USDA Loan vs FHA Loan: Which is Your Best Fit?

So, you are finally ready to buy a home, but saving for a massive down payment feels impossible. If you are stuck choosing between a USDA loan and an FHA loan, you're not alone. Both of these government-backed mortgages are incredibly friendly to buyers with limited cash or moderate incomes.

But which one is the absolute best fit for your financial situation? In my experience helping homebuyers, making the right choice could save you thousands. Let's break down the exact rules, costs, and benefits of each.

Key Takeaways

- USDA loans are ideal for buyers looking for a zero down payment option in qualifying suburban or rural areas, provided they meet strict income limits.

- FHA loans offer unmatched flexibility for borrowers with lower credit scores (down to 500) and have no geographic or income restrictions.

- While FHA requires a 3.5% minimum down payment, USDA offers 100% financing.

- FHA loans carry higher long-term mortgage insurance costs compared to USDA guarantee fees.

What is a USDA Loan?

A USDA loan is a government-backed mortgage supported by the U.S. Department of Agriculture. It is specifically designed to make homeownership accessible for low- to moderate-income households purchasing property in eligible suburban and rural regions.

The biggest misconception I hear from buyers is that you must buy a working farm to qualify. That is entirely false! Many quiet suburbs sitting just outside major cities are fully eligible.

Here are the core requirements to keep in mind:

- 0% Down Payment: You can finance 100% of the home's purchase price.

- Location Requirement: The home must be located in a USDA-eligible designated area.

- Income Limit: Your total household income cannot exceed 115% of the area median income (AMI).

- Credit Score Preference: While there is no hard legal minimum, most lenders strongly prefer a 640+ credit score for an automated system approval.

What is an FHA Loan?

An FHA loan is insured by the Federal Housing Administration. It was created to lower the barriers to homeownership, particularly for first-time homebuyers or those who might not have a spotless financial history.

Unlike conventional mortgages that often demand hefty down payments and pristine credit, the FHA program is incredibly forgiving. It is heavily utilized by buyers who want to purchase a home in city centers or urban environments where USDA loans simply aren't allowed.

To qualify for an FHA mortgage, you'll need to meet these basic standards:

- Minimum 3.5% Down Payment: A small hurdle compared to the traditional 20% standard.

- Credit Score Flexibility: You only need a 580 credit score to qualify for the 3.5% down option. If your score falls between 500 and 579, you can still get approved with a 10% down payment.

- No Geographic Restrictions: You can buy a house in any US city, suburb, or rural county.

- No Strict Income Limits: You can earn a high salary and still utilize this program.

