How to Get a USDA Loan? Qualify, Apply & Approve

I remember when I first wanted to buy a house, the biggest hurdle wasn't the monthly mortgage payments. It was scraping together that dreaded 20% down payment. If you're in the same boat, let me introduce you to a lifesaver: the USDA loan. It offers 100% financing, meaning absolutely zero down.

In today's challenging 2026 housing market, this program is a true game-changer. I'll walk you through exactly how these mortgages work, the realistic eligibility requirements, and the step-by-step process to get your application approved without the usual headaches.

Key Takeaways

- Zero Down Payment: You can buy a house with 0% down.

- Location Matters: Properties must sit in eligible rural or suburban areas.

- Income Caps: Your total household earnings cannot exceed specific regional limits.

- Primary Residences Only: You cannot use this program for investment properties or vacation homes. The home must become your primary residence, and you typically must move in within 60 days of closing.

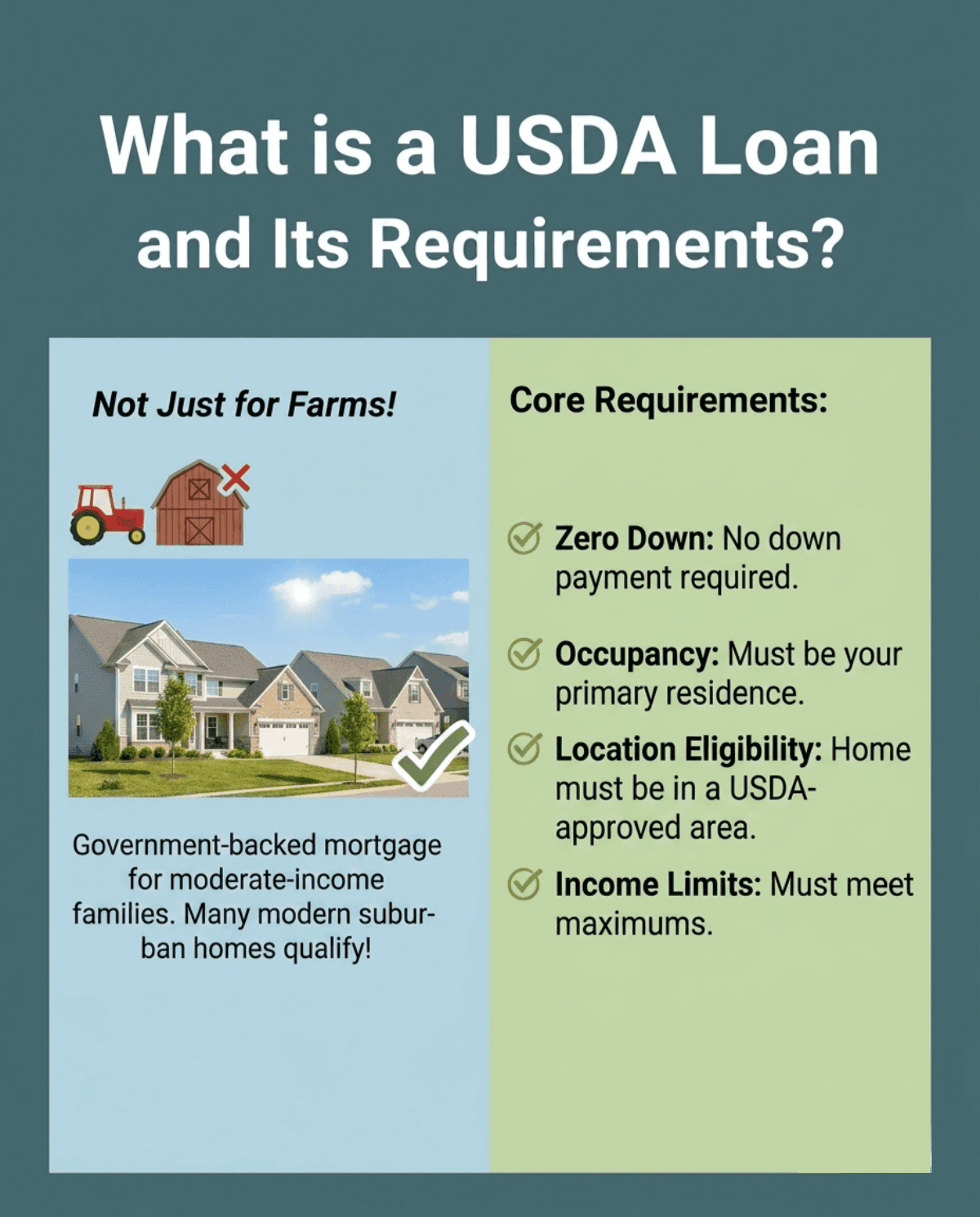

What is a USDA Loan and Its Requirements?

