Best No Income Mortgage Loans: Which One is Your Pick?

I've seen so many brilliant freelancers and small business owners get their mortgage applications stamped "denied" simply because they lack a standard W-2. It's incredibly frustrating. But not having a traditional paycheck doesn't mean your homeownership dream is over. "No income mortgage loans", now properly known as Non-QM loans, are the perfect workaround.

The hardest part? Finding a loan officer who actually understands these niche products. That's why later in this guide, I'll show you how the Bluerate AI Agent can instantly match you with a verified expert who gets your unique financial situation.

What Actually is a "No Income" Mortgage Loan?

Let's clear the air right away: the infamous "NINJA" (No Income, No Job, and No Assets) loans from the 2008 financial crisis are dead and gone. Today's "no income" mortgages are actually Non-Qualified Mortgages (Non-QM).

By federal law, lenders still need to ensure your Ability to Repay (ATR). They just don't need traditional tax returns or pay stubs to prove it. Instead, they use alternative verification methods like reviewing your bank deposits, total liquid assets, or the potential rental income of the property you want to buy. It's all about proving your real-world cash flow.

Best No Income Mortgage Loans to Choose in 2026

Based on what I'm seeing in the current real estate market, alternative financing is booming. If you're stepping outside the conventional lending box this year, here are the five most popular alternative loan options that might just save your home purchase.

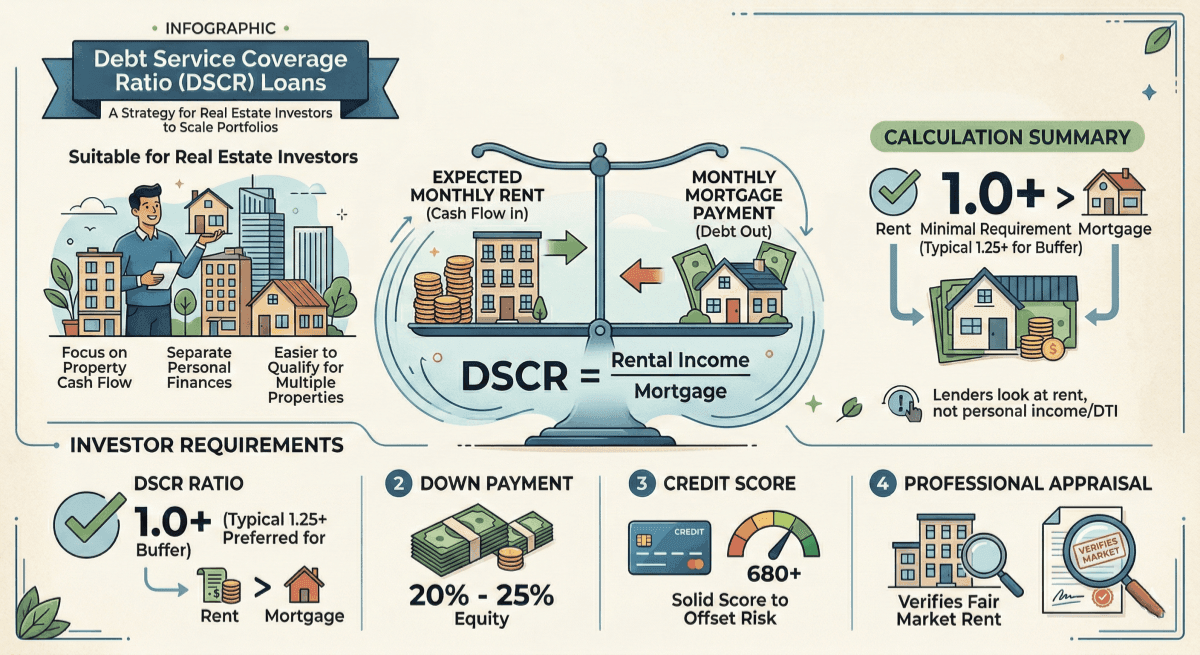

Debt Service Coverage Ratio (DSCR) Loans

Suitable for: Real estate investors

Whenever I talk to property investors who want to scale their portfolios quickly, I always point them toward DSCR loans. Lenders don't look at your personal income or debt-to-income (DTI) ratio at all. Instead, they focus entirely on the property's cash flow. If the expected monthly rent from the property covers the monthly mortgage payment, you're usually good to go. It's a brilliant way to separate your personal finances from your investment ventures, making it much easier to qualify for multiple investment properties.