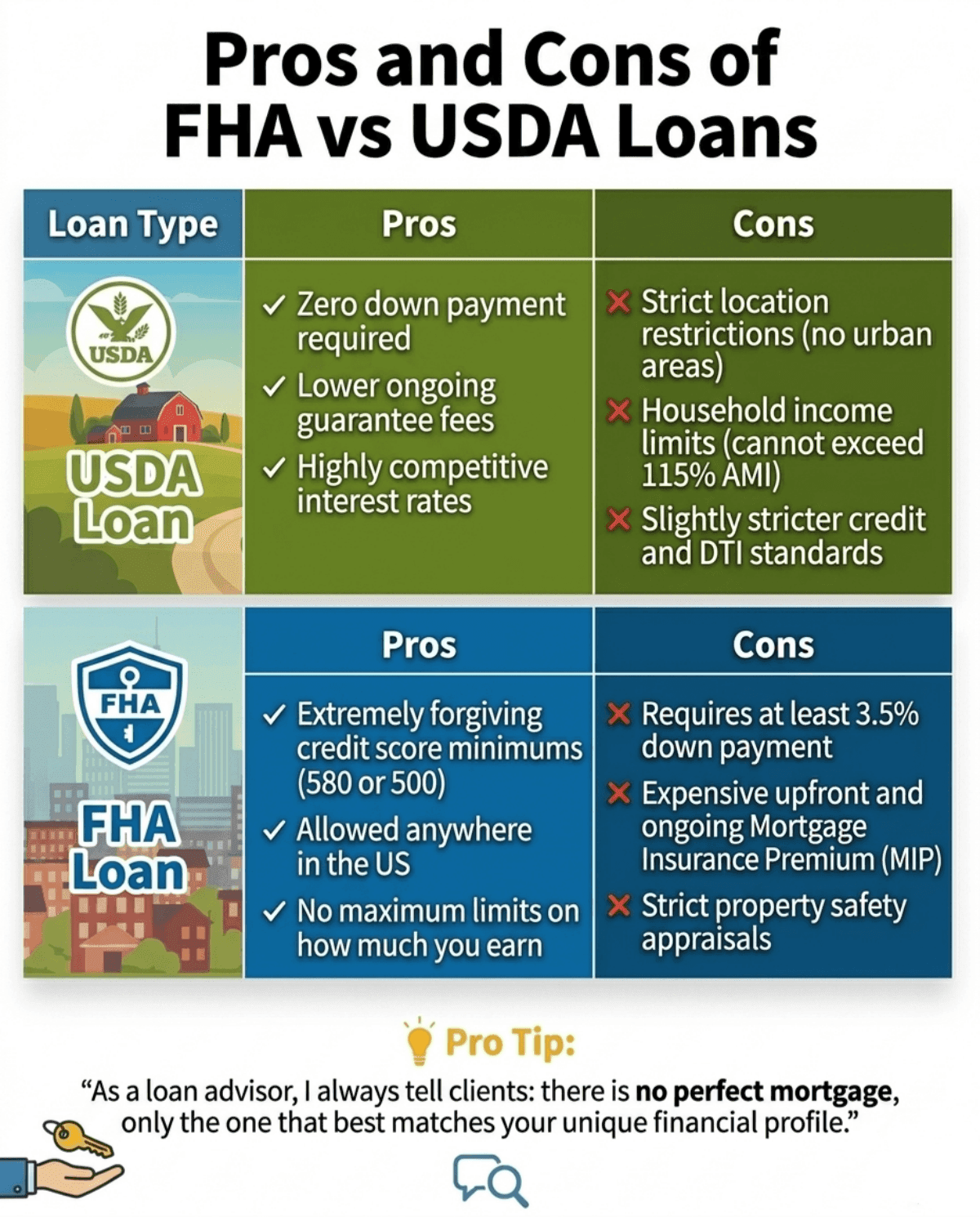

Pros and Cons of FHA vs USDA Loans

As a loan advisor, I always tell clients: there is no perfect mortgage, only the one that best matches your unique financial profile. Let's look at the trade-offs.