A USDA loan is a government-backed mortgage supported by the United States Department of Agriculture. Its primary goal is to make homeownership affordable for folks with moderate incomes.

When I first heard "Agriculture," I pictured buying a farm with tractors. That's a massive myth! Many beautiful, modern suburbs just outside major cities actually qualify.

Here are the core requirements you must meet:

- Zero Down: No down payment is required to purchase the home, but you will still need funds to cover closing costs and any upfront fees, unless those are covered by grants or down payment assistance programs.

- Occupancy: It must be your primary residence. You can't rent it out or use it as a summer cabin.

- Location Eligibility: The home must sit within a USDA-approved geographic footprint.

- Income Limits: Your family must not earn more than the set maximums to prove you genuinely need the assistance.

Also Read: USDA Loan vs FHA Loan: Which is Your Best Fit?

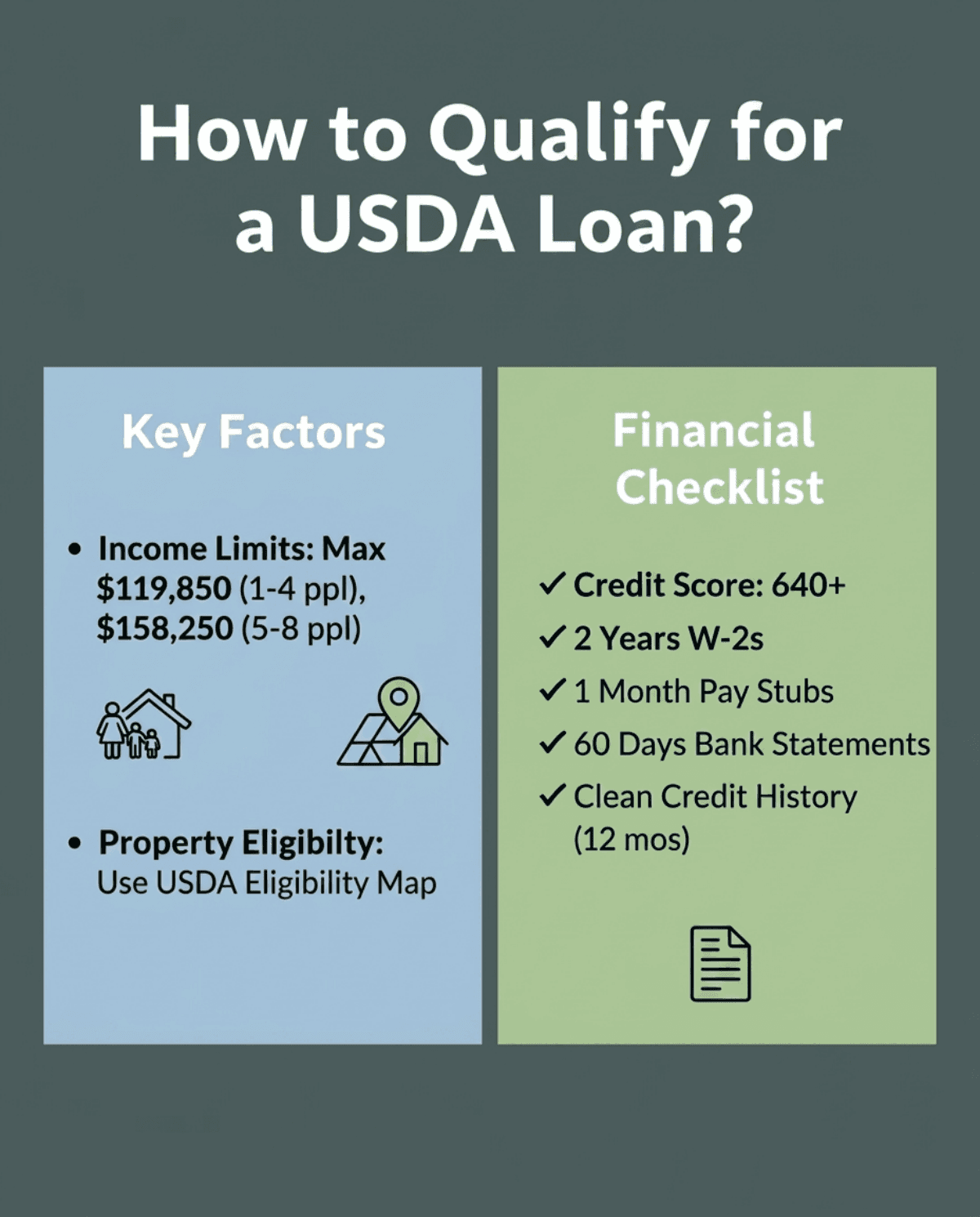

How to Qualify for a USDA Loan?

