What is a Warrantable Condo? Learn Everything Here

Few things are more frustrating than falling in love with a beautiful condominium, only to have your conventional loan denied at the last minute. In my years guiding homebuyers through the mortgage maze, I've seen this scenario play out far too often.

It usually comes down to one critical term: warrantability. Simply put, a warrantable condo is a property that meets specific guidelines, making it eligible for standard, low-cost financing.

Key Takeaways

Before diving into the complex details, here are the vital points you need to know about condo warrantability:

-

Conventional Eligibility: Warrantable condos meet Fannie Mae and Freddie Mac criteria, qualifying you for lower down payments and competitive mortgage rates.

-

Non-Warrantable Alternatives: Non-warrantable properties are tougher to finance, requiring specialty non-QM or portfolio loans.

-

Recent Changes: Major mortgage rule updates have simplified some rules, like relaxing owner-occupancy limits for established projects, but have also phased out simple "Limited Reviews" for larger developments.

What Is a Warrantable Condo?

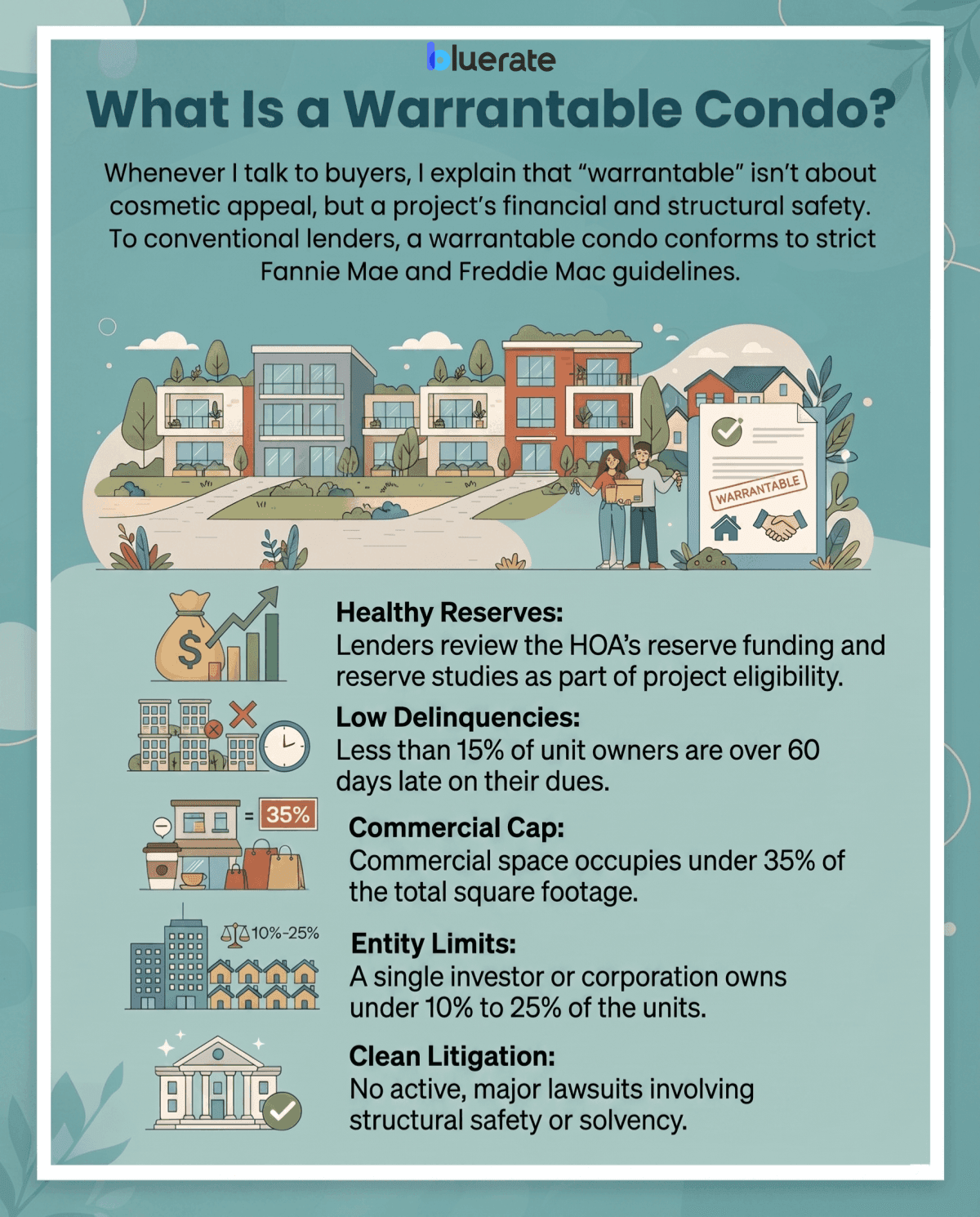

Whenever I talk to buyers, I explain that "warrantable" isn't about cosmetic appeal, but a project's financial and structural safety. To conventional lenders, a warrantable condo conforms to strict Fannie Mae and Freddie Mac guidelines. Because these government-sponsored enterprises buy these mortgages on the secondary market, banks can offer you standard interest rates and low down payment options. It keeps the market highly liquid and accessible.

Generally, a warrantable project must feature:

-

Healthy Reserves: Lenders review the HOA's reserve funding and reserve studies as part of project eligibility.

-

Low Delinquencies: Less than 15% of unit owners are over 60 days late on their dues.

-

Commercial Cap: Commercial space occupies under 35% of the total square footage.

-

Entity Limits: A single investor or corporation owns under 10% to 25% of the units.

-

Clean Litigation: No active, major lawsuits involving structural safety or solvency.

What Makes a Condo Non-Warrantable?