Requirements:

-

A minimum DSCR ratio of 1.0 (meaning rent covers the mortgage), though many lenders require 1.25 or higher for added buffer.

-

A substantial down payment, typically ranging from 20% to 25%.

-

A solid credit score, usually 680 or above, to offset the lender's risk.

-

A professional appraisal specifically verifying the projected fair market rent.

Also Read:

- Full Guide: How to Get a DSCR Loan? Everything Here

- DSCR Loan Requirements: Ratio, Credit Score, Down Payment, Type

- Best DSCR Lenders Near Me: Highlights, Pros & Cons

- DSCR Loan Pros and Cons: Is It the Right Strategy for Your Investment?

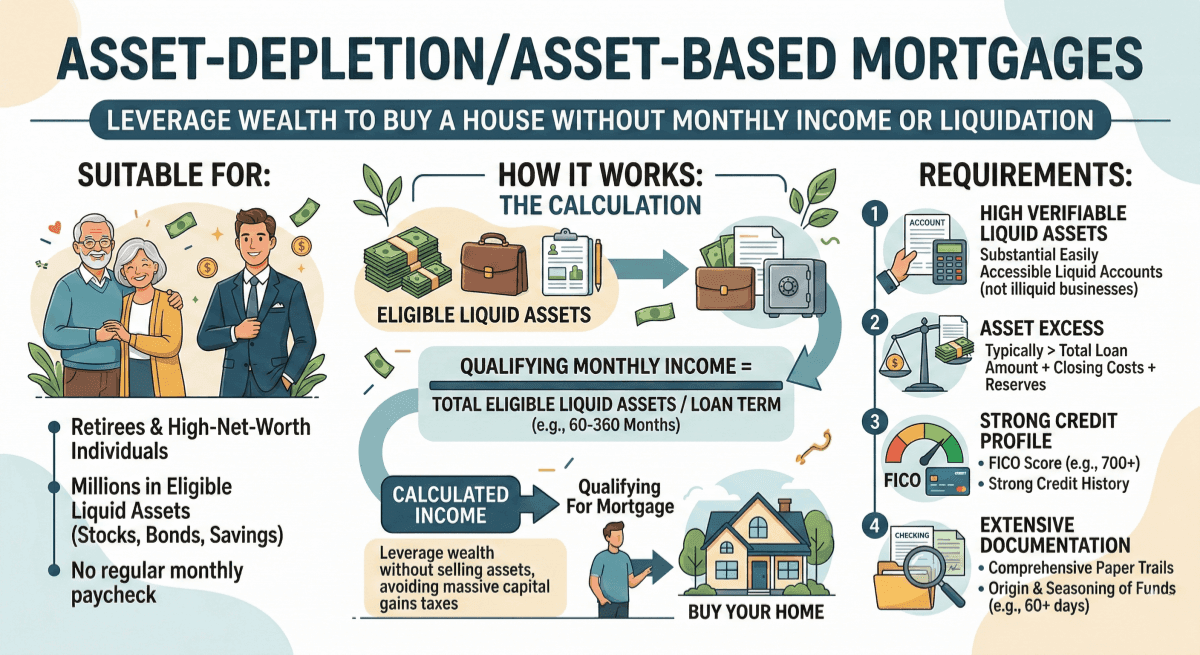

Asset-Depletion/Asset-Based Mortgages

Suitable for: Retirees and high-net-worth individuals

Imagine you have millions in liquid assets but no regular monthly paycheck because you're happily retired. Traditional banks might still reject you. That's where asset-depletion loans come in. Instead of looking at a monthly salary, the lender calculates a "qualifying monthly income" by dividing your total eligible liquid assets, like stocks, bonds, or retirement savings, by the loan term, which is usually 60 to 360 months. I've found this to be an incredibly elegant solution for wealthy buyers. It allows you to leverage your wealth to buy a house without actually liquidating it and triggering massive capital gains taxes.