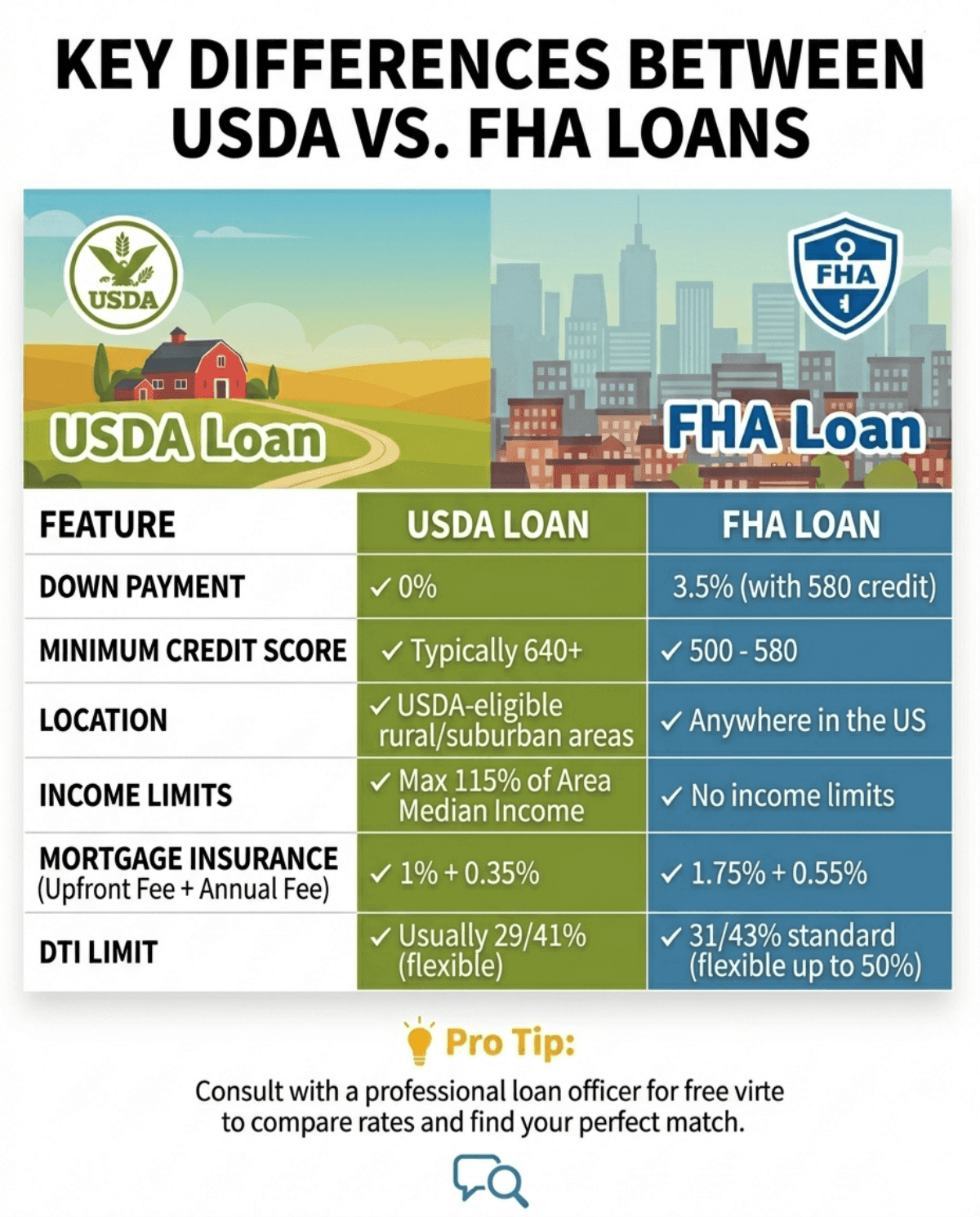

Key Differences Between USDA vs. FHA Loans

To give you a clear perspective, here is a quick look at how these two programs stack up against each other across the most critical lending categories. Let's dive deeper into what these metrics actually mean for you.

Down Payment

The most striking difference between the two is the initial cash required to close. USDA loans are one of the last remaining 100% financing options on the market, meaning a strict 0% down payment. If your savings account is completely depleted but you have steady income, USDA is an absolute lifesaver.

On the flip side, an FHA loan requires a minimum investment of 3.5%. While this isn't zero, it is still highly manageable. For a $300,000 home, you're looking at a $10,500 down payment. The benefit here is that if you can scrape together that 3.5% (even through a verified gift from a family member), the FHA program opens up a much wider pool of eligible properties without the strict zoning rules USDA enforces.

Location

Where do you want to live? Your answer might make this decision for you. FHA mortgages have absolutely no geographic restrictions. You can use one to buy a condo in downtown Chicago or a single-family house in a bustling Miami suburb.

USDA loans, however, are geographically locked. The property must sit within an approved rural or suburban zone mapped out by the US Department of Agriculture. Before you fall in love with a listing, I highly recommend checking the official USDA eligibility map online. Type in the exact property address to see if it qualifies. You might be surprised to find that many sprawling neighborhoods just a few miles outside major city limits perfectly fit the USDA's definition of "rural."

Income Limits

Income caps are where many middle-class buyers hit a wall with USDA financing. Because the program specifically targets low-to-moderate-income families, your total household income (for applicants, typically including spouse and dependents) cannot exceed 115% of the area median income (AMI). The underwriter reviews income from all applicants on the loan, not non-applicant adults in the home.

FHA loans are far less restrictive. Whether you make $40,000 a year or $400,000 a year, the FHA does not care. There are no income limits whatsoever. As long as you have the ability to repay the debt, high earners who happen to have low credit scores can easily lean on an FHA mortgage to secure a home.

Costs & Mortgage Insurance

Both programs charge fees to protect the lender if you default, but the pricing structures are very different.

With a USDA loan, you will pay an upfront Guarantee Fee of 1% (usually rolled into the loan) and an annual fee of 0.35%.

FHA loans hit your wallet a bit harder. They charge a hefty 1.75% Upfront Mortgage Insurance Premium (MIP), plus an annual MIP that typically sits around 0.55% for most 30-year loans (though it can range from 0.15% to 0.75% depending on your down payment).

Because the USDA's ongoing 0.35% fee is significantly cheaper than the FHA's standard 0.55% rate, a USDA mortgage usually results in a notably lower monthly payment over the life of your loan.