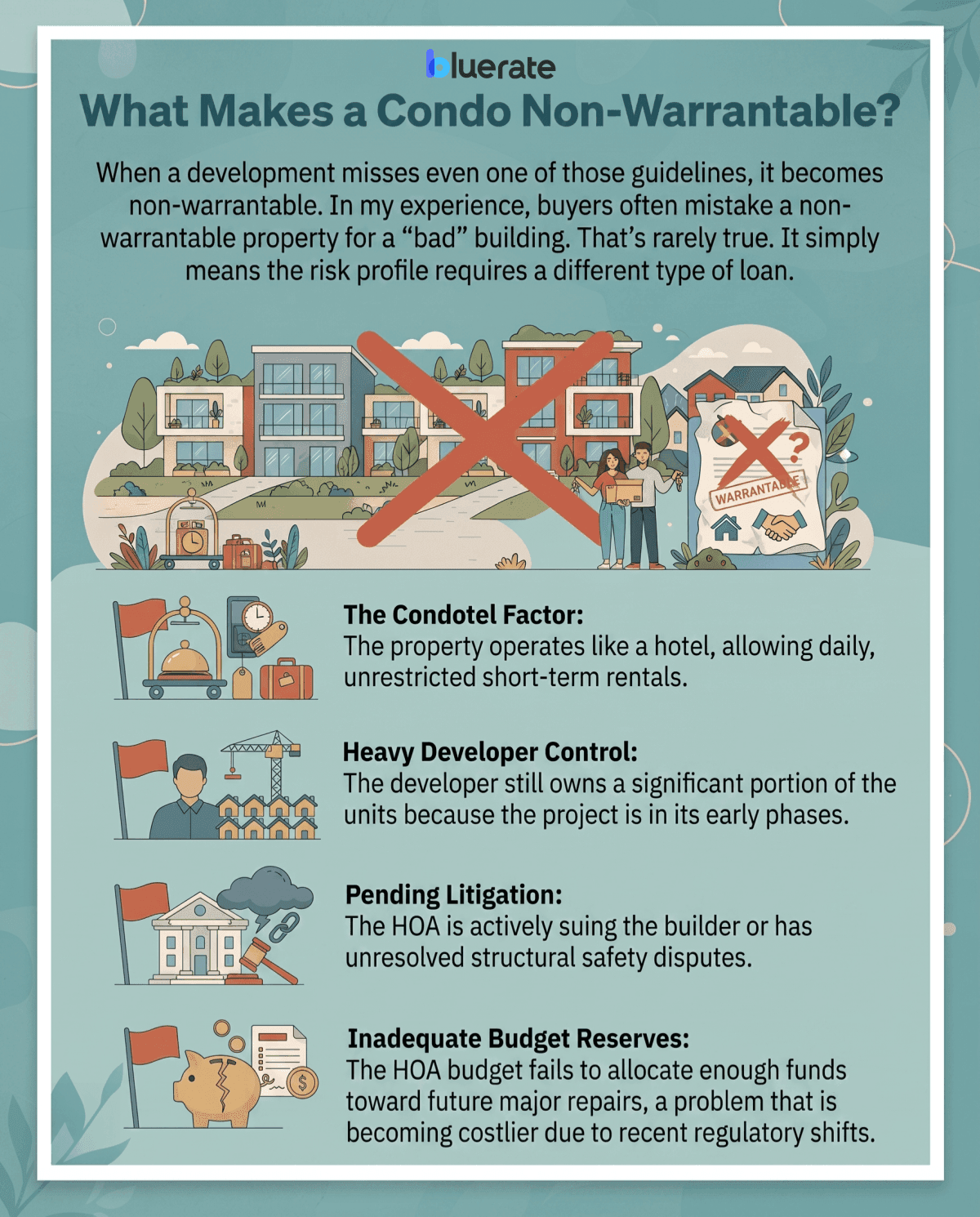

When a development misses even one of those guidelines, it becomes non-warrantable. In my experience, buyers often mistake a non-warrantable property for a "bad" building. That's rarely true. It simply means the risk profile requires a different type of loan.

Here are the most common red flags that trigger this status:

-

The Condotel Factor: The property operates like a hotel, allowing daily, unrestricted short-term rentals.

-

Heavy Developer Control: The developer still owns a significant portion of the units because the project is in its early phases.

-

Pending Litigation: The HOA is actively suing the builder or has unresolved structural safety disputes.

-

Inadequate Budget Reserves: The HOA budget fails to allocate enough funds toward future major repairs, a problem that is becoming costlier due to recent regulatory shifts.