Requirements:

-

High verifiable liquid assets (accounts must be easily accessible, not tied up in illiquid businesses).

-

Assets must typically exceed the total loan amount plus closing costs and reserves.

-

A strong credit profile, often requiring a 700+ FICO score.

-

Extensive paper trails showing the origin and seasoning (usually 60+ days) of the funds.

Also Read:

Also Read:

- Best Asset Depletion Lenders: Top Rank Here

- Top Picks: Best Asset-Based Mortgage Lenders

- What is Asset-Based Loan in Mortgage? Definition and Example

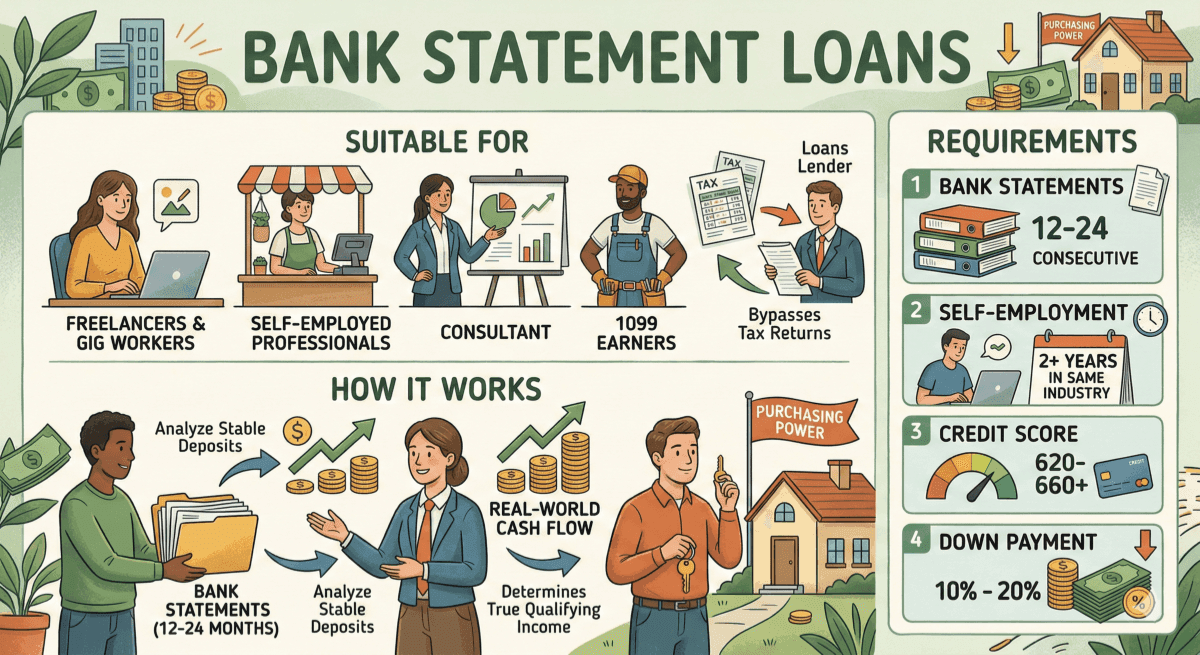

Bank Statement Loans

Suitable for: Self-employed professionals, freelancers, and 1099 earners

This is hands-down my favorite option for gig workers and business owners. If you run a business, you likely take every legal tax deduction possible, which makes your net income look tiny on your tax returns. Bank statement loans bypass tax returns completely. Lenders will ask for your personal or business bank statements over a 12- to 24-month period. They analyze the steady flow of deposits to determine your actual, real-world cash flow and calculate your true purchasing power.

