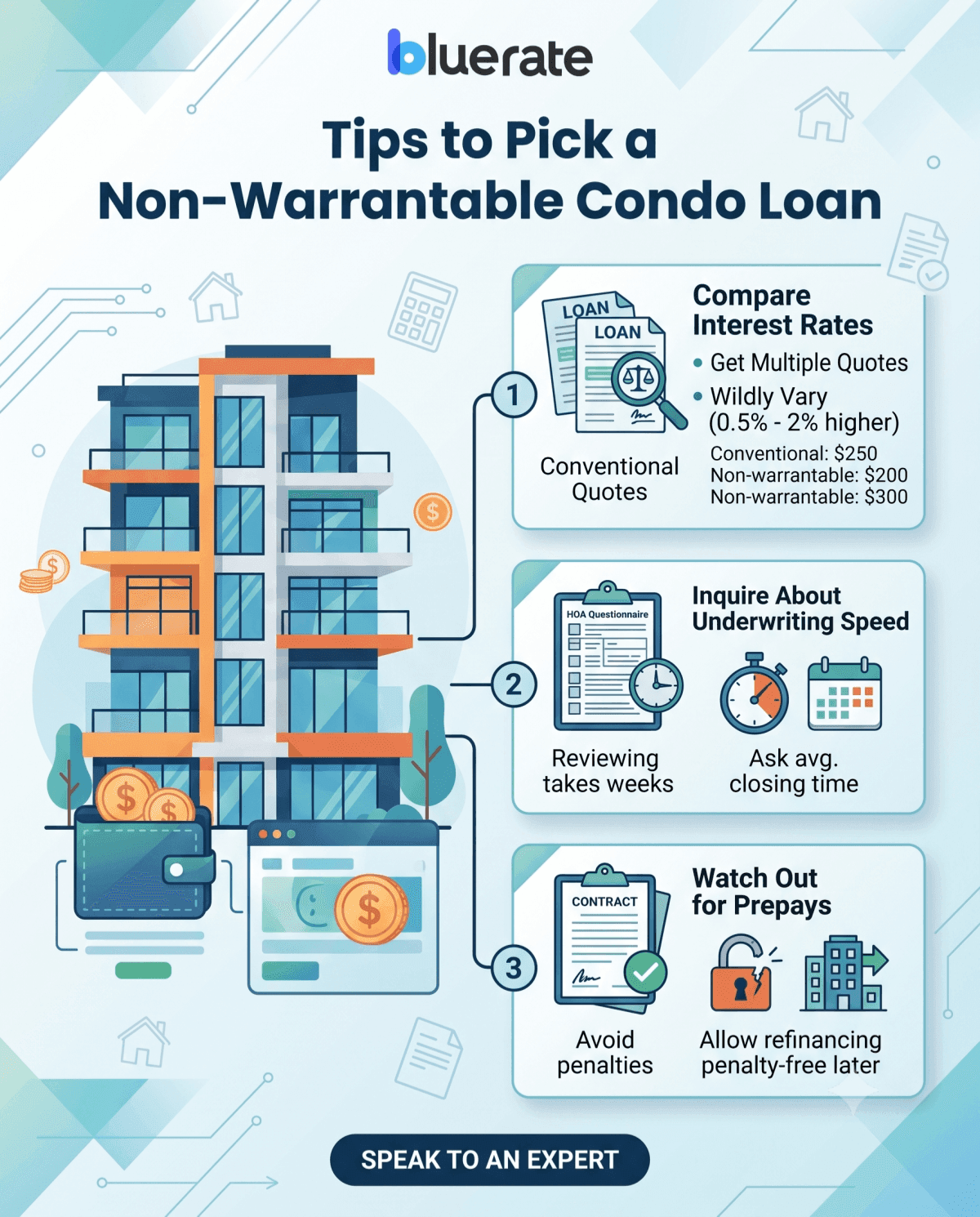

Picking the right mortgage requires a strategic approach. Over the years, I have seen buyers rush into bad terms out of desperation. To ensure you protect your wallet, keep these practical tips in mind:

-

Compare Interest Rates: Because lenders hold these loans on their own books, rates can vary wildly. Expect them to be 0.5% to 2% higher than conventional rates, so get multiple quotes.

-

Inquire About Underwriting Speed: Reviewing an HOA questionnaire can take weeks. Ask the lender about their average closing time for non-warrantable properties.

-

Watch Out for Prepays: Some non-QM products carry prepayment penalties. Ensure your loan allows you to refinance penalty-free later if the building becomes warrantable.

Expert Tip: Financing guidelines for non-warrantable condos can change overnight. Rather than cold-calling dozens of banks, you can use Bluerate to get a free consultation with local, vetted loan officers. Finding an LO who has successfully closed similar deals in your specific neighborhood will save you time and prevent unnecessary loan denials.

Some Non-Warrantable Condo Loan Lenders to Consider

While many institutional banks immediately decline these properties, several specialized lenders in the US market have built robust programs for them:

-

PrimeLending: Excellent for buyers with smaller down payments, offering non-warrantable condo programs with a high Loan-to-Value (LTV) ratio of up to 85%.

-

First National Bank of America: A premier portfolio lender that specializes in alternative financing up to 80% of the property's value.

-

First Heritage Mortgage: Provides flexible, specialized guidelines and custom loan programs tailored specifically for specialty properties.

-

Mortgage Center: Known for crafting tailored, creative financing solutions for buyers purchasing highly unique or otherwise ineligible condominium units.

Remember that because each condominium development has a unique set of challenges, guidelines can change, so I highly recommend consulting them directly to evaluate your specific scenario.

FAQs About Non-Warrantable Condo Loans

Q1. Can I get an FHA or VA loan for a non-warrantable condo?

Not always. FHA and VA loans have their own condominium eligibility rules, and some non-warrantable condos may not qualify. If an HOA has significant financial or project-related issues, the condo may not meet FHA or VA eligibility requirements.

Q2. Why do these loans require a larger down payment?

Lenders require larger down payments to offset their investment risk. Since these mortgages cannot be sold on the secondary market to GSEs, the bank bears the entire financial loss if you default. A larger down payment acts as a protective equity cushion for the lender.

Q3. How do I find out if a condo building is non-warrantable?

The most reliable method is to have your real estate agent request a copy of the HOA questionnaire from the property management company. A specialized loan officer can often review the HOA questionnaire quickly, but the timing depends on the lender and document availability.

Q4. Are interest rates higher for non-warrantable condo loans?

Yes, you should expect interest rates to be roughly 0.5% to 2% higher than standard conventional rates. This rate premium directly compensates the portfolio lender for the increased risk and the lack of liquidity that comes with holding the loan on their own books.

Q5. Can an investor buy a non-warrantable condo using a DSCR loan?

Absolutely. Many savvy investors I work with prefer DSCR loans for non-warrantable properties. It allows them to bypass personal tax returns and qualify using the rental income generated by the condo itself, making the transaction incredibly smooth.

Final Word

Finding out your dream home is non-warrantable is undoubtedly stressful, but it certainly does not mean your homeownership journey is over. With the right financial tools, you can easily secure a specialized loan and close the deal.

The absolute fastest way to save your transaction is to partner with a local expert who knows these complex guidelines inside and out. I highly encourage you to utilize Bluerate to connect with verified, professional Loan Officers in your area today for a free, no-obligation consultation.