Also Read: PMI vs MIP: All the Differences Explained

Credit Score

If your credit history has a few bruises, you need to pay close attention here. The FHA is incredibly accommodating. You can secure a 3.5% down payment with a FICO score as low as 580. If your score is between 500 and 579, you aren't necessarily disqualified. You'll just need to bring a 10% down payment to the table.

The USDA does not officially publish a statutory minimum credit score, but getting approved with poor credit is remarkably tough. In practice, lenders utilize the Guaranteed Underwriting System (GUS). To get an automated, streamlined approval, you typically need a score of at least 640. Anything below that requires manual underwriting, which is a rigorous, deeply scrutinizing process that many buyers struggle to pass.

Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is the percentage of your gross monthly income that goes toward paying debts. This is a critical metric for lenders.

USDA guidelines are notoriously conservative. They generally cap your housing expense ratio (front-end) at 29% and your total debt ratio (back-end) at 41%. You might stretch this slightly if you have strong compensating factors like excellent credit or large cash reserves, but it's difficult.

FHA loans are much more forgiving when it comes to debt. The standard baseline is 31/43%, but automated FHA approval can frequently accept a back-end DTI of up to 50% if you have decent credit or extra savings. If you carry heavy student loans or auto debts, FHA will likely be the path of least resistance.

Appraisal & Property Standards

Both loans require the home to be "Safe, Sound, and Secure." The appraiser isn't just checking the property's value. They are ensuring it meets strict government habitability standards.

For an FHA loan, the appraiser will flag safety hazards like peeling lead-based paint, leaky roofs, or exposed wiring. The seller must fix these issues before the loan can close.

USDA appraisals check for those exact same safety elements, but they carry an extra restriction: USDA appraisals check for those exact same safety elements, but carry an extra restriction: the property must be primarily for your personal residential use and cannot generate significant income (e.g., no large-scale commercial farms. Small accessory farms or multi-unit properties OK if you occupy one unit). It must be strictly for your primary residential use.