Qualifying comes down to two main things: your finances and the house's zip code. Once I understood this dynamic, the whole puzzle made sense. Here's exactly what they look at:

- Income limits: For 2026, the standard income limit in many counties is $119,850 for a household of up to four and $158,250 for a household of five to eight, though higher-cost areas may have elevated limits. Keep in mind, this calculates total household income, meaning every working adult living there, even if they aren't on the mortgage.

- Property eligibility: Don't guess if a town qualifies. Always plug the exact address into the official USDA Property Eligibility Map.

- Credit requirements: You'll typically need a credit score of at least 640 to pass their automated Guaranteed Underwriting System (GUS). Lower scores are possible but require a tougher manual review.

- Quick checklist: Before applying, gather two years of W-2s, a month of pay stubs, 60 days of bank statements, and ensure you have a clean credit history for the past 12 months.

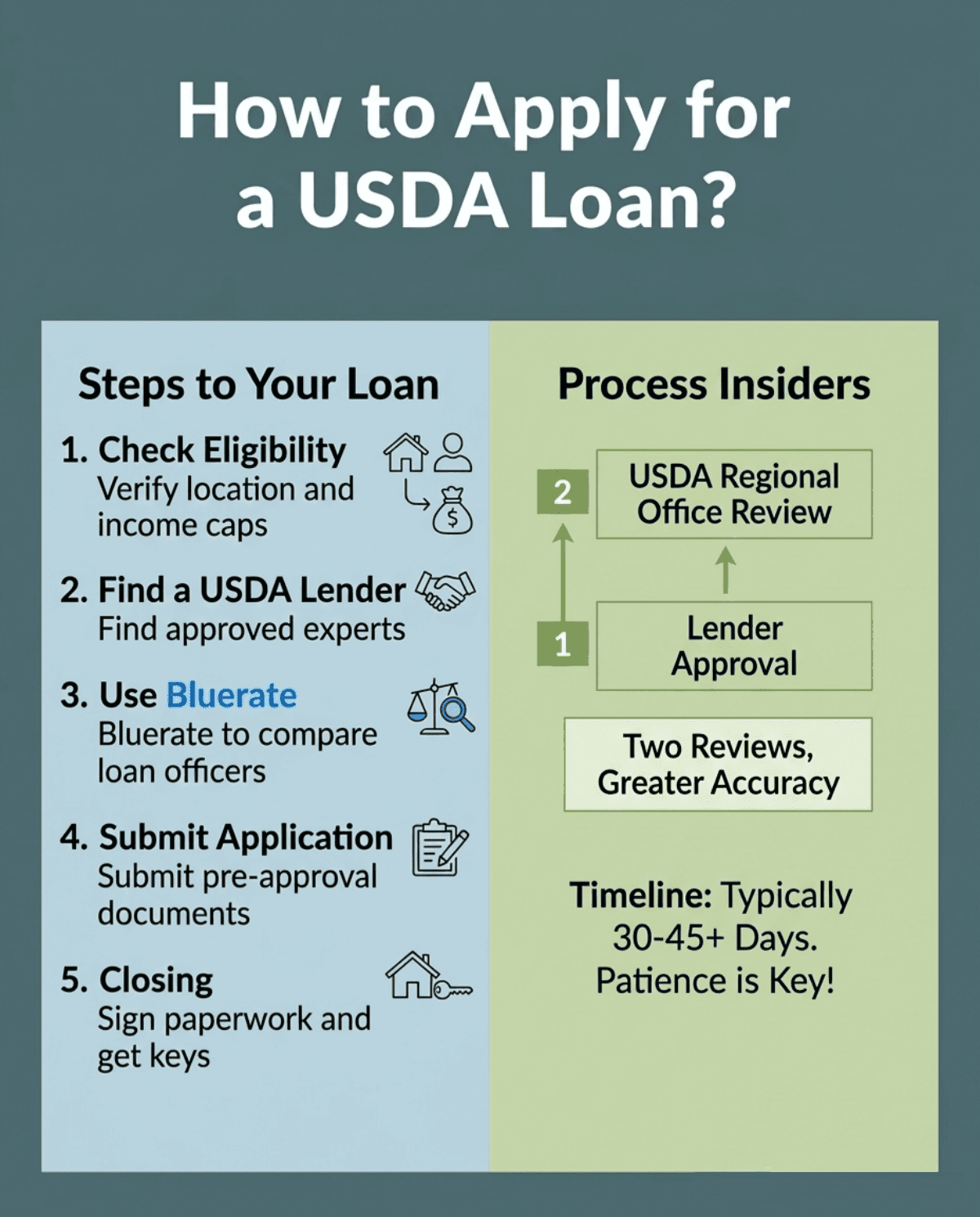

How to Apply for a USDA Loan?

The application process can feel daunting at first glance, but breaking it down into simple steps saved me a lot of stress.

- Step 1: Check eligibility: First, verify your target neighborhood on the official map and ensure your household income stays below the 2026 caps.

- Step 2: Find a USDA-approved lender: Not every bank handles these specific mortgages. I highly recommend using Bluerate to easily compare top-tier loan officers online for free. It matches you with experts who actually know the rural housing guidelines inside and out.

- Step 3: Submit application: Hand over your financial documents to get pre-approved. This shows sellers you are a serious buyer.

- Step 4: Underwriting: Here is an insider secret that USDA loans go through "Dual Underwriting." Your lender approves it first, then it goes to the regional government office for a second review. It typically takes 30 to 45 days, and sometimes longer, due to the dual underwriting process, so patience is key.

- Step 5: Closing: Once both parties give the green light, you'll sign the final paperwork, pay any closing costs, and finally get the keys to your new home.

Tips: How to Get Approved for a USDA Loan Faster?

Because of the dual underwriting process, you really can't afford any hiccups. Here is some hard-earned advice to speed up your approval:

- Improve DTI: Keep your Debt-to-Income ratio in check. The USDA prefers a ratio of 29/41 (29% of income goes to housing, 41% to total debts). Pay down small credit cards if you can.

- Avoid common mistakes: Do absolutely nothing that triggers a hard credit pull. Do not finance a new car, open a retail store card, or change jobs while your application is pending.