Requirements:

-

Provide 12 to 24 months of consecutive personal or business bank statements.

-

Proof of being self-employed in the same line of work for at least two years.

-

A decent credit score, generally starting around 620-660, though some programs accept as low as 620.

-

A down payment of at least 10% to 20%, depending on your credit profile.

Also Read:

- Self-Employed Mortgage Guide: How to Get, Requirements

- Best Mortgage Lenders for Self-Employed: Top-Rated Picks

- Self-Employed Mortgage Requirements: What to Prepare?

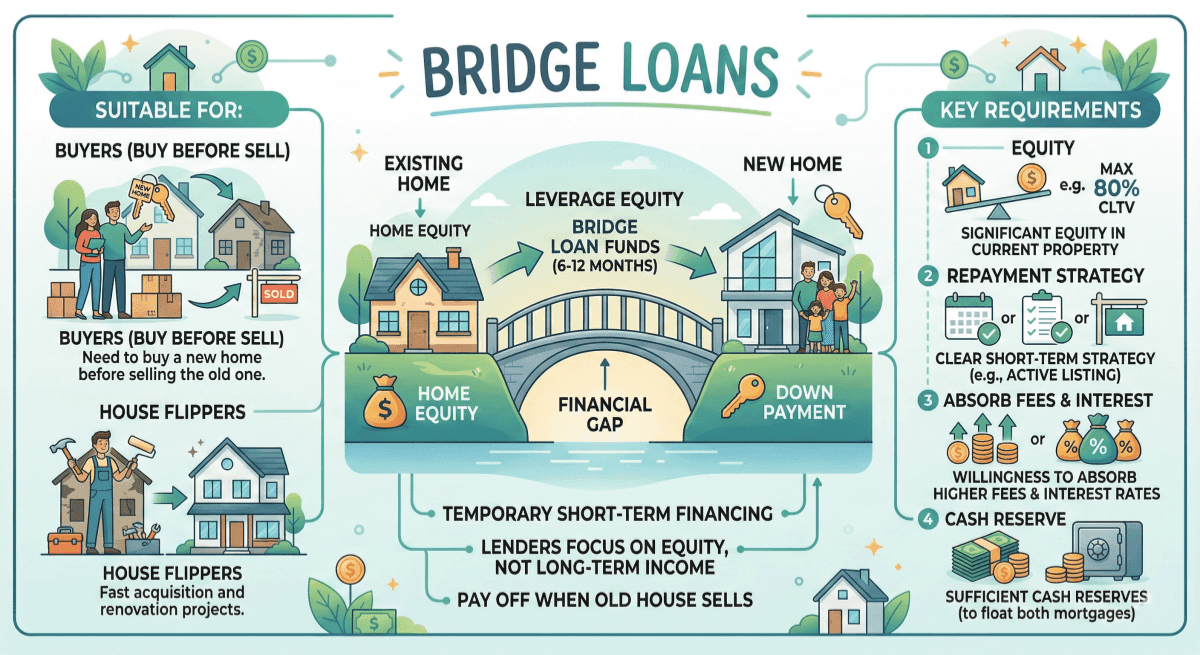

Bridge Loans

Suitable for: Buyers needing to buy before selling, and house flippers

In a competitive housing market, you sometimes need to jump on a new home before your current one sells. A bridge loan literally "bridges" that financial gap. It's a short-term financing tool that leverages the equity in your existing home to supply the down payment for the new one. Because it's temporary, usually lasting 6 to 12 months, lenders are far more concerned with your home equity than your long-term income stability. Once you sell your old house, you simply pay off the bridge loan.

Requirements:

-

Significant equity in your current property. Lenders usually max out at an 80% combined loan-to-value ratio).

-

A clear, short-term repayment strategy, like an active listing agreement for your current home.

-

Willingness to absorb higher upfront origination fees and interest rates.

-

Sufficient cash reserves to float both mortgages temporarily if needed.