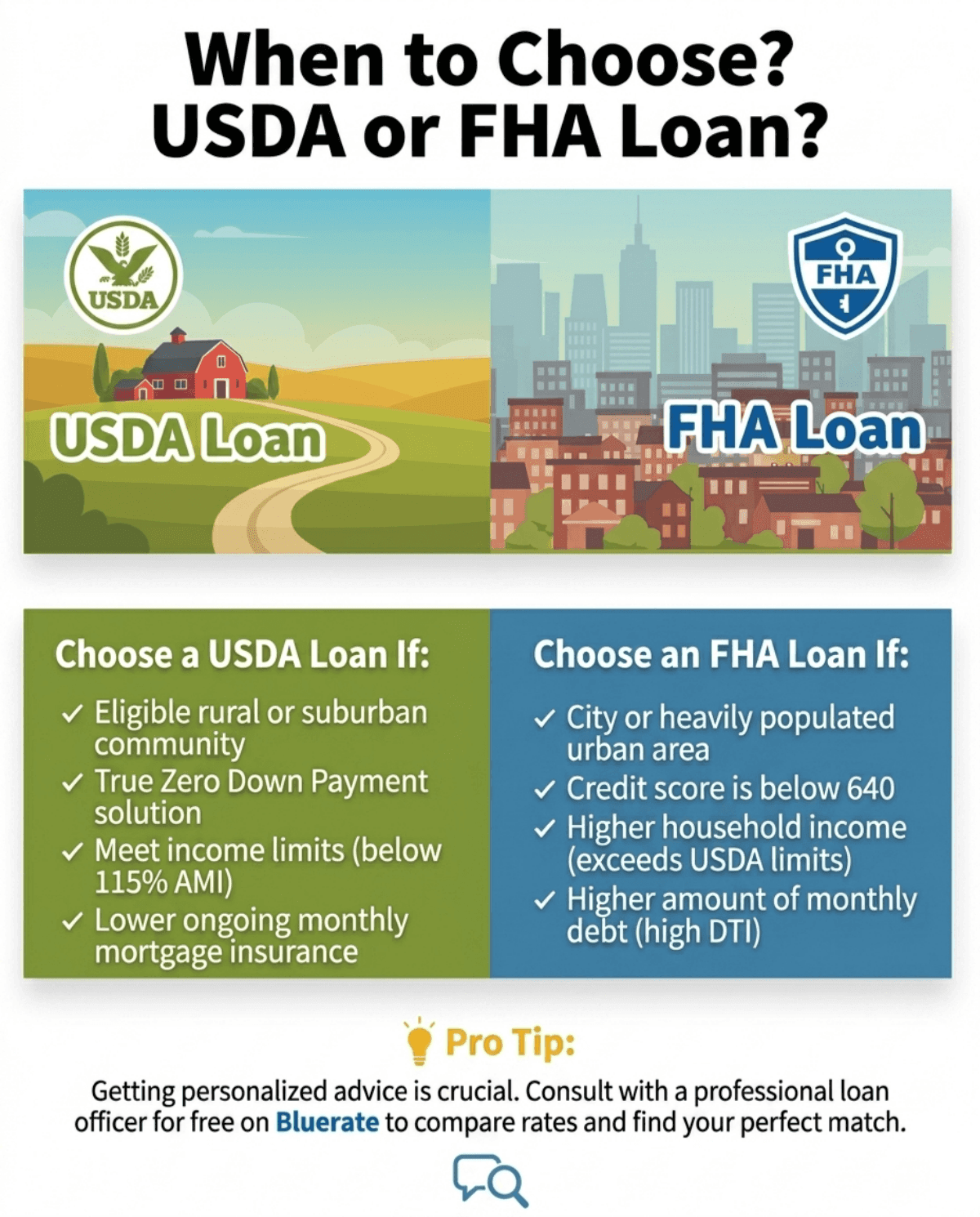

When to Choose? USDA or FHA Loan?

Making the final call comes down to your current cash reserves, where you plan to live, and your financial past. Here is a quick cheat sheet to help you decide:

Choose an FHA loan if:

- You want to buy a house in a city or a heavily populated urban area.

- Your credit score is below 640.

- Your total household income exceeds the strict USDA regional limits.

- You carry a higher amount of monthly debt (high DTI).

Choose a USDA loan if:

- You are buying a property in an eligible rural or suburban community.

- You want a true zero down payment solution.

- You meet the 115% AMI income requirements.

- You want to keep your ongoing monthly mortgage insurance costs as low as possible.

💡 Pro Tip: Still unsure which loan type aligns with your financial goals? Getting personalized advice is crucial. You can consult with a professional loan officer for free on Bluerate to compare rates and find the perfect match for your situation.

FAQs About USDA Loan vs FHA Loan

Q1. What is the disadvantage of USDA loans?

The main disadvantages are geographic and income limitations. You can only purchase homes in USDA-approved rural or suburban areas. Furthermore, high-income earners are entirely disqualified because your total household income cannot legally exceed 115% of the area's median income.

Q2. Is a USDA loan considered an FHA loan?

No, they are entirely different government-backed programs. A USDA loan is supported by the U.S. Department of Agriculture, targeting rural and suburban development. An FHA loan is insured by the Federal Housing Administration, focusing on making homeownership accessible regardless of location.

Q3. Is USDA stricter than FHA?

Yes, USDA is generally stricter. While FHA allows higher debt-to-income ratios and accepts credit scores down to 500, USDA heavily prefers credit scores of 640 or higher, enforces strict property location mapping, and rigidly caps your maximum household income.

Q4. What is better, FHA or USDA?

Neither is universally better. If you have lower credit or want to live in the city, FHA is the superior choice. If you want to avoid a down payment, save money on monthly insurance fees, and prefer a suburban setting, USDA is hands-down the winner.

Q5. Why would someone want a USDA loan?

Buyers want USDA loans because it is one of the only 100% financing (zero down payment) options left on the market, alongside the VA loan. Additionally, its upfront and annual guarantee fees are significantly cheaper than FHA mortgage insurance, saving buyers money monthly.

Conclusion

When comparing a USDA loan versus an FHA loan, your final choice ultimately hinges on your specific housing goals. FHA mortgages win the flexibility game, offering a lifeline to buyers with lower credit scores and those who wish to purchase in urban environments. USDA mortgages, on the other hand, provide an unbeatable zero-down-payment advantage and lower monthly fees, provided you meet the geographic and income criteria.

As a mortgage expert, I know that running these numbers alone can feel incredibly stressful. Navigating the homebuying process shouldn't have to be overwhelming. Let the professionals help you evaluate your unique scenario. Visit Bluerate.ai today to connect with top-rated loan officers, get tailored advice, and confidently take the next step toward your dream home.