Warrantable vs. Non-Warrantable Condos

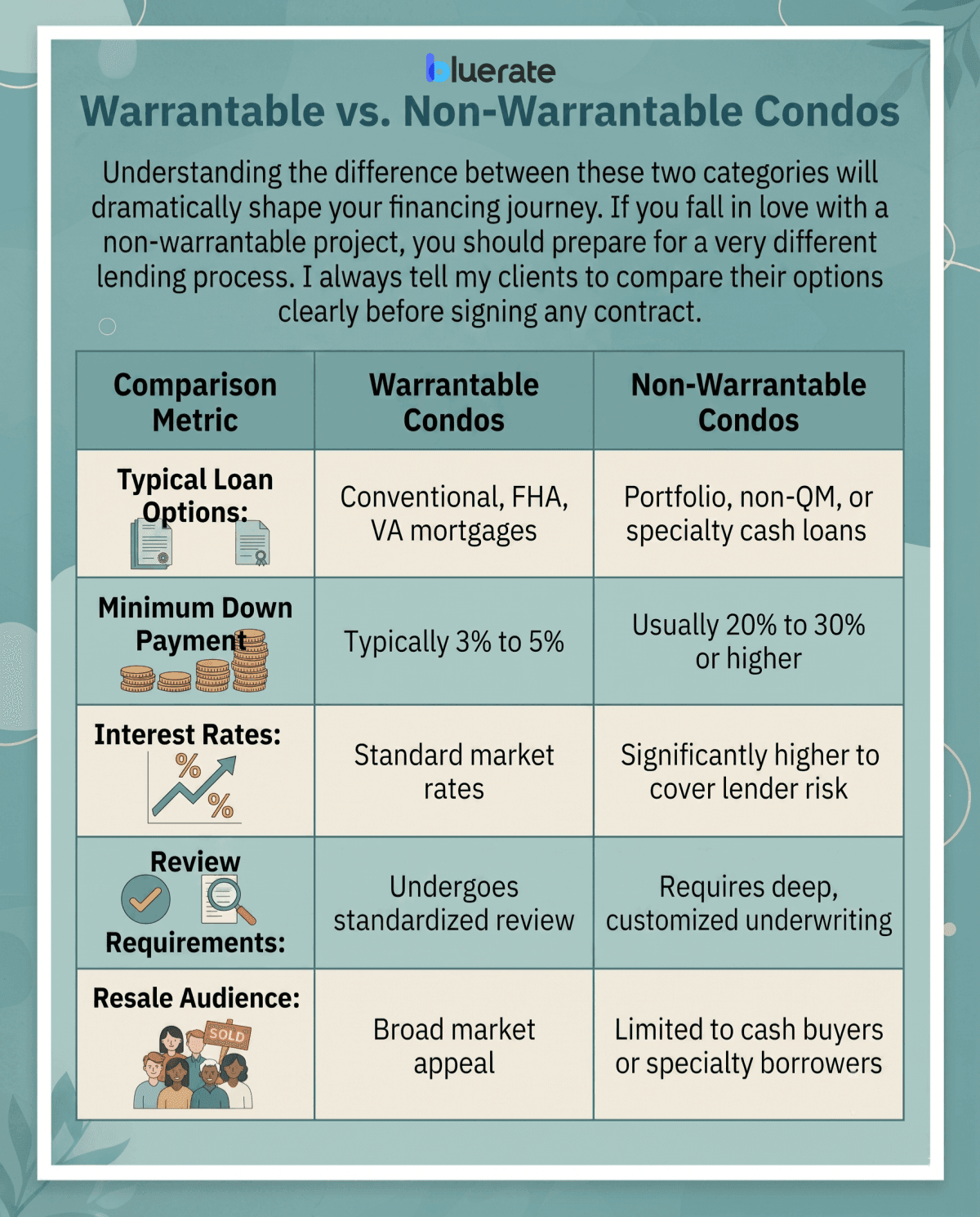

Understanding the difference between these two categories will dramatically shape your financing journey. If you fall in love with a non-warrantable project, you should prepare for a very different lending process. I always tell my clients to compare their options clearly before signing any contract.

Here is how they typically stack up side-by-side:

FAQs About a Warrantable Condo

Q1. How do I find out if a condo is warrantable?

You cannot just look up a public directory, but you can check with your lender. Lenders use database tools like Fannie Mae's Condo Project Manager (CPM) to verify eligibility. I always advise asking the HOA board for their "Condo Questionnaire" early on. This document contains all the necessary financial and owner occupancy data your mortgage lender needs to make a final determination.

Can you get a mortgage on a non-warrantable condo?

Yes, but you will not qualify for a standard conventional loan. You must seek out specialty mortgage options, often called non-QM (non-qualified mortgage) or portfolio loans. Private lenders hold these loans on their own books instead of selling them, meaning they can accept higher risks, though they will require a larger down payment and a higher interest rate.

Does FHA approval mean a condo is warrantable?

Not automatically. FHA and conventional guidelines are separate. While a condo might meet FHA standards and appear on the HUD approved list, it still must pass Fannie Mae or Freddie Mac reviews to be considered warrantable. I recommend working with a mortgage broker who can run both reviews simultaneously to avoid surprises before your closing date.

Why do lenders care about pending litigation in a condo?

Lenders view litigation as a massive financial threat. If a condo board is suing a builder over structural defects, or if a resident is suing the HOA, it could lead to skyrocketing dues or expensive "special assessments." If the association's finances collapse, your property value drops, which directly increases the bank's risk of losing money on your mortgage.

Can a non-warrantable condo become warrantable later?

Absolutely. Condos shift status frequently. If a non-warrantable rating was triggered by active litigation, resolving the lawsuit can restore its warrantability. Similarly, if the HOA increases its annual reserve allocation to the required threshold or if the developer hands over full control to the residents, the project can be re-evaluated and approved for conventional financing.

Conclusion

Navigating condo financing does not have to be overwhelming, but it requires a highly proactive approach. Understanding whether a project is warrantable before falling in love with a unit saves you time, money, and emotional stress.

In my experience, partnering with an experienced real estate agent and a specialized mortgage lender early in the house-hunting process is the best way to safeguard your investment and secure the best possible loan terms. Always ask for the condo's financial health upfront.

Get in contact to local vetted LOs on Bluerate for free.