- Timeline expectations: Have every single document ready before the underwriter even asks. Being proactive with your W-2s and bank statements keeps your file at the top of the pile and prevents agonizing delays.

FAQs About Getting a USDA Loan

Q1. What is the 20% rule for USDA?

Many people misunderstand this. The program targets buyers who genuinely lack down payment funds. If you already have enough liquid assets, such as cash in a savings account, to comfortably put 20% down for a conventional loan, you generally do not meet the USDA's "lack of down payment funds" requirement and may be disqualified from the guaranteed loan program.

Q2. Is it hard to get USDA approved?

If you choose a home in an eligible area and stay within the regional income limits, USDA loans can have lower financial barriers than many conventional mortgages, especially because they require zero down payment and can be more flexible on credit. However, approval still depends on your debt‑to‑income ratio, credit history, and documentation.

Q3. How hard is it to get a USDA land loan?

It is quite difficult if you just want to buy pure, raw land to hold onto. The government generally won't finance an empty lot. However, if you apply for a "construction-to-permanent loan" to immediately build your primary residence, approval becomes totally possible.

Q4. What is the minimum credit score for a USDA loan?

While USDA does not enforce a single official minimum credit score, most USDA‑approved lenders look for a score of about 640 or higher to qualify for approval through the automated Guaranteed Underwriting System (GUS). If your score falls below 640, you'll face a strict manual underwriting process requiring strong compensating factors.

Q5. What are USDA 502 loan requirements?

It helps to know there are two different types. The Section 502 Direct loan is issued directly by the government and targeted at "low-income" applicants. Conversely, the Section 502 Guaranteed loan, which we've discussed in this guide, is issued by private lenders for "moderate-income" buyers.

Final Word

Buying a house without draining your bank account for a down payment felt like an impossible dream to me at first, but the USDA loan program makes it a tangible reality. By understanding the strict location boundaries, keeping your household income within the 2026 limits, and surviving the dual underwriting process with patience, you can secure 100% financing.

Don't let the paperwork intimidate you. Having the right professional by your side makes all the difference. Your very first step is to verify your target home's address on the official map. After that, head over to Bluerate to instantly match with experienced USDA loan officers. They will expertly guide you through the rest of your zero-down homebuying journey!