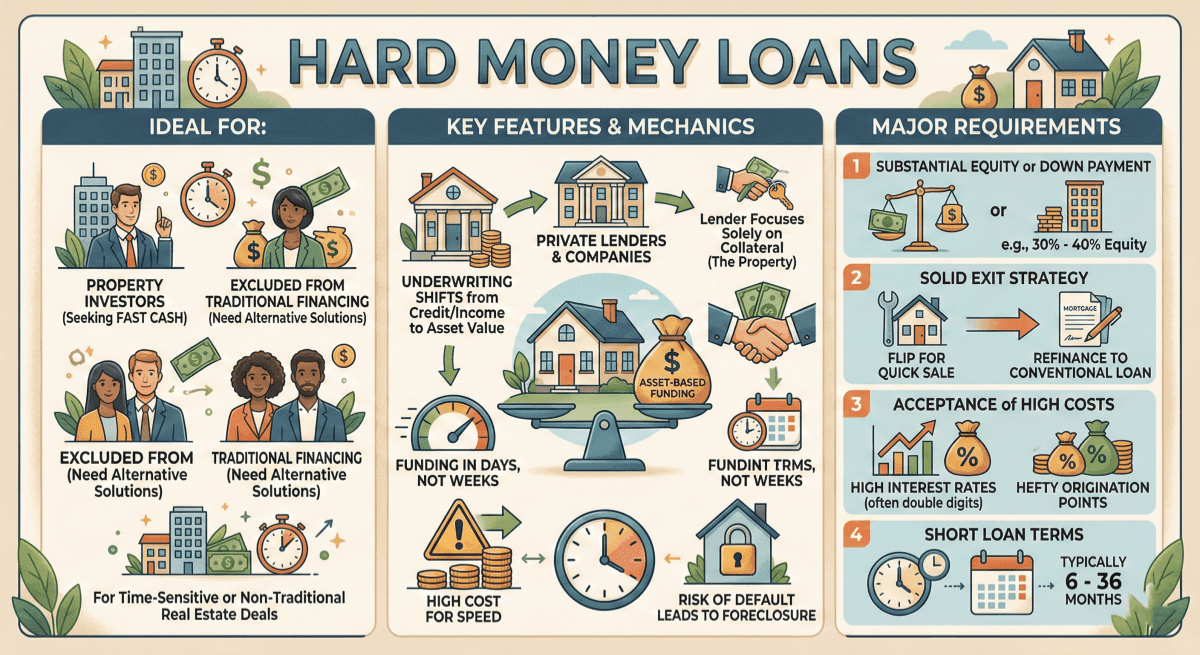

Hard Money Loans

Suitable for: Property investors needing fast cash and those excluded from traditional financing

Hard money loans are the wild west of real estate financing, but they serve a crucial purpose. Issued by private investors or specialized companies, these loans are entirely asset-based. The lender doesn't really care about your credit score or W-2s. They only care about the collateral, the property itself. If you default, they take the property. Because the underwriting process skips standard income checks, you can secure funding in days rather than weeks. However, I always warn people: this speed comes at a steep price.

Requirements:

-

Substantial down payment or existing property equity (often 30% to 40%).

-

A rock-solid exit strategy, such as flipping the house for a quick sale or refinancing into a long-term conventional loan.

-

Acceptance of exceptionally high interest rates (often hitting double digits) and hefty origination points.

-

Very short loan terms, typically ranging from 6 to 36 months.

Key Considerations for a No Income Mortgage Loan

While skipping the W-2 requirement is incredibly convenient, alternative income loans do come with trade-offs. Lenders are taking on more risk, and naturally, they pass that risk onto you. Before signing anything, keep these factors in mind:

-

Higher Interest Rates: Expect your rate to be noticeably higher than standard conventional loans.

-

Larger Down Payments: To offset their risk, lenders usually demand 20% to 30% upfront.

-

Strong Credit Score: Without traditional income, your credit history is key, with minimums typically 620-700 depending on the lender and program.

-

Cash Reserves: Many lenders will require you to have several months' worth of mortgage payments sitting in a savings account just in case.

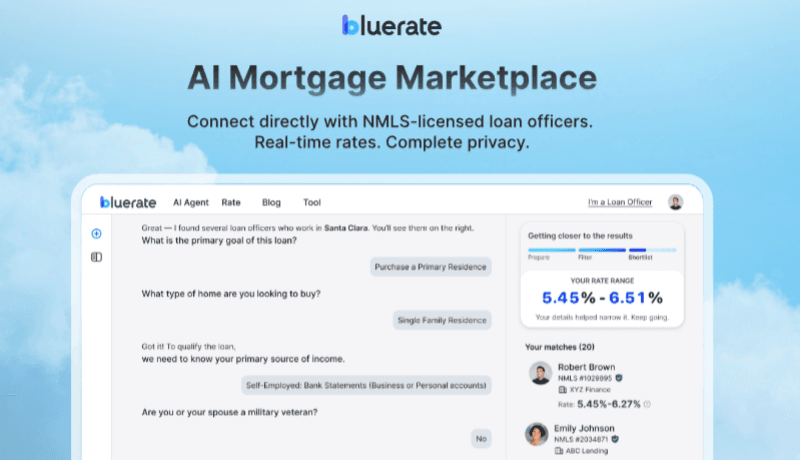

Tip: How to Quickly Find a No Income Loan Officer?

Let's be honest: Non-QM loans are a highly specialized niche. If you walk into your local big-box bank asking for one, the teller will likely just stare at you blankly. Trying to hunt down these experts yourself often leads to immediate rejections or, worse, non-stop spam calls from aggressive brokers.

This is exactly why I recommend using Bluerate. It's an all-in-one marketplace designed to bridge the gap between borrowers and specialized loan officers. Here is what makes it a game-changer for self-employed buyers:

-

Smart AI Chat: Think of it as your 24/7 mortgage buddy. Through a natural chat, it calculates your DTI and instantly matches you with a Non-QM expert who actually understands your situation.

-

Privacy First: You can shop anonymously. Bluerate never sells your data, ensuring a completely spam-free experience.

-

Verified, Real-Time Rates: Say goodbye to fake teaser numbers. You get to compare accurate, real-time rates from over 30 lenders.

-

Top Non-QM Experts: The platform features verified professionals who specialize in 1099, LLC, and alternative income challenges.

-

Fast Track: Using their intuitive tools, you can get pre-qualified 2.5x faster and close 20% sooner.

FAQs About Best No Income Mortgage Loans

Q1. Can I get a mortgage loan with strictly zero income?

No. Even with alternative loans, lenders must comply with federal "Ability to Repay" (ATR) rules. They won't ask for a W-2, but you must prove you can make payments using liquid assets, 12-24 months of bank deposits, or property rental income.

Q2. Do No Income mortgage loans require a higher credit score?

Yes, generally. Because lenders aren't verifying traditional income, they carry more risk. To qualify for decent rates, you typically need a credit score of at least 620, though aiming for 680-700+ unlocks better rates.

Q3. Are interest rates higher on bank statement loans?

Yes. You can expect interest rates on bank statements and other Non-QM loans to be about 1% to 2% higher than standard conventional mortgages. Think of this slight premium as the reasonable cost of gaining financial flexibility for your self-employed lifestyle.

Conclusion

As we navigate the housing market in 2026, relying solely on a traditional W-2 is no longer the only way to get the keys to your dream home. Whether you opt for a Bank Statement loan to highlight your freelance hustle or a DSCR loan to expand your investment portfolio, the doors are wide open.

Please don't waste your time getting frustrated with traditional banks. Instead, head over to Bluerate and click "Chat with AI". Spend just a few minutes talking with the Bluerate AI Agent to securely and privately discover your customized loan options, and connect with a vetted Non-QM loan officer today. Your new home is waiting!